Download presentation

Presentation is loading. Please wait.

1

12 MONOPOLY CHAPTER

2

Objectives After studying this chapter, you will able to

Explain how monopoly arises and distinguish between single-price monopoly and price-discriminating monopoly Explain how a single-price monopoly determines its output and price Compare the performance and efficiency of single-price monopoly and competition

3

Objectives After studying this chapter, you will able to

Define rent seeking and explain why it arises Explain how price discrimination increases profit Explain how monopoly regulation influences output, price, economic profit, and efficiency

4

Market Power Market power is the ability to influence the market, and in particular the market price, by influencing the total quantity offered for sale. A monopoly is an industry that produces a good or service for which no close substitute exists and in which there is one supplier that is protected from competition by a barrier preventing the entry of new firms.

5

Market Power How Monopoly Arises A monopoly has two key features:

No close substitutes Barriers to entry Legal or natural constraints that protect a firm from potential competitors are called barriers to entry.

6

Market Power There are two types of barriers to entry: legal and natural. Legal barriers to entry create a legal monopoly, a market in which competition and entry are restricted by the granting of a: Public franchise Government license Patent and copyright

7

Market Power Natural barriers to entry create a natural monopoly, which is an industry in which one firm can supply the entire market at a lower price than two or more firms can. Figure 12.1 illustrates a natural monopoly.

9

Market Power One firm can produce 4 units of output at 5 cents per unit. Two firms can produce 4 units—2 units each—at 10 cents per unit. Four firms can produce 4 units—1 unit each—at 15 cents per unit.

11

Market Power Monopoly Price-Setting Strategies

There are two types of monopoly price-setting strategies: Price discrimination is the practice of selling different units of a good or service for different prices. Many firms price discriminate, but not all of them are monopoly firms. A single-price monopoly is a firm that must sell each unit of its output for the same price to all its customers.

12

A Single-Price Monopoly’s Output and Price Decision

Price and Marginal Revenue A monopoly is a price setter, not a price taker like a firm in perfect competition. The reason is that the demand curve for the monopoly’s output is the market demand curve. To sell a larger output, a monopoly must set a lower price.

13

A Single-Price Monopoly’s Output and Price Decision

Total revenue, TR, is the price, P, multiplied by the quantity sold, Q. Marginal revenue, MR, is the change in total revenue that results from a one-unit increase in the quantity sold. For a single-price monopoly, marginal revenue is less than price at each level of output. That is, MR < P

14

A Single-Price Monopoly’s Output and Price Decision

Marginal Revenue and Elasticity A single-price monopoly’s marginal revenue is related to the elasticity of demand for its good: If demand is elastic, a fall in price brings an increase in total revenue.

16

A Single-Price Monopoly’s Output and Price Decision

Marginal Revenue and Elasticity The rise in revenue from the increase in quantity sold outweighs the fall in revenue from the lower price per unit, and MR is positive. Total revenue increases.

18

A Single-Price Monopoly’s Output and Price Decision

If demand is inelastic, a fall in price brings a decrease in total revenue. The rise in revenue from the increase in quantity sold is outweighed by the fall in revenue from the lower price per unit, and MR is negative.

20

A Single-Price Monopoly’s Output and Price Decision

Total revenue decreases.

22

A Single-Price Monopoly’s Output and Price Decision

If demand is unit elastic, a fall in price brings total revenue does not change. The rise in revenue from the increase in quantity sold equals the fall in revenue from the lower price per unit, and MR = 0. Total revenue is maximized when MR = 0.

24

A Single-Price Monopoly’s Output and Price Decision

A single-price monopoly never produces an output at which demand is inelastic. If it did produce such an output, the firm could increase total revenue, decrease total cost, and increase economic profit by decreasing output.

25

A Single-Price Monopoly’s Output and Price Decision

Price and Output Decision The monopoly selects the profit-maximizing level of output in the same manner as a competitive firm, where MR = MC. Table 12.1 provides a numerical example to illustrate the profit-maximizing output and price decision. The monopoly may earn an economic profit, even in the long run, because the barriers to entry protect the firm from market entry by competitor firms.

