Download presentation

Presentation is loading. Please wait.

1

Forecasting using simple models

2

Outline Basic forecasting models The basic ideas behind each model

When each model may be appropriate Illustrate with examples Forecast error measures Automatic model selection Adaptive smoothing methods (automatic alpha adaptation) Ideas in model based forecasting techniques Regression Autocorrelation Prediction intervals

Ideas in model based forecasting techniques. Regression. Autocorrelation. Prediction intervals.")

3

Basic Forecasting Models

Moving average and weighted moving average First order exponential smoothing Second order exponential smoothing First order exponential smoothing with trends and/or seasonal patterns Croston’s method

4

M-Period Moving Average

i.e. the average of the last M data points Basically assumes a stable (trend free) series How should we choose M? Advantages of large M? Average age of data = M/2

series. How should we choose M Advantages of large M Average age of data = M/2.")

5

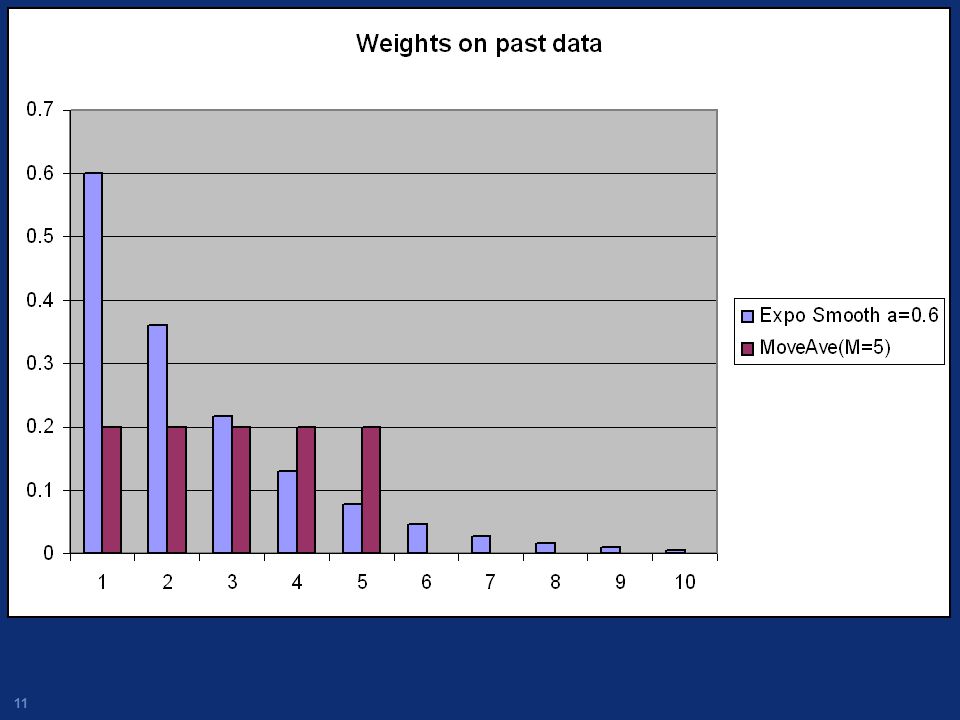

Weighted Moving Averages

The Wi are weights attached to each historical data point Essentially all known (univariate) forecasting schemes are weighted moving averages Thus, don’t screw around with the general versions unless you are an expert

forecasting schemes are weighted moving averages. Thus, don’t screw around with the general versions unless you are an expert.")

6

Simple Exponential Smoothing

Pt+1(t) = Forecast for time t+1 made at time t Vt = Actual outcome at time t 0<<1 is the “smoothing parameter”

= Forecast for time t+1 made at time t. Vt = Actual outcome at time t. 0<<1 is the smoothing parameter")

7

Two Views of Same Equation

Pt+1(t) = Pt(t-1) + [Vt – Pt(t-1)] Adjust forecast based on last forecast error OR Pt+1(t) = (1- )Pt(t-1) + Vt Weighted average of last forecast and last Actual

= Pt(t-1) + [Vt – Pt(t-1)] Adjust forecast based on last forecast error. OR. Pt+1(t) = (1- )Pt(t-1) + Vt. Weighted average of last forecast and last Actual.")

8

Simple Exponential Smoothing

Is appropriate when the underlying time series behaves like a constant + Noise Xt = + Nt Or when the mean is wandering around That is, for a quite stable process Not appropriate when trends or seasonality present

9

ES would work well here

10

Simple Exponential Smoothing

We can show by recursive substitution that ES can also be written as: Pt+1(t) = Vt + (1-)Vt-1 + (1-)2Vt-2 + (1-)3Vt-3 +….. Is a weighted average of past observations Weights decay geometrically as we go backwards in time

= Vt + (1-)Vt-1 + (1-)2Vt-2 + (1-)3Vt-3 +….. Is a weighted average of past observations. Weights decay geometrically as we go backwards in time.")

12

Simple Exponential Smoothing

Ft+1(t) = At + (1-)At-1 + (1-)2At-2 + (1-)3At-3 +….. Large adjusts more quickly to changes Smaller provides more “averaging” and thus lower variance when things are stable Exponential smoothing is intuitively more appealing than moving averages

= At + (1-)At-1 + (1-)2At-2 + (1-)3At-3 +….. Large adjusts more quickly to changes. Smaller provides more averaging and thus lower variance when things are stable. Exponential smoothing is intuitively more appealing than moving averages.")

