Download presentation

Presentation is loading. Please wait.

1

Short-Term Financial Management

Chapter 7 – Managing Supplier Financing

2

Chapter 7 Agenda Managing Supplier Financing

Apply time value of money principles to the payment of accounts payable, decide when the cash discount is optimal, understand ethical issues involved in the payment decision, and assess payables using the balance fraction approach.

3

Cash Flow Timeline The firm is a system of cash flows.

These cash flows are unsynchronized and uncertain. The cash conversion period is the time between when cash is received versus paid. The shorter the cash conversion period, the more efficient the firm’s working capital. Note: The clock typically starts ticking when the order is received, not when the order is placed or the invoice received.

4

A/P Timing In Chapter 4, we studied optimal inventory levels and considered the impact on NPV from quantity and cash discounts. In this chapter, we take it a step further and decide when to pay A/P.

5

Managing Supplier Financing

Most firms buy inventory on credit, creating an Accounts Payable. The inventory is subsequently sold to customers on credit, creating an Accounts Receivable. In the meantime, the firm incurs expenses (e.g.: salaries, wages, taxes) for which payment has not yet been made, creating an Accrual. A/P and Accruals are generally due before A/R are received.

for which payment has not yet been made, creating an Accrual. A/P and Accruals are generally due before A/R are received.")

6

Managing Supplier Financing

A/P (also called Trade Credit) and Accruals represent spontaneous sources of financing for a firm, allowing the working capital cycle to continue without making cash disbursements. Trade credit is effectively a “free” source of financing. Firms establish policies on how to manage these accounts.

and Accruals represent spontaneous sources of financing for a firm, allowing the working capital cycle to continue without making cash disbursements. Trade credit is effectively a free source of financing. Firms establish policies on how to manage these accounts.")

7

Types of Supplier Financing

There are several types of purchase terms: Open Account Once credit is approved, the firm may repeatedly submit orders without reapplying for credit. Net Terms vs. Discount Terms Seasonal Dating Used in seasonal businesses (e.g.: toys). “2/10, net 30, dating 90” allows customers to take the 2% discount within 10 days or pay the invoice in full within 30 days after the 90 day period ends (120 days from purchase date; same as “2/10, net 120”). Consignment Payment is made only if the item is sold (e.g.: textbook inventory in college bookstores).

. 2/10, net 30, dating 90 allows customers to take the 2% discount within 10 days or pay the invoice in full within 30 days after the 90 day period ends (120 days from purchase date; same as 2/10, net 120 ). Consignment. Payment is made only if the item is sold (e.g.: textbook inventory in college bookstores).")

8

Supplier Financing The concept of A/P is the same as A/R, but from the opposite perspective. Say, a firm receives an invoice from a supplier with the terms 2/10, net 30. The firm pays $98 per $100 invoiced amount if they pay within 10 days. Taking the discount requires the firm to part with cash 20 days sooner, but it may deduct 2% from the amount owed. Should the firm take the discount?

9

Modeling A/P Timing We’ll look at two methods: NPV

Annualized Cash Discount Rate

10

A/P Payment Timing Options

Firm’s establish an A/P policy based on the number of days payment is delayed from the purchase date (DD), choosing from: Date of purchase. DD = 0 On or before end of cash discount period (DP). DD < DP On or before end of credit period (CP). DD < CP After credit period ends. DD > CP

, choosing from: Date of purchase. DD = 0. On or before end of cash discount period (DP). DD < DP. On or before end of credit period (CP). DD < CP. After credit period ends. DD > CP.")

11

A/P Payment Timing Options

Say, the terms offered are 2/10, net 30: Firms must determine when to pay invoices. Like before, we apply TVM principles to the payment timing of A/P, seeking the lowest NPV. Purchase DP CP >CP 0 Days 10 Days Days > 30 Days 1) (DD=0) 2) DD < DP 3) DD < CP 4) DD > CP

(DD=0) 2) DD < DP. 3) DD < CP. 4) DD > CP.")

