Download presentation

Presentation is loading. Please wait.

1

Chapter 6: Production and Costs

economic costs & profits short run long run

2

big picture understand behavior of firm understand & measure

production costs

3

I. economic costs & profits

firm’s goal: maximize profit look at factors that affect firm’s decision

4

economic costs opportunity cost of resources used explicit costs

paid in money wages, rent, material, etc. implicit costs

5

example: smoothie shop

explicit costs: wages interest on loan rent on store fruit, blenders

6

implicit costs forgone interest on funds used to buy capital owner’s forgone wages owner’s forgone profit from other venture

7

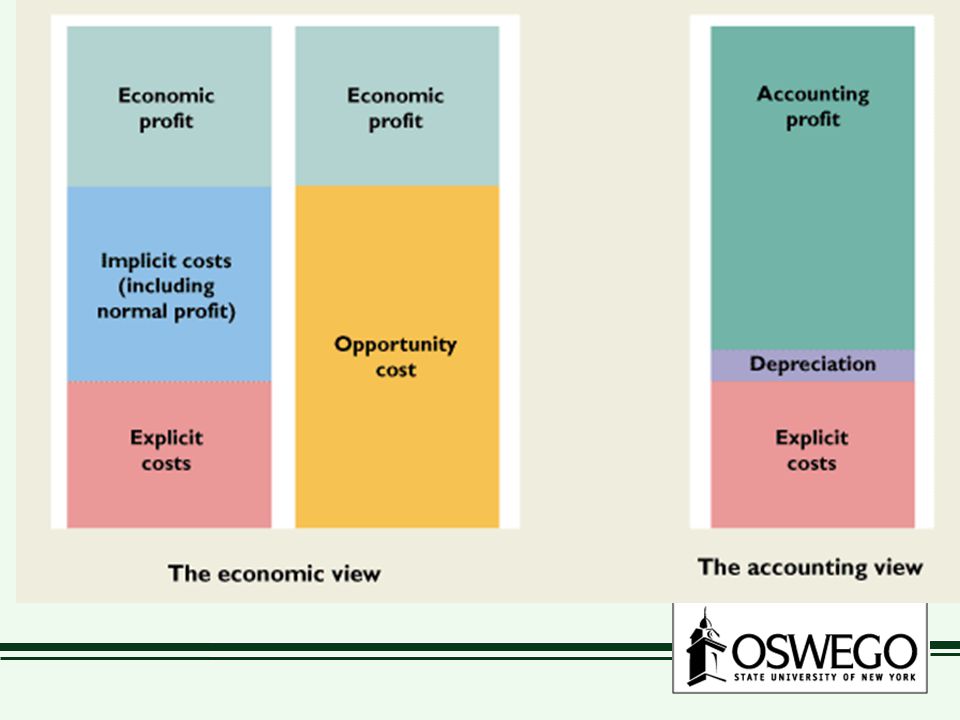

accounting profit total revenue – explicit costs

ignores opportunity cost

8

economic profit includes opp. costs = total revenue - total costs

= (price)(quantity) - (explicit + implicit costs)

(quantity) - (explicit + implicit costs)")

9

normal profit occurs when amount of accounting profit

= opportunity costs of resources if earning a normal profit, economic profit = 0

11

Short Run vs. Long Run Short Run (SR)

time frame where some resources are fixed -- plants, equipment some inputs variable -- labor SR decisions are reversible

12

Long Run (LR) time frame where all inputs are variable --build a bigger plant LR decisions are hard to reverse -- cannot easily get rid of capital -- sunk cost

13

II. SR Production measures of output total product marginal product

average product

14

total product (TP) total quantity of good produced in a given period

at first, increases with labor, then falls

15

TP: gal. of smoothies per hour

# workers TP 1 2 3 4 5 6 7 1 3 6 8 9

16

TP 5 6 9 # workers

17

marginal product (MP) change in TP due to one more worker change in TP

= change in labor

18

At first MP rises with workers

add more workers greater specialization MP of each worker added is larger than previous worker increasing marginal returns

19

then, MP falls with more workers

keep adding workers but same amount of capital so eventually get in the way MP of more workers smaller than MP of previous workers decreasing marginal returns

20

TP, MP: gal. of smoothies 1 2 3 4 5 6 7 1 3 6 8 9 # workers TP MP 1 2

1 2 3 4 5 6 7 1 3 6 8 9 1 2 3 2 1 -1

21

MP 3 Q = # workers

22

law of decreasing returns

As firm uses more labor with capital fixed, MP of labor will eventually fall

23

Average Product (AP) TP = labor = productivity

TP = labor = productivity")