13

Exponential Smoothing Examples

14

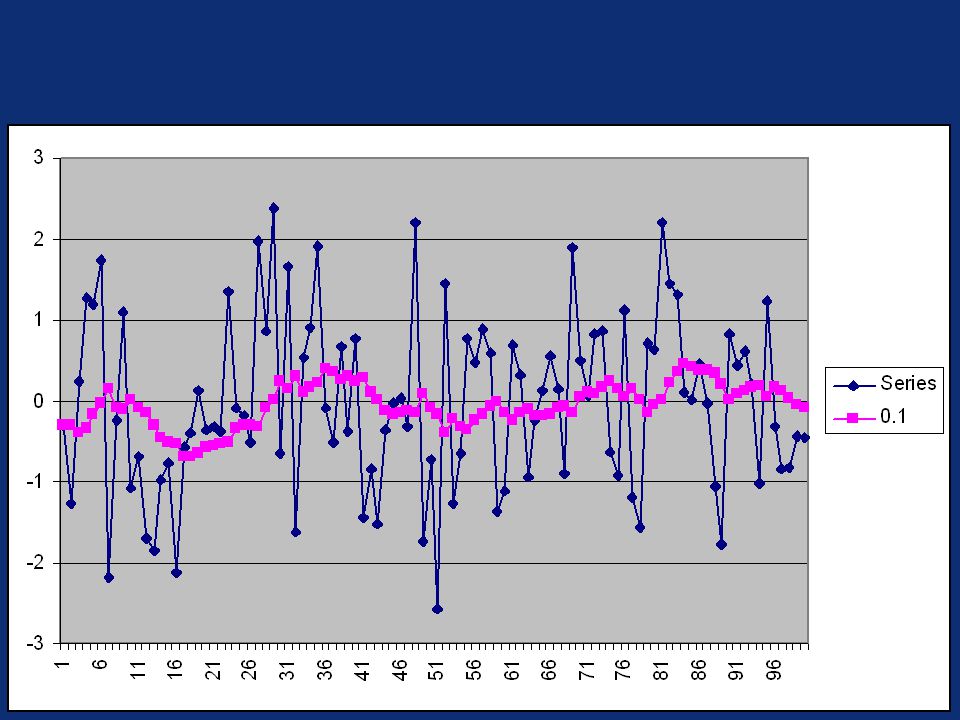

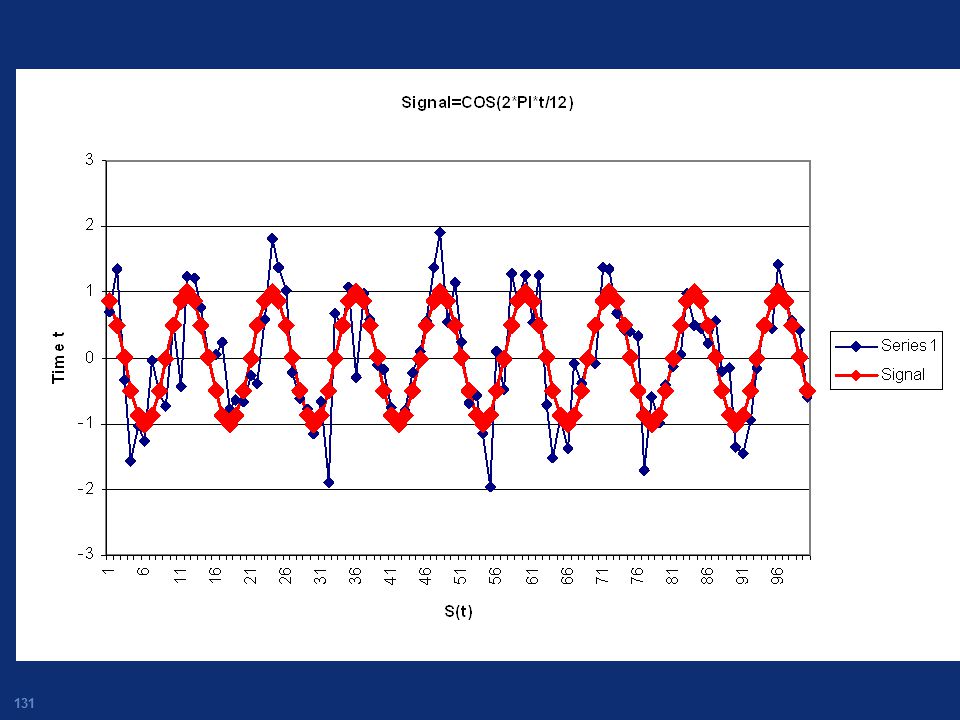

Zero Mean White Noise

17

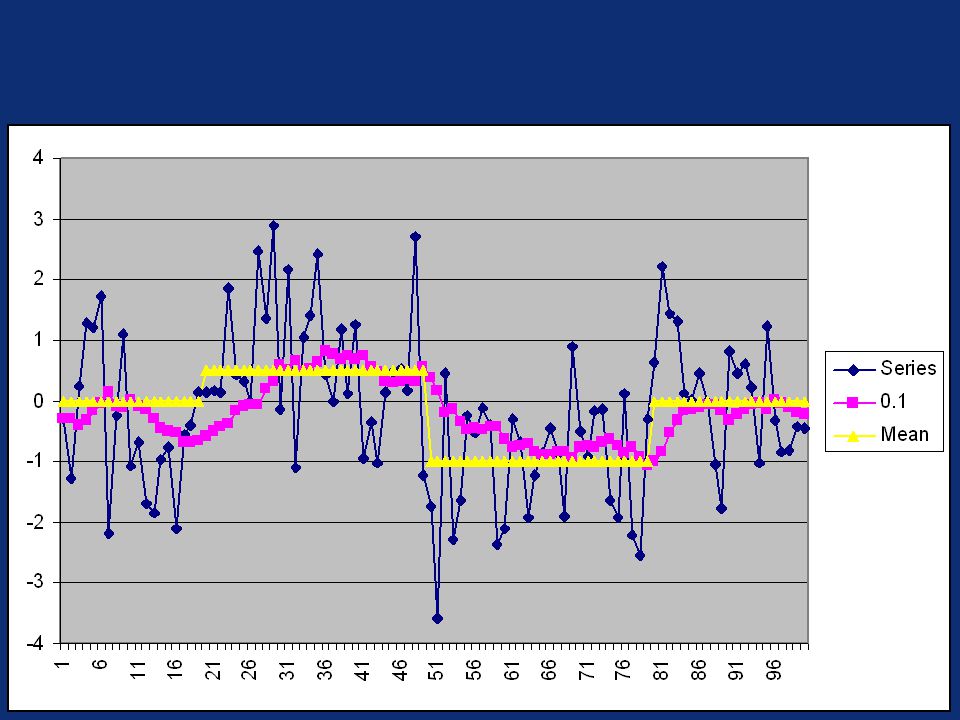

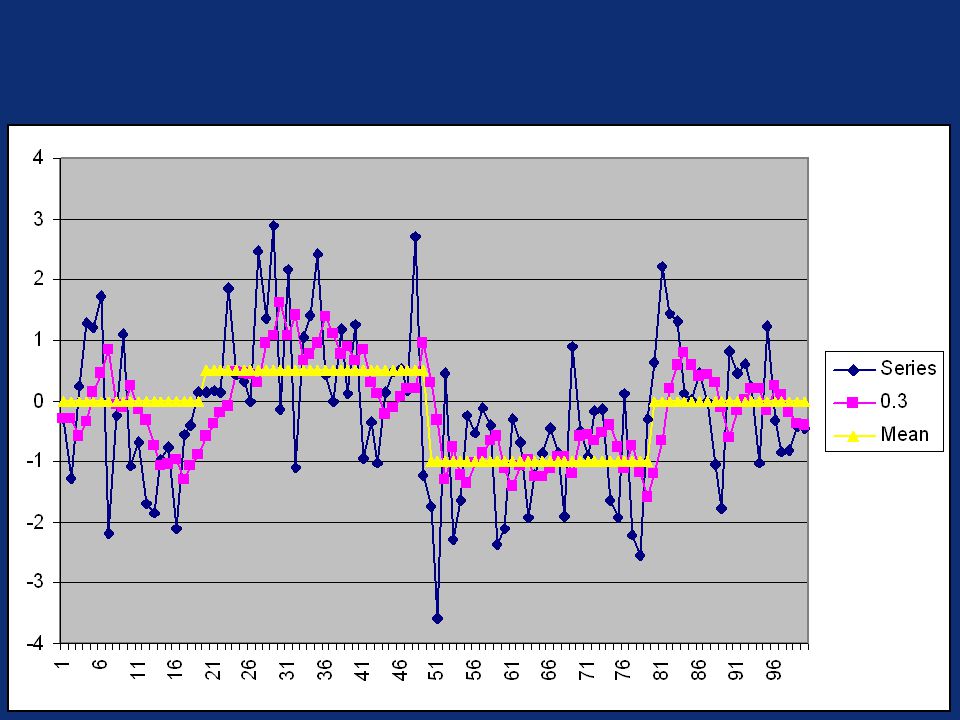

Shifting Mean + Zero Mean White Noise

20

Automatic selection of

Using historical data Apply a range of values For each, calculate the error in one-step-ahead forecasts e.g. the root mean squared error (RMSE) Select the that minimizes RMSE

Select the that minimizes RMSE.")

