Download presentation

Presentation is loading. Please wait.

1

Treasury Yield Curves (Measure of Market Traders’ Y/Y and P/P Expectations) Web address: http://www.federalreserve.gov/releases/h15/ No revisions, instant data from bond markets Reflects the collective wisdom on the likely direction of the economy ( Y/Y) and inflation ( P/P). Expectations of future economic growth and inflation determine which Treasury debt securities are the most attractive to buy. The yield curve shape is a powerful forecasting tool. Federal Reserve sets short-term yields by targeting the fed funds interest rate. Bond traders determine longer-term yields. Normal Yield Curve Shape: Lower short-term yields with yields gradually rising with bond maturity. (longer maturities face greater unknown risks – war, politics, P/P - and hence require higher returns). The 3-month versus 30-year spread is about 2.5 percentage points with a normal yield curve. Steep Yield Curve Shape: Federal Reserve lowers short term rates to counter recession or inflation fears induce bond traders to sell long-term bonds. The 3-month versus 30-year spread is greater than 2.5 percentage points. Flat Yield Curve Shape: The economy is in danger of slipping into recession resulting in lower inflation. Bond traders buy long-term bonds to lock in higher long term yields => long-term yields fall relative to short-term yields. Probability of recession is 50% according to a Federal Reserve study. Inverted Yield Curve Shape: Short-term yields higher than long-term yields. Siren call that a recession is coming. The bond market believes the Federal Reserve is keeping monetary policy to tight and money supply growth to low. The last seven recessions have been preceded by an inverted yield curve 9 months – on average - in advance. If yield inversion is greater than 2.4 percentage points, then probability of recession is 90% in the next 18 months. ------------------------------------------------------------------------------------------------------------------------------------------------ Market Analysis: Bonds: Yield curve represents bond market Stocks: Stock prices are based on expectations of future profits and economic activity, so the yield curve can serve as an effective market-timing strategy tool Dollar: Inverted Y.C. may reduce foreign investor appetite for U.S. assets if believe recession is coming => $. However, an inverted Y.C. may attract “hot money” into U.S. investments if short-term U.S. interest rates are significantly above overseas short-term interest rates => $

. The 3-month versus 30-year spread is about 2.5 percentage points with a normal yield curve. Steep Yield Curve Shape: Federal Reserve lowers short term rates to counter recession or inflation fears induce bond traders to sell long-term bonds. The 3-month versus 30-year spread is greater than 2.5 percentage points. Flat Yield Curve Shape: The economy is in danger of slipping into recession resulting in lower inflation. Bond traders buy long-term bonds to lock in higher long term yields => long-term yields fall relative to short-term yields. Probability of recession is 50% according to a Federal Reserve study. Inverted Yield Curve Shape: Short-term yields higher than long-term yields. Siren call that a recession is coming. The bond market believes the Federal Reserve is keeping monetary policy to tight and money supply growth to low. The last seven recessions have been preceded by an inverted yield curve 9 months – on average - in advance. If yield inversion is greater than 2.4 percentage points, then probability of recession is 90% in the next 18 months Market Analysis: Bonds: Yield curve represents bond market Stocks: Stock prices are based on expectations of future profits and economic activity, so the yield curve can serve as an effective market-timing strategy tool Dollar: Inverted Y.C. may reduce foreign investor appetite for U.S. assets if believe recession is coming => $. However, an inverted Y.C. may attract hot money into U.S. investments if short-term U.S. interest rates are significantly above overseas short-term interest rates => $.")

4

Bank Balance Sheet Assets Liabilities + NW Reserves Deposits (Vault cash/Fed Dep.s) Checking Deposits Investments Savings MMDA Loans CDs Consumer IRAs Business Borrowings Student Building Net Worth Surplus Funds from Savers Channel Funds Lent Funds to Borrowers What is owned What is owed Assets = Liabilities + NW Real Interest Rate Loanable funds QS LF = Deposits QD LF = Loans Stock Vs Flow T –Account Shows in balance sheet + Deposits+ Loans S = I

Checking Deposits Investments Savings MMDA Loans CDs Consumer IRAs Business Borrowings Student Building Net Worth Surplus Funds from Savers Channel Funds Lent Funds to Borrowers What is owned What is owed Assets = Liabilities + NW Real Interest Rate Loanable funds QS LF = Deposits QD LF = Loans Stock Vs Flow T –Account Shows in balance sheet + Deposits+ Loans S = I")

5

Chapter 14 Bank Balance Sheet Reserves Deposits that a bank keeps as cash in its vault or on deposit with the Federal Reserve. Bank run Many depositors simultaneously decide to withdraw money from a bank. Bank panic Many banks experiencing runs at the same time. Required reserves Reserves that a bank is legally required to hold, based on its checking account deposits. Required reserve ratio The minimum fraction of deposits banks are required by law to keep as reserves. Excess reserves Reserves that banks hold over and above the legal requirement. Fractional reserve banking system A banking system in which banks keep less than 100 percent of deposits as reserves.

