Download presentation

Presentation is loading. Please wait.

1

APPLE SAUCE RETAIL BUYING AND MERCHANDISE FALL 2014 By Ashley Cates and Alyssa Mueller

2

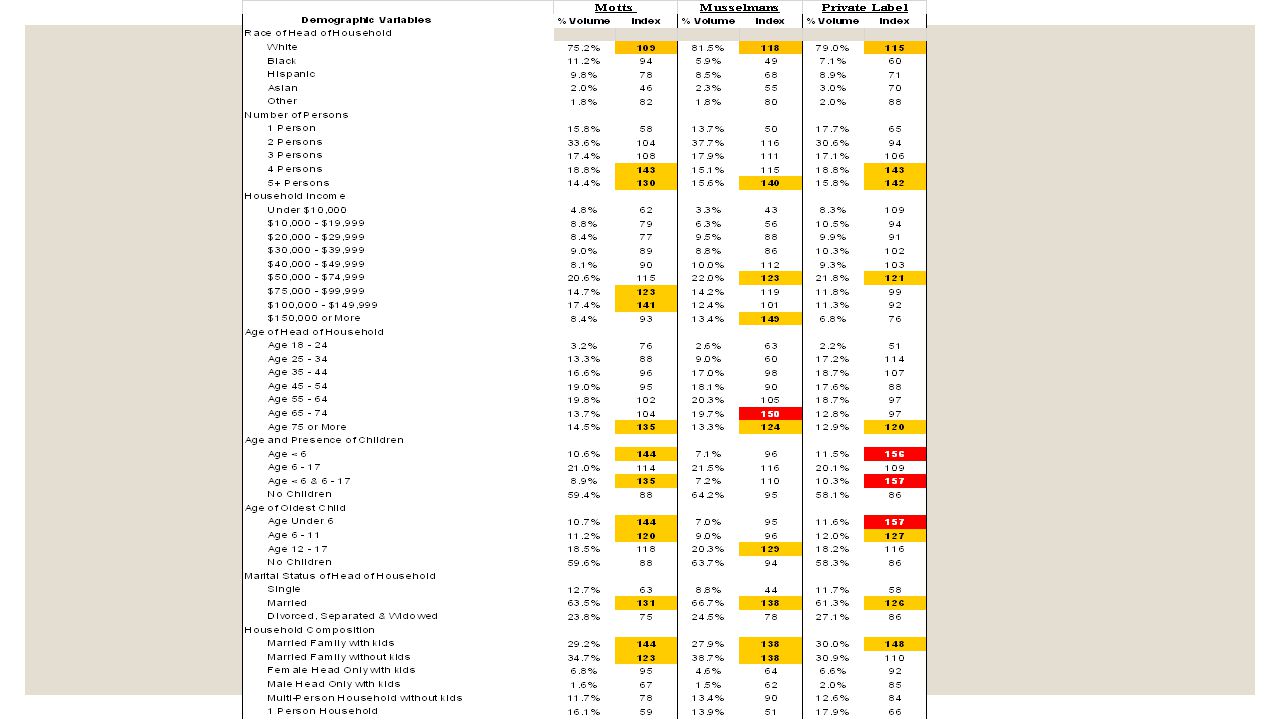

Product Snapshot Total Apple Sauce Category Demographics Apple Sauce is considered a normal category Increases as number of people increases Increases as income increases Primarily in leading brands such as Motts and Musselmans Most likely found in older households or households that have young children. Senior Couples Younger Bustling Families (HOH<40) Older Bustling Families (HOH>40) Presence and age of children is the dominate factor is apple sauce category

Older Bustling Families (HOH>40) Presence and age of children is the dominate factor is apple sauce category.")

3

Product Snapshot

6

Brand Snapshot Differences between Brands ◦ Across most national brands there are not large differences in consumers. ◦ Large household item ◦ Senior Buyers or Large households with children ◦ White is the primary race of all consumers ◦ Private label is bought and consumed more frequently in families with young children ◦ Leading brands are more popular with senior couples/married families without children How category management is affected ◦ Because there is not a much of a demographic difference in apple sauce consumers (between various brands) category management is not heavily affected. ◦ More time could be spent allocated to a different category of need ◦ There are little differences in assortment between retailers. Further proving category management is a minimal in this particular category. ◦ Most stores care 1 or 2 leading brands then a private label. ◦ Target- GoGo and Private Label ◦ Harp’s- Musselmans and Private Label

category management is not heavily affected. ◦ More time could be spent allocated to a different category of need ◦ There are little differences in assortment between retailers. Further proving category management is a minimal in this particular category. ◦ Most stores care 1 or 2 leading brands then a private label. ◦ Target- GoGo and Private Label ◦ Harp’s- Musselmans and Private Label.")