12

A/P Decision Models - NPV

Deciding when to pay considers these rates: Cash discount rate (d) Annualized investment rate (i) Annualized borrowing rate (ib) Annualized late payment rate (fee) Shown are the variables associated with this decision:

Annualized investment rate (i) Annualized borrowing rate (ib) Annualized late payment rate (fee) Shown are the variables associated with this decision:")

13

A/P Decision Models - NPV

There are three Decision Models based on the timing of the delayed payment. Discount Model Credit Period Model Late Payment Model WE ARE DECIDING THE OPTIMAL TIMING OF DD.

14

Payment Decision Model #1

Discount Model - Payment made on or before the end of the cash discount period (DD < DP): PV of discounted invoice price

: PV of discounted invoice price.")

15

Payment Decision Model #2

Credit Period Model - Payment made on or before the end of the credit period (DD < CP): PV of full invoice price

: PV of full invoice price.")

16

Payment Decision Model #3

Late Payment Model - Payment made after the credit period ends (DD > CP): (IP) [1 +(DD-CP)(fee/365)] NPV = [1 + (DD)(i/365)] PV of full invoice price plus late fee

: (IP) [1 +(DD-CP)(fee/365)] NPV = [1 + (DD)(i/365)] PV of full invoice price plus late fee.")

17

Payment Decision Model Example

A firm receives an $100,000 invoice from a supplier with the terms 2/5, net 45. Should the firm: Take the discount? Pay within the credit period? Pay late?

18

Payment Decision Model Example

The invoice is $100,000 with terms of 2/5, net 45: Discount Model - The check amount for 0-5 days is $98,000…the NPV decreases as time passes. Credit Period Model - The check amount for 6-45 days is $100,000…the NPV decreases as time passes. Late Payment Model - The check amount for >45 days is $100,000 plus the late fee…the NPV increases as time passes. $98,000 mailed to supplier The numerator. $100,000 mailed to supplier $100,000 plus time-based fee mailed to supplier

19

Payment Decision Model Example

Discount Model [(IP)(1-d)] / [1 + (DD)(i/365)] [$100,000(1-.02)] / [1+(5)(.10/365)] = $97,866 The invoice is $100,000 with terms of 2/5, net 45. i = 10%

(1-d)] / [1 + (DD)(i/365)] [$100,000(1-.02)] / [1+(5)(.10/365)] = $97,866. The invoice is $100,000 with terms of 2/5, net 45. i = 10%")

20

Payment Decision Model Example

The invoice is $100,000 with terms of 2/5, net 45. Credit Period Model IP / [1 + (DD)(i/365)] $100,000 / [1+(45)(.10/365)] = $98,782

(i/365)] $100,000 / [1+(45)(.10/365)] = $98,782.")

21

Payment Decision Model Example

The invoice is $100,000 with terms of 2/5, net 45. Late Payment Model (IP) [1 +(DD-CP)(fee/365)] / [1 + (DD)(i/365)] ($100,000)[1+(48-45)(.18/365)] / [1+(48)(.10/365)] = $98,848

[1 +(DD-CP)(fee/365)] / [1 + (DD)(i/365)] ($100,000)[1+(48-45)(.18/365)] / [1+(48)(.10/365)] = $98,848.")

22

Payment Decision Model Example

The invoice is $100,000 with terms of 2/5, net 45: Paying on the fifth day and taking the discount provides the lowest NPV. Discount Model [(IP)(1-d)] / [1 + (DD)(i/365)] [$100,000(1-.02)] / [1+(5)(.10/365)] = $97,866 Credit Period Model IP / [1 + (DD)(i/365)] $100,000 / [1+(45)(.10/365)] = $98,782 Late Payment Model (IP) [1 +(DD-CP)(fee/365)] / [1 + (DD)(i/365)] ($100,000)[1+(48-45)(.18/365)] / [1+(48)(.10/365)] = $98,848

(1-d)] / [1 + (DD)(i/365)] [$100,000(1-.02)] / [1+(5)(.10/365)] = $97,866. Credit Period Model. IP / [1 + (DD)(i/365)] $100,000 / [1+(45)(.10/365)] = $98,782. Late Payment Model. (IP) [1 +(DD-CP)(fee/365)] / [1 + (DD)(i/365)] ($100,000)[1+(48-45)(.18/365)] / [1+(48)(.10/365)] = $98,848.")

