Download presentation

Presentation is loading. Please wait.

1

Bond Market Financing by Sub-national Governments:Indian Experience

Dr HK Pradhan Professor of Finance and Economics XLRI Jamshedpur, India September 30-October 1, 2004

3

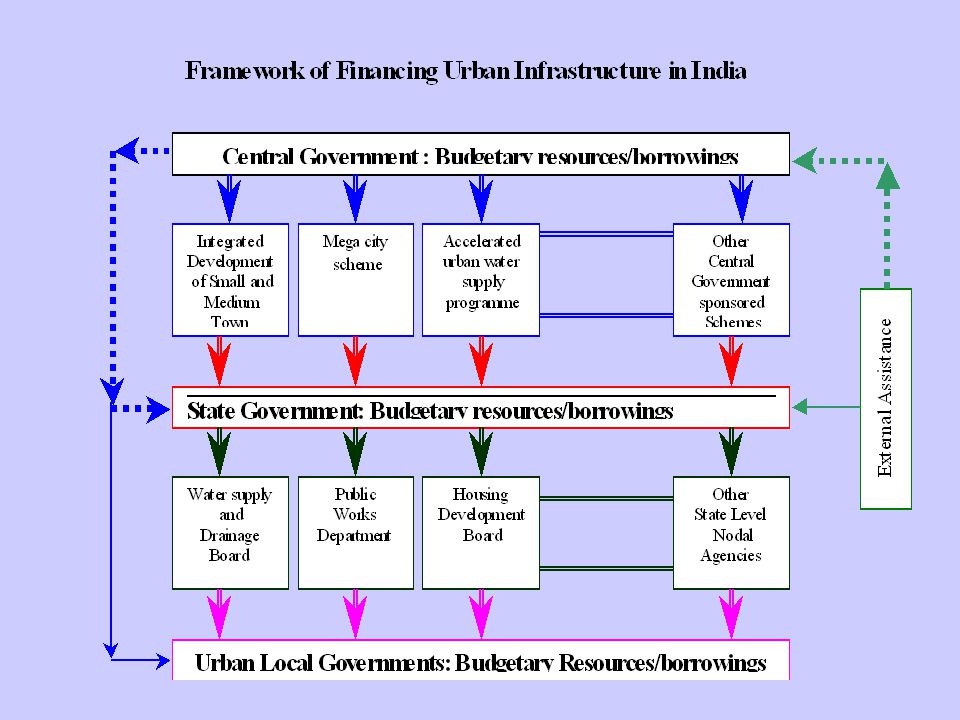

India: A Three-tier Federation

First Tier: Central Government at the National Level Second-Tier : State Governments in 28 States & 7 Union Territories Third-Tier: Numerous Rural and Urban Local Bodies Rural Local Bodies 2,47,033 Panchayats 2,38,662 Autonomous Councils 83,410 Urban Local Bodies 3,682 Municipal Corporations 96 Municipalities ,494 Nagar Panchayats 2,092

5

Wide diversity in terms of revenue raising capabilities and economic performance

Octroi Property tax Other taxes Water / sewerage Building license Vehicle/ animals Fines Investment income Stamp Duty Electricity tax Motor vehicle tax State government Other agencies Growth / sustainability / predictability of key revenue heads: Octroi: Depends on consumption levels within muni. limits, and on use of industrial inouts by manufacturing units located within muni. limits. Sustainability of octroi depends on continued industrial and economic growth within city, and collection efficiency. Problems in octroi come from transport lobby, protest from consumers against adding to costs, protests from producers against eroding their local competitiveness Property tax: % levied on ARVs of residential, industrial and commercial property. Key issues are: 1) Basis of levy (flat rate, area based, mkt value based) 2) how frequently are rates fixed 3) how easy is it to raise rates 4) collection efficiency Litigation prone Water / sewerage charges: usually do not cover service costs. The extent of deficit is a function of: Area covered, # of connections, % of bulk consumption, income profile of users Shared / assigned taxes: passed on by concerned SG. General trend is against passing on these benefits to munis as SGs themselves are in weak position

Basis of levy (flat rate, area based, mkt value based) 2) how frequently are rates fixed. 3) how easy is it to raise rates. 4) collection efficiency. Litigation prone. Water / sewerage charges: usually do not cover service costs. The extent of deficit is a function of: Area covered, # of connections, % of bulk consumption, income profile of users. Shared / assigned taxes: passed on by concerned SG. General trend is against passing on these benefits to munis as SGs themselves are in weak position.")

