Download presentation

Presentation is loading. Please wait.

4

We will be using Cornell Note Taking Format Today! Mo Money Mo Problems One Step at a time to Mo Success in Economics class!

5

Unit Five: Learning Objectives: North Clackamas School District Social Studies Priority Standards: Econ 46. Distinguish between fiscal and monetary policies and describe the role and function of the Federal Reserve.

6

Lesson Two: Daily Learning Target I Can define and explain in writing the following key Economic concepts: The Federal Reserve Bank The Money Supply (M1 and M2)

")

7

Money is anything that is generally acceptable that serves as a medium of exchange, a unit of account, and a store of value. What Is Money?

9

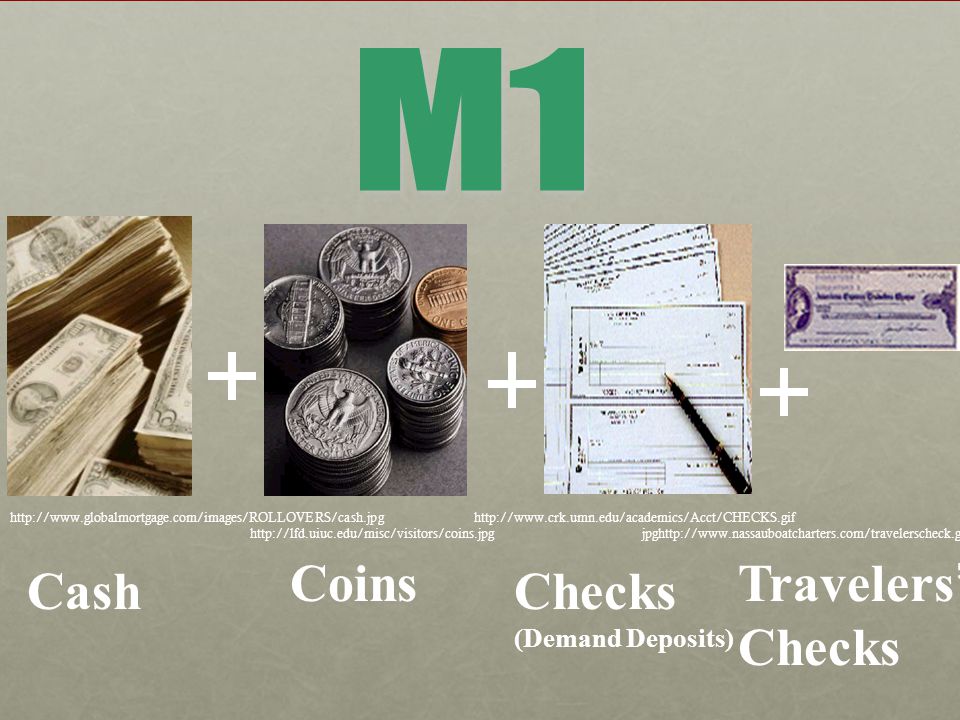

http://www.globalmortgage.com/images/ROLLOVERS/cash.jpg http://lfd.uiuc.edu/misc/visitors/coins.jpg http://www.crk.umn.edu/academics/Acct/CHECKS.gif Cash Coins Checks (Demand Deposits) Travelers’ Checks jpghttp://www.nassauboatcharters.com/travelerscheck.gif

Travelers’ Checks jpghttp://")

10

http://www.catlinbank.com/images/acct/WG-PASSBOOK.gif http://www.pinnbank.com/gifs/photo_moneymarket.gif http://www.cpaofc.com/images/mutualfunds.gif Savings Accounts Money Market (CD’s) Mutual Funds

Mutual Funds")

11

$1,676 billion M 2 [$8,463 billion] M 1 [money or MS] M 2 [near money] Currency 51% Checking Accts 49% Savings Deposits, including Money Market Deposit Accounts 57% Money Market Mutual Funds 9% Small Time Deposits 14% M 1 20% M 1 [money] is part of Traveler’s C hecks $5 B http://www.federalreserve.gov/releases/h6/HIST/h6hist1.htm

