Download presentation

Presentation is loading. Please wait.

1

Functions of Federal Reserve District Banks Clear checks Issue new currency/withdraw damaged currency Make discount loans to banks in district Evaluate mergers/expansions of bank activities Liaison between business community and the Fed Examine bank holding companies and state-chartered member banks Collect data on local business conditions Research Money, Banking and the Financial System FRBNY’s special roles Bond and currency open market operations Supervise bank holding companies in NY district Member of Bank for International Settlements

2

How Independent is the Fed? Instrument independent Goal independent … undemocratic? – Political pressure would impart inflationary bias to monetary policy – Political business cycle? – Could facilitate Treasury financing of large budget deficits— accommodation Independent revenue Structured by Congress/accountable to Congress Presidential influence – Influence on Congress – Appoints members – Appoints chairman

3

European Central Bank Patterned after the Federal Reserve Central banks from each country play similar role as Fed district banks – Monetary operations are not centralized – ECB does not supervise and regulate financial institutions – More independent than Fed Maastricht Treaty would have to be revised to change ECB charge – But less goal independent than Fed Price Stability Rules

4

Multiple Creation of Money and Credit Fed buys something … MB up A bond A bank IOU Seller deposits proceed in Bank A Money supply increases Bank A’s deposits @ Fed up Bank A now has more reserves Bank A holds reserves against its new deposit (required + excess) Bank A makes loan to customer Borrower now has more deposits Money has just been created Borrower buys something Seller holds onto currency and deposits the rest in its Bank B Bank B’s deposits @ Fed up : The Fed’s Balance Sheet Owns Owes. Gold, Forex Federal Reserve Notes Currency in Circulation Vault Cash Reserves Bank IOUs Bank Deposits @ Fed (Discount loans) Bank A Bank B : Securities Gov’t Deposits Gov’t Bonds MBSs Miscellaneous Monetary BaseHigh Powered = MB Money = H = MB Note: MB = Currency + Bank Reserves = C + R M s = Currency + Demand Deposits = C + D

Bank A Bank B : Securities Gov’t Deposits Gov’t Bonds MBSs Miscellaneous Monetary BaseHigh Powered = MB Money = H = MB Note: MB = Currency + Bank Reserves = C + R M s = Currency + Demand Deposits = C + D.")

5

Money Supply Response

6

Reserve Requirements Depository Institutions Deregulation and Monetary Control Act of 1980 sets the reserve requirement the same for all depository institutions 3% of the first $48.3 million of checkable deposits; 10% of checkable deposits over $48.3 million The Fed can vary the 10% requirement between 8% to 14%

7

Deriving the Money Multiplier M = D + C MB = R + C = Required Reserves + Excess Reserves + C r = Required reserves/Deposits = RR / D RR= r x D e = Excess reserves/Deposits = ER/D ER = e x D

8

The Great Depression: Alternative Views The Descent, 1929 - 1933 Lionel Robbins/Friedrich von Hayek/Ludwig von Mises Prior credit expansion Malinvestment Bust Irving Fisher: Debt Deflation Crisis – Balance Sheet Recession John Maynard Keynes: Animal Spirits Investment BOOMS and busts : Milton Friedman and Anna Schwartz: Monetary Contraction

