Download presentation

1

SCHOOL BONDS UNDERSTANIDNG YOUR LOCAL DEBT

2

TALKING POINTS Who all is involved? Understanding how forecasting works Typical timeline Other key details Types of bonds TEA presentation on CABs Region 6 Bonds Stats 50-cent test Ongoing matters Tax rate trends 84 th Legislative Session Municipal Advisor Regs SCHOOL PERSPECTIVEFINANCIAL ADVISOR THOUGHTS

3

WHO ALL IS INVOLVED? Financial advisor Critical that ISD makes decisions and verifies assumptions FA should provide advice Bond counsel Provides legal opinion Facilitates IRS paperwork Rating agency(ies) Underwriters Underwriter counsel Only applicable for negotiated bond sales

Underwriters Underwriter counsel Only applicable for negotiated bond sales.")

4

CASH FLOW FORECASTING Assessed valuations Be conservative Consider only forecasting out 5 years Debt service schedule Existing debt coupled with new money sale Repayment structure - escalating or level debt service State aid estimates Permanent School Fund (PSF) Insurance Tax collection rate Tax rate implications

Insurance Tax collection rate Tax rate implications")

5

TYPICAL TIMELINE Preliminary analysis/discussion with FA FA and ISD decide type of bond sale Competitive Negotiated Board approves parameters (negotiated) Bond sale/refunding amount Designate pricing officer Interest rate Term of bonds

Bond sale/refunding amount Designate pricing officer Interest rate Term of bonds")

6

TYPICAL TIMELINE Preliminary official statement review Audited financial statement Current enrollment, financial, and tax data Conference calls with rating agency(ies) 1-2 days before you will receive questions Trends and key indicators are focal points Due diligence call with underwriter counsel Pre-pricing call Review market conditions Pricing of the bonds

1-2 days before you will receive questions Trends and key indicators are focal points Due diligence call with underwriter counsel Pre-pricing call Review market conditions Pricing of the bonds")

7

OTHER KEY DETAILS Bond purchase agreement Pricing certificate Verification report Official statement review Closing agreement Wire funds to FA, bond counsel, rating agency, etc. Pledged securities Don’t forget to contact the bank about the transaction

8

OTHER KEY DETAILS The ISD has choices throughout the process Call dates for the bonds Decision on bond type(s) to use Decision on debt structure Selection of paying agent Selection of underwriters New money sales can result in capitalized interest Cash payment to the issuer to be used to pay future interest (intended to keep tax rate down)

to use Decision on debt structure Selection of paying agent Selection of underwriters New money sales can result in capitalized interest Cash payment to the issuer to be used to pay future interest (intended to keep tax rate down)")

9

TOOLS FOR ISD’S…POLITICAL PLATFORMS FOR OTHERS TYPES OF BONDS

10

Current interest bond (CIBs) are bonds which principal and interest are due periodically. Capital appreciation bonds (CABs) are bonds basically issued at a discount which have no principal or interest payments due until bond matures. Some facts about CABs are as follow: Depending on term of the bond, it can cost more than twice as much as a CIB of the same term CABs do not count against debt limit until the year payment is due

are bonds basically issued at a discount which have no principal or interest payments due until bond matures. Some facts about CABs are as follow: Depending on term of the bond, it can cost more than twice as much as a CIB of the same term CABs do not count against debt limit until the year payment is due.")

11

TYPES OF BONDS During the 83 rd Session, Sen. Juan “Chuy” Hinojosa, D- McAllen, and Rep. Dan Flynn, R-Van, were trying to curtail the use of CABs by enacting the following: Limit CAB percentage of bonded debt to 20% Limit maturity date to no more than 20 years Require school districts to post proposed bond sale details on their website and possibly board agenda

12

TYPES OF BONDS Last year California Governor Jerry Brown approved a bill to limit CABs in the future. Reduced term from 40 to 25 years District repayment ratio must be less than 4:1 (interest to principal) Requires an early repayment option

Requires an early repayment option.")

13

TYPES OF BONDS While it is not a certainty, it is likely another CAB bill will surface during the 84 TH Legislative Session. HB 114 is in the works to be introduced The TEA was asked to present to the SBOE in late September, 2013 and the following slides were major talking points during this meeting.

