Download presentation

Presentation is loading. Please wait.

1

LGPS 2014 Essex Pension Fund March 2014 Matt Mott

2

LGPS 2014 2014 Scheme Overview 50/50 section APC AVC

Flexible retirement Protections Pensionable Pay & Contributions Employer Responsibilities & Discretions

3

2014 Scheme Overview CARE Scheme (Career Average Revalued Earnings)

Accrual rate of 1/49th - It’s better Annual revaluation by CPI Normal retirement age (NRA) is State Pension Age (SPA) Find your SPA at Voluntary retirement from age 55 (without employer consent) Flexible retirement From age 55 (with employer consent)

is State Pension Age (SPA) Find your SPA at Voluntary retirement from age 55 (without employer consent) Flexible retirement From age 55 (with employer consent)")

4

2014 Scheme Overview 50/50 section

Benefits accrued prior to 1st April 2014 protected Protection for those within 10 years of retirement in April 2012 Actuarial reductions for ER will differ for different periods of membership Pensionable pay is actual pay Vesting (refund) period increased to 2 years Average member contributions of 6.5% Cost envelope of 19.5%

period increased to 2 years. Average member contributions of 6.5% Cost envelope of 19.5%")

5

Contributions bands Band pensionable pay range for an employment

Contribution rate for that employment 1 Up to £13,500 5.5% 2 £13,501 to £21,000 5.8% 3 £21,001 to £34,000 6.5% 4 £34,001 to £43,000 6.8% 5 £43,001 to £60,000 8.5% 6 £60,001 to £85,000 9.9% 7 £85,001 to £100,000 10.5% 8 £100,001 to £150,000 11.4% 9 £150,001 or more 12.5%

6

2014 Scheme Overview All other ancillary benefits to remain the same

Additional Pension Contributions (APC) Pension accounts Automatic Aggregation Link to Public Service schemes AVC Benefit Regulations Received September 2013

Pension accounts. Automatic Aggregation. Link to Public Service schemes. AVC. Benefit Regulations Received September")

7

CARE Example Pay Accrual Pension CPI Total Pension Year 1 £20,000 1/49

£408.16 n/a Year 2 £22,000 £448.98 £12.65 £869.79 Year 3 £24,000 £489.80 £45.23 £

8

50/50 section Employee pays ½ contributions Benefits accrue at 1/98th

All other ancillary benefits to remain the same Temporary arrangement Employees put in main section on AE re-enrolment date Cannot begin or continue APC Unless for “lost pension”

9

50/50 section During periods of nil pay sick leave 50/50 section members must be re-enrolled into main section Employers must maintain full contributions

10

Death benefits Children’s benefits Spouses benefits Civil partners

Lump sum death grant Civil partners Co-habiting partners OK, so that was all about retiring from or leave the scheme, but as some of you may be aware there are other benefits of being in the scheme - one of them being death benefits. Now death benefits can be paid from the scheme if you die in service, or die having left employment but with a set of deferred benefits, and also if you die after retirement. The first of the benefits that would become payable is the lump sum death grant. Now this would be 3 times your final pay (remember final pay is normally your pensionable pay in the year up to the last day of pensionable employment). I must however stress that if you work part-time hours this is one time that the final pay is not calculated using whole-time pay levels. Now, the lump sum is normally payable to your estate, however you can complete a nomination form, nominating a person, or persons, to receive this lump sum on your death. However, if we find out that your circumstances have changed but that you have not changed your nomination form, then we may decide just to pay the money to your estate. In the majority of cases, however, we will honour the nomination form. There are a couple of benefits of completing a nomination form - first of all, if payment is made to a nominee, or nominees, it does not form part of your estate, and therefore it could result in less inheritance tax being paid, if any is paid at all. Furthermore it may save the people dealing with your estate from having to obtain a document known as the PROBATE or letters of administration if no will (dies intestate) - this is a document that we require sight of before we can make any payments to an estate. (NOT IF LESS THAN £5K) The second type of death benefit is the widow or widower’s pension. This is payable if you are married at the time of your death. This pension is normally calculated as a proportion of benefits accrued for each year to age 65 that would have been paid to you if you had retired on ill-health grounds (in new scheme tier 1) Long term = 50% of pre 08 and 37.5% of post 08! However, there will be at least 3 months immediately following death, where the widow or widower’s pension will be equal to your final pay. (dependant on if retirement occurred pre or post 2008) And finally if you have children AGED UNDER 18 or who are in full-time education and aged under 23 or unable to work due to illness (permanently incapacitated) , then small pensions could be paid in respect of them during the period whilst they are still in education or ill. To give you a rough idea, the children’s pensions could be approximately ¼ (1/3 if no survivor) of your prospective ill-health pension. If you have more than two children then a restriction to the overall value of the children’s pensions would apply. PB – PROPORTION PENSION IN PAYMENT, 5X DEFERRED PENSION AS DG 10

