Download presentation

Presentation is loading. Please wait.

1

Lecture 11

2

Topics Pricing Delivery Complications for both Multiple assets can be delivered on the same contract…unlike commodities The deliverable assets all have different prices

3

Copyright: CME Group 2011 Product “Eligible” Maturity Face Amount Min. Tick Values

4

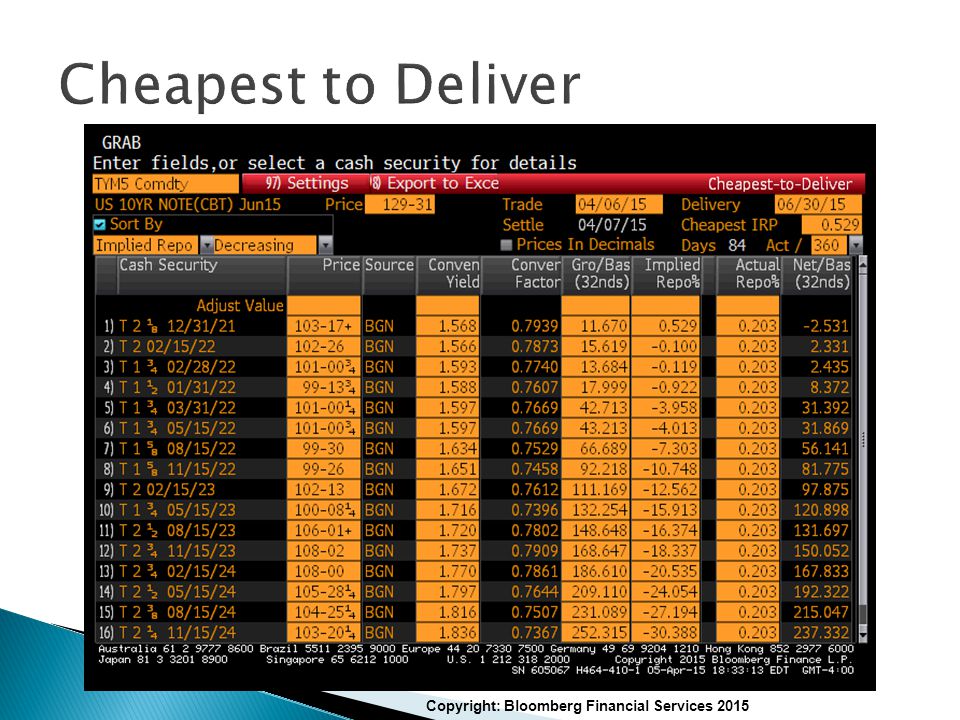

Cheapest to Deliver Delivery = Treasury futures allow the short position to select which bond to deliver (or sell) to the long futures position. The short will deliver the bond which is the least costly for the short position to purchase. This occurs since only 4 contracts are used to hedge all interest rate instruments. Thus, a real underlying asset does not exist. Certain bonds are “eligible” for delivery

5

Copyright: Bloomberg Financial Services 2015

9

Conversion Factor Bond prices vary for many reasons ◦ Higher coupons have higher prices ◦ Lower coupons have lower prices ◦ Longer maturities have higher prices ◦ Shorter maturities have lower prices If you deliver a more expensive bond, the amount you receive at delivery goes up If you deliver cheap bond, the amount you receive at delivery goes down

10

Quoted price = Price of the bond as quoted in the paper Accrued interest = amount of coupon earned on a bond since the last coupon payment Bond Cash Price = (Quoted price of bond X notational amount) + accrued interest Invoice Amount = Amount of money that is exchanged when a futures contract bond is delivered

+ accrued interest Invoice Amount = Amount of money that is exchanged when a futures contract bond is delivered")

12

Example What is the cash price of a bond that pays a 4% semiannual coupon and matures in 12 years and three months, if the YTM is 6.5%? Price FV = 1000 Pmt = 20 int = 3.25 n = 24.50 Solve for PV = $781.20 Quoted Price = 78.12

13

Example (continued) What is the cash price of a bond that pays a 4% semiannual coupon and matures in 12 years and three months, if the YTM is 6.5%? Accrued InterestBond Cash Price

14

Conversion Factor Since the bond we deliver is not specified in the futures contract, the price of the bond must be standardized. The conversion factor converts the futures price into a settlement or invoice price. The conversion factor is the present value of $1 at YTM=6%, assuming coupons are paid semiannual. Repo Rate Difference between the conversion factor yield of 6% and the coupon on the bond.