14

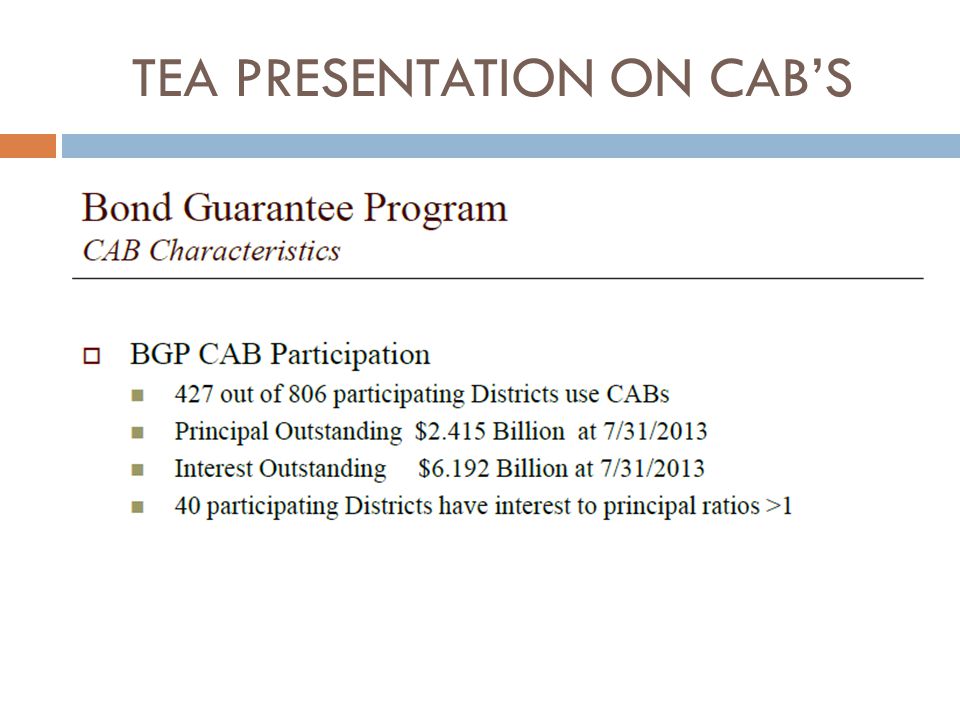

TEA PRESENTATION ON CAB’S

19

REGION 6 ESC BOND STATS 84% of Region 6 districts currently hold I&S debt 63% of Region 6 districts currently holding I&S debt have held CABs within the last five years 53% of Region 6 districts currently holding I&S debt are currently holding CABs

20

REGION 6 ESC BOND STATS Average I&S rate is $0.1855 Number of DistrictsNumber of Districts I&S Rate

21

50-CENT TEST When new debt is issued, I&S tax rate can’t exceed 50 cents per 100 dollar valuation CABs are not subject to the 50 cent test until they reach maturity Provides relief to districts needing to build before the valuations can support the debt Districts are allowed to use EDA/IFA funds and eligible Tier I funds to pass the 50 cent test

22

ONGOING MATTERS Annual Continuing Disclosure reports are required to keep investors informed on financial and operating information Arbitrage – You can not earn higher interest on investment of your bond proceeds than you are paying in interest 3 year working capital exemption Small Issuer Exemption for <$5,000,000/yr. An amount not exceeding the lesser of 5% of the sale proceeds of the issue or $100,000

23

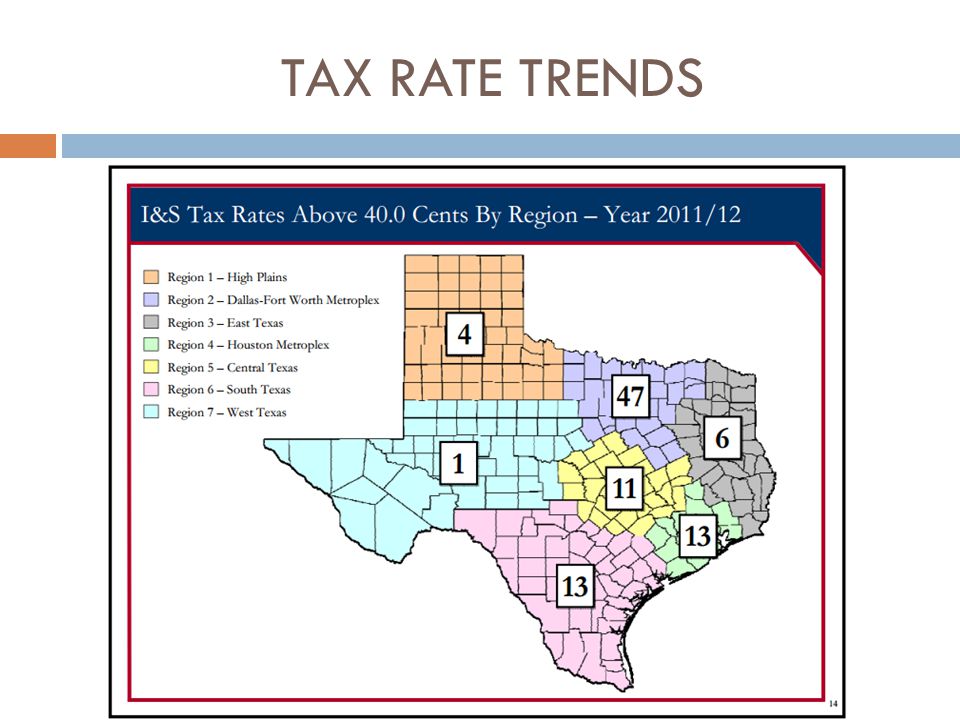

TAX RATE TRENDS

25

84 TH LEGISLATIVE SESSION 83 rd Legislative Session (2013) Limit amount of CAB debt Limit term of CABs Increased information at voting locations and on the ballot 84 th Legislative Session (2015) 50 cent test GO Bonds to require 50% turn-out of registered voters GO Bonds require super-majority to pass Elimination of CABs entirely?

Limit amount of CAB debt Limit term of CABs Increased information at voting locations and on the ballot 84 th Legislative Session (2015) 50 cent test GO Bonds to require 50% turn-out of registered voters GO Bonds require super-majority to pass Elimination of CABs entirely")

26

Municipal Advisor “MA” Regulations Generally, a municipal advisor is defined as a person who solicits or provides financial advice to municipal entities, or obligated persons, with respect to municipal financial products or the issuance of municipal securities. Rule is an extension of the Dodd-Frank Act intended to increase transparency and protect issuers. Verify that your MA is licensed here: http://brokercheck.finra.org/

27

ANSWERS QUESTIONS?

(3) Bonds William P. Scott, Esq. Nixon Peabody LLP.>")

FIN 200: Personal Finance Topic 19–Bonds Lawrence Schrenk, Instructor.>")

Assistant : Sandrine Charron 04 93 95 45 18.>")

or Pay-as you-use (debt)? Which approach is feasible given project costs, fund balances, debt burden, tax rates? How will decision.>")