Download presentation

1

IAS 16 : Tangible Assets The Institute of Chartered Accountants of India (Set up by an Act of Parliament)

")

2

Scope, Objective and Definition

IAS 16 Tangible items which (for Intangibles – refer to IAS 38 ) are held for use in the production or supply of goods or services, for rental to others, or for administrative purposes; and are expected to be used during more than one period. Property, Plant and Equipment Other related accounting standards Investment Property (IAS 40) Borrowing Costs (IAS 23) Leases (IAS 17) Intangible Assets (IAS 38) Impairment (IAS 36)

are held for use in the production or supply of goods or services, for rental to others, or for administrative purposes; and. are expected to be used during more than one period. Property, Plant and Equipment. Other related accounting standards. Investment Property (IAS 40) Borrowing Costs (IAS 23) Leases (IAS 17) Intangible Assets (IAS 38) Impairment (IAS 36)")

3

Key Features Combination of AS 6 & AS 10

Cost of decommissioning liability to be included Component Accounting Revaluation to be recognized on regular basis Accounting for land and building seperately

4

Definition and Scope Scope

The standard applies to accounting for all property, plant and equipment (PPE) except when another standard requires or permits a different accounting treatment Exclusions PPE classified as held for sale (IFRS 5) Biological assets related to agricultural activity (IAS 41) EXCEPT: PPE used to develop or maintain these assets Mineral rights and mineral reserves such oil, natural gas and similar non-regenerative resources Recognition and measurement of exploration and evaluation assets (IFRS 6) 4

except when. another standard requires or permits a different accounting treatment. Exclusions. PPE classified as held for sale (IFRS 5) Biological assets related to agricultural activity (IAS 41) EXCEPT: PPE used to develop or maintain these assets. Mineral rights and mineral reserves such oil, natural gas and similar non-regenerative resources. Recognition and measurement of exploration and evaluation assets (IFRS 6) 4.")

5

Recognition PPE is recognised as an asset when

Future economic benefits are probable, and Cost can be measured reliably PPE is measured initially at cost Criteria apply to all costs when incurred, including Initial acquisition or construction costs and subsequent costs (covered later) 5

5.")

6

Cost of Acquired or Self-Constructed Assets

INCLUDES EXCLUDES Purchase price (including import duties and non-refundable purchase taxes) Less any discounts or rebates deducted implicit interest in deferred payment Plus borrowing costs in the case of “qualifying assets” (refer IAS 23) any other directly attributable costs (e.g. employee benefits, site preparation, initial delivery and handling costs etc.) initial estimate of costs of dismantling & removing the item & restoring the site on which it is located Costs related to Abnormal amounts of wasted material, labour and other resources Opening a new facility introducing a new product or service (including costs of advertising and promotional activities) Conducting business in a new location or with a new class of customer (including costs of staff training) Administration & other general overhead costs Using or redeploying an item Certain incidental operations Period when construction is interrupted, unless certain criteria are met 6

Less. any discounts or rebates deducted. implicit interest in deferred payment. Plus. borrowing costs in the case of qualifying assets (refer IAS 23) any other directly attributable costs (e.g. employee benefits, site preparation, initial delivery and handling costs etc.) initial estimate of costs of dismantling & removing the item & restoring the site on which it is located. Costs related to. Abnormal amounts of wasted material, labour and other resources. Opening a new facility. introducing a new product or service (including costs of advertising and promotional activities) Conducting business in a new location or with a new class of customer (including costs of staff training) Administration & other general overhead costs. Using or redeploying an item. Certain incidental operations. Period when construction is interrupted, unless certain criteria are met. 6.")

7

Cost of PPE acquired in exchange of Another Asset

Cost of exchanged asset is measured at fair value unless Exchange transaction lacks commercial substance, or Fair value of neither asset received nor given up can be measured reliably Fair value of asset given up is used, unless fair value of asset received is more clearly evident Cost of PPE acquired in exchange of another Asset OR If not measured at fair value, carrying amount of the asset given up becomes the new cost

8

Subsequent Costs Subsequent costs are capitalised only if they meet general recognition criteria Future economic benefits are probable Cost can be measured reliably Costs of day-to-day servicing are expensed as incurred Recognise cost of replacing part of PPE item when incurred Recognise major inspection cost in the carrying amount as replacement if recognition criteria is met Any remaining carrying amount of cost of previous inspection is derecognised Derecognise replaced parts (physical or otherwise) in accordance with de-recognition provisions of the standard 8

in accordance with de-recognition provisions of the standard. 8.")