8

Financial market is yet make a strong impact on financing subnational governments and urban infrastructures

9

Potential benefits of bond market access by the local governments:

Leverage the internal resources with long term bonds for financing infrastructure; Make lumpy investments through bond issuance rather than limited pay-as-you-go financing Results in credit discipline by the city governments, by promoting fair discloser and accounting, and better management practices Make feasible one of the vital objective of the 74th Constitution Amendment by balancing the revenue raising capabilities with expenditure responsibilities.

12

Subnational Bond Issuance in India

Bonds issued by state sponsored institutions Bonds issued by ULBs Urban Development Funds

13

Issuance by State Sponsored Institutions

State level Statuary Boards( such as water supply and swerage boards), state owned corporations( such as power, irrigation), state initiated SPVs,, with limited recourse to Government Are the second largest issuers in Indian bond markets component of the local bond segments Issued as private placements, most of which are government guaranteed Taxable or tax-free, often in the form of structured issues or carrying credit enhancement features such as revenue dedication: usually known in India as “structured obligations(SO)” Have created significant fiscal risks for the state governments, as discussed

, state owned corporations( such as power, irrigation), state initiated SPVs,, with limited recourse to Government. Are the second largest issuers in Indian bond markets component of the local bond segments. Issued as private placements, most of which are government guaranteed. Taxable or tax-free, often in the form of structured issues or carrying credit enhancement features such as revenue dedication: usually known in India as structured obligations(SO) Have created significant fiscal risks for the state governments, as discussed.")

14

Noida Toll Bridge Company Limited

SPV promoted by IL&FS for the Noida-Delhi toll bridge project, which include constructing a bridge across the river Yamuna on a BOOT scheme(operations started in February 2001): Equity : Rs 1016 million FCDs : Rs 208 million IL&FS (World Bank) : Rs 600 million Term loans : Rs 1075 million Deep discount bonds : Rs 500 million Credit rating - AAA (SO) by CARE Put option: Investors have the put option to sell the bonds to IL&FS and/or IDFC at a predetermined price at the end of 5th year and 9th year from the date of allotment. Credit enhancement mechanism: By IDFC & ILFS

: Equity : Rs 1016 million. FCDs : Rs 208 million. IL&FS (World Bank) : Rs 600 million. Term loans : Rs 1075 million. Deep discount bonds : Rs 500 million. Credit rating - AAA (SO) by CARE. Put option: Investors have the put option to sell the bonds to IL&FS and/or IDFC at a predetermined price at the end of 5th year and 9th year from the date of allotment. Credit enhancement mechanism: By IDFC & ILFS.")

15

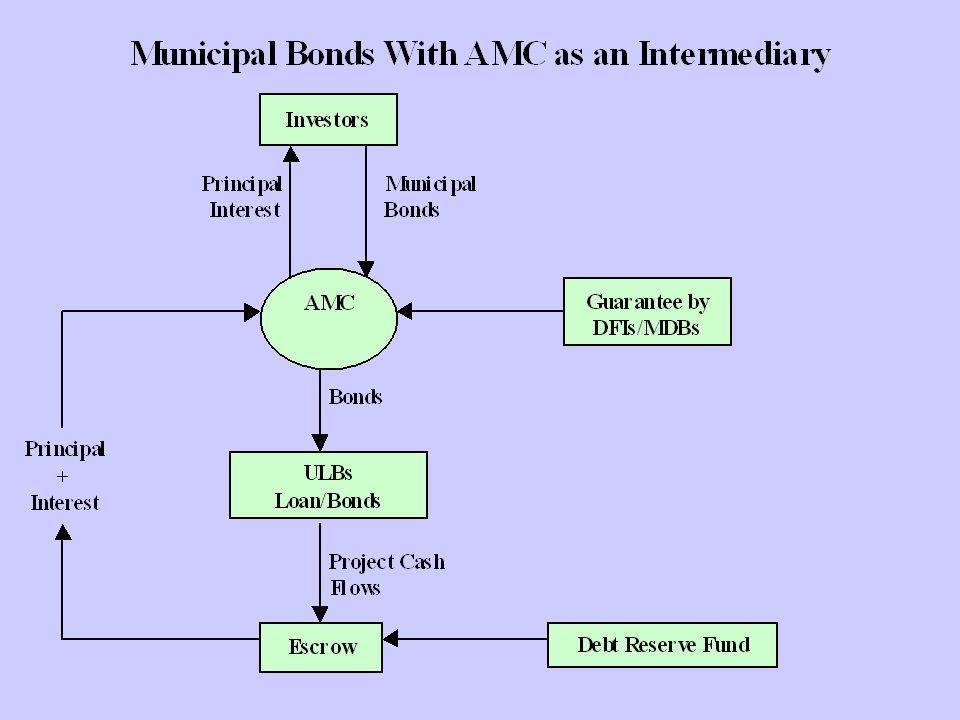

Municipal Bonds Municipal issues are in the nature of revenue bonds, with fixed interest rate, with or without government guarantee, maturity 7-15 years, are in the form of Structured Obligations(SO), taxable or tax free

, taxable or tax free.")

