Download presentation

Presentation is loading. Please wait.

1

Price and Output Determination Under Perfect Competition

2

The concept of perfect competition was first introduced by Adam Smith in his book "Wealth of Nations". Later on, it was improved by Edgeworth. However, it received its complete formation in Frank Kight's book "Risk, Uncertainty and Profit" (1921). Leftwitch has defined market competition in the following words: "Prefect competition is a market in which there are many firms selling identical products with no firm large enough, relative to the entire market, to be able to influence market price". According to Bllas: "The perfect competition is characterized by the presence of many firms. They sell identically the same product. The seller is a price taker".

3

Features or Conditions for Perfect Competition:

(1) Large number of firms. The basic condition of perfect competition is that there are large number of firms in an industry. Each firm in the industry is so small and its output so negligible that it exercises little influence over price of the commodity in the market. A single firm cannot influence the price of the product either by reducing or increasing its output. An individual firm takes the market price as given and adjusts its output accordingly. In a competitive market, supply and demand determine market price. The firm is price taker and output adjuster. (2) Large number of buyers. In a perfect competitive market, there are very large number of buyers of the product. If any consumer purchases more or purchases less, he is not in a position to affect the market price of the commodity. His purchase in the total output is just like a drop in the ocean. He, therefore, too like the firm, is a price taker.

Large number of firms. The basic condition of perfect competition is that there are large number of firms in an industry. Each firm in the industry is so small and its output so negligible that it exercises little influence over price of the commodity in the market. A single firm cannot influence the price of the product either by reducing or increasing its output. An individual firm takes the market price as given and adjusts its output accordingly. In a competitive market, supply and demand determine market price. The firm is price taker and output adjuster. (2) Large number of buyers. In a perfect competitive market, there are very large number of buyers of the product. If any consumer purchases more or purchases less, he is not in a position to affect the market price of the commodity. His purchase in the total output is just like a drop in the ocean. He, therefore, too like the firm, is a price taker.")

4

The product is homogeneous

The product is homogeneous. Another provision of perfect competition is that the good produced by all the firms in the industry is identical. In other words, the cross elasticity between the products of the firm is infinite. No barriers to entry. The firms in a competitive market have complete freedom of entering into the market or leaving the industry as and when they desire. There are no legal, social or technological! barriers for the new firms (or new capital) to enter or leave the industry. Any new firm is free to start production if it so desires and stop production and leave the industry if it so wishes. The industry, thus, is characterized by freedom of entry and exit of firms. (5) Complete information. Another condition for perfect competition is that the consumers and producers possess perfect information about the prevailing price of the product in the market. The consumers know the ruling price, the producers know costs, the workers know about wage rates and so on. In brief, the consumers, the resource owners have perfect knowledge about the current price of the product in the market. A firm, therefore, cannot charge higher price than that ruling in the market. If it does so, its goods will remain unsold as buyers will shift to some other seller. (6) Profit maximization. For perfect competition to exist, the sole objective of the firm must be to get maximum profit.

to enter or leave the industry. Any new firm is free to start production if it so desires and stop production and leave the industry if it so wishes. The industry, thus, is characterized by freedom of entry and exit of firms. (5) Complete information. Another condition for perfect competition is that the consumers and producers possess perfect information about the prevailing price of the product in the market. The consumers know the ruling price, the producers know costs, the workers know about wage rates and so on. In brief, the consumers, the resource owners have perfect knowledge about the current price of the product in the market. A firm, therefore, cannot charge higher price than that ruling in the market. If it does so, its goods will remain unsold as buyers will shift to some other seller. (6) Profit maximization. For perfect competition to exist, the sole objective of the firm must be to get maximum profit.")

5

Distinction Between Pure Competition and Perfect Competitions:

For a pure competition to exist, there are three main requisites, i.e., (1) homogeneity of product (2) large number of firms and (3) ease of entry and exist of firms. A perfect competition, on the other hand, is made up of all the six postulates stated earlier.

homogeneity of product (2) large number of firms and (3) ease of entry and exist of firms. A perfect competition, on the other hand, is made up of all the six postulates stated earlier.")

6

Equilibrium of the Firm: Definition and Explanation of Equilibrium of the Firm:

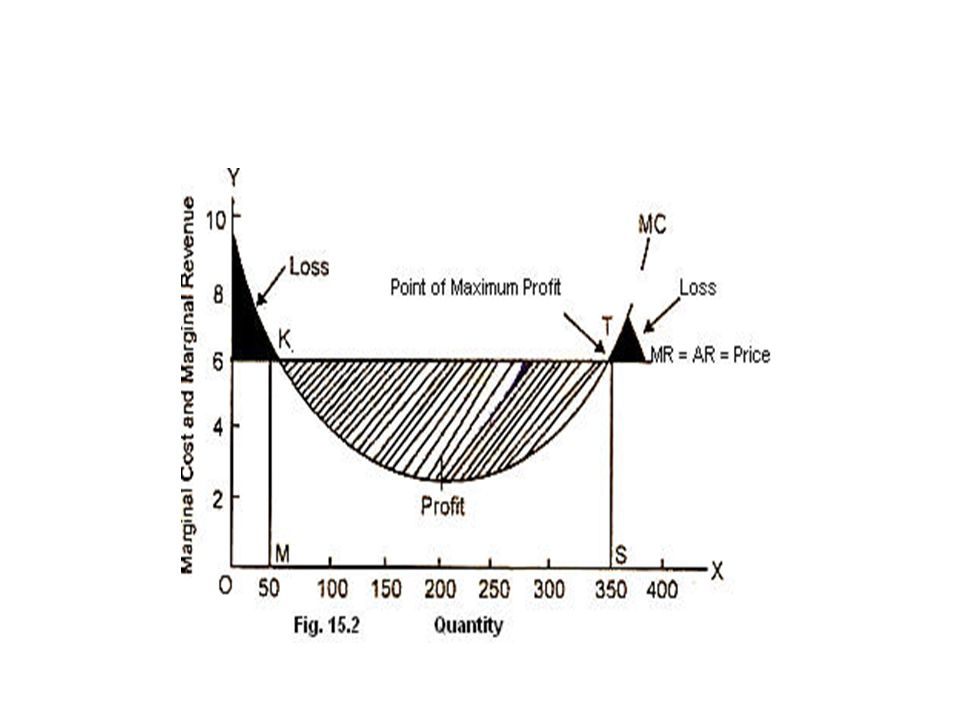

MR = MC (Marginal Revenue = Marginal Cost) Rule:

Rule:")

8

Short Run Equilibrium of the Price Taker Firm: Three cases Super Normal Profits Normal Profits Losses

9

Super Normal Profits

10

Normal Profits

11

Losses

12

Long run equilibrium

Similar presentations

Group Equilibrium Selling.>")

. I. Perfect Competition: A Model A. Basic Definitions 1. Perfect Competition: a model of the market based.>")

products low barriers to entry (free.>")