26

A Single-Price Monopoly’s Output and Price Decision

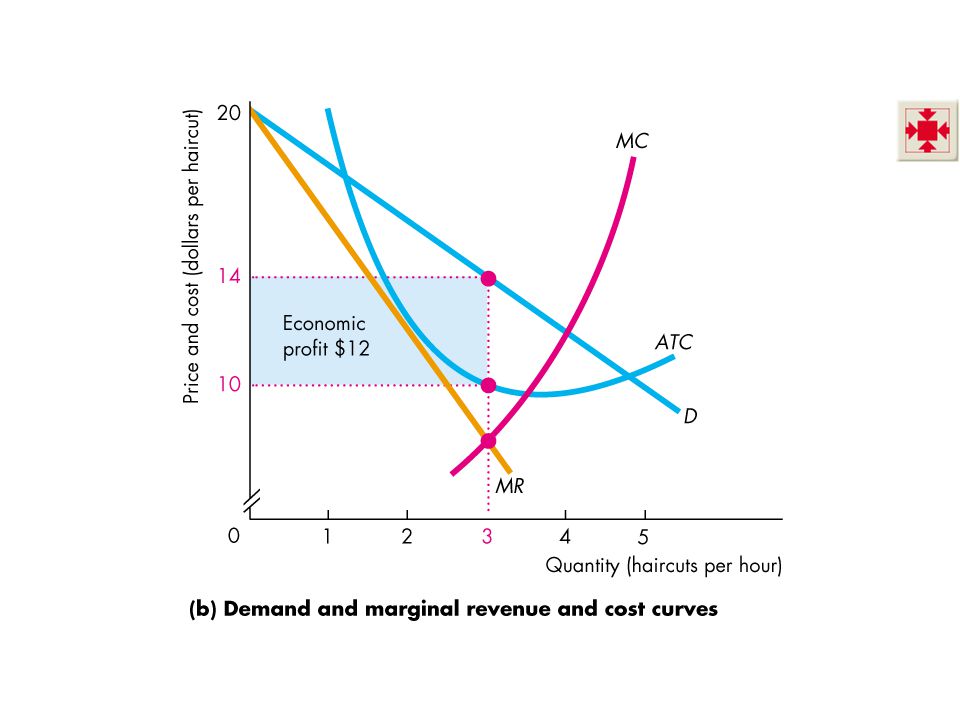

Figure 12.4 illustrates the profit-maximizing choices of a single-price monopolist. In part (a), the monopoly sets the quantity produced at the level that maximizes total revenue minus total cost.

, the monopoly sets the quantity produced at the level that maximizes total revenue minus total cost.")

28

A Single-Price Monopoly’s Output and Price Decision

In part (b), the firm produces the output at which MR = MC and sets the price to sell that quantity. The ATC curve tells us the average cost. The classic monopoly diagram The classic monopoly diagram, Figure 12.4b provides a good opportunity to tell your students about the contribution of one of the most brilliant economists of the 20th century, Joan Robinson. This diagram first appeared in her book, The Economics of Imperfect Competition, published in 1933 when she was just 30 years old. You can learn more about Joan Robinson at (or use the link on the Economics Place Web site). Women are still not attracted to economics on the scale that they’re attracted to most other disciplines. So the opportunity to talk about an outstanding female economist shouldn’t be lost. Joan Robinson was a formidable debater and reveled in verbal battles, a notable one of which was with Paul Samuelson on one of her visits to MIT. Anxious to make and illustrate a point, Samuelson asked Robinson for the chalk. Monopolizing the chalk and the blackboard, the unyielding Robinson snapped, “Say it in words young man.” Samuelson meekly obeyed. This story illustrates Joan Robinson’s approach to economics: work out the answers to economic problems using the appropriate techniques of math and logic, but then “say it in words.” Don’t be satisfied with formal argument if you don’t understand it. Your students will benefit from this story if you can work it into your class time. Economic profit is the profit per unit multiplied by the quantity produced—the blue rectangle.

, the firm produces the output at which MR = MC and sets the price to sell that quantity. The ATC curve tells us the average cost. The classic monopoly diagram. The classic monopoly diagram, Figure 12.4b provides a good opportunity to tell your students about the contribution of one of the most brilliant economists of the 20th century, Joan Robinson. This diagram first appeared in her book, The Economics of Imperfect Competition, published in 1933 when she was just 30 years old. You can learn more about Joan Robinson at (or use the link on the Economics Place Web site). Women are still not attracted to economics on the scale that they’re attracted to most other disciplines. So the opportunity to talk about an outstanding female economist shouldn’t be lost. Joan Robinson was a formidable debater and reveled in verbal battles, a notable one of which was with Paul Samuelson on one of her visits to MIT. Anxious to make and illustrate a point, Samuelson asked Robinson for the chalk. Monopolizing the chalk and the blackboard, the unyielding Robinson snapped, Say it in words young man. Samuelson meekly obeyed. This story illustrates Joan Robinson’s approach to economics: work out the answers to economic problems using the appropriate techniques of math and logic, but then say it in words. Don’t be satisfied with formal argument if you don’t understand it. Your students will benefit from this story if you can work it into your class time. Economic profit is the profit per unit multiplied by the quantity produced—the blue rectangle.")

