Download presentation

Presentation is loading. Please wait.

1

Military Taxpayers MSgt Lance A. Bonlender, EA November 20, 2007

2

Happy Veteran’s Day A veteran – whether active duty, retired, national guard, or reserve – is someone who, at one point in his life, wrote a blank check made payable to ‘The United States of America’, for an amount of ‘up to and including his life.’ That is Honor, and there are way too many people in this country who no longer understand it. --Author Unknown

3

Agenda Active Duty vs Reserve Component AZ Taxable Income State of Domicile AZ Tax Return Requirements Credit for Employing National Guard Members Other Military Issues References IRS Pub 3, Armed Forces’ Tax Guide AZ Pub 704, Taxpayers in the Military AZ Individual Income Tax Ruling (ITR) 97-3 AZ Form 333

97-3 AZ Form 333")

4

What’s the difference between the National Guard or Reserves and Active Duty? Some of you may think….

7

“One weekend a month, two weeks a year” Former slogan used by the U.S. Army National Guard Indicated the time needed to gain benefits Dropped during the Iraq War

8

US Army Reserve

9

“You study hard, you do your homework and you make an effort to be smart, you can do well. If you don’t, you get stuck in Iraq.” Senator John Kerry, to a group of college students in California

10

Minnesota National Guard

11

Active Duty Davis Monthan AFB Title 10 of the U.S. Code Federal missions Residents of states they enlist in (except…) Members directed to change stations (PCS)

Members directed to change stations (PCS).")

12

Reserve Component Title 32 of the U.S. Code 162 nd FW State and Federal missions Can be called up by Governor or President Generally a resident of state they serve Members choose to change assignments Part-time or Full-time (civil service or AGR) Reserves – Federal mission only

Reserves – Federal mission only.")

13

Arizona Tax Treatment of Military Pay This has changed over the last 3 years.

14

Prior to Tax Year 2006 All military pay taxable on federal return was taxable by state of Arizona.

15

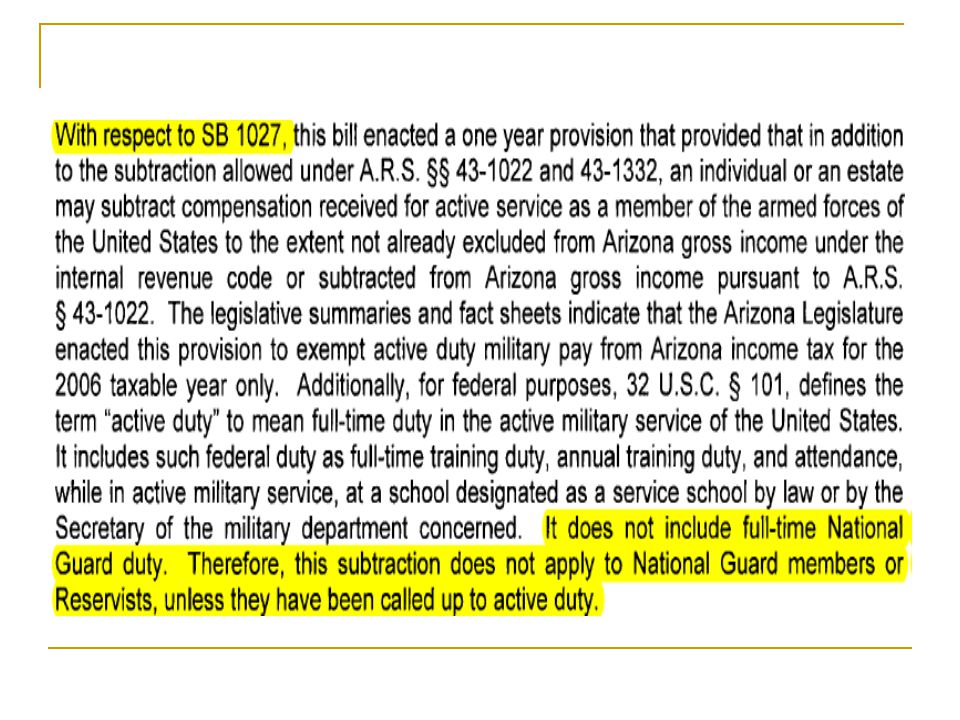

Tax Year 2006 only Senate Bill 1027 (passed in 2005): This bill exempted active duty military pay from Arizona income tax. Additionally, in cases where a taxpayer’s only source of income is active duty pay, the taxpayer is exempt from filing an Arizona income tax return.