9

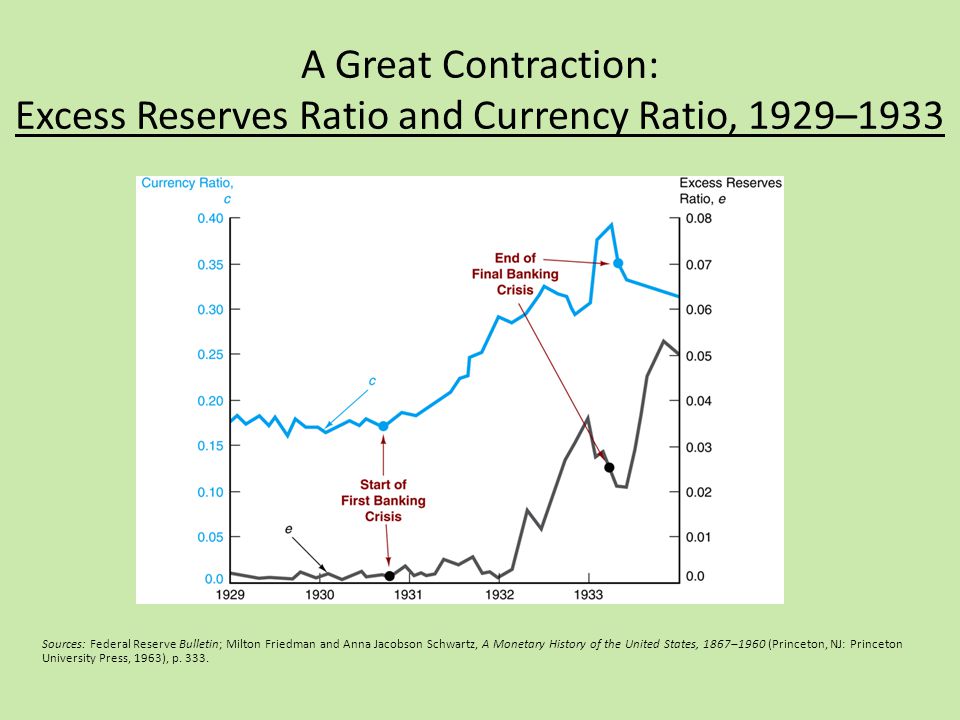

A Great Contraction: Excess Reserves Ratio and Currency Ratio, 1929–1933 Sources: Federal Reserve Bulletin; Milton Friedman and Anna Jacobson Schwartz, A Monetary History of the United States, 1867–1960 (Princeton, NJ: Princeton University Press, 1963), p. 333.

10

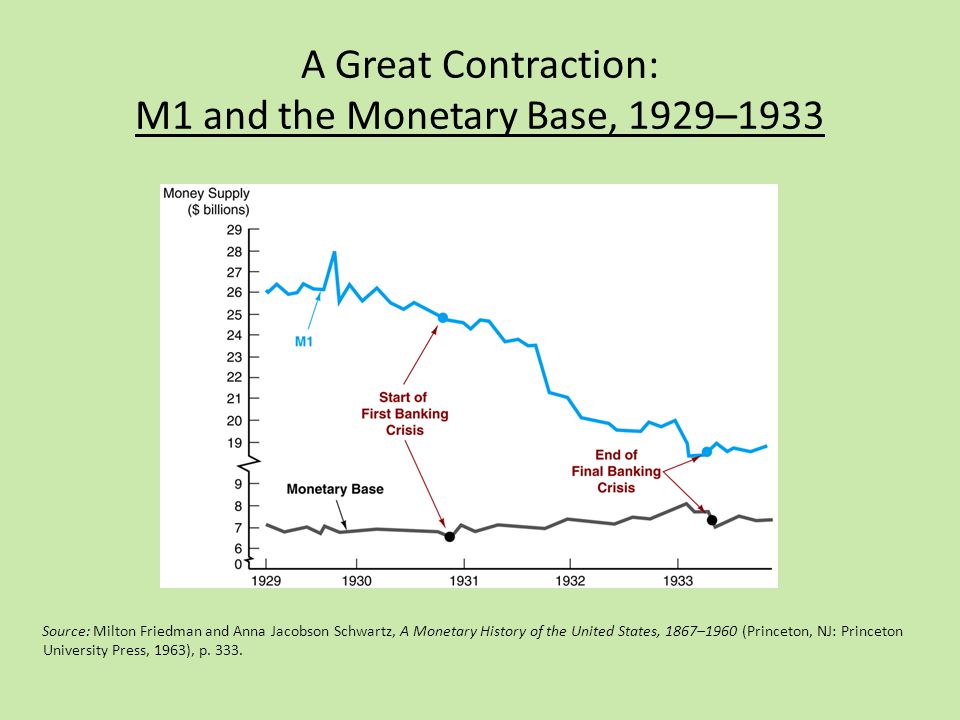

A Great Contraction: M1 and the Monetary Base, 1929–1933 Source: Milton Friedman and Anna Jacobson Schwartz, A Monetary History of the United States, 1867–1960 (Princeton, NJ: Princeton University Press, 1963), p. 333.

11

The Great Depression: Alternative Views The Descent, 1929 - 1933 Lionel Robbins/Friedrich von Hayek/Ludwig von Mises Prior credit expansion Malinvestment Bust Irving Fisher: Debt Deflation Crisis – Balance Sheet Recession John Maynard Keynes: Animal Spirits Investment BOOMS and busts : Milton Friedman and Anna Schwartz: Monetary Contraction Peter Temin: Consumption bust Charles Kindleberger: Lack of leader – lender of last resort Ben Bernanke: Agency costs Credit contraction

12

Ben S. Bernanke Nonmonetary Effects of the Financial Crisis in the Propagation of the Great Depression American Economic Review, June 1983 Why was the Great Depression so deep? Why did it last so long? The credit channel: a career is launched!

13

Why was the Great Depression so deep? Why did it last so long? Friedman and Schwartz: monetary contraction. Bernanke: true, but there’s more. Financial crisis – bank failures – reduced borrower net worth Increased Cost of Credit Intermediation (CCI) (A “rational” credit squeeze) Opposed to Keynes, Minsky, Kindleberger, Shiller: Animal spirits/Irrational exuberance Inherent instability of financial capitalism Bernanke: “push rationality postulate as far as it will go.”

(A rational credit squeeze) Opposed to Keynes, Minsky, Kindleberger, Shiller: Animal spirits/Irrational exuberance Inherent instability of financial capitalism Bernanke: push rationality postulate as far as it will go. .")

14

Cost of Credit Intermediation Intermediaries separate “good” from “bad” borrowers – Screening costs – Monitoring costs – Accounting costs – Bad loan losses Debt build-up in Roaring ‘20s Erosion of collateral values Either write more complex debt contracts or bear higher bad loan losses Either way, CCI rises and lending is reduced. Banks liquidate loans/rush to quality assets (T-bonds) Observe low interest rate…but money isn’t easy.

