Download presentation

Presentation is loading. Please wait.

1

Management 183 Financial Markets Investments 2 (stocks)

")

2

Fundamental Stock Analysis I.Introduction to Securities Analysis II.Value Vs. Growth Investing III.Balance Sheet Valuation Methods IV.Analytical Factors: Growth Rates V.Intrinsic Valuation Methods

3

Common Stocks Residual Owners: o Stockholders of a firm are entitled to dividend income derived from the firm’s earnings. –Stocks may provide a steady stream of current income through dividends. –Stocks may increase in value over time through capital gains.

5

Market Performance Routine Decline: a drop of 5% or more in one of the major market indexes, like the Dow Jones Industrial Average (DJIA) Correction: a drop of 10% or more in one of the major market indexes Bear Market: a drop of 20% or more in one of the major market indexes

Correction: a drop of 10% or more in one of the major market indexes Bear Market: a drop of 20% or more in one of the major market indexes")

6

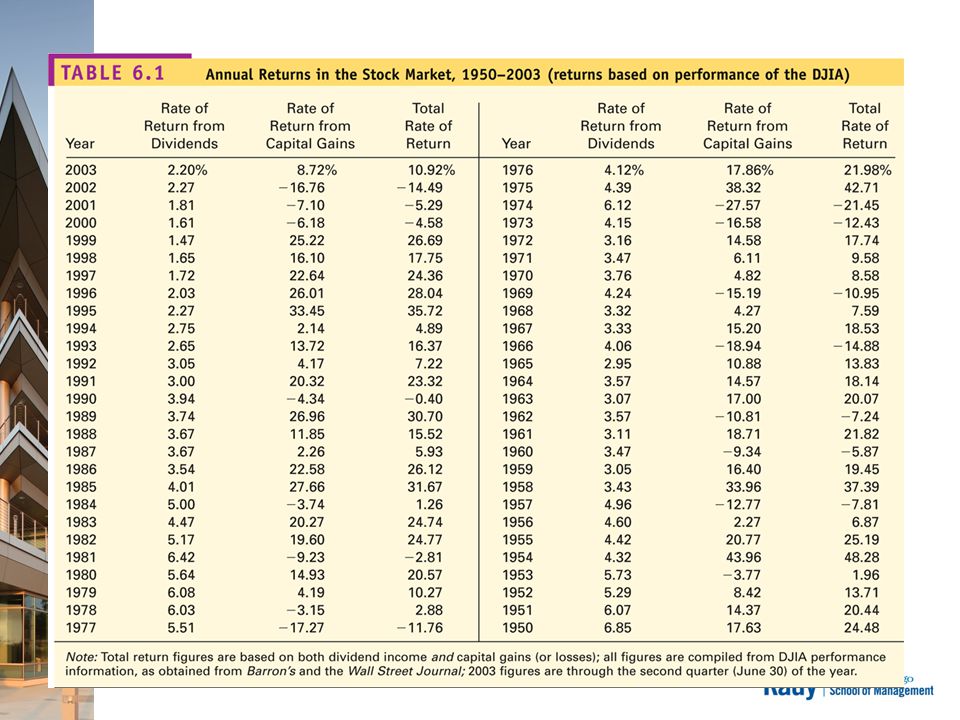

