Download presentation

Presentation is loading. Please wait.

1

OUTLIER, HETEROSKEDASTICITY,AND NORMALITY

Robust Regression HAC Estimate of Standard Error Quantile Regression

8

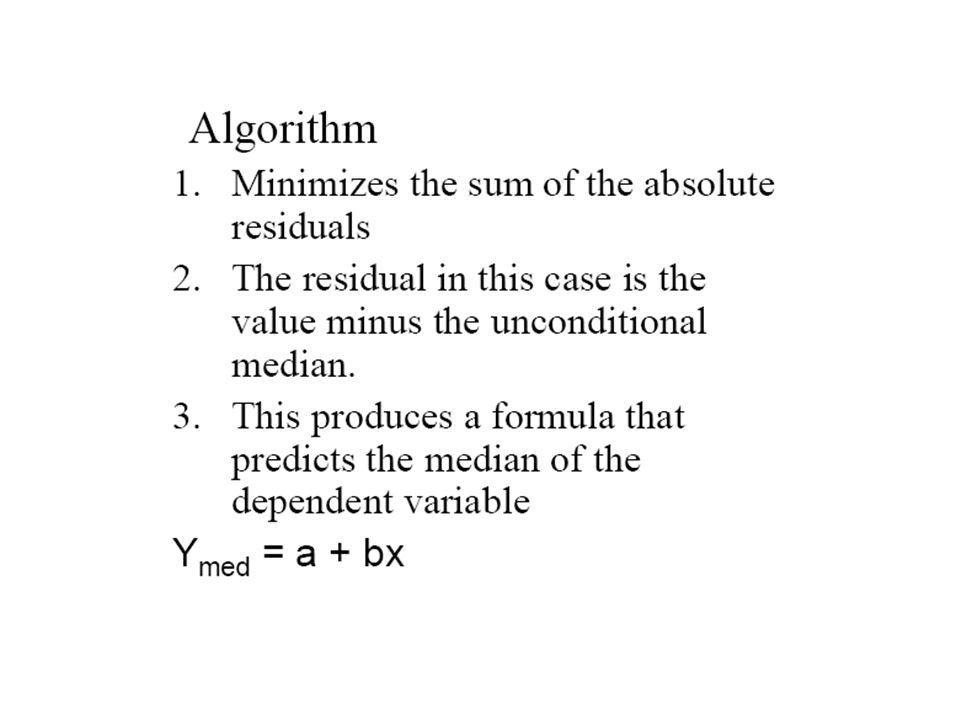

Robust regression analysis

alternative to a least squares regression model when fundamental assumptions are unfulfilled by the nature of the data resistant to the influence of outliers deal with residual problems Stata & E-Views

9

Alternatives of OLS A. White’s Standard Errors

OLS with HAC Estimate of Standard Error B. Weighted Least Squares Robust Regression C. Quantile Regression Median Regression Bootstrapping

13

If the residual distribution is normally distributed, the analyst can determine where the level of significance or rejection regions begin. Even if the sample size is large, the influence of the outlier can increase the local and possibly even the global error variance. This inflation of error variance decreases the efficiency of estimation.

15

OLS and Heteroskedasticity

What are the implications of heteroskedasticity for OLS? Under the Gauss–Markov assumptions (including homoskedasticity), OLS was the Best Linear Unbiased Estimator. Under heteroskedasticity, is OLS still Unbiased? Is OLS still Best?

, OLS was the Best Linear Unbiased Estimator. Under heteroskedasticity, is OLS still Unbiased Is OLS still Best")

16

A. Heteroskedasticity and Autocorrelation Consistent Variance Estimation

the robust White variance estimator rendered regression resistant to the heteroskedasticity problem. Harold White in 1980 showed that for asymptotic (large sample) estimation, the sample sum of squared error corrections approximated those of their population parameters under conditions of heteroskedasticity and yielded a heteroskedastically consistent sample variance estimate of the standard errors

estimation, the sample sum of squared error corrections approximated those of their population parameters under conditions of heteroskedasticity. and yielded a heteroskedastically consistent sample variance estimate of the standard errors.")

24

Quantile Regression Problem

The distribution of Y, the “dependent” variable, conditional on the covariate X, may have thick tails. The conditional distribution of Y may be asymmetric. The conditional distribution of Y may not be unimodal. Neither regression nor ANOVA will give us robust results. Outliers are problematic, the mean is pulled toward the skewed tail, multiple modes will not be revealed.

25

Reasons to use quantiles rather than means

Analysis of distribution rather than average Robustness Skewed data Interested in representative value Interested in tails of distribution Unequal variation of samples E.g. Income distribution is highly skewed so median relates more to typical person that mean.

26

Quantiles Cumulative Distribution Function Quantile Function

Discrete step function

27

Regression Line

28

The Perspective of Quantile Regression (QR)

")

31

Optimality Criteria Linear absolute loss Mean optimizes

Quantile τ optimizes I = 0,1 indicator function

32

Quantile Regression Absolute Loss vs. Quadratic Loss

Quadratic loss penalizes large errors very heavily. When p=.5 our best predictor is the median; it does not give as much weight to outliers. When p=.7 the loss is asymmetric; large positive errors are more heavily penalized then negative errors.

34

Simple Linear Regression

Food Expenditure vs Income Engel survey of 235 Belgian households Range of Quantiles Change of slope at different quantiles?

35

Bootstrapping When distributional normality and homoskedasticity assumptions are violated, many researchers resort to nonparametric bootstrapping methods

39

Bootstrap Confidence Limits

Similar presentations

Review>")