![$1,676 billion M 2 [$8,463 billion] M 1 [money or MS] M 2 [near money] Currency 51% Checking Accts 49% Savings Deposits, including Money Market Deposit Accounts 57% Money Market Mutual Funds 9% Small Time Deposits 14% M 1 20% M 1 [money] is part of Traveler’s C hecks $5 B](http://images.slideplayer.com/14/4248536/slides/slide_11.jpg "$1,676 billion M 2 [$8,463 billion] M 1 [money or MS] M 2 [near money] Currency 51% Checking Accts 49% Savings Deposits, including Money Market Deposit Accounts 57% Money Market Mutual Funds 9% Small Time Deposits 14% M 1 20% M 1 [money] is part of Traveler’s C hecks $5 B")

13

Debit Card

14

Federal Reserve note [just a Federal Reserve note]

![Federal Reserve note [just a Federal Reserve note]](http://images.slideplayer.com/14/4248536/slides/slide_14.jpg "Federal Reserve note [just a Federal Reserve note]")

15

A bank is an institution for receiving, keeping, and lending money.

16

Today, the Federal Reserve Bank Oversees banking in the United States. It was not always this way.

17

There was a time when banks were not regulated by the Federal government. Sometimes bankers made poor decisions that bankrupted their banks.

18

Federalists vs. Anti- Federalists At the founding of the nation, Federalists wanted a strong, central bank. At the founding of the nation, Federalists wanted a strong, central bank. Anti-Federalists did not. Anti-Federalists believed that a strong, central bank would only loan to the rich and powerful. Anti-Federalists did not. Anti-Federalists believed that a strong, central bank would only loan to the rich and powerful. Federalists and Anti-Federalist just didn’t agree. Federalists and Anti-Federalist just didn’t agree.

19

Federalists, like Alexander Hamilton, believed that a strong, central bank was essential for the new nation. A strong, central bank could prevent abuses in banking.

20

Anti-federalists, like Patrick Henry, believed that a strong, central bank would have too much power. Wasn’t the revolution about limiting the power of the government?

21

You see, banks make money by loaning money. However, if banks loan money to people who cannot repay their loans, then banks lose money.

22

The Federal Reserve Bank Eventually, it became clear that the nation needed a strong, central bank to oversee banking in America. Eventually, it became clear that the nation needed a strong, central bank to oversee banking in America. A strong central bank could monitor banking in the country and make sure that banks did not make too many loans. A strong central bank could monitor banking in the country and make sure that banks did not make too many loans. A strong, central bank could hold bankers to higher standards thereby protecting consumers. A strong, central bank could hold bankers to higher standards thereby protecting consumers.

23

In the case of banking, the Federalists may have been right. A central bank does prevent abuses in banking.

24

The Fed The Federal Reserve Bank is commonly referred to as the “Fed.” The Federal Reserve Bank is commonly referred to as the “Fed.” The Federal Reserve Bank can make loans to banks, raise or lower interest rates, and require banks to hold adequate reserves. The Federal Reserve Bank can make loans to banks, raise or lower interest rates, and require banks to hold adequate reserves. The Fed helps banks across America. The Fed helps banks across America. No Dough Bank

25

Philadelphia 3 San Francisco 12 1 Boston 4 Cleveland 9 Minneapolis 11 Dallas Washington, D.C. (Board of Governors) 10 Kansas City 7 Chicago 5 Richmond 2 New York Atlanta 6 St. Louis 8 A. Boston B. New York C. Philly D. Cleveland E. Richland F. Atlanta G. Chicago H. St. Louis I. Minneapolis J. Kansas City K. Dallas L. San Francisco

10 Kansas City 7 Chicago 5 Richmond 2 New York Atlanta 6 St. Louis 8 A. Boston B. New York C. Philly D. Cleveland E. Richland F. Atlanta G. Chicago H. St. Louis I. Minneapolis J. Kansas City K. Dallas L. San Francisco.")

26

7 th -G-Chicago (1) 8 th -H-St. Louis (3) 9 th - I -Minneapolis (1) 10 th -J-Kansas City (3) 11 th -K-Dallas (3) 12 th -L-San F rancisco (4) 1st-A-Boston (0) 2 nd -B-New York (1) 3 rd -C-P hiladelphia (0) 4 th -D-Cleveland (2) 5 th -E-Richmond (2) 6 th -F-Atlanta (5)

9 th - I -Minneapolis (1) 10 th -J-Kansas City (3) 11 th -K-Dallas (3) 12 th -L-San F rancisco (4) 1st-A-Boston (0) 2 nd -B-New York (1) 3 rd -C-P hiladelphia (0) 4 th -D-Cleveland (2) 5 th -E-Richmond (2) 6 th -F-Atlanta (5).")