. I must however stress that if you work part-time hours this is one time that the final pay is not calculated using whole-time pay levels. Now, the lump sum is normally payable to your estate, however you can complete a nomination form, nominating a person, or persons, to receive this lump sum on your death. However, if we find out that your circumstances have changed but that you have not changed your nomination form, then we may decide just to pay the money to your estate. In the majority of cases, however, we will honour the nomination form. There are a couple of benefits of completing a nomination form - first of all, if payment is made to a nominee, or nominees, it does not form part of your estate, and therefore it could result in less inheritance tax being paid, if any is paid at all. Furthermore it may save the people dealing with your estate from having to obtain a document known as the PROBATE or letters of administration if no will (dies intestate) - this is a document that we require sight of before we can make any payments to an estate. (NOT IF LESS THAN £5K) The second type of death benefit is the widow or widower’s pension. This is payable if you are married at the time of your death. This pension is normally calculated as a proportion of benefits accrued for each year to age 65 that would have been paid to you if you had retired on ill-health grounds (in new scheme tier 1) Long term = 50% of pre 08 and 37.5% of post 08! However, there will be at least 3 months immediately following death, where the widow or widower’s pension will be equal to your final pay. (dependant on if retirement occurred pre or post 2008) And finally if you have children AGED UNDER 18 or who are in full-time education and aged under 23 or unable to work due to illness (permanently incapacitated) , then small pensions could be paid in respect of them during the period whilst they are still in education or ill. To give you a rough idea, the children’s pensions could be approximately ¼ (1/3 if no survivor) of your prospective ill-health pension. If you have more than two children then a restriction to the overall value of the children’s pensions would apply. PB – PROPORTION PENSION IN PAYMENT, 5X DEFERRED PENSION AS DG. 10.")

