Download presentation

Presentation is loading. Please wait.

1

Chapter 14. Primary Markets

Traditional Process Regulation Variations in Underwriting

2

Background all types of securities

security being sold for the first time new offerings of firms with publicly held securities -- SEO seasoned equity offering IPOs after initial offering, security is in secondary market

3

I. Traditional Process investment banks play key role

function performed by different institutions roles: (1) advising (2) underwriting/best efforts (3) distribution & support

advising. (2) underwriting/best efforts. (3) distribution & support.")

4

(1) advising timing of offering terms of security pricing regulation

advising timing of offering terms of security pricing regulation")

5

(2) underwriting optional investment bank buys securities from issuer,

then resells to public investment bank bears the price risk

6

price set 2 days prior to issue

security floatation firm commitment resale price - guaranteed price = gross spread = underwriter’s discount

7

size of discount depends on

type of security -- bonds lowest, stock IPOs highest size of issue -- smaller issues have larger discount market conditions .5% - 7% (table 14-1)

")

8

group of investment banks

several investment banks bear price risk lead underwriter -- bulge bracket firm syndicates help underwrite selling group syndicate AND other firms -- help sell issue, do not underwrite

9

tombstone advertisement lists all of the underwriters details of issue

after sale has taken place to get more underwriting business

11

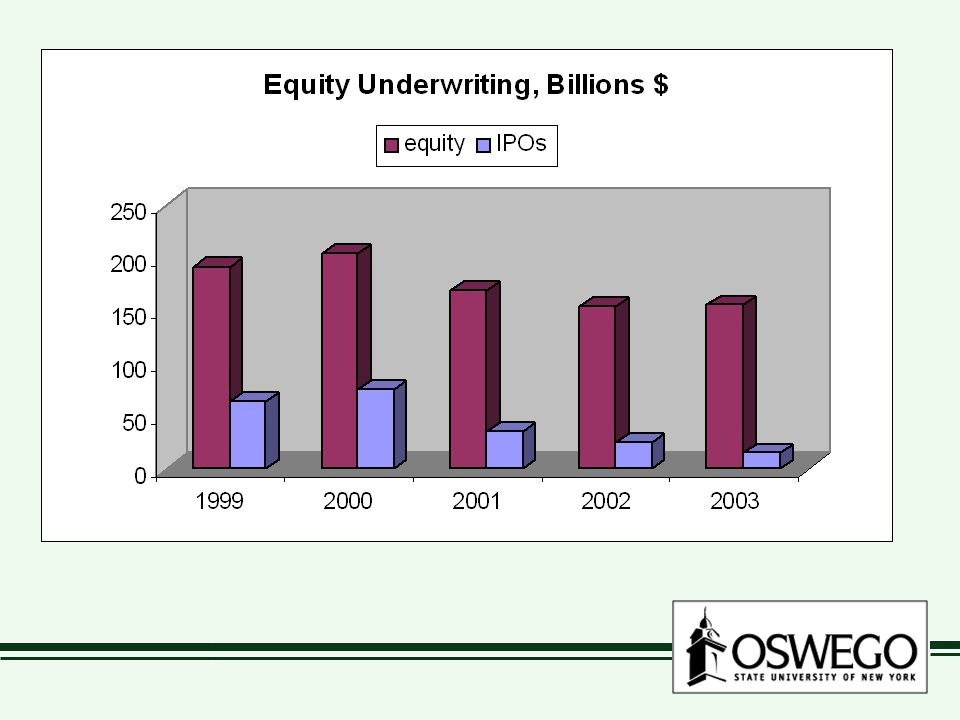

IPOs typically underpriced

1980s: first day return 7% : 15% : 65% why? reduces risk for underwriter issuer accepts underpricing for prestigious underwriter

12

who gets “hot” IPOs? Lucent 1996 Red Hat 1999 (Linux) “spinning”

underwriters allocate shares to preferred customers

13

(2) best efforts placement

alternative to underwriting investment bank promises to use “best efforts” to sell issue but no guarantee of price -- issuer retains price risk done with firms with limited market recognition

14

(3) distribution & support

underwriters expected to support secondary market hold large inventory of securities

15

who underwrites? commercial banks, insurance co.

U.S. firms restricted under Glass Steagall until 1999 no restrictions on firms outside U.S.

16

securities houses top ten underwriters do over 75% of underwriting also leading brokerage firms and dealers

17

top underwriters, 2003 Equity & bonds 1. Citigroup 2. Merrill Lynch

3 . Morgan Stanley

21

II. Regulation SEC regulates primary market disclosure of information

insider trading

22

security registration w/ SEC

prospectus nature of firm features of security risk firm management certified financial statements

23

firms liable for incorrect info

criminal and civil underwriters possibly liable must show due diligence in reviewing info

24

red herring waiting period for SEC approval

firm distributes preliminary prospectus saying so in red ink red herring

25

SEC approval registration is effective SEC determines info is complete

NOT accurate NOT a recommendation investment bank now offers security for sale

26

Shelf registration rule

SEC rule 415 (1982) issuer gets prior approval for several new issues w/in 2-year period investment grade NOT IPOs allows issuer to move quickly when market conditions favorable

issuer gets prior approval for several new issues w/in 2-year period. investment grade. NOT IPOs. allows issuer to move quickly when market conditions favorable.")

27

Exempt from registration

U.S. government debt municipal debt commercial paper small offerings (< $1 million) intrastate offerings

intrastate offerings.")

28

III. Variations in Underwriting

Bought Deal investment bank presents offer to firm to buy entire block of debt securities -- issuer accepts/rejects w/in days -- if accepts, issuer “bought the deal”

29

only 1 underwriter -- greater risk of capital -- issue usually presold to institutional buyers

30

Competitive bidding auction issuer sets terms of issue, places up for bid to competing underwriters -- competition will lower cost required for municipalities, utilities no evidence that this is cheaper

31

Pre-emptive Rights Offering

company w/ stockholders new stock offered to existing shareholders -- below market value -- prevents dillution of voting rights

32

Private Placement issued placed directly with small # of buyers no solicitation/advertising to public buyers are institutional investors -- insurance co., pension funds -- capable of evaluating risks

33

usually bonds no registration w/ SEC -- but must offer prospectus PP are less liquid -- limits on resale for 2 years

34

Growth in private placements

rule 144A (1990) -- allows trading of PP among institutions

-- allows trading of PP among institutions.")

Similar presentations