Download presentation

Presentation is loading. Please wait.

1

LIFE NAT Kick off & platform meeting LATVIA 2006 Aneta Gajda, Financial Desks EC DG ENV – LIFE Unit

2

Common Provisions (CP) Financial Forms General hints for financial reporting Standard Audit Report

Financial Forms General hints for financial reporting Standard Audit Report")

3

COMMON PROVISIONS (CP) SHORT OVERVIEW

SHORT OVERVIEW")

4

CP - a binding document New from 2005 (before – SAP) CP - determines beneficiary’s and partner’s rights and obligations for the duration of the project (+ 5 years after)

CP - determines beneficiary’s and partner’s rights and obligations for the duration of the project (+ 5 years after)")

5

CP define: Project actors (1) Beneficiary (Art 4): Solely legally and financially responsible and receives the EU- contribution Not allowed to act as sub-contractor or supplier to other partners Single point of contact for the Commission Notify a Copy of any agreements Beneficiary-partners (Art 4.7 ) Partner (s) (Art 5): Contributes to one or several of the tasks and to the costs incurred Not allowed to act as sub-contractor to the beneficiary or other partners No direct reporting to the Commission Art 4.6 & 5.3 Analytical accounting (cost centre accounting) New from 2005

Beneficiary (Art 4): Solely legally and financially responsible and receives the EU- contribution Not allowed to act as sub-contractor or supplier to other partners Single point of contact for the Commission Notify a Copy of any agreements Beneficiary-partners (Art 4.7 ) Partner (s) (Art 5): Contributes to one or several of the tasks and to the costs incurred Not allowed to act as sub-contractor to the beneficiary or other partners No direct reporting to the Commission Art 4.6 & 5.3 Analytical accounting (cost centre accounting) New from 2005")

6

CP define: Project actors (2) Co-financer (s) (Art 7): Contributes with financial resources to the project Does not benefit from the Community contribution Is not required to be directly involved in the project Subcontractor (s) (Art 6): Provides external services + specific tasks of a fixed duration Shall not be a partner Clear reference to the LIFE-project shall be included in the invoices/order form Art 6.4 : Public tenders obligatory for public beneficiary/partner Competitive tenders for private beneficiary/partners New from 2005

Co-financer (s) (Art 7): Contributes with financial resources to the project Does not benefit from the Community contribution Is not required to be directly involved in the project Subcontractor (s) (Art 6): Provides external services + specific tasks of a fixed duration Shall not be a partner Clear reference to the LIFE-project shall be included in the invoices/order form Art 6.4 : Public tenders obligatory for public beneficiary/partner Competitive tenders for private beneficiary/partners New from 2005")

7

CP Define: Mechanism of LIFE financial support (Art 20) The Grant Agreement foresees a maximum amount of contribution and a maximum percentage of funding to the eligible costs The final amount of the contribution is determined by applying the percentage defined in the contract to the eligible cost incurred but with the limit of maximum amount as specified in the contract

The Grant Agreement foresees a maximum amount of contribution and a maximum percentage of funding to the eligible costs The final amount of the contribution is determined by applying the percentage defined in the contract to the eligible cost incurred but with the limit of maximum amount as specified in the contract")

8

CP define: Eligible costs (Art 21.1 -21.12) Provided for in the provisional budget/ Directly necessary for the project Incurred during the lifetime of the project: - Legal obligation to pay (the cost) has been contracted after the project start and before the end date - Execution of corresponding action starts after the project start and is completed before the end date - Full payment before submission of final reports Exception: Costs for independent audit can be executed after project end date – but must be terminated, invoiced and fully paid before submission of final report, and auditor is given the assignment before the project ends

Provided for in the provisional budget/ Directly necessary for the project Incurred during the lifetime of the project: - Legal obligation to pay (the cost) has been contracted after the project start and before the end date - Execution of corresponding action starts after the project start and is completed before the end date - Full payment before submission of final reports Exception: Costs for independent audit can be executed after project end date – but must be terminated, invoiced and fully paid before submission of final report, and auditor is given the assignment before the project ends")

9

CP define: Ineligible costs (Art 22) Some examples: Exchange rate losses Debtors interest/interest on borrowed capital Services in kind (e.g. voluntary work) Licence or patent fees related to the protection of intellectual property right

Licence or patent fees related to the protection of intellectual property right.")

