Download presentation

Presentation is loading. Please wait.

1

Institutional Environment and the Quality of Big 4 Auditors Bin Ke Nanyang Technological University Clive Lennox Nanyang Technological University Qingquan Xin Chongqing University

2

Motivational question Do Big 4 accounting firms provide the same audit quality around the world? –Do Big 4 deliver the same quality in China? Potential economic forces governing Big 4’s quality –Ability –Incentives (litigation risk, reputation, quasi-rent) Focus of this study is the incentives of Big 4

Focus of this study is the incentives of Big 4.")

3

Is the idea interesting? I think so because Big 4 auditors play a direct role in determining the quality of financial reporting There is a debate on whether Big 4 can deliver the same high quality audit in weak investor protection countries as in strong investor protection countries

4

Is the idea interesting? Relevance to China and HK: –H shares’ financial reports are allowed to be audited by domestic auditors after December 15, 2010

5

How to test the idea? What is the ideal experiment? The most obvious approach is to compare the audit quality of Big 4 across different countries Common limitations of cross country studies –Accounting standards –Auditing standards –Other cross-country differences

6

Prior research Compare Big4 vs. non-Big4 across countries –This approach does not directly examine the effect of institutional environment on Big 4 –Unclear whether the cross-country differences are effectively controlled for because the effects of country factors could be different for Big4 and non-Big4 –Any differences in results between Big4 vs. non- Big4 could be due to systematic differences of the clients audited by Big4 and non-Big4

7

Our approach Publicly traded firms listed on mainland China and audited by a domestic Big4 over 1995-2009 –Pure A shares –AH firms –AB firms

8

Our specific research question Do domestic Big4 accounting firms provide the same audit quality in China for –Pure A shares, –AB firms, and –AH firms?

9

Mainland China Big 4 of Pure A Firm Mainland China

10

Mainland China Big 4 of AH Firm HK Big 4 of AH firm Hong Kong Mainland China ?

11

Mainland China Big 4 of AB Firm HK Big 4 of AB firm Hong Kong Mainland China ? ?

12

Incentives of HK Big4: AH firms versus AB firms H report of AH firm B report of AB firm HK HKSE √ X HKSFC √ X/? HKICPA √√/? HK court √√/? Market √√/? Mainland CSRC √/?√ market X X

13

Mainland China Big4 Of AB Firms Mainland China Big4 Of AH Firms Mainland China Big4 Of Pure A Firms Hong Kong Mainland China ?

14

Advantages of our approach We directly examine the effect of institutional environment on Big 4’s behavior We can effectively isolate the country effects because we compare the audit quality of Big4 in the same country We do not compare Big4 vs. non-Big4 and thus our results cannot be due to systematic differences of the clients audited by Big4 and non-Big4

15

Pure A share firms (firm years) Domestic auditor Big 4=1Big4=0 Cell5 N=377Cell6 N=12,649

Domestic auditor Big 4=1Big4=0 Cell5 N=377Cell6 N=12,649")

16

AH share firms (firm years) Domestic and HK auditors are the same for 256 firm years Domestic auditor=375 Big 4=1 (cell13)Big4=0 (cell24) HK auditor is big4=1 (cell12)Cell1 N=258Cell2 N=68 HK auditor is big4=0 (cell34)Cell3 N=1Cell4 N=48

Domestic and HK auditors are the same for 256 firm years Domestic auditor=375 Big 4=1 (cell13)Big4=0 (cell24) HK auditor is big4=1 (cell12)Cell1 N=258Cell2 N=68 HK auditor is big4=0 (cell34)Cell3 N=1Cell4 N=48")

17

AB firms (firm years) Domestic (i.e., A share) auditor=1205 Auditor of B share reportBig 4=1 (cell135) 253Big4=0 (cell246) 937 B share auditor is big4=1 (cell12) Cell1 N= 201Cell2 N= 363 B share auditor is big4=0 (cell34) Cell3 N= 1 Cell4 N= 362 No B share auditorCell 5 N=51Cell 6 N=212

Domestic (i.e., A share) auditor=1205 Auditor of B share reportBig 4=1 (cell135) 253Big4=0 (cell246) 937 B share auditor is big4=1 (cell12) Cell1 N= 201Cell2 N= 363 B share auditor is big4=0 (cell34) Cell3 N= 1 Cell4 N= 362 No B share auditorCell 5 N=51Cell 6 N=212")

18

Research design Y = α 0 + α 1 HK_MONITOR + α 2 MULTIPLE_OFFICES + CONTROL VARIABLES + u –Dependent variable= Audit opinion Earnings management (accruals and loss) Audit fees (mainland)

Audit fees (mainland)")

19

Audit opinion model: key variables OPINION=1 if not clean opinion and zero if clean opinion in year t. HK_MONITOR= Dummy variable, 1 if the firm is an AH firm and its HK auditor is a big4 and zero otherwise ; MULTIPLE_OFFICES= Dummy variable, 1 if the firm is audited by more than one office, and zero otherwise.