6

The Federal Reserve System How the Federal Reserve Manages the Money Supply Monetary policy The actions the Federal Reserve takes to manage the money supply and interest rates to pursue economic objectives. To manage the money supply, the Fed uses three monetary policy tools: Open market operations The buying and selling of Treasury securities by the Federal Reserve in order to control the money supply. Federal Open Market Committee (FOMC) The Federal Reserve committee responsible for open market operations and managing the money supply Discount policy Discount loans Loans the Federal Reserve makes to banks. Discount rate The interest rate the Federal Reserve charges on discount loans. Reserve requirements

The Federal Reserve committee responsible for open market operations and managing the money supply Discount policy Discount loans Loans the Federal Reserve makes to banks. Discount rate The interest rate the Federal Reserve charges on discount loans. Reserve requirements.")

7

Currency CHK Dep.s Savings MMDA CDs Other assets Assets HHs Liab. + NW Loans Net Worth Assets FED RES Liab. + NW Assets BANKs Liab. + NW CHK Dep.s Savings MMDA CDs Disc. Loans Net Worth Currency in Circulation Reserves Treasury Bonds Loans Reserves Treasury Bonds FX Reserves Reserves = Required Reserves + Excess Reserves Required Reserves = 10% x CHK Deposits Reserves = Vault cash + Deposits at Fed Res

8

Req. Reserves +10 Loans +90 Deposits +$100 HH Sector Cash = $100 Cash -$100 Dep. +100 Bank A Req. Reserves +9 Loans +81 Deposits +$90 Credit Union B Savings & Loan C Req. Reserves +8.10 Loans +72.90 Deposits +$81 Deposits +$72.90 Req. Reserves +7.29 Loans +65.61 Federal Reserve Currency in Circulation -$100 Required Reserves +100 Dep. +90 Loans +90 Dep. +81 Loans +81 Bank D Dep. +72.9 Loans +72.9 Sum = Dep. + 900 Loans + 900 The act of originating a loan, is the act of creating money Banks are the heart/pump of the economy Assume: 1.RR = 0.10 x Deposits 2.Banks Max. 3.ER = 0 Curr + Chk Deposits Clear checks between A,B,C,D

9

Sum of an Infinite Geometric Series Let OD = original deposit Loans = 0.9 OD + 0.9 2 OD + 0.9 3 OD +… Loans = 0.9 [OD + 0.9 OD + 0.9 2 OD +…] Loans = 0.9 [OD + Loans] (1- 0.9) Loans = 0.9 OD Loans = 0.9 OD (1 - 0.9) Loans = 9 (100) Loans = 900 = Deposits Loans

![Sum of an Infinite Geometric Series Let OD = original deposit Loans = 0.9 OD OD OD +… Loans = 0.9 [OD OD OD +…] Loans = 0.9 [OD + Loans] (1- 0.9) Loans = 0.9 OD Loans = 0.9 OD ( ) Loans = 9 (100) Loans = 900 = Deposits Loans](http://images.slideplayer.com/14/4394208/slides/slide_9.jpg "Sum of an Infinite Geometric Series Let OD = original deposit Loans = 0.9 OD OD OD +… Loans = 0.9 [OD OD OD +…] Loans = 0.9 [OD + Loans] (1- 0.9) Loans = 0.9 OD Loans = 0.9 OD ( ) Loans = 9 (100) Loans = 900 = Deposits Loans")

10

Excess Res. +100 T-Bills -100 Excess Res. -100 Loans +100 HH Sector Assets Liabilities Bank A Req. Reserves +10 Loans +90 Deposits +$100 Credit Union B Savings & Loan C Req. Reserves +9 Loans +81 Deposits +$90 Federal Reserve Reserves +100 Dep. +100 Loans +100 Dep. +90 Loans +90 Dep. +81 Loans +81 The act of originating a loan, is the act of creating money Open Market Purchase 1.Fed buys T-Bill from bank A Bank Excess Reserves 3.r = reserve requirement = 10% Curr + Chk Deposits T-Bill +100 Deposits = (1/r) x Reserves $1,000 = (1/0.10) x $100 Sum = Dep. + 1,000 Loans + 1,000 Asset Exchange Portfolio Rebalance

x Reserves $1,000 = (1/0.10) x $100 Sum = Dep. + 1,000 Loans + 1,000 Asset Exchange Portfolio Rebalance.")