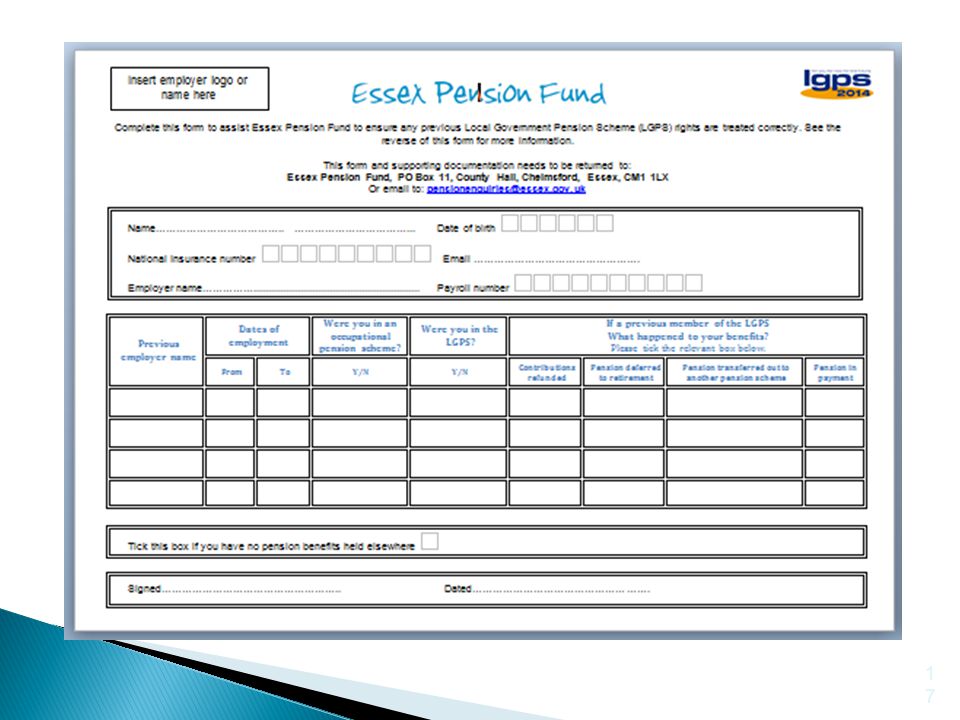

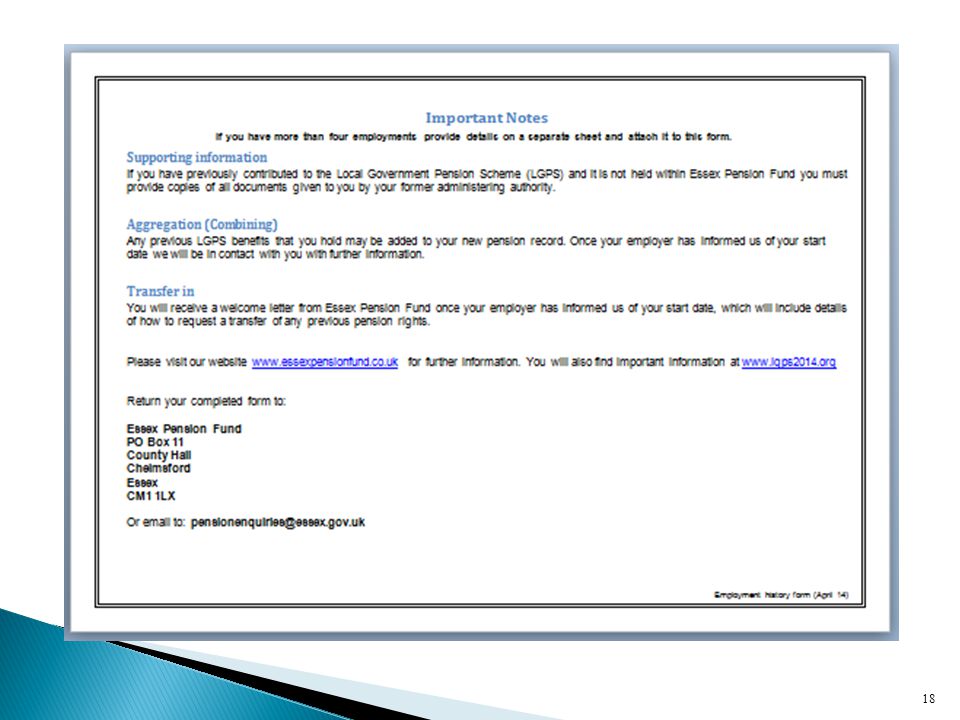

11

APC Maximum £6,500 Monthly or lump sum contribution

A scheme member benefit only Must cease if employee elects for 50/50 section Also shared cost APC Contribution split must be agreed Buy extra pension

12

APC Used to buy “lost pension” Authorised unpaid leave

Child related unpaid leave Strike* If election is made within 30 days of return to work: Employee pays 1/3 Employer 2/3 (except strike*) Election after 30 days of return to work: Full cost paid by employee

Election after 30 days of return to work: Full cost paid by employee.")

13

AVC Current 2014 regulations

Contributions up to 100% of pay after LGPS contributions and NI Tax free cash 100% of AVC fund Added to 25% LGPS lump sum = 55% tax charge Intention (probable amendment) 2014 regulations Tax free cash restricted to 25% of fund Added to 25% LGPS lump sum = Nil tax charge Pre 1 April AVC administered by 2008 regulations

2014 regulations. Tax free cash restricted to 25% of fund. Added to 25% LGPS lump sum = Nil tax charge. Pre 1 April AVC administered by 2008 regulations.")

14

Flexible Retirement From age 55 with employer consent

Actuarial reduction or strain may apply Employees can choose to receive payment: of all benefits of all pre 2008 benefits of all, part or none post 2008 benefits of all, part or none post 2014 benefits Plus “additional benefits” in accordance with actuarial guidance issued by the Secretary of State

15

Protections - Pre 2014 membership

All membership accrued pre 1 April 2014 protected LGPS 2008 regulations apply including: 60th & 80th If applicable lump sums Normal retirement age 65 Link to final salary at eventual retirement Members in receipt of a pension or a deferred benefits are unaffected by LGPS 2014

16

Protections - Pre 2014 membership

Protections can be lost if 2008 deferred benefits are aggregated with current 2014 membership if employee has had a break in public sector pension schemes of more than 5 years

19

Protections - The Underpin

Active members on 31 March 2008 Were within 10 years of NRA on 1 April 2012 Receive pension on or after NRA Do not have more than 5 year break in membership of any public sector pensions The underpin is only paid if the 2008 scheme (had it continued) provides a better pension than LGPS 2014

provides a better pension than LGPS")

20

Protections – Rule of 85 Is so complicated I am not going to try and explain it!! Example: 58 year old member Rule of 85 satisfied Can retire and immediately receive pension Will there be an actuarial reduction? Yes,11% of pension and 6% of lump sum!