23

Payment Decision Model Example

What if the investment rate (i) is 20%. Paying late now has the lowest NPV. Discount Model Credit Period Model Late Payment Model

is 20%. Paying late now has the lowest NPV. Discount Model. Credit Period Model. Late Payment Model.")

24

Payment Decision Model - NPV

While we calculated many possible dates before, only three need to be calculated: Last day of discount period. Last day of credit period. Some late date after credit period ends. In general: A/P should never be paid early. Pay on the last day of the discount period or the last day of the credit period. A/P should not be stretched past the credit period.

25

Paying Late If the late payment penalty fee (fee) is less than the firm's investment rate (i), the firm has a financial incentive to pay late. There are consequences to the firm’s brand for paying late: New orders will not be shipped until the account is current. The firm’s reputation and credit rating can be comprised.

26

Payment Decision Model - NPV

Since late payments should be avoided, it is the one of the first two models (Discount or Credit Period) with the lower NPV that is selected. Choose the smaller of: [(IP)(1-d)] / [1 + (DD)(i/365)] IP / [1 + (DD)(i/365)]

with the lower NPV that is selected. Choose the smaller of: [(IP)(1-d)] / [1 + (DD)(i/365)] IP / [1 + (DD)(i/365)]")

27

Alternative Decision Model

The reason we would forego the discount is to retain the funds to finance operations or to invest short-term. The cash discount is not an interest rate; rather, it is a discount off the amount of the invoice. It can be converted to an interest rate, and then be compared to i and ib. So, an alternative approach to calculating NPV is to compare the Annualized Cash Discount Rate (d).

.")

28

Alternative Decision Model

For terms, 2/5, net 45, if we forego the discount, we pay 2% more for the product. Said another way, we are paying 2% more to simply keep our cash for an extra 40 days. We can convert that to the annualized equivalent: The first piece, [d / (1- d)], provides the effective rate. For 2/5, net 45, this piece is [.02 / (.98)] = You are calculating the percent that 2% represents of 98%, since you are paying only 98% of the IP. Then, the second piece annualizes the effective rate based on how often it recurs. Here, the difference between 45 and 5 days (40 days) is the length of time you forego use of the funds in order to take the discount. So, 365/40 = times during a year the cycle replicates. Putting it together, x = 18.62%. This is now expressed as an interest rate and can be compared to other interest rates, like i and ib. If the i < kTC, the firm is better off taking the discount. If the i > kTC, the firm should keep the cash and forego the discount. Annualized Cash Discount Rate [The first expression is the effective discount rate (the discount divided by the discounted invoice) and the second expressions annualizes the rate (the number of times the rate would be realized in a year).]

], provides the effective rate. For 2/5, net 45, this piece is [.02 / (.98)] = You are calculating the percent that 2% represents of 98%, since you are paying only 98% of the IP. Then, the second piece annualizes the effective rate based on how often it recurs. Here, the difference between 45 and 5 days (40 days) is the length of time you forego use of the funds in order to take the discount. So, 365/40 = times during a year the cycle replicates. Putting it together, x = 18.62%. This is now expressed as an interest rate and can be compared to other interest rates, like i and ib. If the i < kTC, the firm is better off taking the discount. If the i > kTC, the firm should keep the cash and forego the discount. Annualized Cash Discount Rate. [The first expression is the effective discount rate (the discount divided by the discounted invoice) and the second expressions annualizes the rate (the number of times the rate would be realized in a year).]")

29

Alternative Decision Model

Assuming the firm does not have the cash, but has access to short-term credit, borrowing the money to take the discount might make sense if the annualized borrowing rate (ib) is less than annualized cash discount rate (kTC), given by: ib < = > kTC = [d / (1 – d)] [365 / (CP-DP)] If the ib < kTC, the firm should borrow to take the discount. If the ib > kTC, the firm should forego the discount.

is less than annualized cash discount rate (kTC), given by: ib < = > kTC = [d / (1 – d)] [365 / (CP-DP)] If the ib < kTC, the firm should borrow to take the discount. If the ib > kTC, the firm should forego the discount.")