30

Single-Price Monopoly and Competition Compared

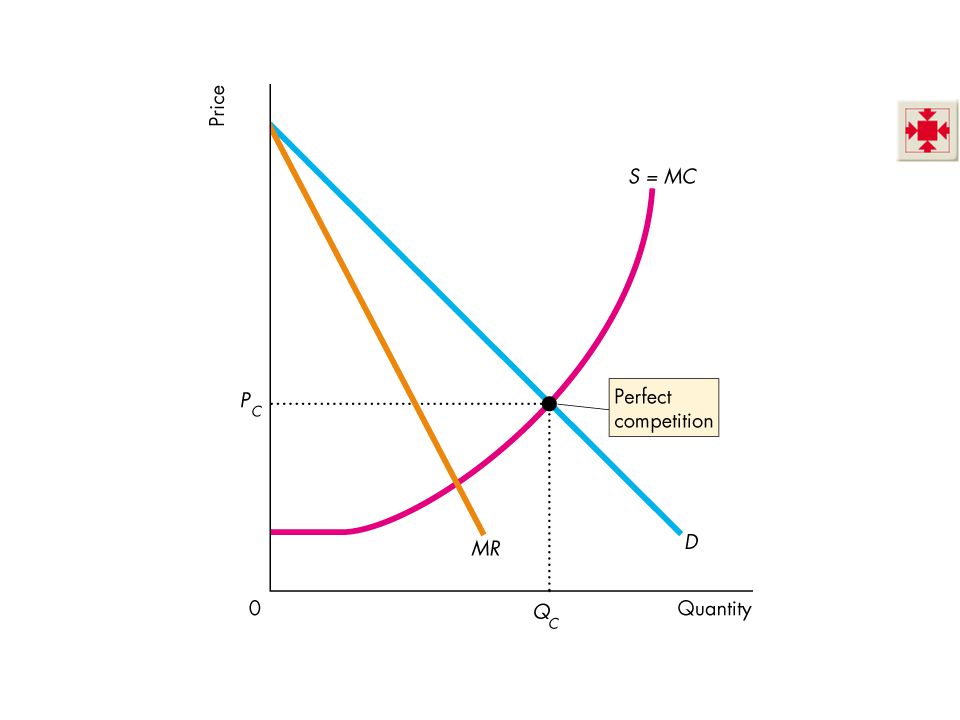

Comparing Output and Price Figure 12.5 compares the price and quantity in perfect competition and monopoly. The market demand curve, D, in perfect competition is the demand curve that the firm faces in monopoly.

32

Single-Price Monopoly and Competition Compared

The market supply curve in perfect competition is the horizontal sum of the individual firm’s marginal cost curves, S = MC. This curve is the monopoly’s marginal cost curve.

34

Single-Price Monopoly and Competition Compared

Equilibrium in perfect competition occurs where the quantity demanded equals the quantity supplied at quantity QC and price PC.

36

Single-Price Monopoly and Competition Compared

Equilibrium output for a monopoly, QM, occurs where marginal revenue equals marginal cost, MR = MC. Equilibrium price for a monopoly, PM, occurs on the demand curve at the profit-maximizing quantity.

38

Single-Price Monopoly and Competition Compared

Because marginal revenue is less than price at each output level, QM < QC and PM > PC. Compared to perfect competition, monopoly restricts output and charges a higher price.

40

Single-Price Monopoly and Competition Compared

Efficiency Comparison Monopoly is inefficient, and Figure 12.6 shows why. The demand curve is the marginal benefit curve, MB, and the competitive market supply curve is the marginal cost curve, MC. So competitive equilibrium is efficient: MB = MC.

42

Single-Price Monopoly and Competition Compared

Consumer surplus is the area below the demand curve and above the price. Producer surplus is the area below the price and above the marginal cost curve. The sum of the two surpluses is maximized and the efficient quantity is produced.

44

Single-Price Monopoly and Competition Compared

Monopoly is inefficient because price exceeds marginal cost so marginal benefit exceeds marginal cost. On all output levels for which marginal benefit exceeds marginal cost, a deadweight loss is incurred. Monopoly is inefficient. The inefficiency of monopoly is one of the key propositions in this chapter. Because P > MR, and because MR = MC, P > MC—single-price monopoly under-produces and creates deadweight loss. Rent seeking uses further resources so potentially the social cost of monopoly is the sum of the deadweight loss and the economic profit that a monopoly might earn. Adam Smith described the situation thus: “People in the same trade seldom meet together, even for merriment and diversion, but the conversation ends in some contrivance to raise prices.”