15

Used to convert futures prices to bond prices What is the cash price of a bond that pays a 4% semiannual coupon and matures in 12 years and three months, if the YTM is 6.5%? Using exact dates on a HP12c provides 82.824

16

Also called the Adjusted Futures price Cash Price = Futures Price x Conversion Factor Futures Price = Cash Price / Conversion Factor

17

Invoice Amount = Futures Price x Conversion factor x Contract Size + accrued Interest Total amount of money exchanged at delivery

18

Futures Price Calculation The price of a treasury futures contract. The price is merely the future value of the spot price of the treasury, less PV of the coupons. This assumes a flat yield curve. I = present value of coupons

19

Example Compute the conversion factor of a bond with exactly 9 years to maturity a 5% coupon, paid semiannually, and a YTM of 4.8%.

20

Example (continued) Compute the quoted price of the bond with exactly 9 years to maturity a 5% coupon, paid semiannually, and a YTM of 4.8%. Price FV = 1000 Pmt = 25 int = 2.4 n = 18 Solve for PV = $1014.48Quoted Price = 101.45

21

Example (continued) Compute the price of the 9 month futures contract. Remember the next coupon payment will be made in 6 months.

22

How To Calculate Delivery Cost (steps) 1 - Look up the price (FP) 2 - Compute “Conversion Factor” (CF) 3 - CF x FP x (contract size) + (accrued interest) = Delivery cost

1 - Look up the price (FP) 2 - Compute Conversion Factor (CF) 3 - CF x FP x (contract size) + (accrued interest) = Delivery cost")

23

The CTD can be found three ways 1. Quoted Bond Price – (Futures Price x CF) Also called the “Gross basis” Select the lowest 2. Invoice Amount (lowest) Also called the “Delivery Cost” 3. Highest Repo Rate The interest rate earned by short selling a security and buying it back later.

Also called the Gross basis Select the lowest 2. Invoice Amount (lowest) Also called the Delivery Cost 3. Highest Repo Rate The interest rate earned by short selling a security and buying it back later..")

24

Theoretical Futures Price (FP)? 3 Ways to Derive CTD 1 – Highest Repo Rate ( The interest rate earned by short selling a security and buying it back later. ) 2 - Calculate Futures Delivery Spot Price 3 - Cost of Delivery (“Gross Basis”) Accrued interest and others items

2 - Calculate Futures Delivery Spot Price 3 - Cost of Delivery ( Gross Basis ) Accrued interest and others items.")

25

Example Two bonds are eligible for delivery on the June 2012 T Bond Futures K 1 - 9.875Nov38 deliveries on 15th of maturity month 2 - 7.25May39 On June 12, you announce to deliver a bond

26

Q: If YTM = 5%, which will you deliver and what is its price? A: CFBond PriceFC Spot Price 9.875Nov381.51171.05113.28 7.25May391.17133.09113.75 Deliver 9.875 Nov38

27

Q: If YTM = 9%, which will you deliver & what is its price? A: CFBond PriceFC Spot Price 9.875Nov381.51108.7672.03 7.25May391.1782.3670.39 Deliver 7 1/4 May39

28

Q: If YTM = 7% and the listed futures price is 110.50, which bond is CTD? A: 9 7/8Nov38CTD = 134.39 - (110.5 x 1.51) = -32.47 7 1/4May39CTD = 103.00 - (110.5 x 1.17) = -26.29 Implied Repo Rate Cost of Carry

= /4May39CTD = (110.5 x 1.17) = Implied Repo Rate Cost of Carry.")

Similar presentations

t FUTURE VALUE OF A SUM F v INVESTED TODAY AT A RATE r FOR A PERIOD t :>")

, maturity –Risk-free interest rates.>")