9

Measurement after Recognition

Cost model – Depreciate cost over useful life Revaluation Model – Depreciate revalued amount over useful life 9

10

Revaluation Model Revaluation model can be adopted for assets whose fair value can be measured reliably Asset to be carried at fair value on date of revaluation Revaluation should be done regularly If an item of PPE is revalued – revalue entire class to which the asset belongs To adjust accumulated depreciation at the date of the revaluation either: Restate it proportionately with the change in the gross carrying amount of the asset so that carrying amount after revaluation equals revalued amount, or Eliminate it against the gross carrying amount of the asset and restate the net amount to the revalued amount of the asset 10

11

An Item of PPE with original value at 120 and accumulated depreciation of 20 with net block at 100 is revalued to 150 Particulars Original Value Revalued Gross Block 120 180 150 Less Accumulated Depreciation 20 30 Net Block 100

12

Revaluation Model Revaluation increases credited to

Profit or loss to the extent they reverse previous revaluation decrease of that asset recognised in profit or loss Otherwise, OCI and accumulated in equity as revaluation surplus Revaluation decreases debited to OCI to the extent of credit balance in revaluation surplus related to that asset Otherwise, profit or loss The revaluation surplus may be transferred to retained earnings when the asset is derecognised or as it is used by the entity

13

Depreciation Each part of a PPE whose cost is significant in relation to the total cost of the PPE is to be depreciated separately Depreciable amount determined after deducting residual value Depreciable amount to be allocated on a systematic basis over the useful life Depreciation method should reflect the pattern in which the asset’s future economic benefits are expected to be consumed by the entity 13

14

Depreciation Depreciation is recognised even if the fair value of the asset exceeds its carrying amount, as long as the asset’s residual value does not exceed its carrying amount Review at least at each financial year end: Residual value Useful life Depreciation method Changes in above are changes in estimate and should be accounted for as per IAS 8 in current and future periods only 14

15

Component Accounting Initial recognition

Allocate cost to significant parts of asset, including non-physical parts Depreciation for each ‘component’ to be charged separately Example: Aircraft costs 200, useful life 10 years Estimated cost of a significant component - 50, to be replaced after 3 years COMPONENT 1 COST: 150 LIFE: 10 YEARS TOTAL AIRCRAFT COST = 200 COMPONENT 2 COST: 50 LIFE: 3 YEARS CAPITALISE AS INCURRED 15

16

IFRIC 1 Changes in existing Decommissioning, Restoration and Similar Liabilities

Changes due to a change in estimated timing and amount of payments discount rate are added to/deducted from cost of underlying asset and depreciated prospectively over remaining useful life Foreign exchange gains and losses may be recognised in profit or loss or adjusted against cost of PPE 16

17

IFRIC 1 Changes in existing Decommissioning, Restoration and Similar Liabilities

Applies regardless of accounting policy (cost or revaluation model) but implementation varies Cost model Changes in liability added/deducted from asset cost in current period No negative carrying amount possible; any excess recognised immediately in profit or loss Increase in carrying amount triggers consideration of impairment, including, if necessary, calculation of recoverable amount 17

but implementation varies. Cost model. Changes in liability added/deducted from asset cost in current period. No negative carrying amount possible; any excess recognised immediately in profit or loss. Increase in carrying amount triggers consideration of impairment, including, if necessary, calculation of recoverable amount. 17.")

18

IFRIC 1 Changes in existing Decommissioning, Restoration

and Similar Liabilities Revaluation model Change in liability does not affect valuation of asset (impact on valuation reserve) Decrease in liability is recognised in revaluation surplus except for: reversal of revaluation deficit recognised previously in P/L if results in negative depreciated cost Increase in liability is recognised in profit/ loss except when there is credit balance remaining in revaluation surplus A change in liability indicates that asset might have to be revalued in order to ensure that the carrying amount does not differ materially from that which would be determined using fair value at the end of the reporting period 18

Decrease in liability is recognised in revaluation surplus except for: reversal of revaluation deficit recognised previously in P/L. if results in negative depreciated cost. Increase in liability is recognised in profit/ loss except when there is credit balance remaining in revaluation surplus. A change in liability indicates that asset might have to be revalued in order to ensure that the carrying amount does not differ materially from that which would be determined using fair value at the end of the reporting period. 18.")

