Download presentation

Presentation is loading. Please wait.

1

Review and Compliance of Exempt and Excluded Property Kimberly Simpson – Durham County Tax Administrator Heather Scheel – North Carolina Department of Revenue

2

Next 50 Minutes Review/ Annual Review and 1/8 Verification of NC Exemptions (105-278), Exclusions and Deferments (105-275, 276 & 277) – NOT PUV (Present Use Value) – Somewhat (Audit/Compliance) » EDV/CB (Elderly, Disabled Vet or Circuit Breaker)

, Exclusions and Deferments ( , 276 & 277) – NOT PUV (Present Use Value) – Somewhat (Audit/Compliance) » EDV/CB (Elderly, Disabled Vet or Circuit Breaker)")

3

Agenda – Legal Framework General Processes – Case Study – Durham County Audit & Review Process – 2011 Legislation – Best Practices/Lessons Learned

4

Legal Framework NC Law – Machinery Act Taxpayer Responsibility – Privilege – Application Assessor’s Duty – Approve & Appeal – Review & Audit – Discover & Report

5

Legal Framework 105-274 – Property Subject to Taxation - All property…shall be subject to taxation unless it is: – (1) Excluded…under the classification power accorded the General Assembly by Article V, § 2(2), of the North Carolina Constitution, or – (2) Exempted by a statute of statewide application enacted under the authority granted the General Assembly by Article V, § 2(3), of the North Carolina Constitution.

Excluded…under the classification power accorded the General Assembly by Article V, § 2(2), of the North Carolina Constitution, or – (2) Exempted by a statute of statewide application enacted under the authority granted the General Assembly by Article V, § 2(3), of the North Carolina Constitution.")

6

Legal Framework Taxpayer Responsibility – 105-282.1 - Every owner of property claiming exemption or exclusion from property taxes under the provisions of this Subchapter has the burden of establishing that the property is entitled to it. – 105-282.1(a) – annually during listing period

– annually during listing period.")

7

Legal Framework Taxpayer Responsibility – 105-282.1 - Every owner of property claiming exemption or exclusion from property taxes under the provisions of this Subchapter has the burden of establishing that the property is entitled to it. Privilege not a right Must at least identify exemption or exclusion sought on application If multi-part test – all must be met (ownership & use) or Historic Properties § 105-278 need ordinance under § 160A-400.5.

or Historic Properties § need ordinance under § 160A")

8

Legal Framework Taxpayer Responsibility – 105-282.1(a) – annually during listing period – Except….

– annually during listing period – Except….")

9

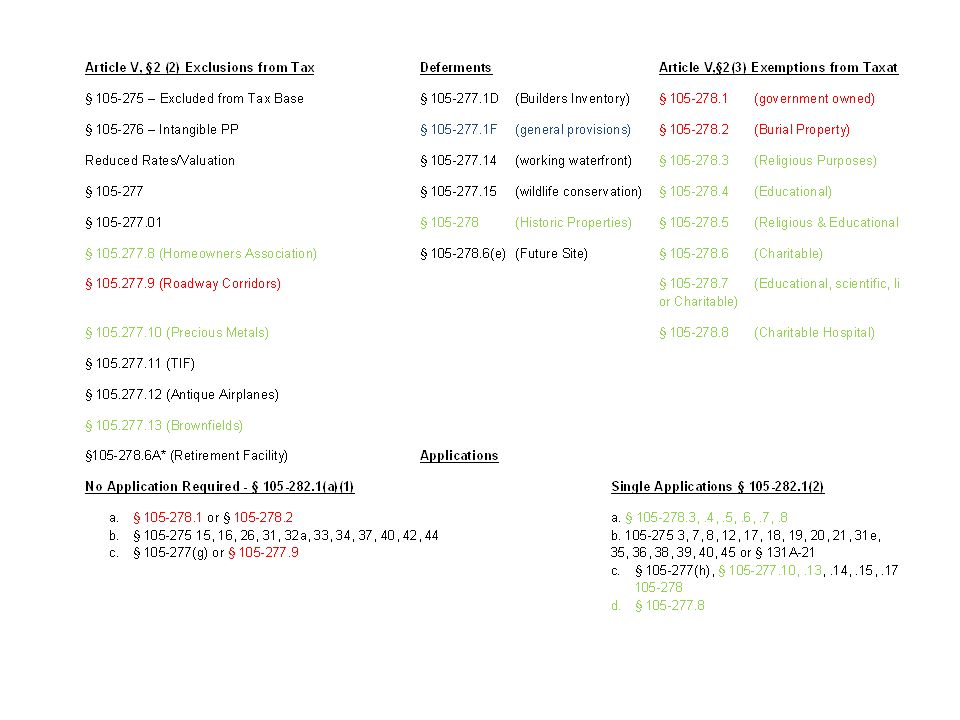

Legal Framework §105-282.1(a)1 No application required. – Owners of the following exempt or excluded property do not need to file an application for the exemption or exclusion to be entitled to receive it: – a. Property exempt from taxation under G.S. 105 ‑ 278.1 or G.S. 105 ‑ 278.2. – b. Special classes of property excluded from taxation under G.S. 105 ‑ 275(15), (16), (26), (31), (32a), (33), (34), (37), (40), (42), or (44). – c. Property classified for taxation at a reduced valuation under G.S. 105 ‑ 277(g) or G.S. 105 ‑ 277.9.