7

A.C. Nielson Data from 2007

8

Category Role Using Nielson Data from ‘07… ◦ The apple sauce as a category has moderate to low penetration (27.5% for U.S Total) ◦ Due to this penetration, visibility is moderately low ◦ Brand penetration is small ◦ Long Purchase Cycle (55.1 days) ◦ Private Label ◦ Highest household penetration of all brands (15.8) ◦ Highest rate of repeat purchase of all brands (45.5) ◦ Highest dollar share (41.0) ◦ Highest Loyalty for total U.S. ◦ Lowest item dollar per trip ◦ Motts is found on deal most frequently ◦ This may explain why senior couples consume this brand most ◦ We classified this as a “Under Fire” Category Sales slightly over 100 million (183,000,000) Mid-to-lower GM % of about 42%

Mid-to-lower GM % of about 42%.")

9

Category Assessment Continued… ◦ The smaller retailers, with limited display space, organized their category with only a leading brand plus private label ◦ Example: Harp’s was Musselmans and Private Label ◦ Every store retailer competed in Private Label for this category ◦ Private Label is incredibly important for this category ◦ Motts was at every store but Walgreens ◦ Walgreens is dedicated to their Private Label, Nice! With only 2 SKU of apple sauce ◦ Motts Natural 6 Pack Applesauce was found at every store (with the exception of Walgreens) ◦ Motts was the only brand found on deal ◦ Corresponds with the Nielson data ◦ At the Wal-Mart Pleasant Crossings store, there were 2 unique SKUs only to this store ◦ Del-Monte Mixed Berry 12 pack and Mott’s Natural No Sugar 6 pack ◦ GoGo would be considered a “Type C” Brand ◦ Yielded the highest dollar gross margins by about $0.40 average ◦ Although it’s the same price as most apple sauce packs, you get less per ounce.

◦ Motts was the only brand found on deal ◦ Corresponds with the Nielson data ◦ At the Wal-Mart Pleasant Crossings store, there were 2 unique SKUs only to this store ◦ Del-Monte Mixed Berry 12 pack and Mott’s Natural No Sugar 6 pack ◦ GoGo would be considered a Type C Brand ◦ Yielded the highest dollar gross margins by about $0.40 average ◦ Although it’s the same price as most apple sauce packs, you get less per ounce..")

10

Perceived Quality Gap How private label is competing There is a low perceived quality gap in Private Label items nationally ◦ Highest household penetration of all brands (15.8) ◦ Highest rate of repeat purchase of all brands (45.5) ◦ Highest dollar share (41.0) ◦ Highest Loyalty for total U.S. ◦ Lowest item dollar per trip ◦ Shortest purchase cycle Although Private Label does well nationally, this could be attributed to a larger amount of families buying apple sauce for their children rather than senior citizens Due to lower prices, Private Label does not generate good dollar gross margins ◦ Most brands generate slightly above a dollar profit for ever sale ◦ Private Label generates around $0.72 cents

11

Stores Audited, Depth & Unique SKUs StoresLocationSKUsUnique SKUsAudited By Wal-Mart SupercenterMLK Blvd-Fayetteville 540 (10 PL) Alyssa Wal-Mart SupercenterPleasant Crossing-Rogers 632 (10 PL) Ashley Wal-Mart Neighborhood Market Citizens Drive-Fayetteville 220 Alyssa Wal-Mart Neighborhood Market Bentonville 280 Ashley TargetShiloh Drive - Fayetteville 100 Alyssa Target Promenade Blvd - Rogers 140 Ashley Harp’sGarland Ave - Fayetteville 120 Alyssa Harp’sStore 127- 160 Ashley WalgreensSchool Ave-Fayetteville 22 (PL) Alyssa Walgreens 22 (PL) Ashley

Alyssa Wal-Mart SupercenterPleasant Crossing-Rogers 632 (10 PL) Ashley Wal-Mart Neighborhood Market Citizens Drive-Fayetteville 220 Alyssa Wal-Mart Neighborhood Market Bentonville 280 Ashley TargetShiloh Drive - Fayetteville 100 Alyssa Target Promenade Blvd - Rogers 140 Ashley Harp’sGarland Ave - Fayetteville 120 Alyssa Harp’sStore Ashley WalgreensSchool Ave-Fayetteville 22 (PL) Alyssa Walgreens 22 (PL) Ashley")

12

Share of Display Space/Facings At Wal-Mart Supercenters, GoGo has the largest share of space Harps carries mostly Musselmans, while Target also focuses on GoGo facings.

13

Shares of Gross Margin Dollar In terms of dollar gross margins, GoGo leads the category followed by Del Monte

14

Share of Gross Margin by Supplier Mott’s leads the category in percent gross margin.