20

Audit opinion model: control variables SIZE= Natural log of total assets in year t ; LEV= The ratio of the client’s total liabilities to total assets at the end of current fiscal year t ; CURRENT=The ratio of the client’s current assets to current liabilities. RETURN= Annual market adjusted abnormal return over the fiscal year t ; BETA= the firm’s beta estimated using a market model over the fiscal year VOL= the variance of the residual from the market model over the fiscal year; INVESTMENT= cash, cash equivalents, and short- and long-term investment securities deflated by total assets at fiscal year-end; ARINV= accounts receivable and inventory divided by total assets in year t ; ROE= net income over year-end total owners’ equity for year t ; LOSS=1 if the firm reports a loss for the current year, and 0 otherwise; SOE= Dummy variable, 1 if the audit firm is stated owned enterprise, and 0 otherwise.

21

Audit opinion model

22

Signed abnormal accrual model: dependent variable

23

Signed abnormal accrual model: control variables

24

Signed abnormal accrual model

25

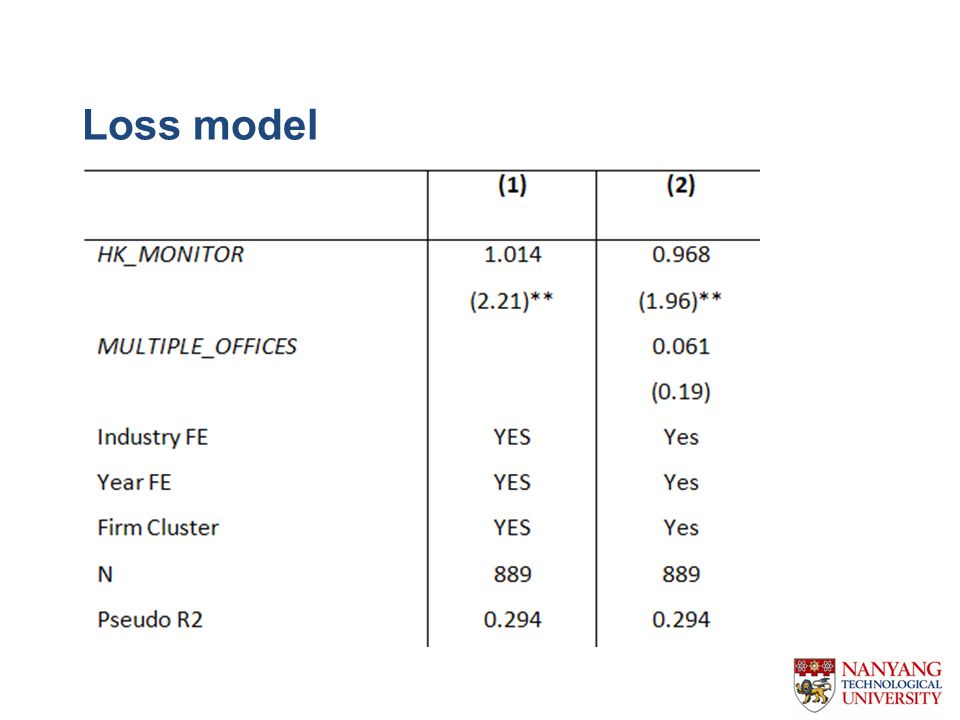

Loss model

27

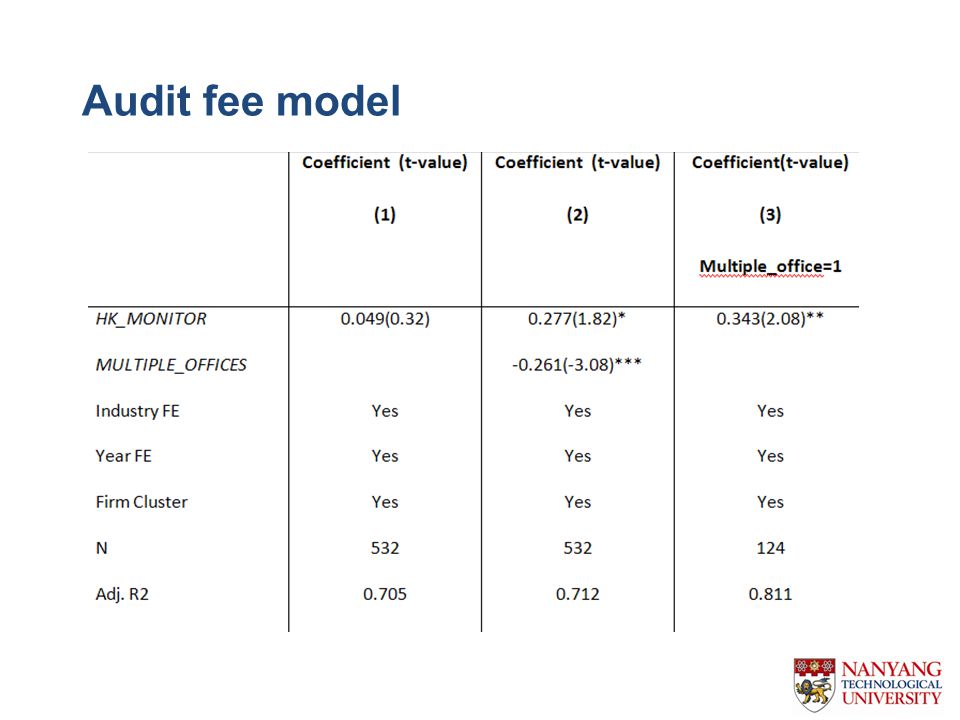

Audit fee model

29

Endogeneity of HK_MONITOR Cross-listing bonding hypothesis would suggest that AH firms are better and thus the self selection would bias against our predictions assess the severity of endogeneity: – SHORT is 1 if the distance between the fiscal year end and the HK IPO date for all AH firm years is less than 5 years (or 8) and zero otherwise

and zero otherwise")

30

Endogeneity of HK_MONITOR

31

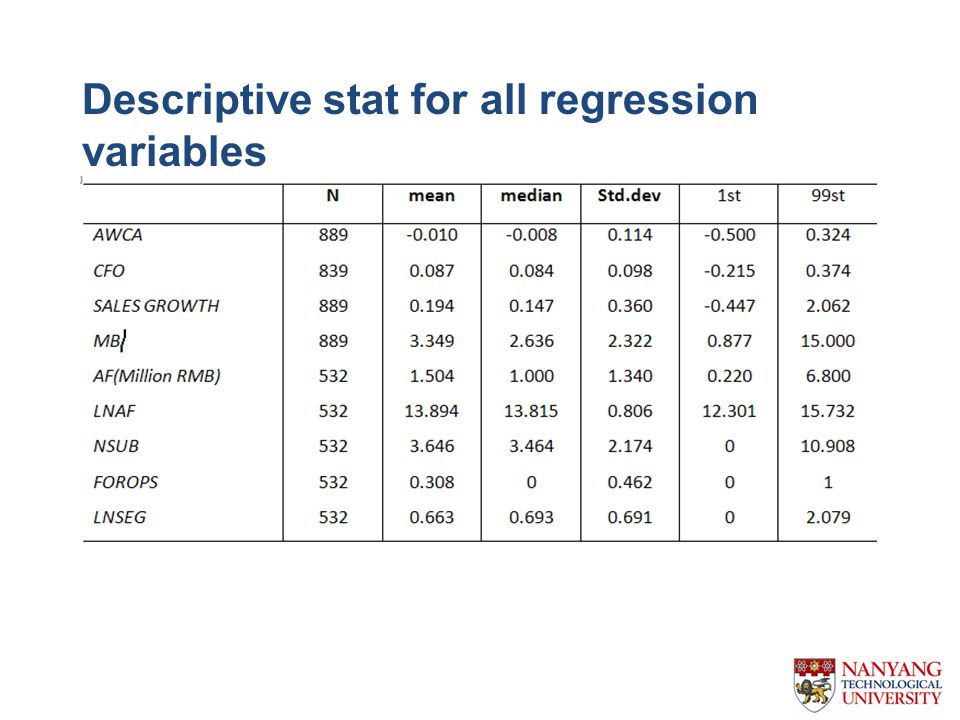

Descriptive stat for all regression variables

Similar presentations

Professor Scott Hoover Business Administration 365.>")

ROSENGARTEN CORPORATION Pro forma balance sheet after 25% sales increase ($)(Δ,$)($)(Δ,$) AssetsLiabilities and Owner's Equity Current assetsCurrent.>")