, (16), (26), (31), (32a), (33), (34), (37), (40), (42), or (44). – c. Property classified for taxation at a reduced valuation under G.S. 105 ‑ 277(g) or G.S. 105 ‑")

10

Legal Framework Single Application Required – § 105-282.1(2) Certain Exempted property Special Classes G.S. § 277.8 (non-profit homeowner’s association) – See Quick Charts (next two slides)

– See Quick Charts (next two slides).")

13

§ 105-275 - Exclusions See Attachments Quick Look – attached exhibit Actual Language – attached exhibit

14

Legal Framework Assessor Duties – Approve & Appeal - § 105-282.1(b) Upon Receipt of (initial) Timely Filed Application – Approve or Deny – Approve (Use of Property) – if approved all relevant taxing units should be notified » Articles of Incorporation, I/E statements, certification from other agencies, local resolution… – Deny – Owner must be notified and provided appeal rights to County Board of Equalization and Review » If Board Denies – Notification and Appeal Rights to NC PTC

Upon Receipt of (initial) Timely Filed Application – Approve or Deny – Approve (Use of Property) – if approved all relevant taxing units should be notified » Articles of Incorporation, I/E statements, certification from other agencies, local resolution… – Deny – Owner must be notified and provided appeal rights to County Board of Equalization and Review » If Board Denies – Notification and Appeal Rights to NC PTC")

15

Legal Framework – Approve & Appeal - § 105-282.1(b) Upon Receipt of Late Filed (initial) Application – Approve or Deny – May be granted upon showing of good cause » Important to remain logical, consistent & fair

Upon Receipt of Late Filed (initial) Application – Approve or Deny – May be granted upon showing of good cause » Important to remain logical, consistent & fair")

16

Legal Framework Assessors Duties – Review & Audit - § 105-282.1(e) Assessor must review and Verify at least 1/8 of parcels in county exempted or excluded from taxation pursuant to §105-296(l) – Assessor may deny – taxpayer may appeal BOE – Assessor may require property owner to make available for inspection information » Taxpayer 60 days to submit information or risk status

Assessor must review and Verify at least 1/8 of parcels in county exempted or excluded from taxation pursuant to § (l) – Assessor may deny – taxpayer may appeal BOE – Assessor may require property owner to make available for inspection information » Taxpayer 60 days to submit information or risk status")

17

Legal Framework Assessors Duties – Discover & Report Discover - § 105-282.1(c) – Owner that may be eligible but neither lists nor files application is subject to Discovery, however owner can establish status through appeal and approval Create Property Roster - § 105-282.1(d) – Assessor prepares and maintains list and reports to DOR » Name » Description of property » Use » Value » Muni breakdown

– Owner that may be eligible but neither lists nor files application is subject to Discovery, however owner can establish status through appeal and approval Create Property Roster - § (d) – Assessor prepares and maintains list and reports to DOR » Name » Description of property » Use » Value » Muni breakdown")

18

Timing Jan – Listing Period - new apps; annual review – run audit reports Feb – Annual review requests (30 days) March – Review; send decision letters (appeal rights); 2 nd 30 day request April – BOE hearings May – Continued review in necessary June - Continued review if necessary July - Continued review if necessary August - Continued review if necessary Sept - Continued review if necessary Oct – All decisions should be out start DOR report Nov – Submit report to DOR Dec – Scrubbing Data; prepping to run Jan audit reports in

March – Review; send decision letters (appeal rights); 2 nd 30 day request April – BOE hearings May – Continued review in necessary June - Continued review if necessary July - Continued review if necessary August - Continued review if necessary Sept - Continued review if necessary Oct – All decisions should be out start DOR report Nov – Submit report to DOR Dec – Scrubbing Data; prepping to run Jan audit reports in")

19

Case Study – Durham County Compliance Review for Property Tax Programs in Durham Assessor’s Duty – Approve & Appeal – Review & Audit – Discover & Report

20

Case Study – Durham County Compliance Review for Property Tax Programs in Durham Assessor’s Duty – Approve & Appeal Initial Review

21

Case Study – Durham County Compliance Review for Property Tax Programs in Durham Assessor’s Duty – Review & Audit Computer Generated Plan – Audit Reports – Feed AV 50 » Last date audited & when is next one scheduled Year 2001 – churches, educational, charitable, religious, elderly, disabled, and veterans. Year 2006 – churches, educational, charitable, religious and other properties. Year 2008 – elderly, disabled and veterans. Year 2012 we will begin to deal with any exemptions scheduled as apart of year to be audited which will include churches, educational, religious, elderly, and others.