30

Alternative Decision Example

For our decision, the annualized cash discount rate (kTC) is: [d / ( 1 – d)] [365/(CP-DP)] [.02/(1-.02)] [365/(45-5)] = 18.62% In our original analysis, with an i of 10%, the discount rate is the more favorable choice since 10% < 18.62%. If i = 20% Here, i > kTC > ib. 20% > 18.62%, so forego discount. However, since the firm has access to ST credit at 12%, borrowing to take the discount would make sense since kTC> ib. i > kTC > ib 20% > 18.62% > 12%

is: [d / ( 1 – d)] [365/(CP-DP)] [.02/(1-.02)] [365/(45-5)] = 18.62% In our original analysis, with an i of 10%, the discount rate is the more favorable choice since 10% < 18.62%. If i = 20% Here, i > kTC > ib. 20% > 18.62%, so forego discount. However, since the firm has access to ST credit at 12%, borrowing to take the discount would make sense since kTC> ib. i > kTC > ib. 20% > 18.62% > 12%")

31

Taking The Cash Discount

It almost always make sense to take the discount since the cost is high for not taking the discount. Research shows that: 51% of firms always take the discount. 40% sometimes take the discount. 9% take the discount regardless of when they pay!

32

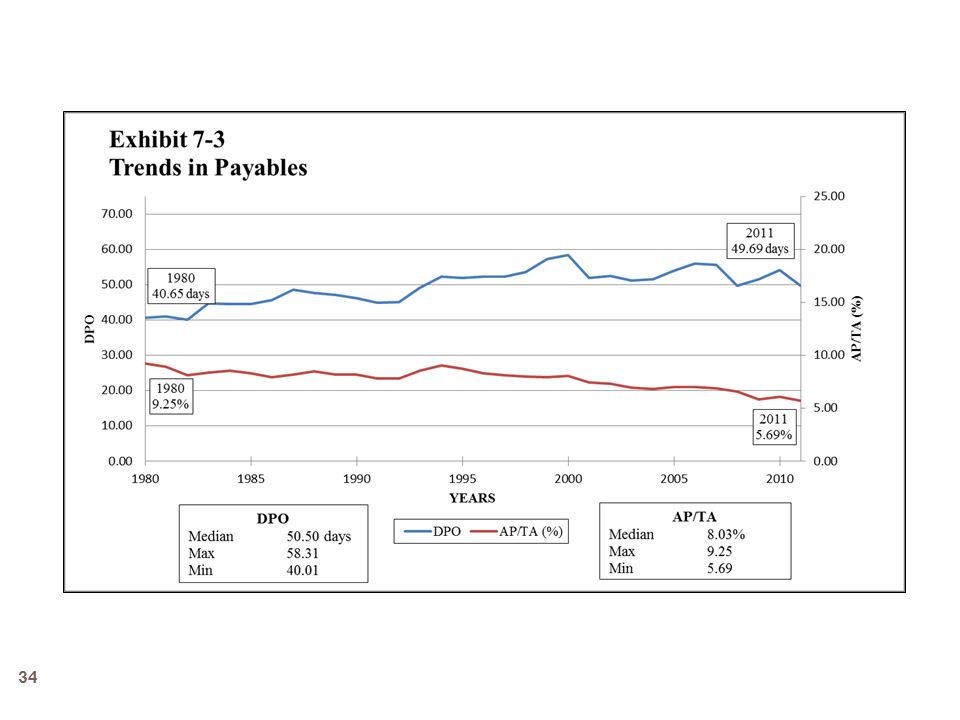

Managing Payables Credit Managers watch trends for:

Payables Turnover Ratio Days Payables Outstanding (DPO) Balance Fraction Approach Compares ratio of purchases to payables outstanding by month.

Balance Fraction Approach. Compares ratio of purchases to payables outstanding by month.")

33

Accruals Accruals represent an operating expense that has contributed to firm productivity but for which the expense has not been paid. A firm has minimal latitude in the timing of paying Accruals. e.g.: Lengthening accrued wages means delaying payment to your workers.

Similar presentations

. 7/11/03.>")