21

RMSE vs Alpha 1.45 1.4 1.35 RMSE 1.3 1.25 1.2 1.15 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1 Alpha

22

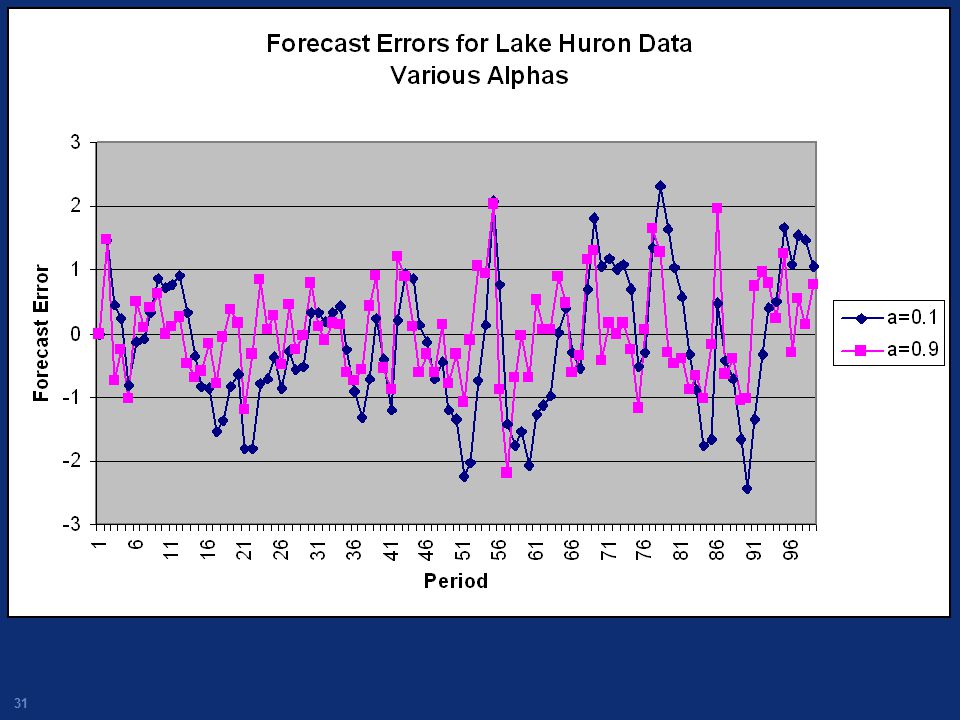

Recommended Alpha Typically alpha should be in the range 0.05 to 0.3

If RMSE analysis indicates larger alpha, exponential smoothing may not be appropriate

25

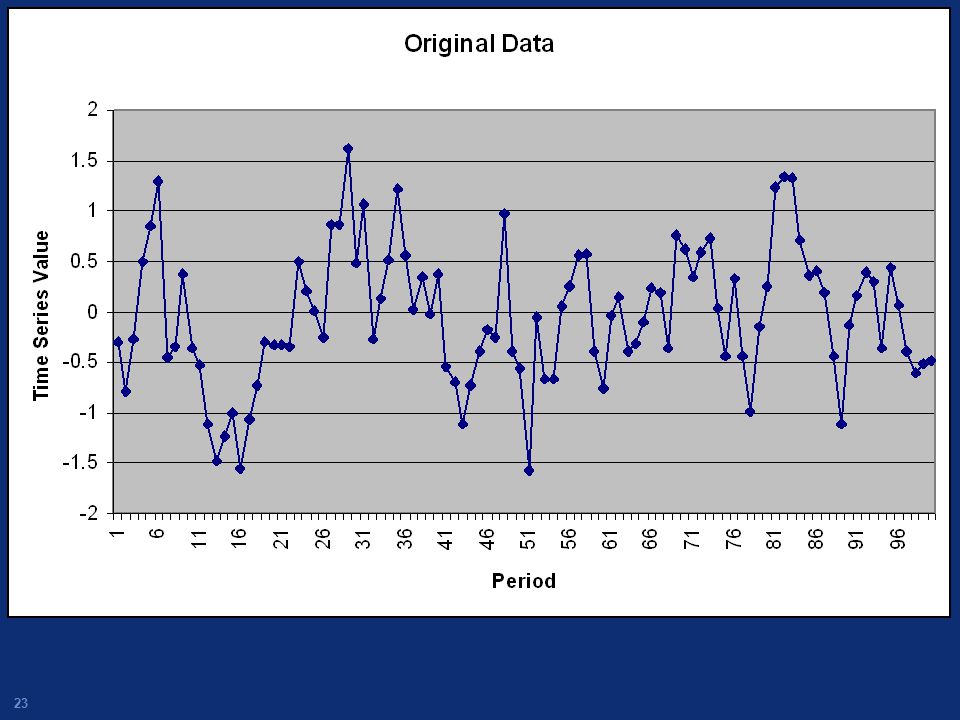

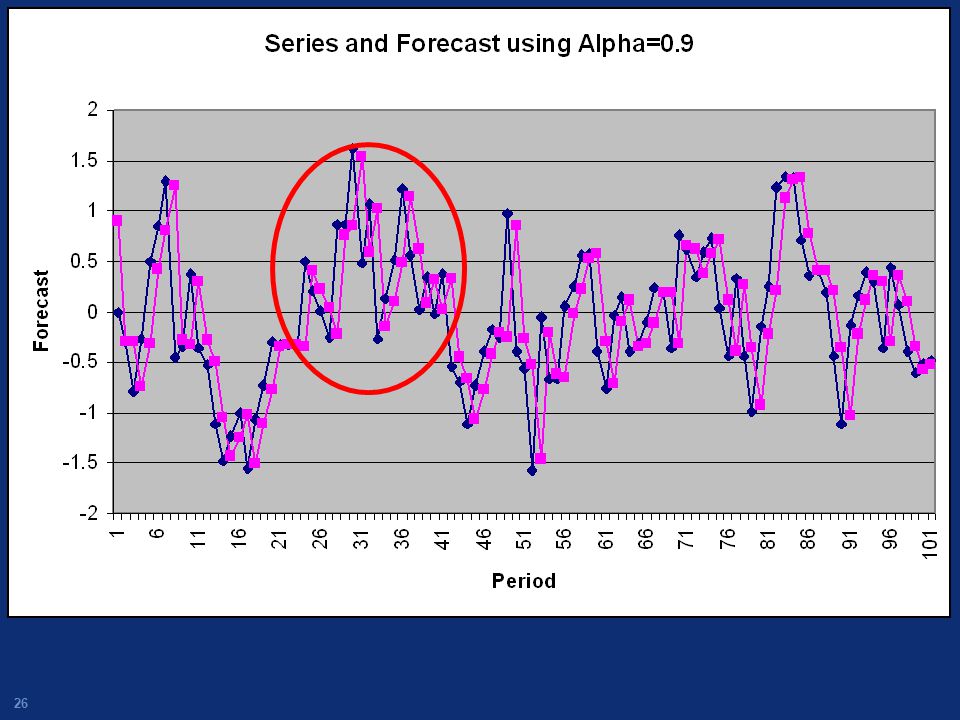

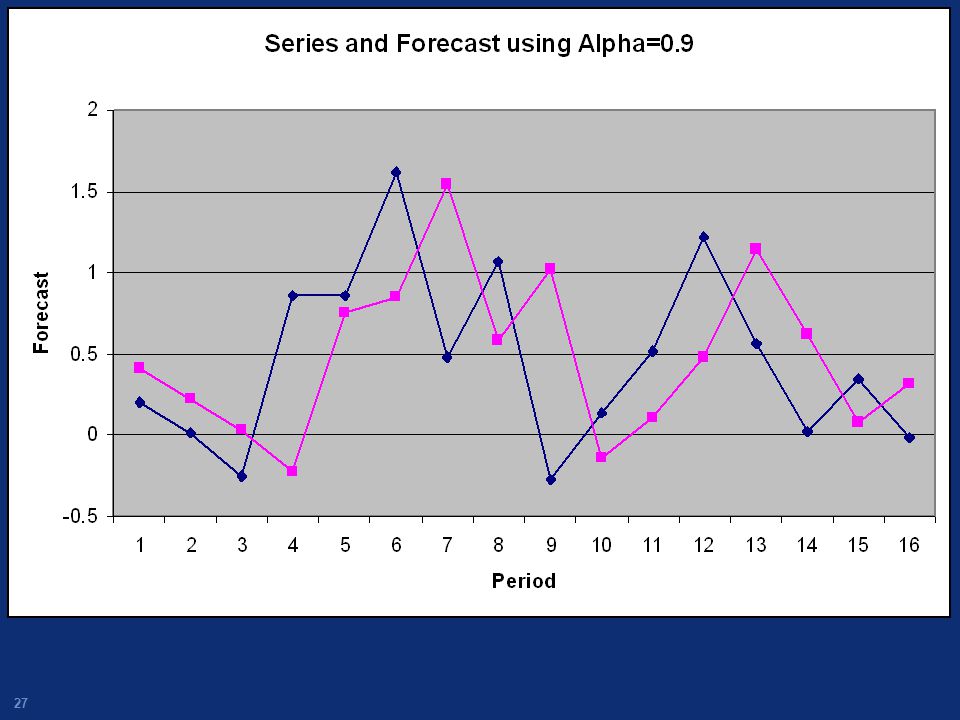

Might look good, but is it?

