Download presentation

Presentation is loading. Please wait.

1

Contract and Certificate of Insurance Review Welcome! Sept. 15, 2014

2

What is a Contract Foundation of all business relationships A contract is a voluntary and legally binding agreement between two or more competent parties Each party to the contract makes certain promises

3

Contracts When you enter into a contract with another party, each side makes promises, such as: To undertake to do certain work To pay for the work done To indemnify and hold harmless the party who is having the work done

4

Contracts are a method of transferring liability – unfortunately it’s often overlooked Hold harmless agreements Indemnification clauses Waivers Releases Disclaimers

5

Examples of Contracts Construction – roads, buildings Services – snow removal, arborist Employment – Mutual Aid Agreement (Fire), 911 routing Rental - Arena Ice Time, Community Centre etc. Partnership Agreements Lease Space

6

Clauses in a Contract: What to look for Who are the parties involved? What is the intent of the contract? Does the contract clearly outline the responsibilities of all parties? How does the contract deal with emergencies? How can the contract be terminated?

7

If the contract runs indefinitely, is it to be reviewed on a regular basis? What types and amounts of insurance are required? Which party is protected by the indemnity clause? Prior to signing, has the contract been reviewed by the risk manager and legal counsel?

8

Parties to Consult 1.Lawyer A contract is a legally binding agreement between 2 or more persons for a particular purpose

9

2.Insurance Broker/Company The insurance requirements of some contracts reflect a lack of understanding of the nature and scope of insurance. In many cases, the requirements either make no sense, are contrary to the interests of the client, or are impossible to accommodate.

10

Environmental Impairment Liability/Pollution Legal Liability/Contractors Pollution Liability insurance (or equivalent) including bodily injury, property damage and clean up, with coverage including the activities and operations conducted by the Contractor and the Contractor’s employees, Directors, Officers, subcontractors and agents. This policy will (1) be written on an occurrence basis with coverage for any one occurrence or claim of not less than Seven Million Dollars ($7,000,000) with an aggregate limit of not less than Fourteen Million Dollars ($14,000,000) (2) name the Entity as additional insured and

be written on an occurrence basis with coverage for any one occurrence or claim of not less than Seven Million Dollars ($7,000,000) with an aggregate limit of not less than Fourteen Million Dollars ($14,000,000) (2) name the Entity as additional insured and.")

11

4 Important Items Indemnity Clause Types and Amount of Insurance Additional Insured Certificate of Insurance

12

Indemnity Clauses Indemnity The act or making someone “whole” or protected from any losses which have occurred or will occur. Indemnify To guarantee against any loss which another may suffer.

13

Hold harmless A promise to pay any cost or claims which may result from an agreement Indemnification/Hold Harmless Clause Is only as good as the guarantor of the indemnity Indemnity should be guaranteed by Insurance

14

There must be a promise to indemnify and defend Who is to be protected Against what (types of actions/claims)

")

15

Resulting from what causes Caused by Whom What are the limitations

16

Sample Indemnification/ Hold Harmless Clause The Service Provider shall indemnify and hold harmless the School, its officers, members of school council and employees from and against any liabilities, claims, expenses, demands, loss, cost, damages, actions, suits or other proceedings by whomsoever made, directly or indirectly arising out of the Contract attributed to bodily injury, sickness, disease or death or to damage to or destruction of tangible property including loss of revenue or incurred expense resulting from disruption of service and caused by any acts or omissions of the Service Provider, its officers, agents, servants, employees, customers, invitees or licensees, or occurring in or on the premises or any part thereof and, as a result of activities under this agreement.

17

To ensure that the indemnifying party has the resources to fulfill this promise, a certain amount of insurance is typically required as a part of the agreement

18

Insurance A reliable method of having funds to pay for losses A universally accepted method of financing an indemnity In the contract you must ensure that the type and amount of insurance requested are being provided

19

What Should be Included in the Insurance Clause? Additional Insured Cross liability clause Severability of interest clause Contractual liability

20

Employers liability Products and completed operations Broad form property damage Pollution from hostile fire

21

Where the work involves the handling of asbestos, coverage must not contain an asbestos exclusion Where the work involves the use of explosives (blasting), vibration (pile driving), removal or weakening of support of any property, building or land (natural or otherwise)…..

, vibration (pile driving), removal or weakening of support of any property, building or land (natural or otherwise)…..")

22

Explosion, Collapse or Underground coverage's must be added (XCU)

")

23

Explanation of Terms Cross Liability The insurance policy will apply to each insured as if it was the only insured. This triggers the policy to respond if a claim is made by one insured against another.

24

Severability of Interests The insurance policy applies separately to each insured who has a claim brought against them Waiver of Subrogation When the insurer waives its right of recovery against the responsible third party

25

Sample Insurance Requirements “______________”, at his or her expense, obtain and keep in force during the term of this agreement, Commercial General Liability Insurance satisfactory to the _____________, be written by an insurer licensed to conduct business in the province of __________ and include but not limited to the following: A.A limit of liability not less than $X,000,000/occurrence. B.The School shall be named as additional insured; C.The policy shall contain a provision for cross liability in respect of the named insured; D.Non-owned automobile coverage with a limit of $X,000,000, including contractual non-owned coverage; E.Products and completed operations coverage (broad form) with an aggregate limit not less than $X,000,000. F.That 30 days prior notice of an alteration, cancellation or material change in policy terms which reduces coverage’s shall be given in writing to the Township. G.Hostile Fire The insurance clause should include a Severability of interest clause, Contractual Liability – Oral & Written, Contingent Employer’s Liability, Employer’s Liability, Broad Form Property Damage, Pollution from a Hostile Fire.

with an aggregate limit not less than $X,000,000. F.That 30 days prior notice of an alteration, cancellation or material change in policy terms which reduces coverage’s shall be given in writing to the Township. G.Hostile Fire The insurance clause should include a Severability of interest clause, Contractual Liability – Oral & Written, Contingent Employer’s Liability, Employer’s Liability, Broad Form Property Damage, Pollution from a Hostile Fire..")