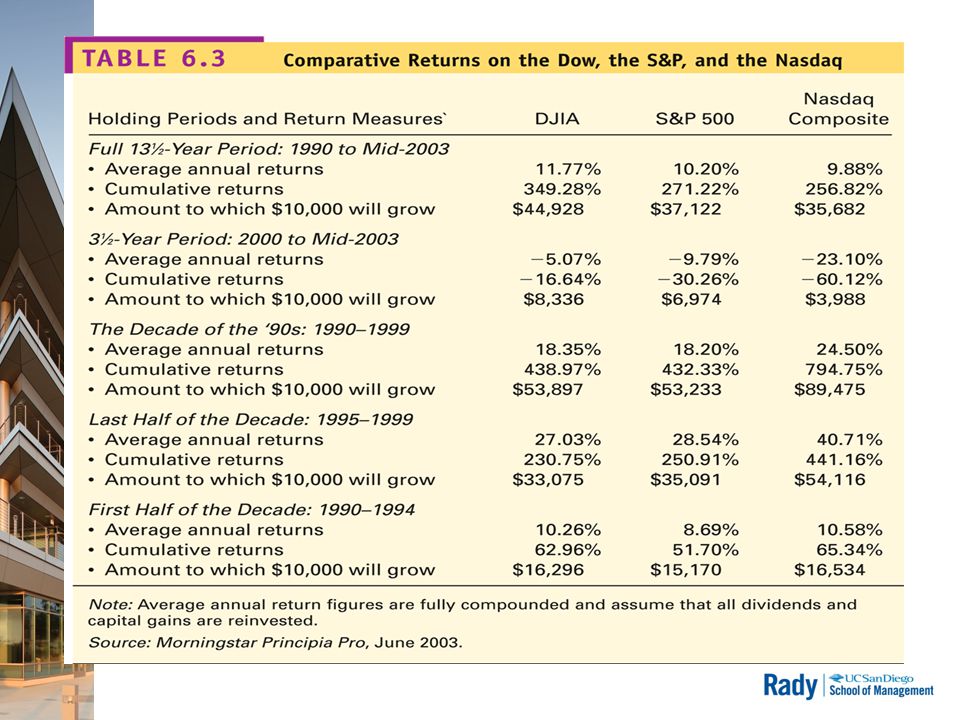

Stock Returns: Both price changes, called capital gains, and dividend income: –Over past 50 years, stock returns have ranged from +48.28% in 1954 to -21.45% in 1974 –Stock returns over past 50 years have averaged around 11% –From 1998 through mid-’03, DJIA averaged 1.7%

7

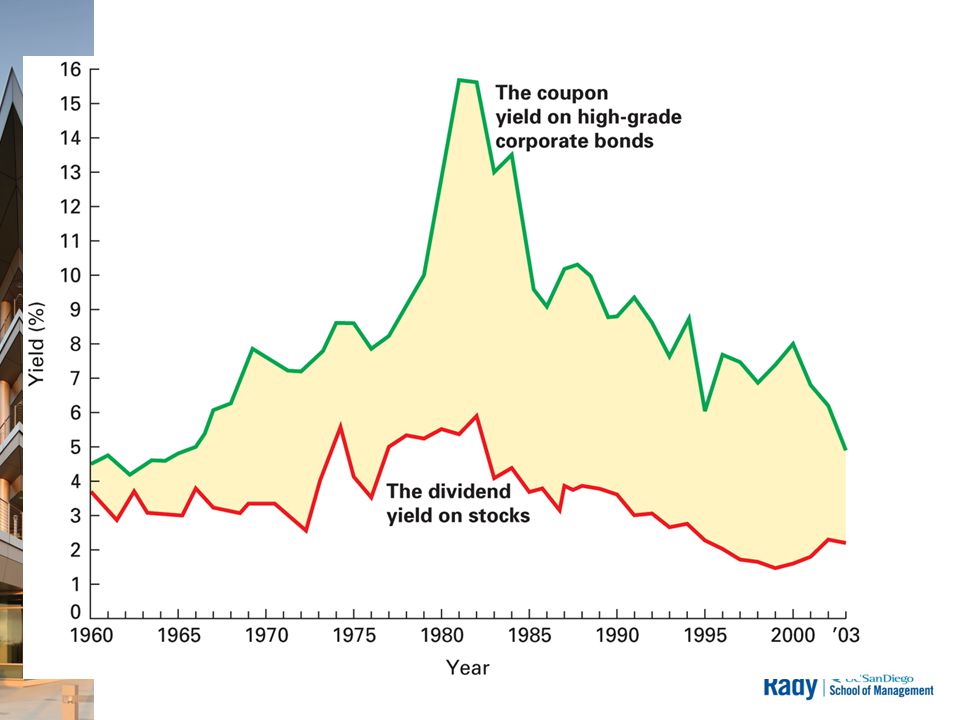

Provide opportunity for higher returns than other investments Over past 50 years, stocks averaged 11% and high-grade corporate bonds averaged 6% Good inflation hedge since returns typically exceed the rate of inflation Easy to buy and sell stocks Price and market information is easy to find in financial media Unit cost per share of stock is low enough to encourage ownership

10

Stocks are subject to many different kinds of risk: –Business risk –Financial risk –Market risk –Event risk Hard to predict which stocks will go up in value due to wide swings in profits and general stock market performance Low current income compared to other investment alternatives

