Download presentation

Presentation is loading. Please wait.

1

Topic # 03 TVM Effective Annual Rate and Annuities Senior Lecturer

Ayesha Saimoon BBA, MBA(Finance), DU Senior Lecturer

, DU. Senior Lecturer.")

2

What is Time value of money?

Time value of money refers to the fact that the same money return has a higher present value if it is to be received early that it is to be received later. Time value of money means that the value of a sum of money received today is more than its value received after some time. Conversely, the sum of money received in future is less valuable in the future. The time value of money is one of the most important concepts in finance. Money that the firm has in its possession today is more valuable than future payments because the money it now has can be invested and earn positive returns. Money received now can be invested to earn additional cash (interest). Most financial decisions involve costs and benefits that are spread out over time. Time value of money allows comparison of cash flows from different periods.

. Most financial decisions involve costs and benefits that are spread out over time. Time value of money allows comparison of cash flows from different periods.")

3

Time Value Terminology

Future value (FV) is the amount an investment is worth after one or more periods. Present value (PV) is the current value of future cash flows of an investment.. Another way to think of present value is to adopt a stance out on the time line in the future and look back toward time 0 to see what was the beginning amount. Simple interest refers to interest earned only on the original capital investment amount. Compound interest refers to interest earned on both the initial capital investment and on the interest reinvested from prior periods. Compounding is the process of finding FV Discounting is the process of finding PV The nominal interest rate (NIR) is the interest rate expressed in terms of the interest payment made each period. The effective annual interest rate (EAR) is the interest rate expressed as if it was compounded once per year.

is the amount an investment is worth after one or more periods. Present value (PV) is the current value of future cash flows of an investment.. Another way to think of present value is to adopt a stance out on the time line in the future and look back toward time 0 to see what was the beginning amount. Simple interest refers to interest earned only on the original capital investment amount. Compound interest refers to interest earned on both the initial capital investment and on the interest reinvested from prior periods. Compounding is the process of finding FV. Discounting is the process of finding PV. The nominal interest rate (NIR) is the interest rate expressed in terms of the interest payment made each period. The effective annual interest rate (EAR) is the interest rate expressed as if it was compounded once per year.")

4

Time Line. A horizontal line on which time zero appears at the leftmost end and future periods are marked from left to right; can be used to depict investment cash flows is called time line.

5

Future Value of a Single Sum

or Total Compound Interest = FV – PV Simple Interest = (PV)(i)(n) Interest Difference = Compound Interest – Simple Interest FV = Future Value n = Number of Year (Period) i = rate of return (interest) m = Number of periods in a Year (1 + i)n = future value interest factor (FVIF).

(i)(n) Interest Difference = Compound Interest – Simple Interest. FV = Future Value. n = Number of Year (Period) i = rate of return (interest) m = Number of periods in a Year. (1 + i)n = future value interest factor (FVIF).")

6

01. What’s the FV of an initial $100 after 3 years if i = 10%?

FV Practice 01. What’s the FV of an initial $100 after 3 years if i = 10%? FV3 = PV(1 + i)3 = $100(1.10)3 = $ Compound Interest = FV – PV = $ $ 100 = $ 33.10 02. How much total compound interest will be taken after 03 years?. 03. What will $1 000 amount to in 5 years’ time if interest is 12% per annum, compounded annually? 04. What will $1 000 amount to in 5 years’ time if interest is 12% per annum, compounded monthly?

3. = $100(1.10)3 = $ Compound Interest = FV – PV. = $ $ 100. = $ How much total compound interest will be taken after 03 years What will $1 000 amount to in 5 years’ time if interest is 12% per annum, compounded annually 04. What will $1 000 amount to in 5 years’ time if interest is 12% per annum, compounded monthly")

7

Future Value: Practice Problems

01. Jane Farber places $800 in a savings account paying 6% interest compounded annually. She wants to know how much money will be in the account at the end of 5 years. $ 02. You deposit $1,000 now, $1,500 in one year, $2,000 in two years and $2,500 in three years in an account paying 10% interest per annum. How much do you have in the account at the end of the third year? Tips: You can solve it by: calculate the future value of each cash flow first and then total them. $7846

8

Finding The Interest Rate (Rate of Return)

Problem: Abir Hasan, who recently won $ 10,000 in the lottery, wants to buy a car in 5 years. Abir estimates that the car will cost $ 16,105 at that time. What interest rate must he earn to be able to afford the car?