10

CP define: Payments (Art 23) The First pre-financing payment (40%) The Second pre-financing payment (30%) at least 150% of the first pre-financing used New from 2005 (other conditions for the projects of 2004 and earlier) The Balance final payment

The First pre-financing payment (40%) The Second pre-financing payment (30%) at least 150% of the first pre-financing used New from 2005 (other conditions for the projects of 2004 and earlier) The Balance final payment")

11

FINANCIAL FORMS Where to find the model of financial forms: http://ec.europa.eu/environment/life/toolbox/fi nancial_sheet.htm

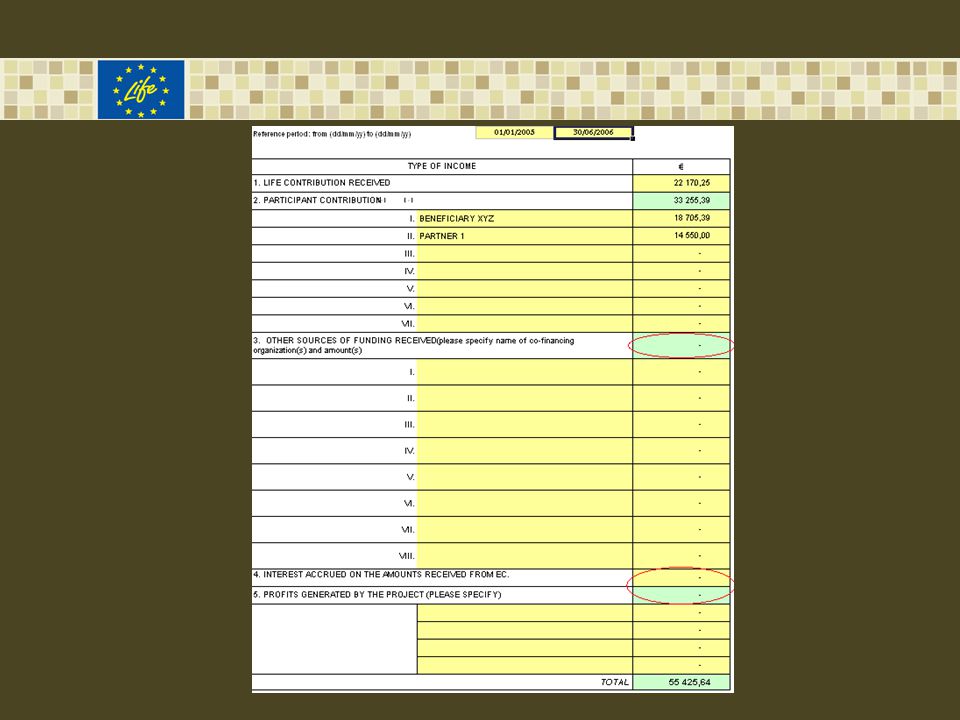

14

Statement of expenditure To be delivered: Project consolidated statement of expenditure, completed and signed by beneficiary Participant statement of expenditure, completed and signed by each participant

17

Personnel costs (Art 21.2) (1) Relate to costs of employees – not to costs of consultants etc. (external assistance) Service contracts with individuals – obligatory conditions: work at beneficiary’s/partner’s premises, under his supervision and complies with the relevant national legislation (New from 2005) Costs of civil servants/public employees -- only if work not standard activity -- for staff already working to be covered by the own contribution (New from 2005) Actual (annual) gross salary or wages plus obligatory social charges, borne by the employer and not included in the salary, e.g. contributions to pension, sickness and unemployment schemes

Service contracts with individuals – obligatory conditions: work at beneficiary’s/partner’s premises, under his supervision and complies with the relevant national legislation (New from 2005) Costs of civil servants/public employees -- only if work not standard activity -- for staff already working to be covered by the own contribution (New from 2005) Actual (annual) gross salary or wages plus obligatory social charges, borne by the employer and not included in the salary, e.g. contributions to pension, sickness and unemployment schemes.")