11

Let x = loaned out/pass through % Let r = required reserve ratio = 1 - x Sum of Infinite Geometric Series S = 1 + x + x 2 + x 3 + … S = 1 + x [1 + x + x 2 + …] S = 1 + x [ S] S – x S = 1 S = 1/(1 - x) S = 1/r Simple deposit multiplier (ratio of chk deposits / reserves) If r = 10%, then multiplier = 10 checking deposits = 1/r * reserves $1,000 = 10 * $100 Recall Expenditure Multiplier Y = (1/1-MPC) x I

![Let x = loaned out/pass through % Let r = required reserve ratio = 1 - x Sum of Infinite Geometric Series S = 1 + x + x 2 + x 3 + … S = 1 + x [1 + x + x 2 + …] S = 1 + x [ S] S – x S = 1 S = 1/(1 - x) S = 1/r Simple deposit multiplier (ratio of chk deposits / reserves) If r = 10%, then multiplier = 10 checking deposits = 1/r * reserves $1,000 = 10 * $100 Recall Expenditure Multiplier Y = (1/1-MPC) x I](http://images.slideplayer.com/14/4394208/slides/slide_11.jpg "Let x = loaned out/pass through % Let r = required reserve ratio = 1 - x Sum of Infinite Geometric Series S = 1 + x + x 2 + x 3 + … S = 1 + x [1 + x + x 2 + …] S = 1 + x [ S] S – x S = 1 S = 1/(1 - x) S = 1/r Simple deposit multiplier (ratio of chk deposits / reserves) If r = 10%, then multiplier = 10 checking deposits = 1/r * reserves $1,000 = 10 * $100 Recall Expenditure Multiplier Y = (1/1-MPC) x I")