9

01. What’s the PV of $100 due in 3 years if i = 10%?

Present Value or 01. What’s the PV of $100 due in 3 years if i = 10%? 02. How much would you have to deposit now to have $15,000 in 8 years if interest is 7%?

10

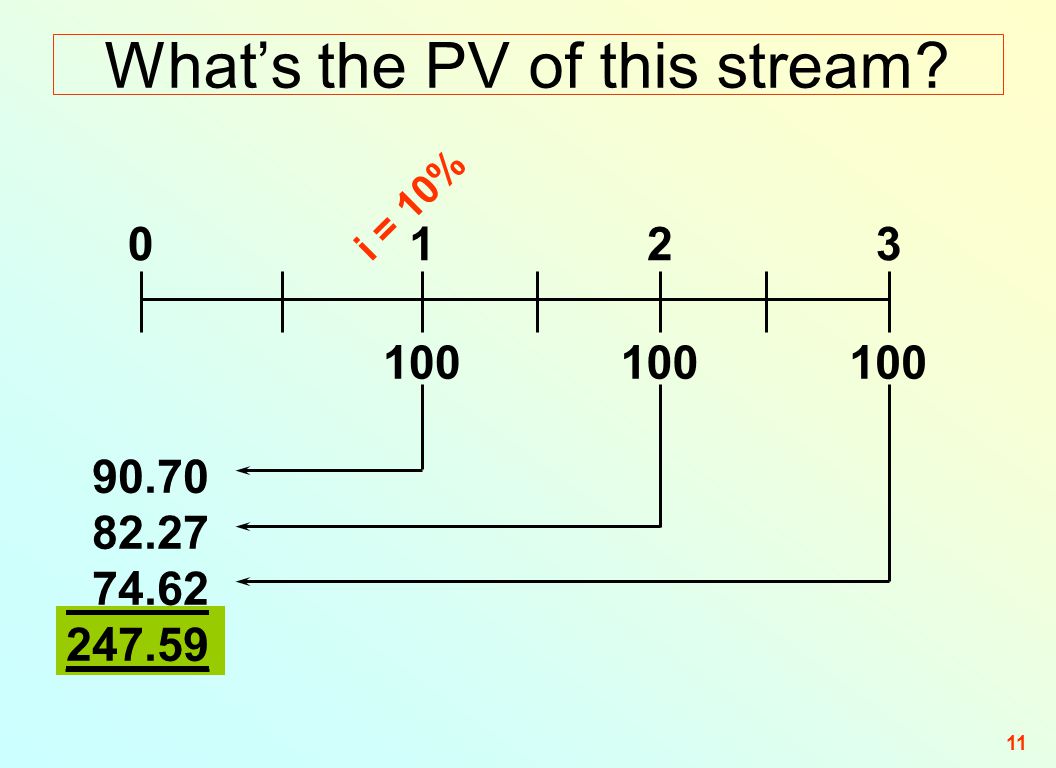

What’s the PV of this stream?

1 2 3 1500 2000 2500 1364 1653 1878 $4 895

11

What’s the PV of this stream?

1 2 3 100 100 100 90.70 82.27 74.62 247.59

12

Present Value of Multiple Cash Flows

You will get $1 500 in one year, $2000 in two years and $2 500 in three years in an account paying 10% interest per annum. What is the present value of these cash flows? Tips: You can solve by either: discounting back one year at a time; or calculating the present value of each cash flow first and then total them.

13

Effective Annual Interest Rate (EAR)

The annual rate of interest actually paid or earned is called Effective Annual Rate (EAR). Example 01: Find out the EAR for a nominal rate of 10%, compounded semiannually?

