Download presentation

Presentation is loading. Please wait.

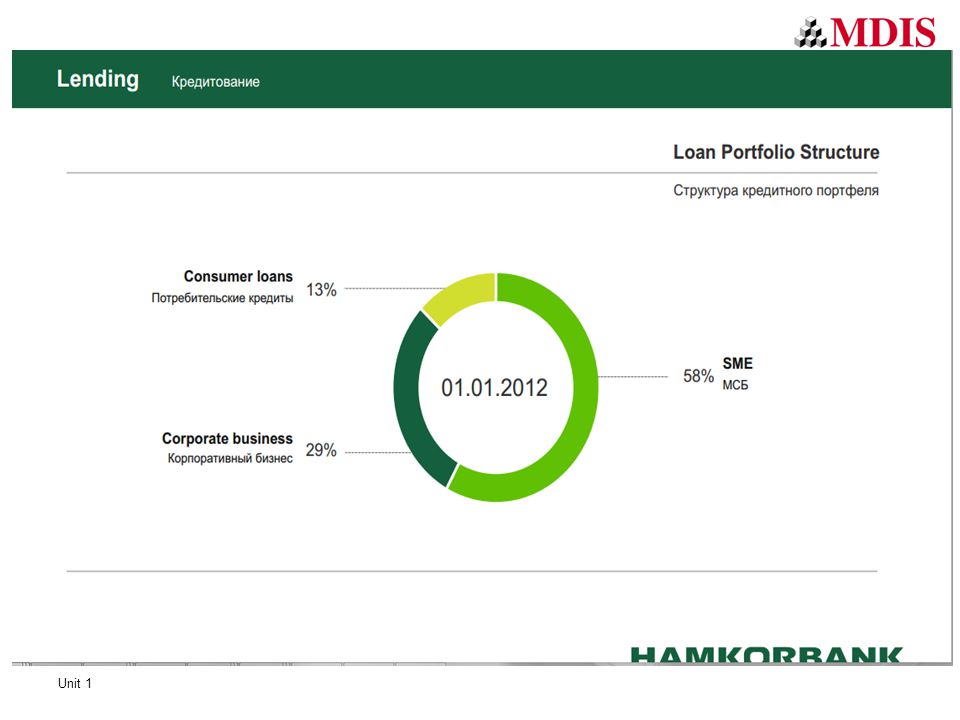

1

Unit 1 Risk Management in Banking

2

Unit 1 READ: Bessis 3 rd edition, Sections 2, 5, 6 Home Review Questions: Discuss the various types of banking business lines. Explain the difference between the banking book and the trading book. Describe types of banking risks. Discuss banking regulations in place and its purpose. Conduct a research in the area of the Basel Accord to explore how the capital adequacy requirement has evolved since its inception until today and evaluate its effectiveness. Explain the types of risk measures in banking. Additional reading (Study pack notes are taken from this book) Anthony Saunders:Financial Institutions Management- A risk management approach, 6th edition.

Anthony Saunders:Financial Institutions Management- A risk management approach, 6th edition..")

3

Unit 1 Risk Management in Banking Unit 1 BANKING RISKS AND RISK REGULATIONS

4

Unit 1 Learning Objectives By the end of this unit, you should be able to: Discuss the various types of banking business lines. Explain the difference between the banking book and the trading book. Describe types of banking risks. Discuss banking regulations including the Basel Accord. Explain the types of risk measures in banking. YESTERDAY TODAY

5

Banking Business Lines 1.Commercial banking which comprise of: –retail banking –corporate banking 2.Investment banking 3.Trading – which comprise of: –The bank’s proprietary trading –trading for third parties 4.Private banking 5.Custody – asset management and advisory services. Unit 1

6

Banking Book vs Trading Book The Banking Book The banking book records all commercial banking transactions including all lending and borrowing activities. It is based on the buy and hold principle and accounting rules rely on book values of assets and liabilities. Liquidity and interest risk arise due to maturity mismatch and mismatch due to fixed and variable interest rates differences of loans and deposits. Loans in the asset of the banking portfolio are also exposed to credit risk. However, there is no market risk in the banking portfolio. Asset-Liability Management (ALM) is used to manage the liquidity and interest rate risk. Unit 1

is used to manage the liquidity and interest rate risk. Unit 1.")

7

Banking Book vs Trading Book The Trading Book The trading book records all market transactions tradable in the market. It is accounted for based on the Profit and Loss (P&L) resulting from changes in the mark-to- market values of instruments held. The market portfolio gives rise to market risk – risk of adverse change to the market value of the instrument held, and market liquidity risk – risk that low volumes of trade that result in downward price movement. For non-tradable instruments including derivatives such as swaps and over-the-counter options, credit risk exposure should be considered – risk of loss if the counterparty fails. Unit 1

resulting from changes in the mark-to- market values of instruments held. The market portfolio gives rise to market risk – risk of adverse change to the market value of the instrument held, and market liquidity risk – risk that low volumes of trade that result in downward price movement. For non-tradable instruments including derivatives such as swaps and over-the-counter options, credit risk exposure should be considered – risk of loss if the counterparty fails. Unit 1.")