26

Occurrence vs. Claims Made Policy Forms Occurrence Policy Form Coverage for claims that occurred during the policy period Trigger is when the event occurred that gave rise to the claim The policy that was in effect when the claim occurred is the responding policy

27

Claims Made Policy Form Triggered when the claim is first reported There must be policy in place when the claim is made

28

Claims Made Policies Request Extended Reporting Period Cancellation Notice Insured vs. Insured Exclusion carved out if you wish to be added as an “Additional Insured”

29

Additional Insured Additional Insured vs. Named Insured Additional Insured gives you a defense without the obligations of a named insured under an insurance contract A named insured owns the policy, can make changes to the policy and has to pay for the policy.

30

Purpose of Being an Additional Insured The additional insured gets added to the insurance policy with respect to the operations of the named insured Provides a legal defense and indemnity coverage

31

Allows for the financial transfer of risk Augments the indemnity or hold harmless clause

32

Ensures that funds are available in the event of a loss that was within the scope of the agreement

33

Certificate of Insurance To ensure that insurance conditions have been met, proof is required by means of a certificate of insurance

34

A COI is a document that indicates that a person, company or organization carries specific types and amounts of insurance. However, it is a ‘snapshot’ of insurance coverage's and policy terms at a specific moment in time

35

Always insist on a COI for every contract-even if you always do work with the contractor. It is possible the contractor’s limits may have changed, or a policy has been cancelled.

36

You must receive the COI BEFORE the work begins Require the COE at least 10 business days before work commences so you have time to review the COI.

37

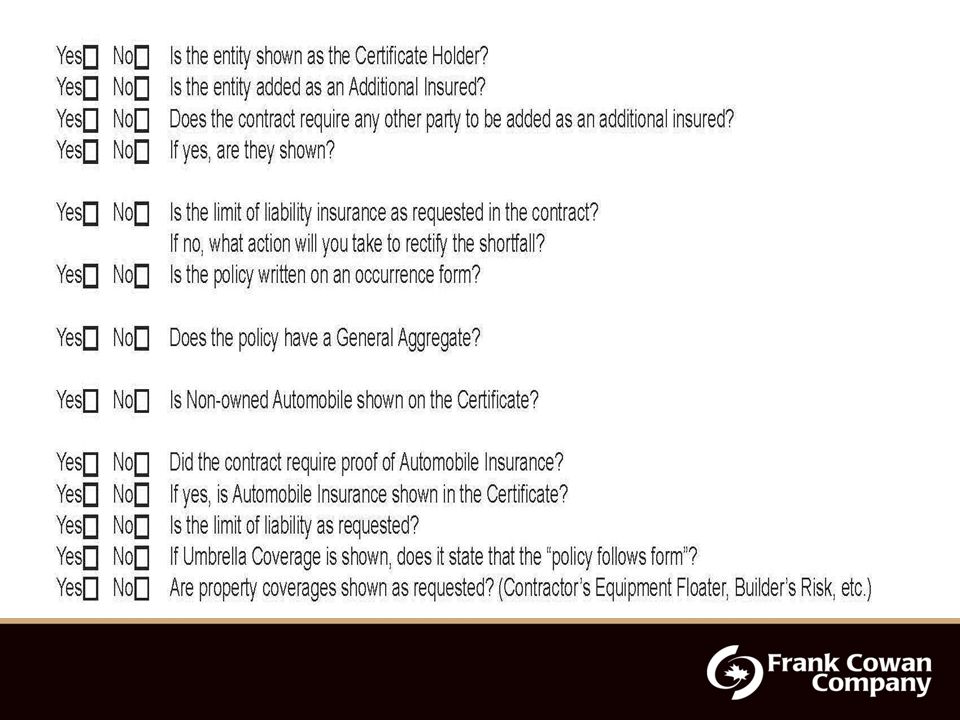

Reviewing a COI 37

39

39

40

When to Seek Help Involve legal counsel, the risk manager or the insurer when the COI is different from the requirements set out in the contract

41

The named insured is not the contracting party The policy has expired The insurance coverage is incorrect

42

The required endorsements are not listed The insurance amount (limit) is not correct

is not correct")

43

The insurer is not licensed to do business in the province You are not shown as the additional insured Notice of cancellation of coverage is not indicated

44

Abeyance System A COI will reflect the policy term of the insurance policy If the project or work will take longer than the contractor’s insurance term, then a new COE must be obtained Retention – Keep them forever

45

Retention Keep them forever

46

When Reading a Contract Read the Whole contract Think of “what if” scenarios & how the contract would respond Focus on insurance & indemnity clauses, any releases and damages

47

Look for the overall intent Who is in the position of power? Who is holding most of the risk?

48

More Specifically, Determine….. Who is being held harmless? What is the level of insurance underlying the agreement?

49

Will you be notified if the insurance is reduced or cancelled? Are you an additional insured? Is the transfer of risk reasonable?

50

Before You Sign What are you agreeing to? Are the contract conditions reasonable & achievable? Are you assuming any unnecessary or unreasonable liability?

51

Check with your insurance company to ensure that you have the proper coverage's requested in the contract.

53

Megan Martisius, CIP, CRM Risk Analyst Megan.martisius@frankcowan.com excellence.frankcowan.com frankcowan.com

Similar presentations

/principal. A GIA is a standard, typical document in the construction.>")

615-5325 Know Your Indemnity Obligation Know Your Risk Know Your Insurance Company by KEVIN R. CARLIN, ESQ.>")