18

After Tax Year 2006 House Bill 2795 (passed in 2006): Makes permanent the state income tax exemption for active duty members. Additionally, it expands the exemption to include the military income of reservists and members of the National Guard.

20

State of Domicile Active Duty Member’s State of Domicile W-2 Box 15 (State) Go to that state’s website Search on ‘military’

Go to that state’s website Search on ‘military’")

21

Arizona Tax Return Requirement (S) Non-Resident no other income – No (S) Non-Resident with part-time job – Yes If income exceeds AZ AGI or to claim AZ refund This is where it can become tricky. (MFJ) Spouse’s State of Residence? (MFJ) AZ Resident Spouse no income – No (MFJ) AZ Resident Spouse / w/income – Yes MFS…even trickier – review AZ Pub 704.

Spouse’s State of Residence. (MFJ) AZ Resident Spouse no income – No (MFJ) AZ Resident Spouse / w/income – Yes MFS…even trickier – review AZ Pub")

22

Community Property States AZ Individual Income Tax Ruling (ITR 97-3) “Ruling: An Arizona resident married to a nonresident active duty military member who is a resident of a community property state is not subject to Arizona income tax on his or her community property interest in the military spouse’s active duty military pay. However, the nonmilitary resident spouse is taxable on all separate income and one-half of community income from all other sources.”

23

Group Test: File Which AZ Form? 1. (S) AZ resident, no other income? 2. (S) AZ resident, earns $7,000 at Wendy’s? 3. (S) AK resident, earns $7,000 at Wendy’s? 4. (MFJ) both are AZ residents, two incomes? Those were the easy ones. 5. (MFJ) military spouse, CT resident; non- military spouse, AZ resident; two incomes? 6. (MFJ) military spouse and non-military spouse are FL residents; two incomes?

AZ resident, earns $7,000 at Wendy’s. 3. (S) AK resident, earns $7,000 at Wendy’s. 4. (MFJ) both are AZ residents, two incomes. Those were the easy ones. 5. (MFJ) military spouse, CT resident; non- military spouse, AZ resident; two incomes. 6. (MFJ) military spouse and non-military spouse are FL residents; two incomes .")

24

Last Test Question 7. (MFS) military spouse, CA resident; non- military spouse, AZ resident; two incomes?

military spouse, CA resident; non- military spouse, AZ resident; two incomes .")

25

AZ Tax Credit – AZ Form 333 Credit for Employing National Guard Members $1,000 for each employee called to active duty Employee must be member of AZ National Guard Employee must be full-time when called to active duty Must be called for more than the required annual training period Employer may claim only once per year per employee called to active duty Available to individuals, C-Corps, and S-Corps Credit may be passed through to partners and shareholders

26

Other Military Issues (IRS Pub 3) Combat Pay exclusion – will not be included in Box 1 of W-2 Can use combat pay to calculate EITC Section 121 exclusion – suspend test period 10% withdrawal penalty exception Moving Expenses – DITY moves can result in taxable income reported on a W-2 Miscellaneous Itemized Deductions Uniforms….”it depends” Haircuts….of course not!

Combat Pay exclusion – will not be included in Box 1 of W-2 Can use combat pay to calculate EITC Section 121 exclusion – suspend test period 10% withdrawal penalty exception Moving Expenses – DITY moves can result in taxable income reported on a W-2 Miscellaneous Itemized Deductions Uniforms…. it depends Haircuts….of course not!")

27

Other Military Issues (con’t) The Heroes Earnings Assistance and Relief Tax Act of 2007 (Senate is expected to pass soon after Thanksgiving holiday): Includes Make permanent using combat pay for EITC Tax free military death gratuity rollovers to IRAs REVENUE RAISING PROPOSALS!!!!!!! VITA offices on military bases May limit the number of military returns off base I see higher ranking individuals / complex issues

28

Retirement Active Duty Can retire after 20 years of military service Will receive military retirement pay after retiring Could be 37 if they enlisted at age 17 National Guard Reserves Can retire after 20 years of total military service Must wait until age 60 to receive military retirement pay Arizona Residents: Can exclude up to $2,500 from taxable income on the Arizona return.

29

"We are not retreating—we are advancing in another direction." General Douglas MacArthur (1880–1964), American Soldier

, American Soldier")

30

Questions?

Similar presentations