17

Spectra Concentric Area Wal-Mart Supercenter Comparison MLK: ◦ Race of Head of Household was largely “Other” ◦ One person living in the houses or multiple people living in the house and are non-related. ◦ Low income (Under $10,000) ◦ Young Members of Household ◦ Single with No Children ◦ Largely Renters ◦ Example- Typical College Kid ◦ Expectations: Less Depth, Less Private Label Pleasant Crossings: ◦ Majority of Hispanic shoppers ◦ Large Households (4-5 people) ◦ Mid Income Levels or Very higher income levels ◦ Married Family with young kids (Children 11 or under) ◦ Not a high school graduate ◦ Example- Blue Collar Family or Young Family ◦ Expectations: Higher Depth, More Private Label and more Motts Harp’s Comparison Garland: ◦ Largely Asian or “other” ◦ One person household or multi-person adult home ◦ Low Income ◦ Young Households (18-24) ◦ Single with no children ◦ Rent homes rather than own ◦ Example- Typical College Kid ◦ Expectations: Less Depth, Less Private Label Bentonville: ◦ Race is largely white ◦ Larger Households (3-4 people) ◦ Very High income (100,000-150,000+) ◦ Primary age is 35-44. Most are older than 25 but younger than 55 ◦ Married Family with young kids or Female Head only with kids ◦ Two age gaps with kids: Children younger than 6 or teenagers 12-17 ◦ College Graduate ◦ Example- Idealize Suburban American Family or “The Cleaver Family” ◦ Expectations: Higher Depth, More Private Label and Musselmans

◦ Young Members of Household ◦ Single with No Children ◦ Largely Renters ◦ Example- Typical College Kid ◦ Expectations: Less Depth, Less Private Label Pleasant Crossings: ◦ Majority of Hispanic shoppers ◦ Large Households (4-5 people) ◦ Mid Income Levels or Very higher income levels ◦ Married Family with young kids (Children 11 or under) ◦ Not a high school graduate ◦ Example- Blue Collar Family or Young Family ◦ Expectations: Higher Depth, More Private Label and more Motts Harp’s Comparison Garland: ◦ Largely Asian or other ◦ One person household or multi-person adult home ◦ Low Income ◦ Young Households (18-24) ◦ Single with no children ◦ Rent homes rather than own ◦ Example- Typical College Kid ◦ Expectations: Less Depth, Less Private Label Bentonville: ◦ Race is largely white ◦ Larger Households (3-4 people) ◦ Very High income (100, ,000+) ◦ Primary age is Most are older than 25 but younger than 55 ◦ Married Family with young kids or Female Head only with kids ◦ Two age gaps with kids: Children younger than 6 or teenagers ◦ College Graduate ◦ Example- Idealize Suburban American Family or The Cleaver Family ◦ Expectations: Higher Depth, More Private Label and Musselmans.")

18

Category Tactics Visibility and Location in the Store: Category was given display space in a middle aisle of all dry grocery for every retailer. Most retailers had this category toward one end of the canned fruit aisle. Display: In Wal-Mart’s GoGo is getting the best, eye-level display while Musselman takes Harp’s, Target also uses GoGo as main display Unless a retailer is completely dedicated to Private Label, it is typically found on the bottom shelf of display space Brands are kept together within the respected size/package type. Representation of the Consumer Photos taken at Wal-Mart on MLK

19

Category Comparison Spring 2013

20

Category Comparison Changes from Spring 2013 Audit File Spring 2013 ◦ Fewer SKUs (60) ◦ Great Value 6 pack were $1.88 ◦ Musselmans was sold for $2.42 at Wal-Mart (6 pack) ◦ Harp’s mostly carried Musselmans and Wal-Mart displayed the most Motts ◦ Private label seems to be maintained at the same level. No increase, no decrease. ◦ Focused on 2 leading brands and private label specific to every retailer ◦ Unit 2 Cost were set higher than ours in leading brands such as.. ◦ Motts (.07) ◦ Musselmans (.07) ◦ The higher unit two cost cause lower percent gross margins ◦ Around 25% Fall 2014 ◦ More SKUs (66) ◦ Great Value 6 packs are now sold for $1.68 ◦ Motts are sold at the same price for a six-pack at Wal-Mart ◦ Musselman has raised their price at Wal-Mart $2.77 ◦ For Wal-Mart Supercenters, GoGo had the most display space while Harp’s carried mostly Musselmans. ◦ Had higher gross margins due to lower unit 2 costs ◦ Around 42%

◦ Musselmans (.07) ◦ The higher unit two cost cause lower percent gross margins ◦ Around 25% Fall 2014 ◦ More SKUs (66) ◦ Great Value 6 packs are now sold for $1.68 ◦ Motts are sold at the same price for a six-pack at Wal-Mart ◦ Musselman has raised their price at Wal-Mart $2.77 ◦ For Wal-Mart Supercenters, GoGo had the most display space while Harp’s carried mostly Musselmans. ◦ Had higher gross margins due to lower unit 2 costs ◦ Around 42%.")

21

Our own findings.. ◦ Private Label Product Taste Test: ◦ More bland compared to national brand ◦ Not as thick as national brand ◦ Comparison testing: ◦ Color variation ◦ Texture variation ◦ Our preferences: ◦ Prefer national brand, specifically Mott’s, to private label brand ◦ Mott’s had an overall better flavor and quality than Great Value ◦ As an adult, we would say there is a definite foils aka a bad private labels to steer us to buying the higher margin, national brands. ◦ From the past category audit, we observed innovations in packaging: ◦ Del Monte and GoGo are trending toward a “squeezable pouch” rather than a standard cup. ◦ This may help with inventory ◦ Provides convenience for mothers who pack their children lunches or use apple sauce as a snack

Similar presentations