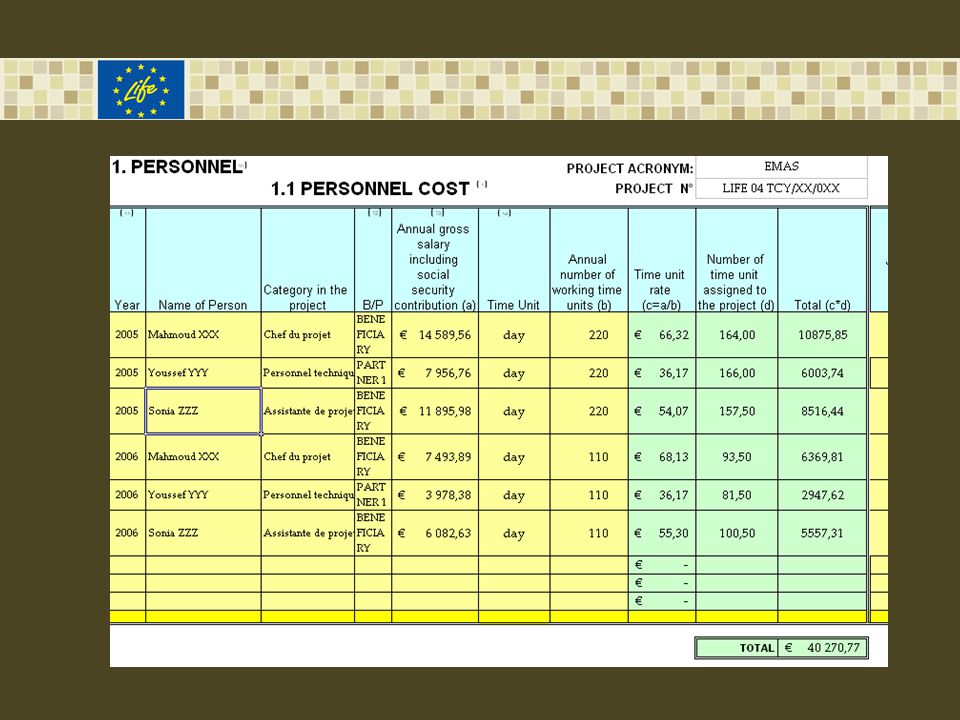

20

Personnel costs (Art 21.2) (2) Actual time devoted to the project : to be registered by means of time sheets which should be established timely, signed by the staff member and certified by the responsible project manager Monitoring of personnel costs: Model - monthly time-sheet http://ec.europa.eu/environment/life/toolbox/timesheet.htm

(2) Actual time devoted to the project : to be registered by means of time sheets which should be established timely, signed by the staff member and certified by the responsible project manager Monitoring of personnel costs: Model - monthly time-sheet")

21

Travel costs (Art 21.3) Shall be charged in accordance with the internal rules of the participant Travel outside EU and not already envisaged in the proposal - Require prior approval of the Commission Should in general relate to persons accounted for under “personnel costs” (travel costs of consultants should be part of their service contract/fees)

Shall be charged in accordance with the internal rules of the participant Travel outside EU and not already envisaged in the proposal - Require prior approval of the Commission Should in general relate to persons accounted for under personnel costs (travel costs of consultants should be part of their service contract/fees)")

23

External assistance costs (Art 21.4) External assistance costs may not represent more than 35% of the total eligible costs unless explicitly foreseen in the project Relate to the purchase of services, not of goods ATTENTION: such costs must be directly and exclusively attributed to the LIFE project NOT: costs of independent audit – explicitly attributed to “other costs” NOT: costs related to leasing/purchase of durable goods or consumables (attribute to those cost categories)

External assistance costs may not represent more than 35% of the total eligible costs unless explicitly foreseen in the project Relate to the purchase of services, not of goods ATTENTION: such costs must be directly and exclusively attributed to the LIFE project NOT: costs of independent audit – explicitly attributed to other costs NOT: costs related to leasing/purchase of durable goods or consumables (attribute to those cost categories)")

25

Durable goods (Art 21.5 to Art 21.7) Relate to expenditure on purchase, manufacture or lease of equipment/infrastructure (placed on the inventory of durable goods, treated as capital expenditure, purchased or leased at normal market costs) Purchased within project duration BUT not at the last days of the project duration Durable goods: Depreciation of expenditure on durable goods – beneficiary/partners apply own rules BUT ceilings: infrastructure 25%, equipment 50% prototypes 100%