28

Series and Forecast using Alpha=0.9

2 1.5 1 Forecast 0.5 -0.5 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 Period

29

Forecast RMSE vs Alpha 0.67 0.66 0.65 0.64 0.63 Forecast RMSE 0.62

Series1 0.61 0.6 0.59 0.58 0.57 0.2 0.4 0.6 0.8 1 Alpha

32

Forecast RMSE vs Alpha for Lake Huron Data

1.1 1.05 1 0.95 0.9 RMSE 0.85 0.8 0.75 0.7 0.65 0.6 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1 Alpha

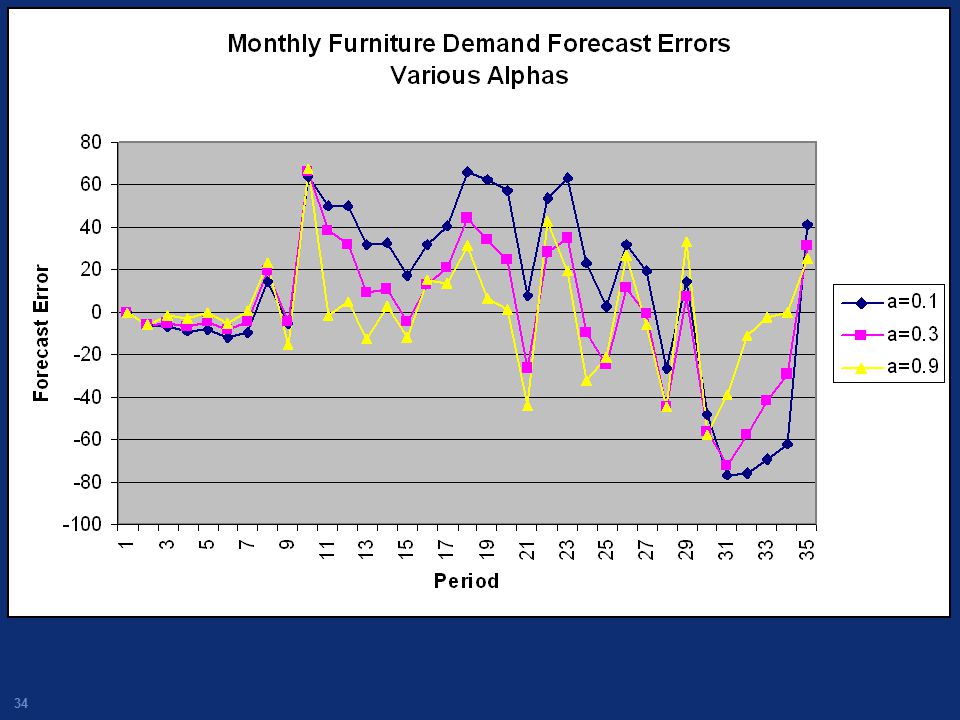

35

for Monthly Furniture Demand Data

Forecast RMSE vs Alpha for Monthly Furniture Demand Data 45.6 40.6 35.6 30.6 25.6 RMSE 20.6 15.6 10.6 5.6 0.6 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1 Alpha

36

Exponential smoothing will lag behind a trend

Suppose Xt=b0+ b1t And St= (1- )St-1 + Xt Can show that

St-1 + Xt. Can show that.")

38

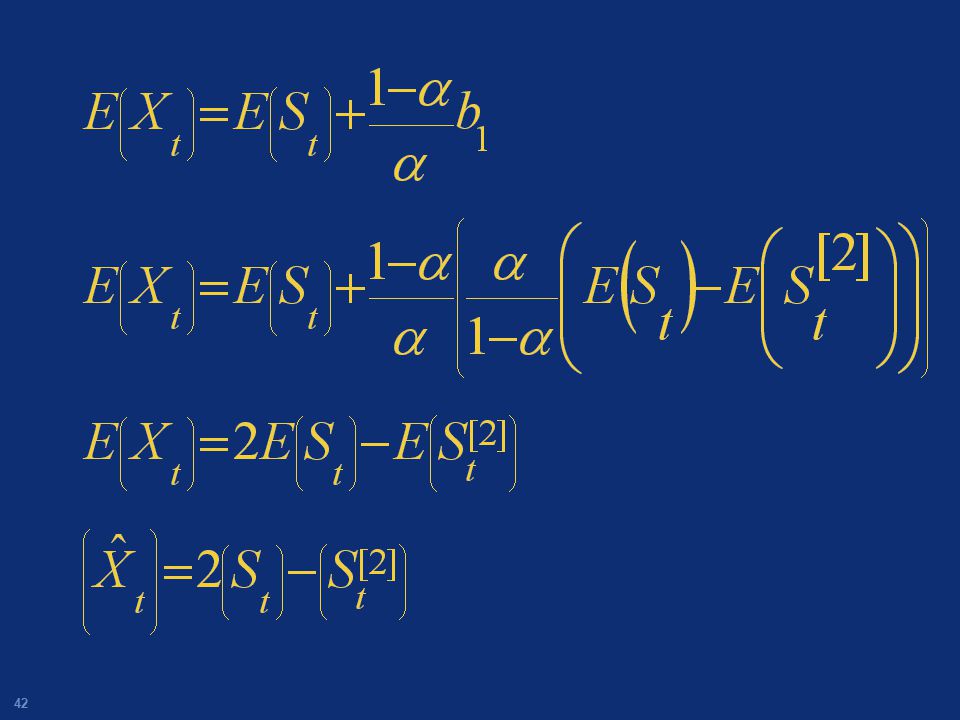

Double Exponential Smoothing

Modifies exponential smoothing for following a linear trend i.e. Smooth the smoothed value

39

St Lags St[2] Lags even more

![St Lags St[2] Lags even more](http://slideplayer.com/slide/4919574/16/images/39/St+Lags+St%5B2%5D+Lags+even+more.jpg "St Lags St[2] Lags even more")

40

2St -St[2] doesn’t lag

![2St -St[2] doesn’t lag](http://slideplayer.com/slide/4919574/16/images/40/2St+-St%5B2%5D+doesn%E2%80%99t+lag.jpg "2St -St[2] doesn’t lag")

44

Example

45

=0.2

46

Single Lags a trend

47

Double Over-shoots a change (must “re-learn” the slope)

6 5 4 Double Over-shoots a change (must “re-learn” the slope) 3 Trend 2 Series Data Single Smoothing 1 Double smoothing -1 1 6 11 16 21 26 31 36 41 46 51 56 61 66 71 76 81 86 91 96 101

3. Trend. 2. Series Data. Single Smoothing. 1. Double smoothing")

48

Holt-Winters Trend and Seasonal Methods

“Exponential smoothing for data with trend and/or seasonality” Two models, Multiplicative and Additive Models contain estimates of trend and seasonal components Models “smooth”, i.e. place greater weight on more recent data

49

Winters Multiplicative Model

Xt = (b1+b2t)ct + t Where ct are seasonal terms and Note that the amplitude depends on the level of the series Once we start smoothing, the seasonal components may not add to L

ct + t. Where ct are seasonal terms and. Note that the amplitude depends on the level of the series. Once we start smoothing, the seasonal components may not add to L.")