21

Protections – Rule of 85 Why? Age plus membership in whole years = 85

Who has protection? = In before 1 October 2006 This protection continues from April 2014 *Does not apply to* new option of drawing your pension from age 55-60

22

Protections – Rule of 85 Exercise discretion to waive the reduction

If so you will have a strain cost Employers must publish a policy Essential to read the HR and Payroll guides

23

Pay & Contributions Actual pensionable pay (PP) Including overtime

Does not include expenses Assumed Pensionable Pay (APP) What the employee would have earned Replaces notional pay See HR/Payroll guides 1/2 employee contribution rate if 50/50 elected Employer contributions always paid in full

What the employee would have earned. Replaces notional pay. See HR/Payroll guides. 1/2 employee contribution rate if 50/50 elected. Employer contributions always paid in full.")

24

Pay & Contributions Final Pay (2008 definition)

Required for all pre 2014 membership 10 year Underpin Also PT hours and average hours Added years and CoP Will you know who these apply to? Therefore, we require them for all employees!! Contribution bands will be revalued every 3 years only Employers to review employee contributions Annually in April When material change occurs ie promotion

25

Employer Responsibilities

To provide starter details to the Fund within 1 month By spreadsheet To request within 3 months of employee start date employment and LGPS histories Inform employee: Contractual enrolment Auto Enrolment Contribution rate payable They can opt out Where to find scheme information ie website!

26

Employer Responsibilities

Upon 50/50 section election provide employee with impact of pension loss Upon AE re-enrolment all 50/50 section members must be put into main section For periods of nil pay sick leave 50/50 section members must be put into main section Inform employees where to find the opt out form But not to supply it!! Opt out with less than 3 months membership, refund contributions and notify the Fund

27

Employer Responsibilities

Opt out with over 3 months membership, send the Fund normal leaver forms APC for “lost pension” employers must: Enable employee to make election within 30 days Should ideally: inform employee of the amount of lost pay inform employee of the amount of lost pension To provide data on spreadsheets (do not amend) each month Same data fields for all employees To provide end of year data (correct) by date specified by Fund, usually mid April

each month. Same data fields for all employees. To provide end of year data (correct) by date specified by Fund, usually mid April.")

28

50 50 switch form

29

Main switch form

30

Join the scheme form

31

Opt out form

32

Employer Responsibilities

All leaving details must be provided within 1 month of date of leaving: All pay figures Periods of membership Main Section 50/50 Section Contribution amounts