19

De-recognition Derecognise carrying amount of an item of PPE

on disposal, or when no future benefits expected from use or disposal Date of disposal to be determined on the basis of IAS 18 Difference between carrying amount and net disposal proceeds is recognised as gain/loss in profit and loss account Gains (or proceeds) are not classified as revenue 19

are not classified as revenue. 19.")

20

De-recognition Exception: when an entity routinely sells items of PPE that it has held for rental, it transfers them to inventory at the carrying amount when they cease to be rented. The proceeds from sale are treated as revenue Consideration receivable on disposal of PPE to be measured at fair value If payment for an item of PPE is deferred – consideration is recognised initially at the cash price equivalent Difference between nominal amount of consideration and cash price equivalent recognised as interest revenue as per IAS 18 reflecting the effective yield on the receivable 20

21

Compensation for Impairment, Loss or Surrender

Compensation from third parties for items of PPE that were impaired, lost or given up shall be included in the profit or loss when the compensation becomes receivable Impairments – in accordance with IAS 36 De-recognition – in accordance with IAS 16 Compensation from third parties – include in profits or loss when it becomes receivable (in accordance with IAS 16) Cost of PPE restored, purchased or constructed as replacements is determined in accordance with IAS 16 21

Cost of PPE restored, purchased or constructed as replacements is determined in accordance with IAS")

22

Disclosures Measurement basis

Depreciation methods, useful lives or depreciation rates used Gross carrying amount and accumulated depreciation at the beginning and end of the period Reconciliation of the carrying amount at the beginning and end of the period showing additions, assets classified as held for sale, acquisitions through business combination, increase or decrease from revaluation, impairment loss etc. Existence and amount of restrictions on title to PPE; PPE pledged as security for liabilities Amount of expenditure recognised in the carrying amount of PPE during construction Commitments for acquisition of PPE 22

23

Disclosures Compensation from third parties for PPE that were impaired, lost or given up Specific disclosures have also been prescribed for revalued assets such as: Effective date of revaluation Whether an independent valuer was involved, methods and significant assumptions applied in estimating fair values Extent to which fair values were determined based on observable prices in an active market or recent market transactions on arm or other valuation techniques Carrying amount of each class of revalued PPE as if under the cost model Revaluation surplus, including change for the period and any restrictions on distribution of balance to shareholders 23

24

Borrowing Costs Scope Apply in accounting for borrowing costs

An entity need not apply the standard to borrowing costs related to acquisition, construction or production of: a qualifying asset measured at fair value; or inventories that are manufactured, or otherwise produced, in large quantities on a repetitive basis Borrowing Costs Borrowing costs are interest and other costs incurred by an entity in connection with the borrowing of funds and includes: Interest expense calculated using the effective interest rate method as described in IAS 39; finance charges in respect of finance leases (as in IAS 17); and exchange differences to the extent that they are regarded as an adjustment to interest costs Does not include actual or imputed cost of equity

; and. exchange differences to the extent that they are regarded as an adjustment to interest costs. Does not include actual or imputed cost of equity.")

25

Qualifying Assets and Costs eligible for capitalisation

An asset that necessarily takes a substantial period of time to get ready for its intended use or sale Depending on the circumstances, any of the following may be qualifying assets: Inventories, manufacturing plants, power generation facilities, intangible assets, investment properties

26

Qualifying Assets and Costs eligible for capitalisation

Borrowing costs eligible for capitalisation are those directly attributable to acquisition, construction or production of a qualifying asset which would have been avoided otherwise Specific borrowings Actual borrowing costs less any investment income on the temporary investment of borrowed funds General borrowings Use weighted average borrowing rate as capitalisation rate and the expenditure on the asset to calculate eligible amount

27

Period of Capitalisation

Expenditure begins Borrowing costs incurred Activities in progress Activities suspended Activities suspended, but substantial technical or admin work Asset is ready for intended use Funds borrowed Start to use % to deduct Start Start Continue Suspend Stop