12

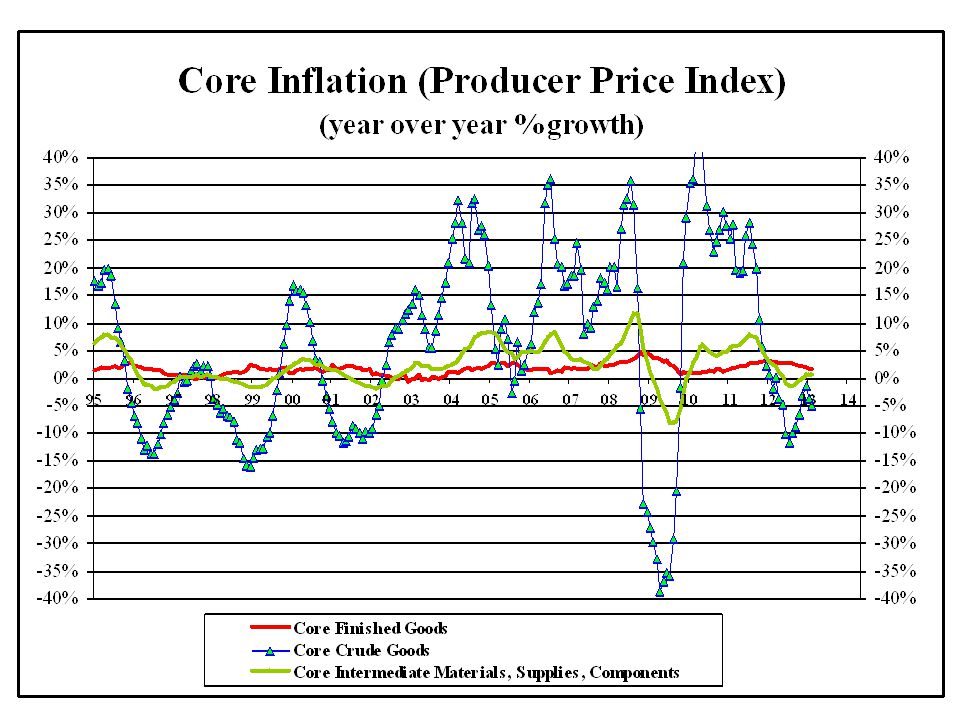

Producer Price Index (Measures changes in prices paid by businesses) Web: www.bls.gov/ppi One revision published with 4 month lag. Annual revision in February. PPI measures changes in prices that manufacturers and wholesales pay for goods during various stages of production. It is the oldest inflation measure; index began in 1902. Labor department issues questionnaires to 30,000 firms on 100,000 different items. A basket of goods is formed to create an index that starts at 100 and reflects average price of goods in 1982. PPI is the first inflation number of the month. Follow price changes along the production pipeline to determine where price pressures originate. 3 progressive stages of production give rise to 3 price indexes: PPI Crude Goods – cost of raw materials entering the market for the first time (wheat, cattle, soybeans, coal, crude petroleum, sand, timber). Price changes can be a function of changing supply which is a function of droughts, freezes, animal disease, geopolitical factors. Core Crude Goods – (nonfood materials less energy) is a good leading indicator of U.S. and world economic growth. This index responds quickly to shifts in economic activity. Prices are very sensitive to economic turning points. If businesses expect an increase in future demand, the demand for metals, paper boxes, timber will rise => price crude goods => price intermediate goods => price final goods. Price increases move down the production pipeline. PPI Intermediate Goods – cost of commodities that have undergone transitional processing (flour, paper, auto parts, leather, fabric) PPI Finished Goods – final processing stage (apparel, furniture, automobiles, meats, gasoline) Products retailers pay for. Total finished goods index is a measure of inflation in the long-run. Not a perfect leading indicator of consumer price inflation. There is a link between PPI finished goods and CPI. The two indexes may diverge on a month-to-month basis, but tend to move in tandem and are correlated over a longer (6-9 month) term. PPI does not include service prices or imported prices, whereas CPI does. Core PPI Finished Goods – excludes food and energy prices and gives a more accurate reading of the underlying inflation trend. The core rate index is a proxy for near-term inflation Inflation, P/P, is public enemy number one to the financial markets. An PPI => CPI A 12-month perspective is a better way to view the PPI numbers. ------------------------------------------------------------------------------------------------------------------------------------------------ Market Analysis: Bonds: PPI => ( P/P) E t+1 => D Bonds => i Bonds Stocks: PPI => production costs => profits => dividends => price stocks Dollar: PPI => ( P/P) E t+1 => i short-term => dollar

. Price changes can be a function of changing supply which is a function of droughts, freezes, animal disease, geopolitical factors. Core Crude Goods – (nonfood materials less energy) is a good leading indicator of U.S. and world economic growth. This index responds quickly to shifts in economic activity. Prices are very sensitive to economic turning points. If businesses expect an increase in future demand, the demand for metals, paper boxes, timber will rise => price crude goods => price intermediate goods => price final goods. Price increases move down the production pipeline. PPI Intermediate Goods – cost of commodities that have undergone transitional processing (flour, paper, auto parts, leather, fabric) PPI Finished Goods – final processing stage (apparel, furniture, automobiles, meats, gasoline) Products retailers pay for. Total finished goods index is a measure of inflation in the long-run. Not a perfect leading indicator of consumer price inflation. There is a link between PPI finished goods and CPI. The two indexes may diverge on a month-to-month basis, but tend to move in tandem and are correlated over a longer (6-9 month) term. PPI does not include service prices or imported prices, whereas CPI does. Core PPI Finished Goods – excludes food and energy prices and gives a more accurate reading of the underlying inflation trend. The core rate index is a proxy for near-term inflation Inflation, P/P, is public enemy number one to the financial markets. An PPI => CPI A 12-month perspective is a better way to view the PPI numbers Market Analysis: Bonds: PPI => ( P/P) E t+1 => D Bonds => i Bonds Stocks: PPI => production costs => profits => dividends => price stocks Dollar: PPI => ( P/P) E t+1 => i short-term => dollar.")

13

Finished Goods: Ready for sale to final demand user Bread Apparel Cars Furniture Gasoline Intermediate Goods: Semi-finished goods Flour Cotton yarn Steel Lumber Petroleum Crude Materials: Unmanufactured goods Grains Raw cotton Scrap steel Timber Crude petroleum 3 Stages of Production 3 Price Indexes Manufacturer 1Manufacturer 2Wholesaler

Similar presentations