50

Holt-Winters Trend Model

Xt = (b1+b2t) + t Same except no seasonal effect Works the same as the trend + season model except simpler

+ t. Same except no seasonal effect. Works the same as the trend + season model except simpler.")

51

Example:

52

(1+0.04t)

")

53

*150%

54

*50%

55

The seasonal terms average 100% (i.e. 1)

Thus summed over a season, the ct must add to L Each period we go up or down some percentage of the current level value The amplitude increasing with level seems to occur frequently in practice

56

Recall Australian Red Wine Sales

57

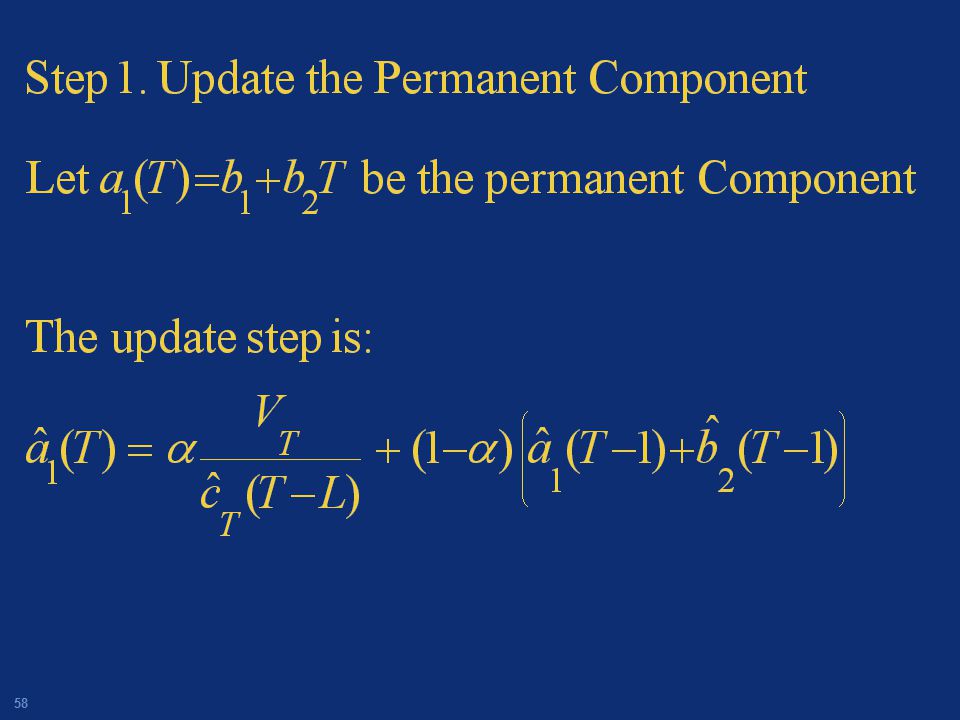

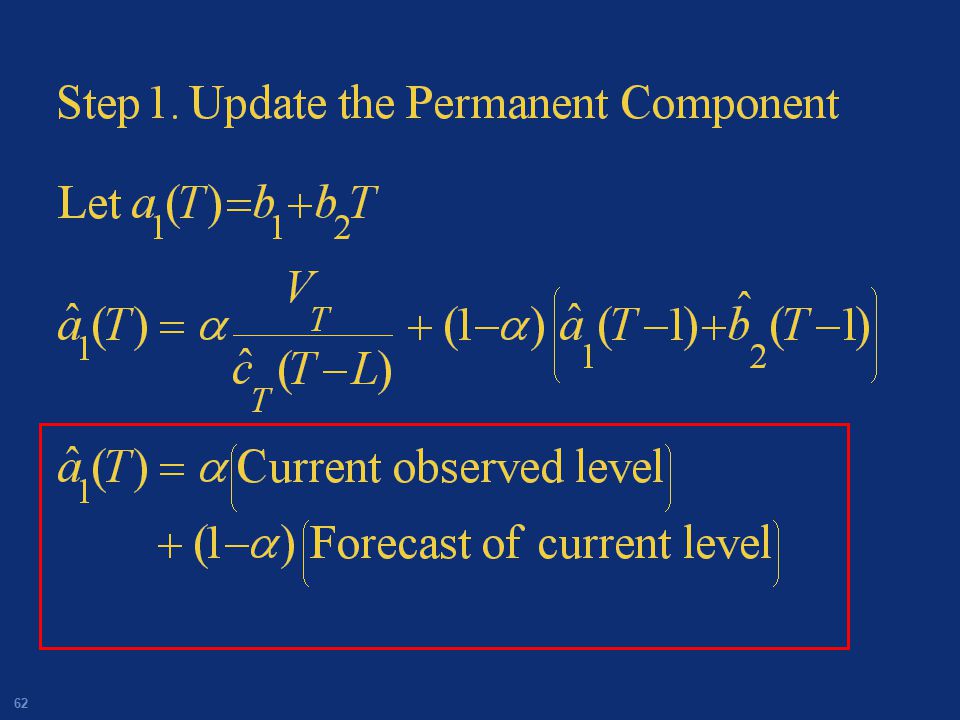

Smoothing In Winters model, we smooth the “permanent component”, the “trend component” and the “seasonal component” We may have a different smoothing parameter for each (, , ) Think of the permanent component as the current level of the series (without trend)

Think of the permanent component as the current level of the series (without trend)")

59

Current Observation

60

Current Observation “deseasonalized”

61

Estimate of permanent component from

last time = last level + slope*1

64

“observed” slope

65

“observed” slope “previous” slope

68

Extend the trend out periods ahead

69

Use the proper seasonal adjustment

70

Winters Additive Method

Xt = b1+ b2t + ct + t Where ct are seasonal terms and Similar to previous model except we “smooth” estimates of b1, b2, and the ct