33

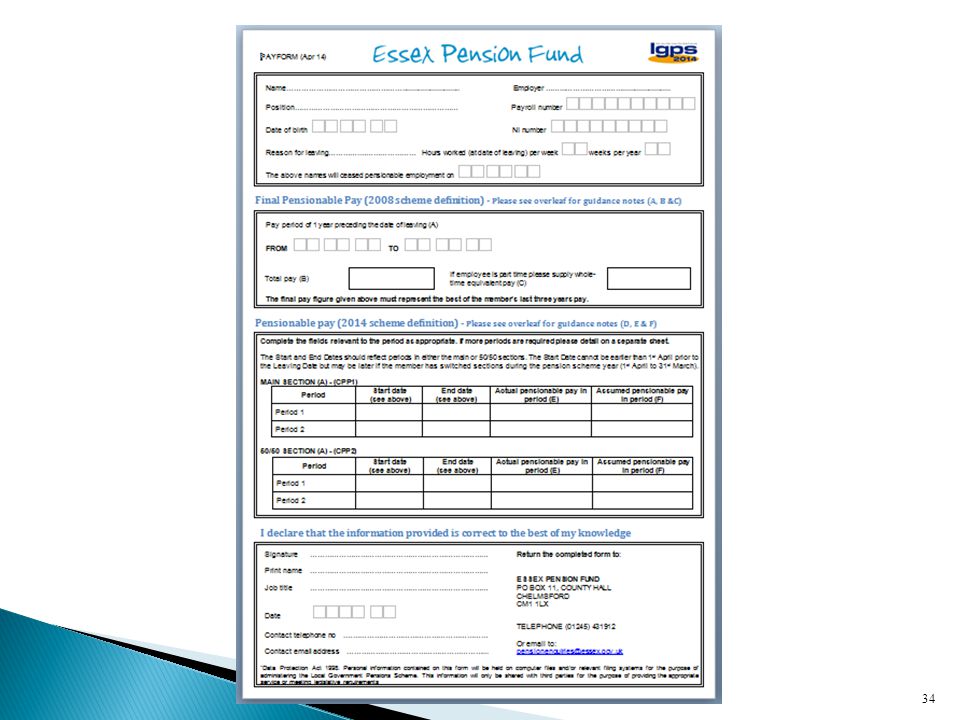

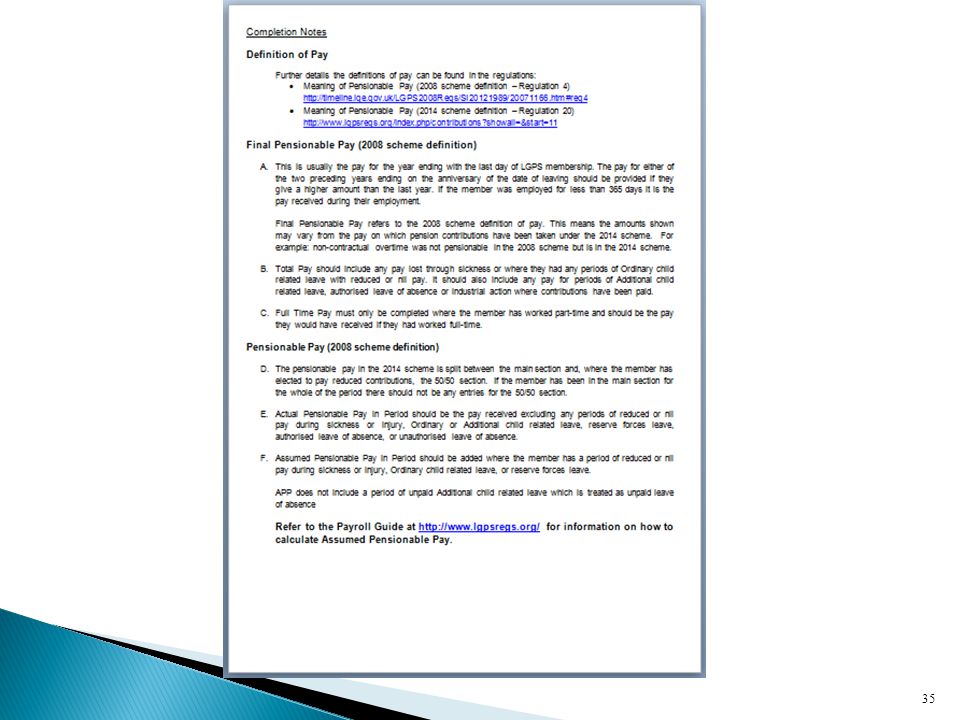

Pay Form The draft pay form contains up to 9 different values

Required for all employees

36

Discretions & Policies

Employers must formulate, publish and keep under review policy statements The Fund should receive these by 30 June Five main areas: Voluntary funding of additional pensions (SCAPC) Awarding additional pension via whole cost APC Switching on 85 year rule for those 55-60 Flexible retirement Waiving of actuarial reductions A list of discretions will be provided by the Fund

Awarding additional pension via whole cost APC. Switching on 85 year rule for those Flexible retirement. Waiving of actuarial reductions. A list of discretions will be provided by the Fund.")

37

More Information www.lgps2014.org www.lgpsregs.org

Please read the HR & Payroll Guides Contains essential information! telephone:

38

Thank you for listening

Essex Pension Fund

Similar presentations

LGPS 2014 ‘ New Career Average Scheme from 1 April 2014’ V1 – 11 February 2014.>")

Eligibility Requirements: AgeYears Optional5530 6020 62 5 Early Optional/Discontinued Service5020 Any Age25 DisabilityAny.>")

Employer Presentation Andy Cunningham Employer Relationship & Fund.>")