12

Stock Split: when a company increases the number of shares outstanding by exchanging a specified number of new shares of stock for each outstanding share –Usually done to lower the stock price to make it more attractive to investors –Stockholders end up with more shares of stock that sells for a lower price –Investor with 200 shares in a 2-for-1 stock split would have 400 shares after the stock split –If the stock price was $100 before the split, the price would be near $50 after the split

13

Treasury Stock: shares of stock that were originally sold by the company and have been repurchased by the company. Share repurchases are often called “buybacks.” –Reduces the number of shares outstanding to public –Companies buyback when they believe stock is undervalued and a good buy –Companies may try to raise undervalued stock price or prop up overvalued stock price –May be used for employee stock option plans

14

Classified Common Stock: common stock issued in different classes, each of which offers different privileges and benefits to its holders –Different shares may have different voting rights –Often used to allow a relatively small group to control the voting of a publicly-trade company –Ford family owns “B” shares and other investors own “A” shares; Ford family controls 40% of Ford Motor Company –May have different dividend payout schedules

16

Par Value: the stated, or face, value of a stock –Mainly an accounting term and not very useful to investors Book Value: the amount of stockholders’ equity –The difference between the company’s assets minus the company’s liabilities and preferred stock Market Value: the current price of the stock in the stock market

17

Market Capitalization: the overall current value of the company in the stock market –Total number of shares outstanding multiplied by the market value per share Investment Value: the amount that investors believe the stock should be trading for, or what they think it’s worth –Probably the most important measure for a stockholder

18

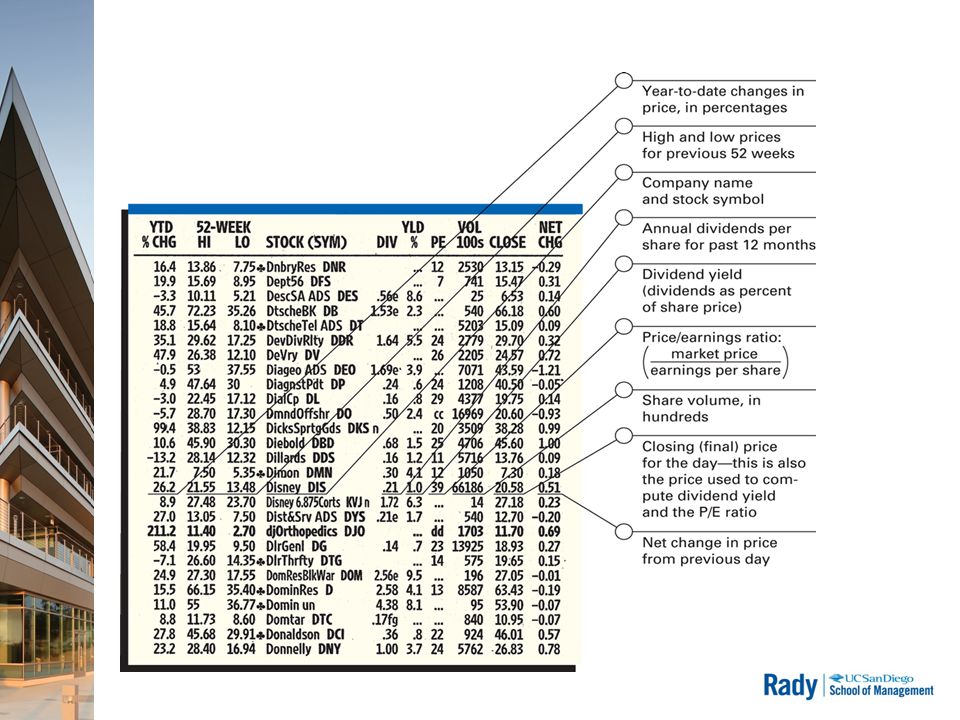

Earnings Per Share: the amount of annual earnings available to common stockholders, stated on a per-share basis

19

Dividends Dividend income is one of the two basic sources of return to investors. Dividend income is more predictable than capital gains, so preferred by investors seeking lower risk. Dividends are taxed at maximum 15% tax rate, same as capital gains. Dividends tend to increase over time as companies’ earnings grow; increases average 3-5% per year. Dividends represent the return of part of the profit of the company to the owners, the stockholders.