71

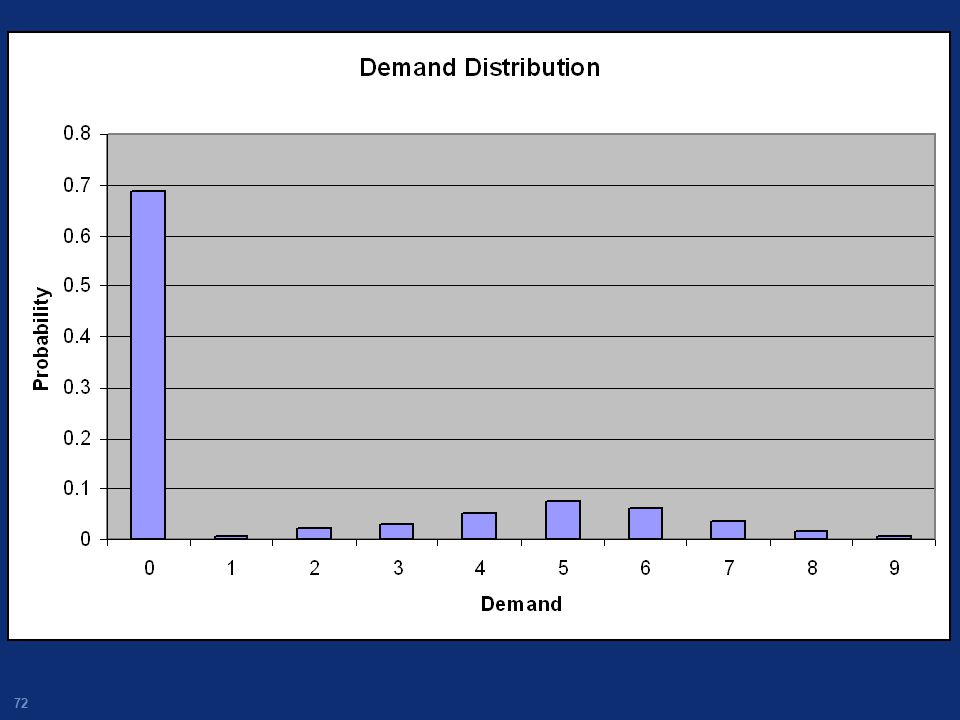

Croston’s Method Can be useful for intermittent, erratic, or slow-moving demand e.g. when demand is zero most of the time (say 2/3 of the time) Might be caused by Short forecasting intervals (e.g. daily) A handful of customers that order periodically Aggregation of demand elsewhere (e.g. reorder points)

A handful of customers that order periodically. Aggregation of demand elsewhere (e.g. reorder points)")

73

Typical situation Central spare parts inventory (e.g. military)

Orders from manufacturer in batches (e.g. EOQ) periodically when inventory nearly depleted long lead times may also effect batch size

periodically when inventory nearly depleted. long lead times may also effect batch size.")

74

Example Demand each period follows a distribution that is usually zero

75

Example

76

Example Exponential smoothing applied (=0.2)

")

77

Using Exponential Smoothing:

Forecast is highest right after a non-zero demand occurs Forecast is lowest right before a non-zero demand occurs

78

Croston’s Method Forecast = Separately Tracks

Time between (non-zero) demands Demand size when not zero Smoothes both time between and demand size Combines both for forecasting Demand Size Forecast = Time between demands

demands. Demand size when not zero. Smoothes both time between and demand size. Combines both for forecasting. Demand Size. Forecast = Time between demands.")

79

Define terms V(t) = actual demand outcome at time t

P(t) = Predicted demand at time t Z(t) = Estimate of demand size (when it is not zero) X(t) = Estimate of time between (non-zero) demands q = a variable used to count number of periods between non-zero demand

= Predicted demand at time t. Z(t) = Estimate of demand size (when it is not zero) X(t) = Estimate of time between (non-zero) demands. q = a variable used to count number of periods between non-zero demand.")

80

Forecast Update For a period with zero demand Z(t)=Z(t-1) X(t)=X(t-1)

No new information about order size Z(t) time between orders X(t) q=q+1 Keep counting time since last order

time between orders X(t) q=q+1. Keep counting time since last order.")

81

Forecast Update q=1 For a period with non-zero demand

Z(t)=Z(t-1) + (V(t)-Z(t-1)) X(t)=X(t-1) + (q - X(t-1)) q=1

=Z(t-1) + (V(t)-Z(t-1)) X(t)=X(t-1) + (q - X(t-1)) q=1.")

82

Forecast Update q=1 Latest order size

For a period with non-zero demand Z(t)=Z(t-1) + (V(t)-Z(t-1)) X(t)=X(t-1) + (q - X(t-1)) q=1 Update Size of order via smoothing Latest order size

=Z(t-1) + (V(t)-Z(t-1)) X(t)=X(t-1) + (q - X(t-1)) q=1. Update Size of order via smoothing. Latest. order size.")

83

Forecast Update q=1 Latest time between orders

For a period with non-zero demand Z(t)=Z(t-1) + (V(t)-Z(t-1)) X(t)=X(t-1) + (q - X(t-1)) q=1 Update size of order via smoothing Update time between orders via smoothing Latest time between orders

=Z(t-1) + (V(t)-Z(t-1)) X(t)=X(t-1) + (q - X(t-1)) q=1. Update size of order via smoothing. Update time between orders via smoothing. Latest time. between orders.")

84

Forecast Update q=1 Reset counter For a period with non-zero demand

Z(t)=Z(t-1) + (V(t)-Z(t-1)) X(t)=X(t-1) + (q - X(t-1)) q=1 Update size of order via smoothing Update time between orders via smoothing Reset counter of time between orders Reset counter

=Z(t-1) + (V(t)-Z(t-1)) X(t)=X(t-1) + (q - X(t-1)) q=1. Update size of order via smoothing. Update time between orders via smoothing. Reset counter of time between orders. Reset. counter.")

85

Forecast P(t) = = Finally, our forecast is: Z(t) Non-zero Demand Size

X(t) Time Between Demands

Time Between Demands.")

86

Recall example Exponential smoothing applied (=0.2)

")

87

Recall example Croston’s method applied (=0.2)

")

88

True average demand per period=0.176

What is it forecasting? Average demand per period True average demand per period=0.176

89

Behavior Forecast only changes after a demand

Forecast constant between demands Forecast increases when we observe A large demand A short time between demands Forecast decreases when we observe A small demand A long time between demands

90

Croston’s Method Croston’s method assumes demand is independent between periods That is one period looks like the rest (or changes slowly)

")

91

Counter Example One large customer Orders using a reorder point

The longer we go without an order The greater the chances of receiving an order In this case we would want the forecast to increase between orders Croston’s method may not work too well

92

Better Examples Demand is a function of intermittent random events

Military spare parts depleted as a result of military actions Umbrella stocks depleted as a function of rain Demand depending on start of construction of large structure

93

Is demand Independent? If enough data exists we can check the distribution of time between demand Should “tail off” geometrically

94

Theoretical behavior

95

In our example:

96

Comparison

97

Counterexample Croston’s method might not be appropriate if the time between demands distribution looks like this:

98

Counterexample In this case, as time approaches 20 periods without demand, we know demand is coming soon. Our forecast should increase in this case

99

Error Measures Errors: The difference between actual and predicted (one period earlier) et = Vt – Pt(t-1) et =can be positive or negative Absolute error |et| Always positive Squared Error et2 The percentage error PEt = 100et / Vt Can be positive or negative

100

Bias and error magnitude

Forecasts can be: Consistently too high or too low (bias) Right on average, but with large deviations both positive and negative (error magnitude) Should monitor both for changes

Right on average, but with large deviations both positive and negative (error magnitude) Should monitor both for changes.")

101

Error Measures Look at errors over time

Cumulative measures summed or averaged over all data Error Total (ET) Mean Percentage Error (MPE) Mean Absolute Percentage Error (MAPE) Mean Squared Error (MSE) Root Mean Squared Error (RMSE) Smoothed measures reflects errors in the recent past Mean Absolute Deviation (MAD)

Mean Percentage Error (MPE) Mean Absolute Percentage Error (MAPE) Mean Squared Error (MSE) Root Mean Squared Error (RMSE) Smoothed measures reflects errors in the recent past. Mean Absolute Deviation (MAD)")

102

Error Measures Measure Bias Look at errors over time

Cumulative measures summed or averaged over all data Error Total (ET) Mean Percentage Error (MPE) Mean Absolute Percentage Error (MAPE) Mean Squared Error (MSE) Root Mean Squared Error (RMSE) Smoothed measures reflects errors in the recent past Mean Absolute Deviation (MAD)

Mean Percentage Error (MPE) Mean Absolute Percentage Error (MAPE) Mean Squared Error (MSE) Root Mean Squared Error (RMSE) Smoothed measures reflects errors in the recent past. Mean Absolute Deviation (MAD)")