28

[thousands]

![[thousands]](http://images.slideplayer.com/14/4248536/slides/slide_28.jpg "[thousands]")

29

Destroy/Issue paper notes The Fed clears 40%; The Fed clears 40%; Banks clear rest electronically.

30

$97.50 +30% The Fed controls the banks’ ability to create new money to ensure the economy doesn’t get too much money, nor too little. Overfed Fed just right 1980 1983 $75.00 Money Prices Underfed And – so it is with money. Not too much, not too little.

31

Saving and Investing When a person saves money, he is storing money. When a person saves money, he is storing money. When a person invests money, he is trying to significantly increase his money. When a person invests money, he is trying to significantly increase his money. Investing money involves greater risk but also potentially greater gain. Investing money involves greater risk but also potentially greater gain.

32

People invest when they buy stocks and bonds.

33

Stocks and Bonds When a person buys stock, he is buying partial ownership in a corporation. When a person buys stock, he is buying partial ownership in a corporation. When a person buys a bond, he is loaning money to a corporation or government. When a person buys a bond, he is loaning money to a corporation or government.

34

There is an old investment Poem: Stocks, you own. Bonds, you loan.

35

Interest is the price of borrowed money.

36

Interest When money is deposited in a bank, the customer receives interest on the money. When money is deposited in a bank, the customer receives interest on the money. A person who borrows money must pay interest. A person who borrows money must pay interest. Interest is the price of borrowed money. Interest is the price of borrowed money.

37

Default When a person fails to pay back a loan, he has defaulted on the loan. When a person fails to pay back a loan, he has defaulted on the loan. Defaulting on a loan leads to bad credit and higher interest rates in the future. Defaulting on a loan leads to bad credit and higher interest rates in the future. By defaulting, a person ruins his reputation for repaying a loan. By defaulting, a person ruins his reputation for repaying a loan.

38

Housing Boom and Bust From 2000 to 2006, house prices in the U.S. skyrocketed. Many factors contributed to this boom, but bank lending practices played a major role. From 2000 to 2006, house prices in the U.S. skyrocketed. Many factors contributed to this boom, but bank lending practices played a major role. Deregulation changed banks from local institutions into national megabanks. Instead of collecting payments on a mortgage for 30 years, banks began to sell these loans to other financial institutions for a quick profit. Deregulation changed banks from local institutions into national megabanks. Instead of collecting payments on a mortgage for 30 years, banks began to sell these loans to other financial institutions for a quick profit.

39

Housing Boom and Bust Banks became less interested in verifying that clients could repay a mortgage and more interested in making as many mortgage loans as possible. The easy money fueled the housing price bubble. Banks became less interested in verifying that clients could repay a mortgage and more interested in making as many mortgage loans as possible. The easy money fueled the housing price bubble.

40

There are many financial intermediaries to help people invest.

41

Financial Intermediaries A financial intermediary transfers money from savers to borrowers. A financial intermediary transfers money from savers to borrowers. Financial intermediaries can help a person invest. Financial intermediaries can help a person invest. Banks, finance companies, and mutual funds are examples of financial intermediaries. Banks, finance companies, and mutual funds are examples of financial intermediaries.

42

By investing in a variety of stocks and bonds, a person reduces his risk.

43

The key is: Diversification The idea of spreading out investments to reduce risk is called diversification. The idea of spreading out investments to reduce risk is called diversification. Think of diversification as not putting all your eggs in one basket! Think of diversification as not putting all your eggs in one basket! By investing in a variety of stocks and bonds, the investor is less likely to lose his entire investment. By investing in a variety of stocks and bonds, the investor is less likely to lose his entire investment.

44

Let’s reemphasize the main point here! Don’t “put All your eggs in one basket!” Have a plan B (or C or D for that matter). We all know the real path to success & happiness in life is to? Marry a Kardashian!

. We all know the real path to success & happiness in life is to. Marry a Kardashian!.")

46

Work on Your Project!

Similar presentations

and borrowers.>")