Observe low interest rate…but money isn’t easy..")

15

Real Consequences of Credit Contraction Aggregate supply impacts Reduced intermediation reduced allocative efficiency Large, indivisible projects not funded Production Possibilities Frontier shifts inward Upward shift of AS Y down, i up … but i didn’t rise Aggregate demand impacts High cost of credit when CCI rises would-be borrowers buy less stuff (substitution effect) AD down Y down and i down … as observed in Great Depression

AD down Y down and i down … as observed in Great Depression")

16

Why did it last so long? New credit channels emerge only slowly. Insolvent debtors recover only slowly. – Credit difficulties for small business lasted 2 + years after 1933 banking holiday – Very little mortgage lending occurred for years after 1933 {Bernanke uses narrative methodology to make these points. Cites comments of contemporary authorities, news items, etc.} New Deal recovery: Rehabilitating the financial system was only positive contribution. » New Deal fiscal stimulus was weak » National Industrial Recovery Act (cartelization) hurt recovery

hurt recovery.")

17

The Great Depression: Alternative Views The Descent, 1929 - 1933 Lionel Robbins/Friedrich von Hayek/Ludwig von Mises Prior credit expansion Malinvestment Bust Irving Fisher: Debt Deflation Crisis – Balance Sheet Recession John Maynard Keynes: Animal Spirits Investment BOOMS and busts : Milton Friedman and Anna Schwartz: Monetary Contraction Peter Temin: Consumption bust Charles Kindleberger: Lack of leader – lack of lender of last resort Ben Bernanke: Agency costs Credit contraction Barry Eichengreen/Ben Bernanke: Golden Fetters Recovery: 1933 – 1937 Christina Romer: Monetary expansion Barry Eichengreen/Ben Bernanke: Abandoning Gold M - expansion Peter Temin/Gauti Eggertsson: Reflationary expectations

18

Tools of Monetary Policy Open market operations – Affect the quantity of reserves and the monetary base Changes in borrowed reserves – Affect the monetary base Changes in reserve requirements – Affect the money multiplier Federal funds rate: the interest rate on overnight loans of reserves from one bank to another – Primary instrument of monetary policy

19

Equilibrium in the Market for Reserves Interest paid on excess reserves Primary credit rate Discount rate Federal funds rate

20

Response to an Open Market Operation By paying interest on reserves, the Fed can expand its balance sheet – inject liquidity into financial system by lending via exotic “facilities” – without increasing the money supply. The increased NBRs are absorbed as excess reserves. When the Fed buys something on the open market, the quantity of non-borrowed reserves (and total reserves) in the banking system increases, driving down the federal funds rate.

in the banking system increases, driving down the federal funds rate..")

21

How the Federal Reserve’s Operating Procedures Limit Fluctuations in the Federal Funds Rate By paying interest on reserves, the Fed has been able to increase its balance sheet (MB) without much increasing the money supply. Once the quantity of non-borrowed reserves in the banking system drives the federal funds rate to i er, banks hold on to excess reserves.

22

Advantages and Disadvantages of Discount Policy Used to perform role of lender of last resort – Important during the subprime financial crisis of 2007-2008. Cannot be controlled by the Fed; the decision maker is the bank Discount facility is used as a backup facility to prevent the federal funds rate from rising too far above the target

23

Open Market Operations Dynamic open market operations Defensive open market operations Primary dealers TRAPS (Trading Room Automated Processing System linked to primary dealers) Repurchase agreements Matched sale-purchase agreements Outright transactions

Repurchase agreements Matched sale-purchase agreements Outright transactions")

24

List of the Primary Government Securities Dealers Reporting to the Government Securities Dealers Statistics Unit of the Federal Reserve Bank of New York BNP Paribas Securities Corp. Barclays Capital Inc. Cantor Fitzgerald & Co. Citigroup Global Markets Inc. Credit Suisse Securities (USA) LLC Daiwa Capital Markets America Inc. Deutsche Bank Securities Inc. Goldman, Sachs & Co. HSBC Securities (USA) Inc. Jefferies & Company, Inc. J.P. Morgan Securities LLC Merrill Lynch, Pierce, Fenner & Smith Incorporated Mizuho Securities USA Inc. Morgan Stanley & Co. Incorporated Nomura Securities International, Inc. RBC Capital Markets, LLC RBS Securities Inc. UBS Securities LLC.

LLC Daiwa Capital Markets America Inc. Deutsche Bank Securities Inc. Goldman, Sachs & Co. HSBC Securities (USA) Inc. Jefferies & Company, Inc. J.P. Morgan Securities LLC Merrill Lynch, Pierce, Fenner & Smith Incorporated Mizuho Securities USA Inc. Morgan Stanley & Co. Incorporated Nomura Securities International, Inc. RBC Capital Markets, LLC RBS Securities Inc. UBS Securities LLC..")

Similar presentations