Download presentation

Presentation is loading. Please wait.

1

I. Modigliani-Miller (MM) Capital Structure Propositions Assumptions include: Homogeneous expectations Perpetual cash flows: V = CF/r Perfect capital markets: No taxes, transaction costs, costs of distress Firms and investors borrow and lend at the same rate r B MM Proposition I:V L = V U MM Propositions II: r S = r 0 + B/S(r 0 - r B ), where r 0 is the cost of capital for an all equity firm.

Capital Structure Propositions Assumptions include: Homogeneous expectations Perpetual cash flows: V = CF/r Perfect capital markets: No taxes, transaction costs, costs of distress Firms and investors borrow and lend at the same rate r B MM Proposition I:V L = V U MM Propositions II: r S = r 0 + B/S(r 0 - r B ), where r 0 is the cost of capital for an all equity firm..")

2

M&M Proposition II: With no taxes, WACC = R 0 = (S/V) x R S + (B/V) x R B. Solving for R S, R S = R 0 + (R 0 - R B ) x (B/S) Cost of Capital (figure 15.3) R0R0 R S =R 0 +(R 0 -R B ) x B/S R WACC RBRB B/S

x (B/S) Cost of Capital (figure 15.3) R0R0 R S =R 0 +(R 0 -R B ) x B/S R WACC RBRB B/S.")

3

II. Modigliani Miller with Corporate Taxes (T c ) PV of the interest tax shield = (T C x R B x B)/R B = T C x B. V L = EBIT*(1-T C )/R 0 + T C R B B/R B = V U + T C B Proposition II becomes: R S = R 0 + (R 0 - R B ) x (B/S) x (1-T C ) Cost of Capital (figure 15.6) R0R0 R S =R 0 +(1-T C )(R 0 -R B ) x B/S R WACC RBRB B/S

PV of the interest tax shield = (T C x R B x B)/R B = T C x B. V L = EBIT*(1-T C )/R 0 + T C R B B/R B = V U + T C B Proposition II becomes: R S = R 0 + (R 0 - R B ) x (B/S) x (1-T C ) Cost of Capital (figure 15.6) R0R0 R S =R 0 +(1-T C )(R 0 -R B ) x B/S R WACC RBRB B/S.")

4

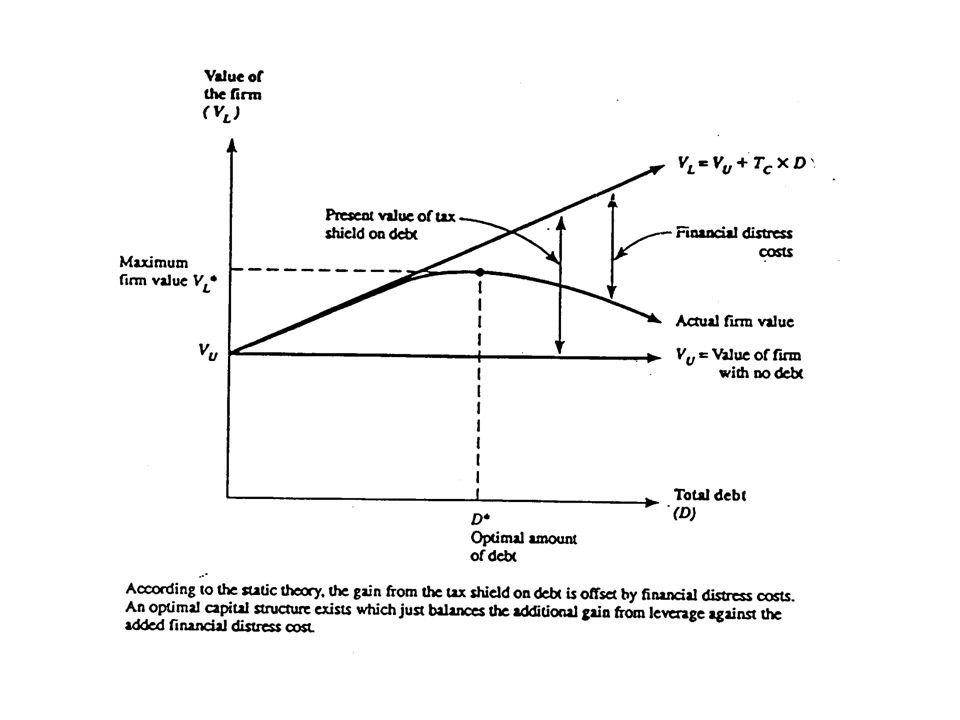

III. Limits to use of debt: bankruptcy & distress costs. An optimal capital structure will balance the valuable interest tax shield against the higher probability of facing bankruptcy costs. Expected costs of distress = probability of distress x distress costs Direct costs of financial distress Indirect costs of financial distress Agency costs of debt & equity

5

Agency costs of debt: Overinvestment in risky projects Tri-State Paving, Inc. –Owners-managers literally took all of the company’s cash to Las Vegas in an attempt to win enough money “to pay the corporate-debtor’s creditors and solve the financial problems of all three debtors...” Continental Airlines. –Frank Lorenzo’s Texas Air purchased a controlling interest in Continental Airlines cheaply when the latter was already in serious financial difficulty. Continental filed Chapter 11, locked the union out, and attempted to hire a new, non-union labor force while selling tickets to anywhere in the US for $49. Creditors opposed the scheme. Had it been unsuccessful, they would have born most of the cost Sambo’s Restaurants. –While In Chapter 11, Sambo’s Restaurants borrowed against its unencumbered assets and invested the money in changing the name, look, and concept of its restaurants. The gamble failed, the money was lost, and unsecured creditors ended up with only about 11 cents on the dollar Storage Technology –Storage Technology brought a new data-storage device to the market during its Chapter 11 case. The produce was so successful that the company was solvent with a substantial cushion of equity by the time it emerged.

8

IV. Empirical Implications of Capital Structure Theories Effects of changing capital structure Stock repurchases Debt/equity swaps Factors to consider in establishing a capital structure: Taxes Type of assets Uncertainty of operating income Pecking order and financial slack

Similar presentations