28

Commencement, Suspension and Cessation of Capitalisation

Commencement of Capitalisation Suspension of Capitalisation Commence capitalisation when entity: incurs expenditures for the asset AND incurs borrowing costs, AND undertakes activities necessary to prepare asset for intended use or sale Suspend capitalisation during extended periods in which active development is suspended Do not suspend in case of : temporary delay that is caused by external event interruption caused by technical or legal obstructions that are a typical part of process activities suspended, but substantial technical or admin work to be carried out Cessation of Capitalisation Cease capitalisation when substantially all activities necessary to prepare the qualifying asset for intended use or sale are complete

29

Disclosures Amount of borrowing costs capitalised during period

Capitalisation rate used to determine the amount of borrowing costs eligible for capitalisation

30

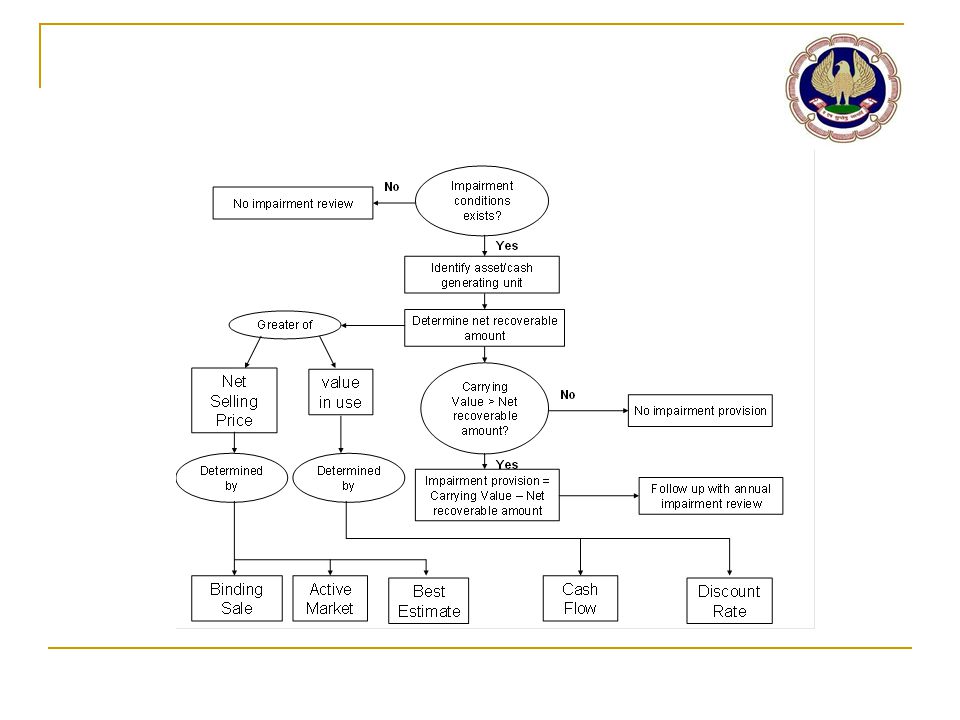

Impairment – Assessment and Loss Recognition

Assess at each balance sheet date indicators of impairment If indication exists, measure and recognise impairment in accordance with IAS 36, Impairment of Assets Compare carrying amount with the recoverable amount Recoverable amount is higher of fair value (less costs to sell) and value in use Recognise impairment loss as expense immediately Unless carried at revalued amount (treat as revaluation) Depreciation in future to be calculated on the basis of the new carrying amount 30

and value in use. Recognise impairment loss as expense immediately. Unless carried at revalued amount (treat as revaluation) Depreciation in future to be calculated on the basis of the new carrying amount. 30.")

![PROPERTY, PLANT & EQUIPMENT [IAS 16]](/5/1478062/big_thumb.jpg "PROPERTY, PLANT & EQUIPMENT [IAS 16]>")

>")

Accounting for Government Grants. Scope This Statement does not deal with: (i) the special problems arising in accounting for government grants.>")

>")

The prior period's closing balances have been correctly brought forward to the current period or, when appropriate, have been restated; and ◦ (b)>")