24

AP # workers TP MP 1 2 3 4 5 6 7 1 3 6 8 9 1 2 3 -1 1 1.5 2 1.8 1.1

25

MP 3 AP # workers

26

MP & AP MP intersects AP at max of AP why? MP > AP AP is rising

AP is falling

27

III. SR cost measure cost 3 ways: total cost marginal cost

average cost

28

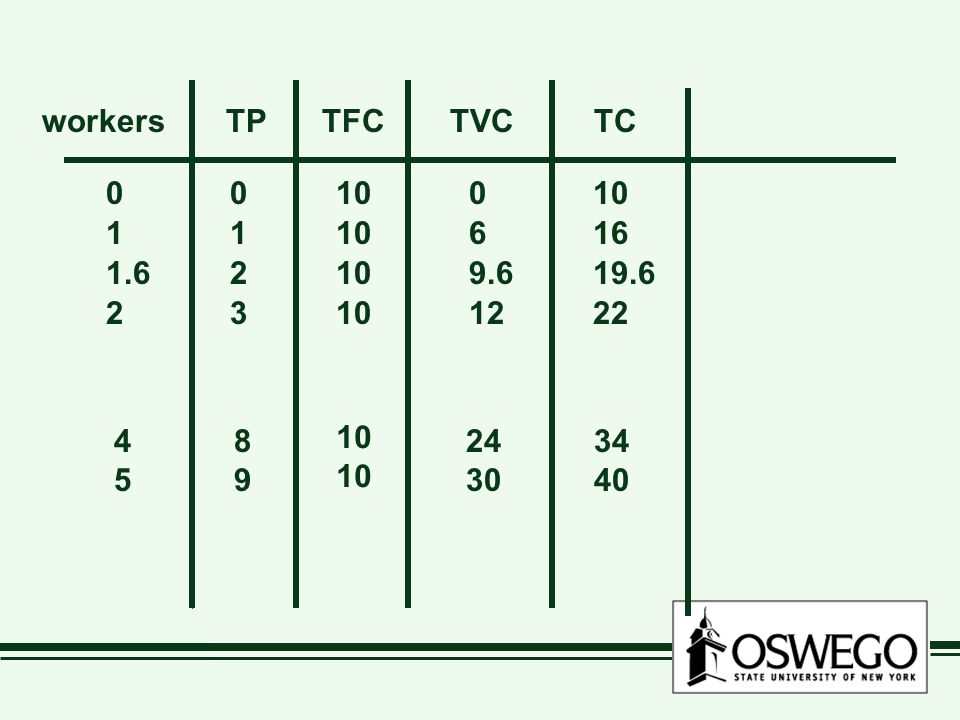

Total Cost (TC) cost of all factors used total fixed cost (TFC)

cost of land, capital, etc. does not change in SR total variable cost (TVC) cost of labor changes in SR TC = TFC + TVC

cost of labor. changes in SR. TC = TFC + TVC.")

29

example : yogurt labor = $6/ hour TFC = $10/ hour

30

workers TP TFC TVC TC 4 5 8 9 10 24 30 34 40

31

Q = output TC TC TVC TFC 10

32

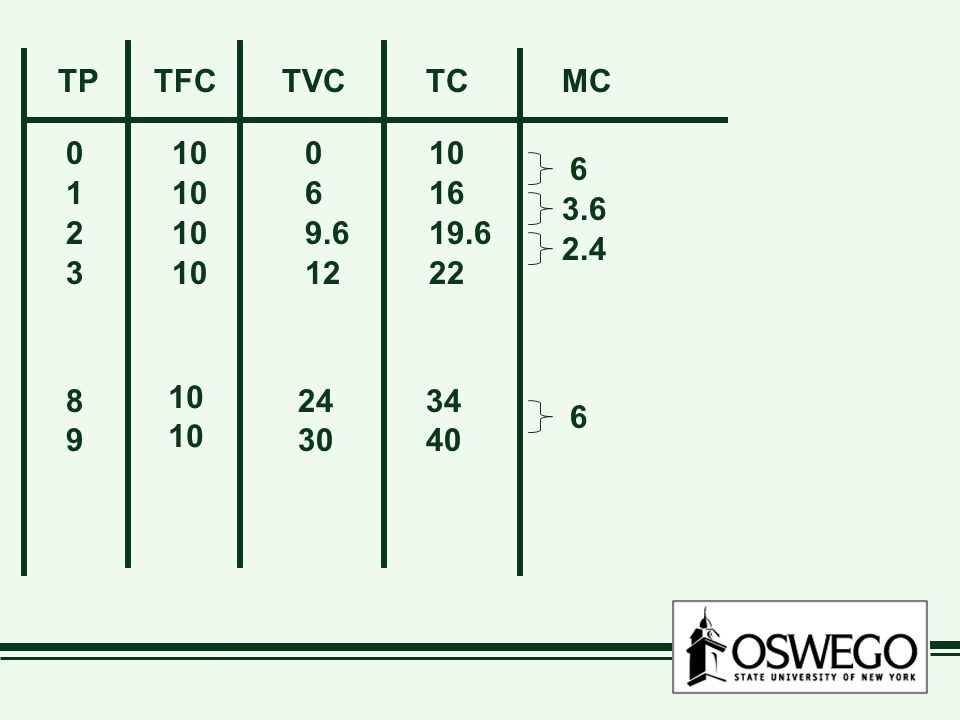

Marginal Cost change in TC due to one-unit increase in output (Q)