. Example 01: Find out the EAR for a nominal rate of 10%, compounded semiannually")

14

Example 02: Comparing EARs

Consider the following interest rates quoted by three banks: Bank A: 15%, compounded daily (365 or 360 days in a year) Bank B: 15.5%, compounded quarterly Bank C: 16%, compounded annually Which is the best bank? For a saver, Bank B offers the best (highest) interest rate. For a borrower, Bank C offers the best (lowest) interest rate. The highest NIR (Nominal Interest Rate) is not necessarily the best. Compounding during the year can lead to a significant difference between the NIR and the EAR.

Bank B: 15.5%, compounded quarterly. Bank C: 16%, compounded annually. Which is the best bank For a saver, Bank B offers the best (highest) interest rate. For a borrower, Bank C offers the best (lowest) interest rate. The highest NIR (Nominal Interest Rate) is not necessarily the best. Compounding during the year can lead to a significant difference between the NIR and the EAR.")

15

Practice 01: EAR What is the Effective Annual INTEREST rate (EAR) for a sum of money compounded at the rate of 15% pa On a quarterly basis? On a monthly basis? On a weekly basis? On a daily basis? On a continuous basis? Assume a 360 day year.

16

Practice 02: TVM and EAR Delia Martin has $10000 that she can deposit in any of three accounts for a 3-year period. Bank A compounds interest on an annual basis, bank B compounds interest twice each year, and Bank C compounds interest each quarter. All three banks have a stated annual interest rate of 4%. What amount would Ms. Martin have at the end of the third year, leaving all interest paid on deposit, in each Bank? What effective annual rate (EAR) would she earn in each of the banks? On the basis of your findings in parts 01 and 02, which bank should Ms. Martin deal with? Why? If a fourth bank (Bank D), also with a 4% stated interest rate, compounds interest continuously, how much would Ms. Martin have at the end of the third Year? Does this alternative change your recommendation in part c? Explain why or why not.

would she earn in each of the banks On the basis of your findings in parts 01 and 02, which bank should Ms. Martin deal with Why If a fourth bank (Bank D), also with a 4% stated interest rate, compounds interest continuously, how much would Ms. Martin have at the end of the third Year Does this alternative change your recommendation in part c Explain why or why not.")

17

Annuities An annuity is a series of equal, periodic payments. Followings are the types of annuities: Ordinary Annuity: An ordinary annuity is a series of constant cash flows that occur at the end of each period for some fixed number of periods. Examples include consumer loans and home mortgages. Annuity Due: An annuity for which the cash flow occurs at the beginning of each period is called Annuity Due. Perpetuity: A perpetuity is an annuity in which the cash flows continue forever. Preparation at Home: What are the differences between Ordinary annuity and Annuity Due? Which annuity gives the higher value?

18

Present Value of An Ordinary Annuity

Present Value of An Annuity Due The discounting term is called the present value interest factor for annuities (PVIFA).

.")

19

Examples Examples 03. What is the present value of an ordinary annuity of $100 per year at 12% per annum for three years? Examples 04. You borrow $7 500 to buy a car and agree to repay the loan by way of equal monthly repayments over 5 years. The current interest rate is 12% per annum, compounded monthly. What is the amount of each monthly repayment?

20

Practice 03: Present Value of Annuity (from the Text)

For each case in the following table, answer the following questions that Follow: Case Amount of Annuity Interest rate Year A 2500 8% 10 B 500 12% 6 C 30000 20% 5 D 11500 9% 8 E 6000 14% 30 Calculate the Present value of the annuity assuming that it is An Ordinary annuity An Annuity Due Compare the findings in part (a) and (b). All else being identical, which type of annuity is preferable? Explain Why?

and (b). All else being identical, which type of annuity is preferable Explain Why")

21

Practice 04 : Finding the Periodic Payment (PMT)

Suppose you borrow $100,000 to buy a new house. If the mortgage interest rate is 8% on a 15-year mortgage, how much would your MONTHLY payments (Installment) be? A. $ B. $ C. $ D. $980.55 $955.66

be A. $ B. $ C. $ D. $ $")

22

Multiple Period In A Year

Examples 05: What is the present value of an ordinary annuity of $50 paid every 6 months at 12% per annum for 3 years? A. $ B. $ C. $ D. $279.12 Examples 06: You will receive $500 at the end of each of the next 5 years. The current interest rate is 9% per annum. What is the present value of this series of cash flows?