103

Error Measures Measure error magnitude Look at errors over time

Cumulative measures summed or averaged over all data Error Total (ET) Mean Percentage Error (MPE) Mean Absolute Percentage Error (MAPE) Mean Squared Error (MSE) Root Mean Squared Error (RMSE) Smoothed measures reflects errors in the recent past Mean Absolute Deviation (MAD)

Mean Percentage Error (MPE) Mean Absolute Percentage Error (MAPE) Mean Squared Error (MSE) Root Mean Squared Error (RMSE) Smoothed measures reflects errors in the recent past. Mean Absolute Deviation (MAD)")

104

Error Total Sum of all errors Uses raw (positive or negative) errors

ET can be positive or negative Measures bias in the forecast Should stay close to zero as we saw in last presentation

105

MPE Average of percent errors Can be positive or negative

Measures bias, should stay close to zero

106

MSE Average of squared errors Always positive

Measures “magnitude” of errors Units are “demand units squared”

107

RMSE Square root of MSE Always positive Measures “magnitude” of errors

Units are “demand units” Standard deviation of forecast errors

108

MAPE Average of absolute percentage errors Always positive

Measures magnitude of errors Units are “percentage”

109

Mean Absolute Deviation

Smoothed absolute errors Always positive Measures magnitude of errors Looks at the recent past

110

Percentage or Actual units

Often errors naturally increase as the level of the series increases Natural, thus no reason for alarm If true, percentage based measured preferred Actual units are more intuitive

111

Squared or Absolute Errors

Absolute errors are more intuitive Standard deviation units less so 66% within 1 S.D. 95% within 2 S.D. When using measures for automatic model selection, there are statistical reasons for preferring measures based on squared errors

112

Ex-Post Forecast Errors

Given A forecasting method Historical data Calculate (some) error measure using the historical data Some data required to initialize forecasting method. Rest of data (if enough) used to calculate ex-post forecast errors and measure

error measure using the historical data. Some data required to initialize forecasting method. Rest of data (if enough) used to calculate ex-post forecast errors and measure.")

113

Automatic Model Selection

For all possible forecasting methods (and possibly for all parameter values e.g. smoothing constants – but not in SAP?) Compute ex-post forecast error measure Select method with smallest error

Compute ex-post forecast error measure. Select method with smallest error.")

114

Automatic Adaptation

Suppose an error measure indicates behavior has changed e.g. level has jumped up Slope of trend has changed We would want to base forecasts on more recent data Thus we would want a larger

115

Tracking Signal (TS) Bias/Magnitude = “Standardized bias”

![]()

116

Adaptation If TS increases, bias is increasing, thus increase

I don’t like these methods due to instability

117

Model Based Methods Find and exploit “patterns” in the data

Trend and Seasonal Decomposition Time based regression Time Series Methods (e.g. ARIMA Models) Multiple Regression using leading indicators Assumes series behavior stays the same Requires analysis (no “automatic model generation”)

Multiple Regression using leading indicators. Assumes series behavior stays the same. Requires analysis (no automatic model generation )")

118

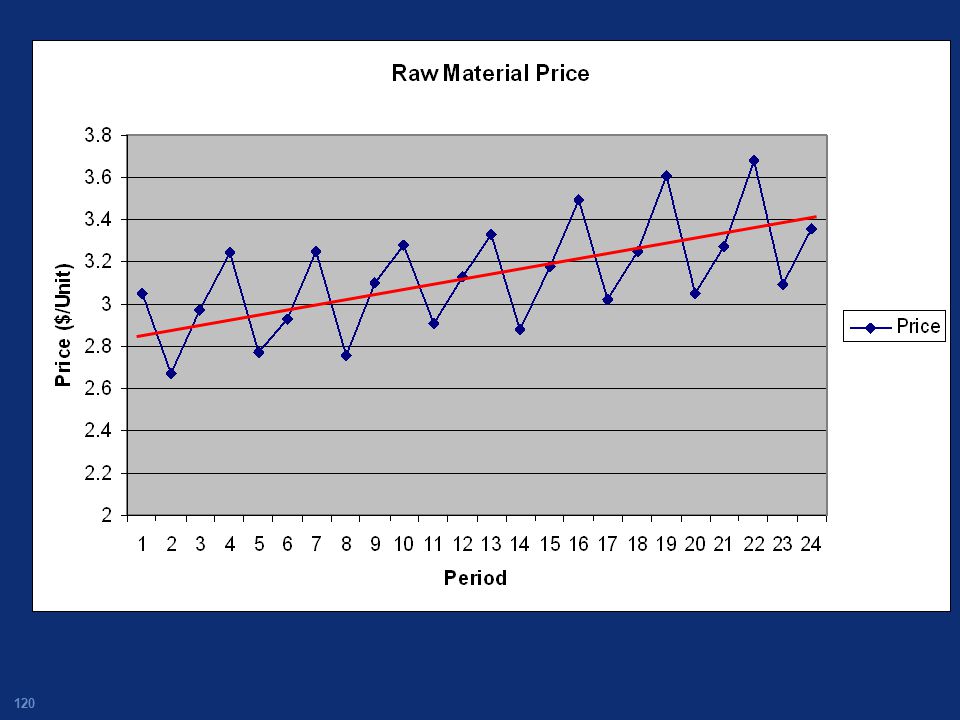

Univariate Time Series Models Based on Decomposition

Vt = the time series to forecast Vt = Tt + St + Nt Where Tt is a deterministic trend component St is a deterministic seasonal/periodic component Nt is a random noise component

119

(Vt)=0.257

=0.257")

121

Simple Linear Regression Model: Vt=2.877174+0.020726t

122

Use Model to Forecast into the Future

123

Residuals = Actual-Predicted et = Vt-(2.877174+0.020726t)

")

124

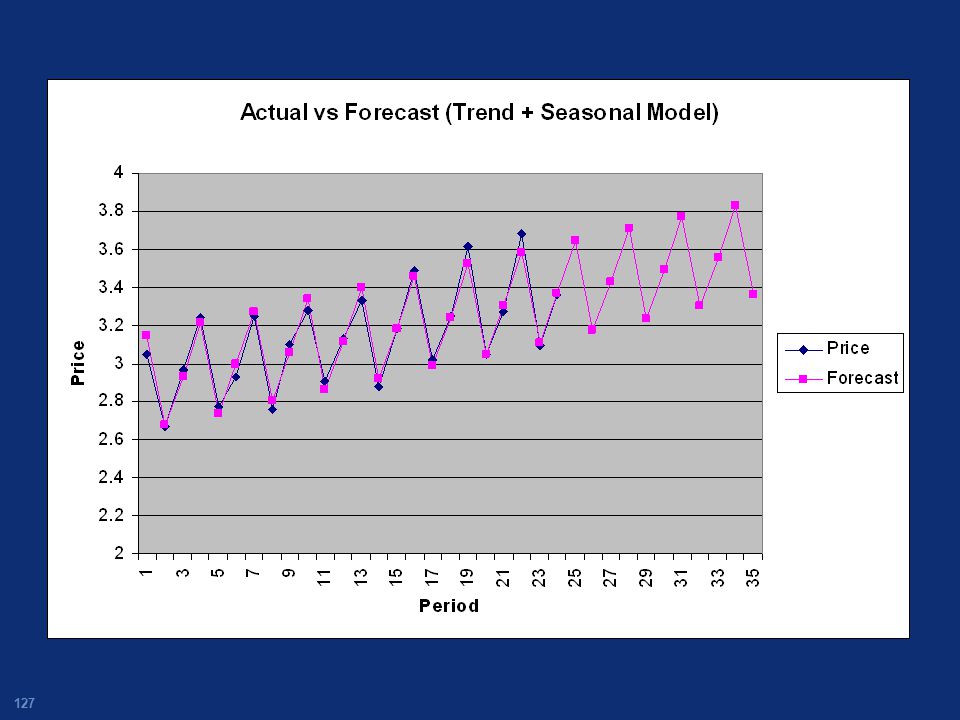

Simple Seasonal Model Estimate a seasonal adjustment factor for each period within the season e.g. SSeptember

125

Sorted by season Season averages

126

Trend + Seasonal Model Vt=2.877174+0.020726t + Smod(t,3) Where

Where")

128

et = Vt - ( t + Smod(t,3)) (et)=0.145

) (et)=0.145")

129

Can use other trend models

Vt= 0+ 1Sin(2t/k) (where k is period) Vt= 0+ 1t + 2t2 (multiple regression) Vt= 0+ 1ekt etc. Examine the plot, pick a reasonable model Test model fit, revise if necessary

(where k is period) Vt= 0+ 1t + 2t2 (multiple regression) Vt= 0+ 1ekt. etc. Examine the plot, pick a reasonable model. Test model fit, revise if necessary.")