46

Single-Price Monopoly and Competition Compared

Redistribution of Surpluses Monopoly redistributes a portion of consumer surplus by changing it to producer surplus.

48

Single-Price Monopoly and Competition Compared

Rent Seeking The social cost of monopoly may exceed the deadweight loss through an activity called rent seeking, which is any attempt to capture consumer surplus, producer surplus, or economic profit. There are two forms of rent seeking activity to pursue monopoly: 1. Buy a monopoly 2. Create a monopoly—political activity(influence).

.")

49

Single-Price Monopoly and Competition Compared

Rent-Seeking Equilibrium only normal profit. Figure 12.7 shows the normal profit that result from rent seeking.

51

Single-Price Monopoly and Competition Compared

A potential profit shown by the blue area gets used up in rent seeking. Average total cost increases and the profits disappear to become part of the enlarged deadweight loss from rent seeking.

53

Price Discrimination Price discrimination is the practice of selling different units of a good or service for different prices. To be able to price discriminate, a monopoly must: Identify and separate different buyer types Sell a product that cannot be resold Price differences that arise from cost differences are not price discrimination. Price discrimination may not be fair, but it is efficient Be sure that the students understand that aside from equity considerations, resources will be allocated more efficiently in a monopoly market under any price discrimination scenario than under a single-price scenario.

54

Price Discrimination Price Discrimination and Consumer Surplus

Price discrimination converts consumer surplus into economic profit. A monopoly can discriminate Among units of a good. Quantity discounts are an example. Among groups of buyers. airline tickets are an example.

55

Price Discrimination Profiting by Price Discriminating

Figures 12.8 and 12.9 show the same market with a single price and price discrimination and show how price discrimination converts consumer surplus into economic profit.

57

Price Discrimination As a single-price monopolist, this firm maximized profit by producing 8 units, where MR = MC and selling them for $1,200 each.

59

Price Discrimination By price discriminating, the firm can increase its profit. In doing so, it converts consumer surplus into economic profit.

61

Price Discrimination Perfect Price Discrimination

Perfect price discrimination extracts the entire potential consumer surplus and converts it to economic profit.

63

Price Discrimination With perfect price discrimination:

1. Output increases to the quantity at which price equals marginal cost 2. Economic profit increases above that earned by a single-price monopoly. 3. Deadweight loss is eliminated

65

Price Discrimination Efficiency and Rent Seeking with Price Discrimination perfect price discrimination achieve efficiency. But this outcome differs from the outcome of perfect competition in two ways: The monopoly captures the entire consumer surplus. The increase in economic profit attracts even more rent-seeking activity that leads to an inefficient use of resources.

66

Monopoly Policy Issues

Gains from Monopoly A single-price monopoly creates inefficiency and price discriminating monopoly captures consumer surplus and converts it into producer surplus and economic profit. And monopoly encourages rent-seeking, which wastes resources. But monopoly brings benefits. A quick introduction The treatment of monopoly policy here is brief and designed for the instructor who wants to cover the topic briefly and at this point in the course. Chapter 17 provides a more extensive treatment of regulation and antitrust law. You can cover that chapter, in whole or part, right now if you want to do more on the topic.

67

Monopoly Policy Issues

Product innovation Patents and copyrights provide protection from competition and let the monopoly enjoy the profits. Economies of scale and scope Where economies of scale or scope exist, a monopoly can produce at a lower average total cost.

68

Monopoly Policy Issues

Regulating Natural Monopoly Figure shows how a natural monopoly might be regulated.

70

Monopoly Policy Issues

With no regulation, the monopoly maximizes profit. It produces the quantity at which marginal revenue equals marginal cost.

72

Monopoly Policy Issues

Regulating a natural monopoly in the public interest sets output where MR = MC and the price equal to marginal cost. This regulation is the marginal cost pricing rule, and it results in an efficient use of resources.

74

Monopoly Policy Issues

With price equal to marginal cost, ATC exceeds price and the monopoly incurs an economic loss. If the monopoly receives a subsidy to cover its loss, taxes must be imposed on other economic activity, which create deadweight loss

76

Monopoly Policy Issues

Another alternative is to produce the quantity at which price equals average total cost and to set the price equal to average total cost—the average cost pricing rule.

78

THE END

Similar presentations