Download presentation

Presentation is loading. Please wait.

1

The Costs of Organization Scott E. MastenJames W. Meehan, Jr.Edward A. Snyder Presented by Carla Fernández-Corrales, Fall 2013 Journal of Law, Economics, & Organization, Vol. 7, No. 1. (Spring, 1991), pp. 1-25. University of MichiganColby College University of Michigan (currently at Yale School of Management)

, pp University of MichiganColby College University of Michigan (currently at Yale School of Management).")

2

Overview Problem for empirical research : Unobservability of transaction costs. Indirect tests are unable to distinguish between market and internal transaction costs. The article focuses on the role of internal organization costs. Econometric methods are applied to analyze a large naval construction project The nature of data allowed them to isolate the effects of transaction on the costs of organizing and to provide dollar estimates.

3

Hypothesis Criticism: Latent costs: for example inflexibility Unquantifiable costs: loses due to withholding of information Institution chosen Internal organization Market exchange Costs of each alternative

4

Reduced-Form Analysis X, Z: vectors of attributes , : vectors of coefficients e, u: normally distributed random variables

5

Direct tests Regression techniques yield dollar estimates of the costs of organization Regression estimation can identify the magnitude of the coefficients to perform test of hypotheses.

6

General hypotheses

7

Empirical setting: naval shipbuilding Final product large, discrete, and immobile during most of its fabrication Assembly must proceed in order Buffer inventories are impractical High complexity High human asset specificityy Physical assets are less specific Mainly involves low technology, labor intensive activities.

8

Specific Hypotheses

9

Data

11

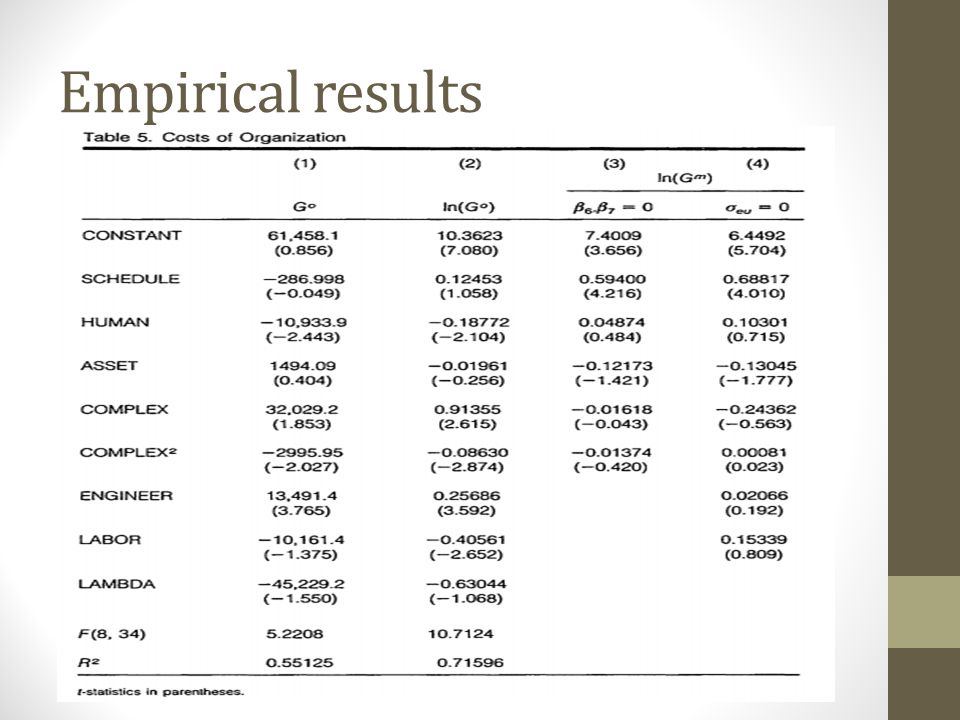

Empirical results

13

Discussion Temporal specificity can be a major determinant of organization. Integration occurs for relation specific human capital and very complex components, but the incentive comes from the internal costs rather than market costs. Relationship specific physical assets reduces the costs of governance. The firm is more likely to integrate engineering intense activities and more likely to internalize labor intense activities.

14

Discussion The independent variables have their principal influence on costs of internal organization. Effects of engineering. Need to know the industry under study. Implications of changes in regulations. Idiosyncrasies of shipbuilding must be taken into consideration.

Similar presentations

:>")