20

Dividend Payout Ratio: the portion of earnings per share (EPS) that a firm pays out as dividends –Companies are not required to pay dividends –Some companies have high EPS, but reinvest all money back into company

that a firm pays out as dividends –Companies are not required to pay dividends –Some companies have high EPS, but reinvest all money back into company")

21

Key Dates for Dividends

22

Dividends and Dividend Yield Dividend Yield: a measure to relate dividends to share price on a percentage basis –Indicates the rate of current income earned on the investment dollar –Convenient method to compare income return to other investment alternatives

23

Stock Dividend: payment of a dividend in the form of additional shares of stock Dividend Reinvestment Plans (DRIPs): plans where cash dividends are automatically reinvested into additional shares of the firm’s common stock –Over 1,000 companies offer DRIPs –Usually have no brokerage fees –Uses dollar-cost averaging

: plans where cash dividends are automatically reinvested into additional shares of the firm’s common stock –Over 1,000 companies offer DRIPs –Usually have no brokerage fees –Uses dollar-cost averaging")

24

Blue Chip Stocks: financially strong, high-quality stocks with long and stable records of earnings and dividends –Companies are leaders in their industries –Relatively lower risk due to financial stability of company –Popular with investing public looking for steady growth potential, perhaps dividend income –Provide shelter during unsettled markets –Examples: Wal-Mart, Proctor & Gamble, Microsoft, United Parcel Service, Pfizer and 3M Company

25

Income Stocks: stocks with long and sustained records of paying higher-than average dividends –Dividends tend to increase over time (unlike interest payments on bonds) –Examples: Verizon, Conagra Foods, Pitney Bowes.

–Examples: Verizon, Conagra Foods, Pitney Bowes.")

27

Growth Stocks: stocks that experience high rates of growth in operations and earnings Investors expect higher price appreciation due to increasing earnings; pay little or no dividends Examples: Lowe’s, Harley-Davidson, Starbucks, Kohls

29

Speculative Stocks: stocks that offer potential for substantial price appreciation, usually due to some special situation such as a new product. Examples: P.F. Chang’s, Quicksilver.

31

Tech Stocks: stocks representing the technology sector of the market –Small companies that have never shown a profit and blue chip stocks of large companies that are growth-oriented –Difficult to put value on due to erratic or no earnings –Examples: Microsoft, Cisco Systems, Dell.

33

Cyclical Stocks: stocks whose earnings and overall market performance are closely linked to the general state of the economy –Best for investors willing to move in and out of market as economy changes –Examples: Caterpillar, Maytag Corp.

35

Defensive Stocks: stocks that tend to hold their value, and even do well, when the economy starts to falter Stock price remains stable or increases when general economy is slowing Products are staples that people use in good times and bad times, such as electricity, beverages, foods and drugs; Gold stocks. Best for aggressive investors looking for “parking place” during slow economy Examples: Proctor & Gamble, WD-40

37

Market Capitalization Small-Cap Stocks: under $1 billion Mid-Cap Stocks: $1 billion to $4 or $5 billion Large-Cap Stocks: more than $4 or $5 billion

38

Small-Cap Stocks: small companies with market capitalizations less than $1 billion –Provide opportunity for above-average returns (or losses) –Usually do not have a financial track record –Earnings tend to grow in spurts and can have dramatic impact on stock price –Usually not widely-traded; liquidity is issue –Examples: Rubio’s, Hot Topic, Sonic Corp.

–Usually do not have a financial track record –Earnings tend to grow in spurts and can have dramatic impact on stock price –Usually not widely-traded; liquidity is issue –Examples: Rubio’s, Hot Topic, Sonic Corp.")

39

Mid-Cap Stocks: medium-sized companies with market capitalizations between $1 billion and $4 or $5 billion –Provide opportunity for greater capital appreciation than Large-Cap stocks, but less price volatility than Small-Cap stocks –Usually have long-term track records for profits and stock valuation –“Baby Blues” offer same characteristics of Blue Chip stocks except size –Examples: Wendy’s, Barnes & Noble, Petsmart, Cheesecake Factory

40

Large-Cap Stocks: large companies with market capitalizations over $4 or $5 billion –Number of companies is smaller, but account for 80% to 90% of the total market value of all U.S. equities –Bigger is not necessarily better –Tend to lag behind small-cap and mid-cap stocks, but typically have less volatility –Examples: AT&T, General Motors, Microsoft

41

Investing in Foreign Stocks Globalization of financial markets is growing –U.S. equity market is less than 50% of world equity markets –Six countries make up 80% of world equity market –U.S. market remains largest and one of best performing equity markets –Much of performance of non-U.S. markets is due to changes in currency exchange rates