18

TamilNadu Urban Development Fund

A Trust established in 1996 under the Indian Trusts Act, 1882, by GoTN, ICICI, HDFC and IL&FS with a line of credit from the World Bank, to fund urban infrastructure needs. The share holding pattern of TNUDF is GoTN (49%), ICICI (21%), and HDFC and IL&FS (15% each) Management responsibility is taken up by ICICI, the lead institution in the arrangement. ULBs, statutory boards, and joint sector projects are the eligible borrowers, with maturity varying from years Special recovery mechanisms such as escrow accounts of property tax, water charges and hypothecation of movables are generally used.

, ICICI (21%), and HDFC and IL&FS (15% each) Management responsibility is taken up by ICICI, the lead institution in the arrangement. ULBs, statutory boards, and joint sector projects are the eligible borrowers, with maturity varying from years. Special recovery mechanisms such as escrow accounts of property tax, water charges and hypothecation of movables are generally used.")

19

Pooled Financing in Tamil Nadu

A State level pooled financing mechanism launched in Tamil Nadu, with the financial assistance of the USAID For smaller and medium sized municipalities Under the arrangement, 14 smaller ULBs, who are unable to access capital markets due to weak financial position and lack of capacity, pooled some water and sanitation projects under a special purpose vehicle (SPVs) called the Water and Sanitation Pooled Fund(WSPF), and raised about Rs 300 million from the bond market at an interest of 9.2 per cent for 15 years maturity

called the Water and Sanitation Pooled Fund(WSPF), and raised about Rs 300 million from the bond market at an interest of 9.2 per cent for 15 years maturity.")

20

Tamil Nadu Experience is unique, needs to be replicated, in the urban and semi-urban areas of developing countries. The financing of local infrastructure met by market based funding techniques with beneficiary participation (loans and grants are blended for the poorer municipalities). Bringing to one platform a number of stakeholders: governments at the levels of central, state and municipality, multilateral donor, domestic financial institutions, and private investors; The Fund has built significant capacity by improving the financial, managerial, administrative, and technical performance of the municipalities, and has the potential of ultimately turning them into creditworthy and well functioning entities. Direct and positive environmental benefits in the urban areas through solid waste and sanitation facilities, storm drainage and water supply facilities. Established significant participatory governance, whereby City Development Strategies are undertaken through a consultative process involving elected officials, municipal officers, community and professional groups, business and industry representatives and government agencies.

. Bringing to one platform a number of stakeholders: governments at the levels of central, state and municipality, multilateral donor, domestic financial institutions, and private investors; The Fund has built significant capacity by improving the financial, managerial, administrative, and technical performance of the municipalities, and has the potential of ultimately turning them into creditworthy and well functioning entities. Direct and positive environmental benefits in the urban areas through solid waste and sanitation facilities, storm drainage and water supply facilities. Established significant participatory governance, whereby City Development Strategies are undertaken through a consultative process involving elected officials, municipal officers, community and professional groups, business and industry representatives and government agencies.")

21

The TNUDF has the potential to revolutionize the concept of development financing and empowering local communities, and could serve well as an effective tool towards the fulfillment of Millennium Development Goals.

22

Deepening of Subnational Capital Markets and Bonds Markets

Depends much on the growth and diversity of the national bond markets, and its constituents, its institutional structure and regulatory framework Securities regulations are not designed in segments; should be viewed as part of an overall system, existing alongside and complemented by established national systems of regulations Create the enabling environment, thereby enhancing the attractiveness of the Subnational securities, by reducing transaction costs and risks for investors

23

Environment promoting Subnational bond issuance should include..

Broadening of the issuers and investor’s base Credit ratings of the Subnational bodies Securities regulations covering issuing, listing, trading, and settlements Defined borrowing powers Bankruptcy regulations with defined and enforceable debt contracts Fiscal incentives such as taxation and credit enhancement such as guarantees

24

Issuers Broadening of the issuers base, through capacity building efforts Financial restructuring of the SPVs and salutatary boards, making them creditworthy Bringing medium and smaller urban areas into municipal bond markets Promotion of pooled financing structure

25

Investors Most of the central and state government securities are held by the institutional investors Subnational securities are generally seen as high yield, but more risky Attracting more and more retail investors, and by designing customized bond structures, in order that the risk perceptions improved, wider publicity, improving transparency of local bodies Innovative mechanisms such as embedded options, pooled financing/bond banks, specialized funds, securitization, “take-out financing” etc will strengthen this markets Building capital market relationship, making investors aware of the issuer profile, familiarity with market intermediaries and regulatory environment

26

Secondary Markets Presently the secondary market trading comprises mostly the central and state government securities. Investors in municipal bonds effectively held to maturity Municipal issuers will benefit from listing and trading in secondary market, as this will greatly enhance trading and visibility. NSE would be the preferred exchange, has terminals in most of the Indian cities, allowing nationwide access for investors. Listing and trading requires continuing disclosure requirements for the local bond issuers.