= change in Q

33

TP TFC TVC TC MC 6 3.6 2.4 8 9 10 24 30 34 40 6

34

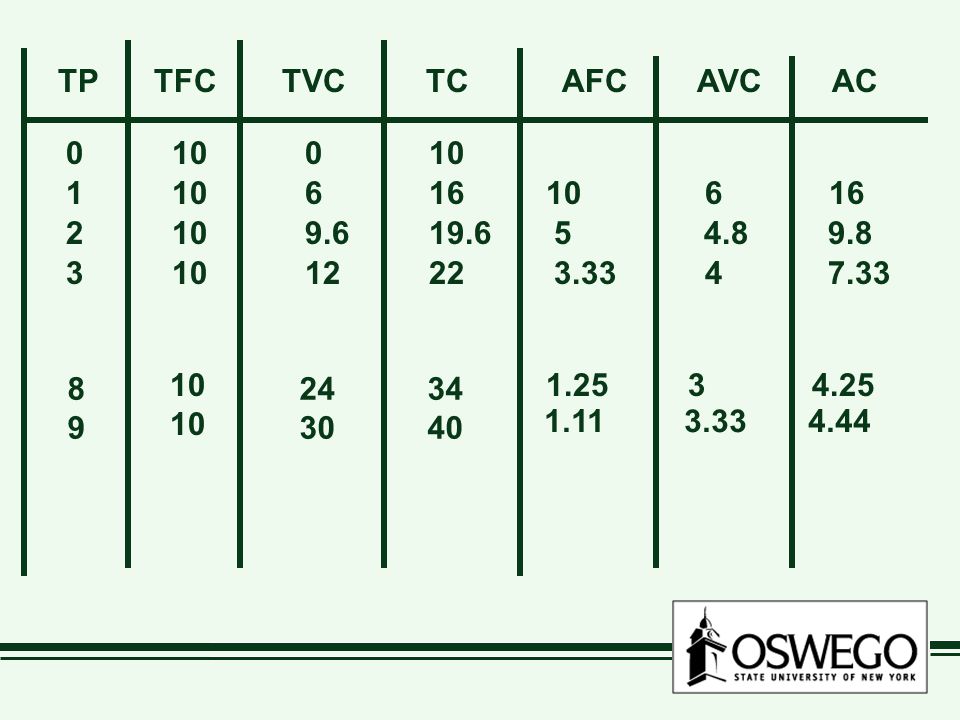

Average Cost (ATC) = TC/Q average fixed cost (AFC) (TFC/Q)

average variable cost (AVC) (TVC/Q) ATC = AFC + AVC

(TVC/Q) ATC = AFC + AVC.")

35

TP TFC TVC TC AFC AVC AC 8 9 10 24 30 34 40

36

Q = output AC, MC AFC ATC AVC MC

37

MC & AC MC intersects AC at its minimum MC < AC AC is falling

AC is rising

38

AC is U-shaped why? AFC falls with Q AVC falls then rises

decreasing marginal returns so ATC falls, then rises

39

cost & product curves when MP is at maximum, MC is at minimum

when AP is at maximum, AVC is at minimum

40

what shifts cost curves?

technology make more with same inputs shifts TP, MP, AP up changes ATC curve

41

changes in factor prices

increase fixed costs -- TFC, AFC shift up -- TC shift up increase wages (variable) -- TVC, AVC, MC shift up

-- TVC, AVC, MC shift up.")

42

IV. LR costs all inputs (and costs) are variable

what happens if increase plant AND labor by 10%? ATC fall? ATC rise? ATC stay same?

43

Economies of scale increase inputs 10% output increase > 10%

ATC falls why? gains from specialization -- labor -- capital

44

Diseconomies of scale increase inputs 10% output increase < 10%

ATC rises why? too hard to control large firm

45

Constant returns to scale

increase inputs 10% output increase = 10% ATC stays same

46

LR Average Cost (LRAC) lowest average cost when all inputs are variable SRAC curves from different plant sizes

47

Q = output AC ATC1 ATC2 ATC3 ATC4 LRAC

48

Q = output AC ATC1 ATC2 ATC3 ATC4 diseconomies of scale economies of scale constant returns to scale

49

summary: costs = implicit + explicit SR, only labor variable

LR, all inputs variable Production & costs total, marginal, average fixed, variable

Similar presentations