Relate to expenditure on purchase, manufacture or lease of equipment/infrastructure (placed on the inventory of durable goods, treated as capital expenditure, purchased or leased at normal market costs) Purchased within project duration BUT not at the last days of the project duration Durable goods: Depreciation of expenditure on durable goods – beneficiary/partners apply own rules BUT ceilings: infrastructure 25%, equipment 50% prototypes 100%")

26

Durable goods (Art 21.7) For LIFE-Nature projects, the cost incurred for durable goods by public authorities or non-governmental/non-profit organisations intrinsically connected with implementation of the project, explicitly envisaged and used to a significant degree within its duration shall be considered eligible in full. Such eligibility shall be subject to the beneficiary and partners undertaking to continue to assign these goods definitively to nature conservation activities beyond the end of the project co-financed under LIFE-Nature.

27

Consumable material (Art 21.10) Relate to the purchase, manufacture, repair or use of any material, goods or equipment which: - are not on the inventory of durable goods, - are not treated as capital expenditure, - are specifically related to implementation of the project. General consumables/supplies will be charged to the “overheads” cost category.

29

Other costs (Art 21.11) Relate to costs not falling within another defined cost category Examples: costs for bank guarantee (covering the project period + 6 months), costs of independent audit Other examples: bank fees for money transfers, inscription fees

Relate to costs not falling within another defined cost category Examples: costs for bank guarantee (covering the project period + 6 months), costs of independent audit Other examples: bank fees for money transfers, inscription fees")

31

Overheads (Art 21.12) indirect costs – not include costs assigned to another budget heading; needed to employ/ manage/ accommodate/ support personnel working on the project flat rate funding of 7% of the total amount of eligible direct costs New from 2005

indirect costs – not include costs assigned to another budget heading; needed to employ/ manage/ accommodate/ support personnel working on the project flat rate funding of 7% of the total amount of eligible direct costs New from 2005")

32

GENERAL HINTS FOR FINANCIAL REPORTING

33

Study carefully the Common Provisions (CP) and « re-read » them whenever a problem of administrative-financial nature occurs Distribute the CP to all project partners and make sure that CP are applied by them Oblige your partners to forward their project accounting data to you regularly.

and « re-read » them whenever a problem of administrative-financial nature occurs Distribute the CP to all project partners and make sure that CP are applied by them Oblige your partners to forward their project accounting data to you regularly.")

34

Keep the project accounting up-to-date, including regular update of the financial forms Introduce all data requested, i.e. complete all “cells” of the financial forms, or explain why they remain “empty” Describe with sufficient detail the types of purchased services/goods and their link with the work programme or action Keep all appropriate supporting documentation for all expenditure and income – including copies of the partners’ supporting documentation Supporting documentation - Examples: e.g. purchase orders, invoices, payment proofs, public tendering documents for personnel: monthly salary slips, presence/time sheets, calculation of social charges if not included in salary

35

VAT: For VAT charges to be considered eligible the beneficiary must provide a declaration from the relevant national authorities that it and/or its partners must pay and may not recover the VAT for the assets and services required for the project. Currency of the reports: only the Euro (€), Art. 25.4 Payments made in different currencies: use the exchange rate applied by the European Central Bank on the first day of the month in which the financial report is presented to the Commission Where to find: http://ec.europa.eu/budget/inforeuro/index.cfm

, Art Payments made in different currencies: use the exchange rate applied by the European Central Bank on the first day of the month in which the financial report is presented to the Commission Where to find:")

36

INDEPENDENT AUDIT New from 2005 Maximum amount of grant ≥ € 500.000 pre-financing (s) > € 750.000 Final payment request > € 150.000

> € Final payment request > €")

37

External/Independent Auditor’s Report Find a model of the standard audit report at: http://ec.europa.eu/environment/life/toolbox/standardaudit.htm

38

Thank you for your attention !

Similar presentations

ETC Regulation 16th meeting of the Expert Group on.>")

is co-funded by the European Community's ICT Programme under FP7 6 - Resource Allocation and Budgeting.>")

EXPENDITURES.>")