23

Future Value of An Annuity

The compounding term is called the future value interest factor for annuities (FVIFA).

.")

24

Examples of Future Value of Annuity

Example 07: What is the future value at the end of 3 years of an ordinary annuity of $100 at 12% per annum? A. $ B. $ C. $ D. $377.93 Example 08: What is the future value $200 deposited at the end of every year for 10 years if the interest rate is 6% per annum?

25

Practice 05: Future Value of Annuity )from the Text)

For each case in the following table, answer the following questions that Follow: Case Amount of Annuity Interest rate Year A 2500 8% 10 B 500 12% 6 C 30000 20% 5 D 11500 9% 8 E 6000 14% 30 Calculate the future value of the annuity assuming that it is An Ordinary annuity An Annuity Due Compare the findings in part (a) and (b). All else being identical, which type of annuity is preferable? Explain Why?

and (b). All else being identical, which type of annuity is preferable Explain Why")

26

Practice 06: Future Value of Annuity (from the Text)

Ramesh Abdul wishes to choose the better of two equally costly cash flow streams: annuity X and annuity Y. X is an annuity due with a cash inflow of $9,000 for each of 6 years. Y is an ordinary annuity with a cash inflow of $10,000 for each of 6 years. Assume that Ramesh can earn 15% on his investments. On a purely subjective basis, which annuity do you think is more attractive? Why? Find the future value at the end of year 6, FVA6, for both annuity X and annuity Y. Use your finding in part b to indicate which annuity is more attractive. Why? Compare your finding to your subjective response in part a.

27

Practice 07: Present Value of A Retirement Annuity

An insurance agent is trying to sell you an immediate-retirement annuity, which for a single amount paid today will provide you with $12,000 at the end of each year for the next 25 years. You currently earn 9% on low-risk investments comparable to the retirement annuity. Ignoring taxes, what is the most you would pay for this annuity? $117,870.96

28

Practice 08: Future Value Of A Retirement Annuity

To supplement your planned retirement in exactly 42 years, you estimate that you need to accumulate $220,000 by the end of 42 years from today. You plan to make equal annual end-of-year deposits into an account paying 8% annual interest. a. How large must the annual deposits be to create the $220,000 fund by the end of 42 years? b. If you can afford to deposit only $600 per year into the account, how much will you have accumulated by the end of the 42nd year? PMT = $723.10 FVAn = $182,546.40

29

Growing Annuity & Growing Perpetuity

A growing stream is one in which each successive cash flow is larger than the previous one. A common problem is one in which the cash flows grow by some fixed percentage A growing annuity is an annuity in which the cash flows grow at a constant rate g: A growing perpetuity is an annuity where the cash flows continue indefinitely:

30

Types of Loans A pure discount loan is a loan where the borrower receives money today and repays a single slump sum in the future. An interest only loan requires the borrower to pay interest each period and to repay the entire principal at some point in the future. An amortized loan requires the borrower to repay both the principal and interest over time.

31

Example: Simple Amortized Loan Schedule

Suppose a business takes out a $5000, five-year loan at 9%. The agreement calls for the borrower to pay the interest on the loan balance each year and to reduce the loan balance each year by $1000. Please make an amortization Schedule. Year Beginning Balance Total Payment Interest Paid Principal Paid Ending Balance 1 $5000 $1450 $450 $1000 4000 2 1360 360 1000 3000 3 1270 270 2000 4 1180 180 5 1090 90 Totals $6350 $1350 $500

32

Practice: Simple Amortized Loan Schedule

Suppose a business takes out a $10000, five-year loan at 10%. The agreement calls for the borrower to pay the interest on the loan balance each year and to reduce the loan balance each year by $2000. Please make an amortization Schedule. Year Beginning Balance Total Payment Interest Paid Principal Paid Ending Balance 1 $10000 $3000 $1000 $2000 8000 2 3 4 5 Totals

Similar presentations

Chapter Six.>")

>")