8

Basel I and II Capital = Exposure x Risk Weight x 8% Cooke ratio and Credit Risk (1988) Inclusion of Market Risk component (1996) Basel II (2007) –Min. Capital requirements: credit, market, operation risks –Supervisory review –Market discipline Unit 1

9

Basel II Credit Risk Components PD EAD LGD Credit conversion factor (for off-balance sheet exposures) Unit 1

Unit 1")

10

Basel II Risk weights vary by Asset classes: Corporate Banks Sovereign Retail customers and SMEs Equity Unit 1

11

Basel II THREE approaches to RISK WEIGHTS: Standardised Foundation (IRB) – banks own assessment of PD but Basel Standardised rules for LGD and EAD Advanced (IRB) – both PD and LGD inputs are internal In all cases, capital is calculated using IRB formulas Unit 1

– banks own assessment of PD but Basel Standardised rules for LGD and EAD Advanced (IRB) – both PD and LGD inputs are internal In all cases, capital is calculated using IRB formulas Unit 1")

12

Function of risk (economic) capital Protection against UNEXPECTED losses

capital Protection against UNEXPECTED losses")

13

Bank’s Product Lines 1.Retail financial services 2.Corporate Lending 3.Off-balance sheet transactions 4.Specialized finance 5.Market transactions Unit 1

14

Review or Tutorial Questions Discuss the various types of banking business lines. Explain the difference between the banking book and the trading book. Describe types of banking risks. Discuss banking regulations in place and its purpose. Conduct a research in the area of the Basel Accord to explore how the capital adequacy requirement has evolved since its inception until today and evaluate its effectiveness. Explain the types of risk measures in banking. Supp. Reading: Anthony Saunders:Financial Institutions Management- A risk management approach, 6th edition.\

15

Off-balance Sheet Transactions Off-balance sheet transactions are contingencies given and obtained. They include: –guarantees provided, –committed credit lines not yet drawn down or stand-by lines of credit. Derivative such as swaps, futures and options are off-balance sheet market transactions where obligation to make agreed payments are contingent on the occurrence of a specified event. Unit 1

16

Bank’s Financial Statements 1.The balance comprise of four levels: –Treasury and banking transactions –Intermediation –Financial assets –Long-term assets and liabilities 2.Income Statement –Fair value accounting requires the banking book to be mark-to-market. Unit 1

17

Banking Risks Credit Risk Interest rate risk Market risk Liquidity risk Operational risk Foreign exchange risk Country risk Performance risk Settlement risk Solvency risk Model risk Unit 1

18

Banking Regulations The regulators goals are: –Manage systemic risk –Promote a level playing field –Promote sound practices that contribute to financial system safety. Unit 1

19

Capital Adequacy Oversight body of the Basel Committee on Banking Supervision. Cooke Ratio (Basel I) Second Basel Accord (Basel II) Basel III Unit 1

Second Basel Accord (Basel II) Basel III Unit 1.")

20

Risk Measures Quantitative measures of risks comprise of three categories: –Sensitivity: Sensitivity measures the variation of a variable due to the unit movement of a single market factor. –Volatility: Dispersion around the average, including both the upside and downside. –Downside measures of risk: focuses on the adverse deviation only Unit 1

21

Financial Services Industry Depository Institutions- commercial banks, savings institutions, credit unions(non-profit) i.sources and uses of funds, assets, liabilities, equity, off-balance sheet activities,other fee-generating activities Non-depository Institutions:Insurance Companies-Life and property i.Assets, liabilities, balance sheet, underwriting risks, loss risks, reinsurance Securities Firms and Investment Banks i.investing, investment banking, market making, trading, cash management, mergers & acquisitions. ii.Assets,liabilities, balance sheet, regulation (unethical activities by Bear Stearns, Lehman Brothers, Merrill lynch) Unit 1

Unit 1.")

22

Non-depository Institutions Mutual Funds i.Long term-Bond funds, equity funds, hybrid funds, Short-term- money market mutual funds. ii.Mutual funds- open-end and closed-end Hedge Funds i.More risky, moderate risk, risk-avoidance ii.Regulation of hedge funds-mostly unregulated Finance Companies i.Sales finance institutions, personal credit institutions, business credit institutions ii.Assets, liabilities and equity Unit 1

26

Credit risk Level of importance Commercial bank: HSBC Amount of risk Market risk Operational risk

27

Market risk Level of importance Investment bank: UBS Amount of risk Operational risk Credit risk

28

Market risk Level of importance Trading house: Goldman Sachs Amount of risk Credit risk Operational risk

29

Level of importance Asset manager: L & G Amount of risk Market risk Credit risk

Similar presentations

and borrowers.>")

1 Risk Management in Financial Institutions (II): Hedging with Financial Derivatives Forwards Futures Options.>")