132

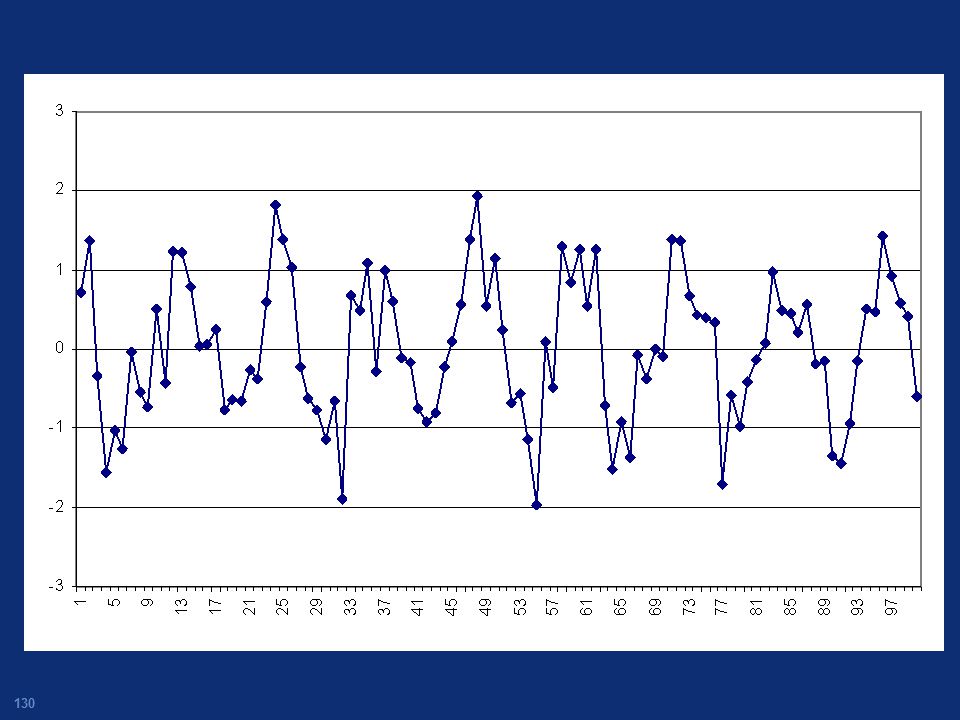

Model: Vt = Tt + St + Nt After extracting trend and seasonal components we are left with “the Noise” Nt = Vt – (Tt + St) Can we extract any more predictable behavior from the “noise”? Use Time Series analysis Akin to signal processing in EE

Can we extract any more predictable behavior from the noise Use Time Series analysis. Akin to signal processing in EE.")

133

Zero Mean, and Aperiodic: Is our best forecast ?

134

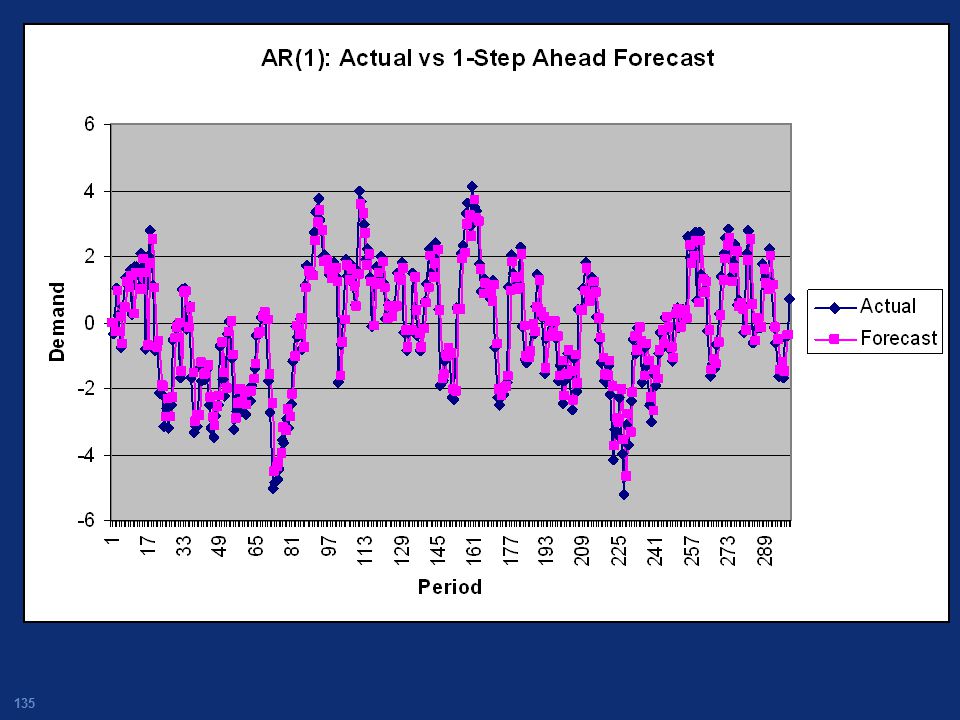

AR(1) Model This data was generated using the model Nt = 0.9Nt-1 + Zt

Where Zt ~N(0,2) Thus to forecast Nt+1,we could use:

Thus to forecast Nt+1,we could use:")

137

Time Series Models Examine the correlation of the time series to past values. This is called “autocorrelation” If Nt is correlated to Nt-1, Nt-2,….. Then we can forecast better than

138

Sample Autocorrelation Function

139

Back to our Demand Data

140

No Apparent Significant Autocorrelation

141

Multiple Linear Regression

V= 0+ 1 X1 + 2 X2 +….+ p Xp + Where V is the “independent variable” you want to predict The Xi‘s are the dependent variables you want to use for prediction (known) Model is linear in the i‘s

Model is linear in the i‘s.")

142

Examples of MLR in Forecasting

Vt= 0+ 1t + 2t2 + 3Sin(2t/k) + 4ekt i.e a trend model, a function of t Vt= 0+ 1X1t + 2X2t Where X1t and X2t are leading indicators Vt= 0+ 1Vt-1+ 2Vt-2 + 12Vt-12 +13Vt-13 An Autoregressive model

+ 4ekt. i.e a trend model, a function of t. Vt= 0+ 1X1t + 2X2t. Where X1t and X2t are leading indicators. Vt= 0+ 1Vt-1+ 2Vt-2 + 12Vt-12 +13Vt-13. An Autoregressive model.")

143

Example: Sales and Leading Indicator

144

Example: Sales and Leading Indicator

Sales(t) = Sales(t-3) -0.78Sales(t-2)+1.22Sales(t-1) -5.0Lead(t)

= Sales(t-3) -0.78Sales(t-2)+1.22Sales(t-1) -5.0Lead(t)")

Similar presentations

Models>")

is average of last m observations>")