22

Query of system data identifies all parcels of this type scheduled for re-qualification in 2012.

24

Case Study – Durham County Compliance Review for Property Tax Programs in Durham Assessor’s Duty – Review & Audit – Cover Letters & Questionnaires – What to do with non-compliance – Outside Sources and Relationships to Assist with Reviews

25

Case Study – Durham County Compliance Review for Property Tax Programs in Durham Assessor’s Duty – Review & Audit – Cover Letters & Questionnaires

26

Case Study – Durham County Compliance Review for Property Tax Programs in Durham Assessor’s Duty – Review & Audit – What to do with non-compliance » Churches

27

Case Study – Durham County Compliance Review for Property Tax Programs in Durham Assessor’s Duty – Review & Audit – Outside Sources and Relationships to Assist with Reviews » IRS - www.irs.gov/charities/article/0,,id=240099,00.htmlwww.irs.gov/charities/article/0,,id=240099,00.html » Secretary of State – www.secstate.state.nc.uswww.secstate.state.nc.us » Physically Inspect » Chamber of Commerce » Zoning & Planning » Cities » Social Services

28

Case Study – Durham County Compliance Review for Property Tax Programs in Durham Assessor’s Duty – Discover & Report » AV50

29

2011 Legislation G.S. 105-275. — Property classified and excluded from the tax base: Exempts any real and personal property that meets each of the following requirements: a. It is a contiguous tract of land previously (i) used primarily for commercial or industrial purposes and (ii) damaged significantly as a result of a fire or explosion. b. It was donated to a nonprofit corporation formed under the provisions of Chapter 55A of the General Statutes by an entity other than an affiliate, as defined in G.S. 105-163.010. c. No portion is or has been leased or sold by the nonprofit corporation. G.S 105-275(12) — Property classified and excluded from the tax base: Modifies when land used for conservation purposes is to be excluded from property taxes. Amends 105-275(12) by providing that real property that (i) is owned by a nonprofit corporation or association organized to receive and administer lands for conservation purposes, (ii) is exclusively held and used for one or more of the purposes listed in this subdivision, and (iii) produces no income or produces income that is incidental to and not inconsistent with the purpose or purposes for which the land is held and used and if a disqualifying event occurs, provides for the collection of five years of deferred taxes under G.S. 105-277.1F(a).

used primarily for commercial or industrial purposes and (ii) damaged significantly as a result of a fire or explosion. b. It was donated to a nonprofit corporation formed under the provisions of Chapter 55A of the General Statutes by an entity other than an affiliate, as defined in G.S c. No portion is or has been leased or sold by the nonprofit corporation. G.S (12) — Property classified and excluded from the tax base: Modifies when land used for conservation purposes is to be excluded from property taxes. Amends (12) by providing that real property that (i) is owned by a nonprofit corporation or association organized to receive and administer lands for conservation purposes, (ii) is exclusively held and used for one or more of the purposes listed in this subdivision, and (iii) produces no income or produces income that is incidental to and not inconsistent with the purpose or purposes for which the land is held and used and if a disqualifying event occurs, provides for the collection of five years of deferred taxes under G.S F(a)..")

30

2011 Legislation G.S. 105-278.6. — Real and personal property used for charitable purposes: Extends the time period for holding real property as a future site for housing for low or moderate income individuals and families from five years to 10 years. The deferred taxes would be due after 10 years if the property was not used for the intended purpose. This change goes into effect for the 2011 tax year so any property which would have lost its exclusion due to the 5 year time limit now has 5 more years to put the property into use. (Effective July 1, 2011; HB 417, s. 1, S.L. 2011-368) G.S. 105-277.9A. — Taxation of property inside certain roadway corridors: Reduces the property tax owed for improved property inside certain roadway corridors. Adds the following provision which taxes improved real property located within a roadway corridor at 50% of its appraised value. This law is repealed in July of tax year 2021.

G.S A. — Taxation of property inside certain roadway corridors: Reduces the property tax owed for improved property inside certain roadway corridors. Adds the following provision which taxes improved real property located within a roadway corridor at 50% of its appraised value. This law is repealed in July of tax year")

31

Best Practices/Lessons Learned Share

32

Questions End

Similar presentations

Update August 24, 2006.>")

. Is the Property currently exempt?>")