27

Regulatory Structures

Issuance of debt instruments by local bodies are governed by multiple legislations Too many regulators, with less effective regulations

28

Regulatory Design for Local Debt Markets

The Public Debt Act 1944 The Securities and Exchange Board of India(SEBI) Act of 1992 The Local Authorities Loan Act 1914 The Companies Act 1956 The Securities Contracts (Regulation) Act 1956 The Depositories Act 1996 Subnational bodies taking the tax exempt status come under the MUD&PA and the MOF State governments themselves regulate borrowings

Act of The Local Authorities Loan Act The Companies Act The Securities Contracts (Regulation) Act The Depositories Act Subnational bodies taking the tax exempt status come under the MUD&PA and the MOF. State governments themselves regulate borrowings.")

29

Case for Integration of Different Regulatory Agencies for subnational issuance

Case to have a single law or single window clearance for bond issuance by local bodies. State Finance Commissions (SFCs) is expected to deal with assignment of powers relating to taxes, transfers, but extremely limited role in so far as borrowing powers are concerned.

is expected to deal with assignment of powers relating to taxes, transfers, but extremely limited role in so far as borrowing powers are concerned.")

30

Borrowing Powers Local Authorities Loans Act of 1914 is very old and have outdated provisions Estimates of borrowing powers are made based on the annual rental value, which have not been revised for long Few States have passed laws on guarantees, but none has passed a law on capping borrowings Necessary for a clear policy on borrowing powers It will also bring in market discipline and fiscal stability

31

Credit Ratings Mandatory rating which along with a statutory limitation on borrowing powers of Subnational bodies would bring in considerable market discipline Credit rating is definitely not just a regulatory issue as much as a measure of market discipline Government guarantee is not a substitute for important disclosure through credit ratings Socio-political changes at the local level need to be captured by rating agencies Rating agency should monitor the ULBs as part of its surveillance during the tenor of the bonds State governments could take important initiatives in making available the credit ratings of their local bodies, something like pre-screening of the potential issuers or in the form of comparative urban indicators

32

Municipal Bankruptcy The existing framework of insolvency in India mainly relates to corporate insolvency Not relevant insofar as enforcing secured assets of or bringing about insolvency proceedings against the ULBs Need for laws relating to Municipal Bankruptcy: Promulgation of a law to lay down a separate insolvency process (in the nature of a fast-track recovery process) for local bodies. Constitution of separate insolvency courts to try matters pertaining to borrowings by and insolvency of, local bodies. Promulgation of a separate statute setting out the revised manner of constitution of local bodies, in order to facilitate greater transparency and responsibility in fiscal dealings

for local bodies. Constitution of separate insolvency courts to try matters pertaining to borrowings by and insolvency of, local bodies. Promulgation of a separate statute setting out the revised manner of constitution of local bodies, in order to facilitate greater transparency and responsibility in fiscal dealings.")

33

Fiscal Incentives Tax exemptions allowed under various sections of the Indian Income Tax Act from the following: Interest received from bonds Capital gains from bonds Tax rules and rates are prone to changes every year Tax environment should be stable and predictable

34

Capacity building in capital planning process ULBs

Municipal Bond Issuance Process Project Feasibility study Capital planning process Prepare for Disclosure Decision to Issue Credit Rating Formation of Bond Parties (underwriter, trustee, State government guarantee) Information Memorandum Audit and Standing Committee Approval GOI and SEBI approval Issuance of bonds Listing Use of Funds and Follow Up

Information Memorandum. Audit and Standing Committee Approval. GOI and SEBI approval. Issuance of bonds. Listing. Use of Funds and Follow Up.")

35

Enabling Environment Existence of viable infrastructure projects, with definite cash flows Regulatory framework enabling private sector participation in local projects Cash flow generating capability of projects through defined user charges Fiscal and financial capability of the city governments Strong accounting and disclosure standards and good corporate governance Human resource development, with requisite skills

36

Investment financing for urban infrastructure creation, with bond financing as one component, seems to have been more successful where the state governments and the supporting institutions have established complementarities

37

It is to be recognized that developing Subnational bond markets can be more complicated, time-taking, having both national and regional dimensions

38

Thank You

Similar presentations

Specialty Chemicals Conclave - 2008 14-1-2008.>")

Monetary Authority of Singapore.>")