42

Going Global International investing is more complex and riskier than domestic investing International investing requires investors to be right on more factors: –Must pick right stock –Must pick right market –Must pick correct direction for currency exchange rate fluctuations

43

Returns on International Investments Stronger U.S. dollar has negative impact on foreign investments Weaker U.S. dollar has positive impact on foreign investments

44

Stock Investment Strategies Buy-and-Hold –Investors buy high-quality stocks and hold them for extended time periods –Goal may be current income and/or capital gains –Investors often add to existing stocks over time –Very conservative approach; value-oriented

45

Strategies Current Income –Investors buy stocks that have high dividend yields –Safety of principal and stability of income are primary goals –May be preferable to bonds because dividends levels tend to increase over time –Often used to provide to supplement other income, such as in retirement

46

Strategies Quality Long-Term Growth –Investors buy high-quality growth stocks, mid- cap stocks and tech stocks –Capital gains are primary goal –Higher level of risk due to emphasis on capital gains –Significant trading of stocks may occur over time –Diversification is used to spread risk –“Total Return Approach” is version that emphasizes both capital gains and high income

47

Strategies Aggressive Stock Management –Investors buy high-quality growth stocks, blue chip stocks, mid-cap stocks, tech stocks and cyclical stocks –Capital gains are primary goal –High level of risk due to emphasis on capital gains –Investors aggressively trade in and out of stocks, often holding for short periods –Timing the market is key element –Time consuming to manage

48

Strategies Speculation and Short-Term Trading –Also called “day trading” –Buy speculative stocks, small-cap stocks and tech stocks –Capital gains are primary goal –High risk due to emphasis on capital gains in short time period –Trade in and out of stocks, often holding for extremely short periods –Looking for “big score” on unknown stock –Time consuming & high trading costs

49

Analysis Security Analysis: determining correct value of a security in the market place. How do analysts choose the stock and other securities to hold in their portfolio? –Macroeconomic Analysis –Sector Selection –Industry Analysis –Company Selection –Security Analysis –Technical Analysis

50

Fundamental Analysis:Fundamental Analysis: Research to find the appropriate time, place, company, and stock. Focuses on determinants of sales and earnings, risks and expectations for future company performance. Attempt to find mis-priced securities. Technical Analysis:Technical Analysis: Research to find recurrent and predictable stock price patterns, proxies for buy or sell pressure in the market.

51

The Changing Paradigm. –In long run, earnings are the most important factor in determining stock value. –In the short run, however, changes in market sentiment and consumer confidence are equally if not more important.

52

Security prices reflect information ? –Global news – economic and political –Domestic news –Industry news - trends –Firm news – marketing, products, management.

53

Economic Analysis –Structural economic changes. Demographic trends. Lifestyle changes Technological changes. Politics and Regulation.

54

Economic Analysis –Cyclical Changes - business cycle Financial companies tend to bottom just prior to the business cycle troughs and peak before the peak of a business cycle. At troughs, stock of consumer durable goods companies tend to bottom and peak at the peak. Capital goods companies tend to bottom shortly following a trough and peak when there is evidence the economy is weakening. As the economy enters into a recession investors tend to gravitate towards consumer staple companies.

55

Industry Analysis – Porter Five –threats of new entrants –Rivalry among existing competitors –Threat of substitutes –Buyer’s bargaining power –Supplier’s bargaining power –By considering each of these five elements of industry structure an analyst will develop a better estimate of how the industry is likely to fare in the future.

56

Industry Analysis – Life Cycle Analysis –Pioneering development –Rapid accelerating growth –Mature growth –Stabilization and market maturity –Deceleration of growth

57

Company Analysis –Choosing particular companies: Growth rates Price to Earning Ratio Price to Book Ratio Intrinsic Valuation Models

58

Value Vs. Growth Investing Two factions within Fundamental analysis –Value investors believes that securities should be purchased only when the underlying fundamentals (macroeconomic information, industry news, and a firm’s financial statements) justify the purchase. –Growth investors seek steadily growing companies. Growth traders are willing to pay more than might seem reasonable because they like the stock’s future prospects; they are buying future earnings that may or may not develop.

justify the purchase. –Growth investors seek steadily growing companies. Growth traders are willing to pay more than might seem reasonable because they like the stock’s future prospects; they are buying future earnings that may or may not develop..")

Similar presentations

that.>")

FIN 200: Personal Finance Topic 17–Stock Analysis and Valuation Lawrence Schrenk, Instructor.>")