Download presentation

Presentation is loading. Please wait.

1

KBC Bank & Insurance Group Company presentation Spring 2004 Website: www.kbc.com Ticker codes: KBC BB (Bloomberg) KBKBT BR (Reuters) B:KB (Datastream) ISIN code: BE0003565737

KBKBT BR (Reuters) B:KB (Datastream) ISIN code: BE")

2

2 Table of contents 1.Company profile 2.Strategy overview 3.Financial highlights 4.Additional information

3

Company profile

4

4 Considerable scale in Euroland Note: DJ Euro Stoxx Banks constituents as of 31 Jan 2004 Giant cap Large cap Mid cap Number 12 in Euroland bank ranking KBC is a top-20 financial service provider in the Euro-zone with a market cap of ± 14 bn

5

5 Successful core businesses Top bancassurer in Belgium : 3 rd bank (market share: ± 22%) 1 st asset manager (± 31% in funds) 3 rd retail insurer (± 13% Life, ± 8% PC) Successful expansion in the 5 most advanced countries in ‘Emerging Europe’ : Growth market of ± 65 m inhabitants ± 3.4 bn capital invested Prominent position in banking Focused activities in corporate and investment banking. As investments in CEE progressed, CIB activities have been scaled down. Share in allocated capital (excl. goodwill and group items) KEY FIGURES : Total assets : ± 226 bn Net profit ‘03 : 1.12 bn ROE ’03 : 12.7 % Headcount : ± 50 000 Customers : ± 12 m Credit rating : AA-, AA3, A+

KEY FIGURES : Total assets : ± 226 bn Net profit ‘03 : 1.12 bn ROE ’03 : 12.7 % Headcount : ± Customers : ± 12 m Credit rating : AA-, AA3, A+.")

6

6 Banking Insurance Allocated capital Slovakia: Market share: 6% (no 4) Czech Republic: Market share: 18% (no 1) Total assets: 18.3 bn Profit/ROAC ‘03: 143 m / 17% Hungary: Market share: 11% (no 2) Total assets: 5.5 bn Profit/ROAC ‘03: 13 m / 8% (20%) Poland: Market share: 6% (no 7) Total assets: 4.8 bn Profit ‘03: -295 m Slovenia: Minority interest (34%) Market share: 43% (no 1) Profit ‘03: 10 m Czech Republic: Life M share: 9% (no 4) Non-life M share: 4% (no 6) Assets/Profit ‘03: 0.5 bn/-1.6 m Slovakia: Life M share: 4% (no 8) Non-life M share: 2% (no 6) Assets/Profit ‘03: 50 m/-0.3 m Hungary: Life M share: 2% (no 13) Non-life M share: 4% (no 6) Assets/Profit ‘03:79 m/0.3 m Poland: Life M share: 5% (no 5) Non-life M share: 14% (no 2) Assets/Profit ‘03: 0.8 bn/-1,9 m Slovenia: Startup life business Prominent player in CEE Note: profit contribution to KBC Group result after minorities.

Czech Republic: Market share: 18% (no 1) Total assets: 18.3 bn Profit/ROAC ‘03: 143 m / 17% Hungary: Market share: 11% (no 2) Total assets: 5.5 bn Profit/ROAC ‘03: 13 m / 8% (20%) Poland: Market share: 6% (no 7) Total assets: 4.8 bn Profit ‘03: -295 m Slovenia: Minority interest (34%) Market share: 43% (no 1) Profit ‘03: 10 m Czech Republic: Life M share: 9% (no 4) Non-life M share: 4% (no 6) Assets/Profit ‘03: 0.5 bn/-1.6 m Slovakia: Life M share: 4% (no 8) Non-life M share: 2% (no 6) Assets/Profit ‘03: 50 m/-0.3 m Hungary: Life M share: 2% (no 13) Non-life M share: 4% (no 6) Assets/Profit ‘03:79 m/0.3 m Poland: Life M share: 5% (no 5) Non-life M share: 14% (no 2) Assets/Profit ‘03: 0.8 bn/-1,9 m Slovenia: Startup life business Prominent player in CEE Note: profit contribution to KBC Group result after minorities.")

7

7 Building a 2 nd home in CEE Minority in CSOB Insurance Majority in CSOB Bank & CSOB Insurance Take-over of IPB banking Take-over of IPB Insurance & majority in ERGO Minority in K&H Bank & creation of Argosz Non- life & K&H Life Majority in K&H Bank Merger of K&H/ ABNAmro Magyar Minority in Kredyt Bank Majority in Agropolisa Minority in WARTA Majority in Kredyt Bank Majority in WARTA Minority in NLB Bank Creation of NLB Life 1999 2001 20002002 2003< 1999 Czech/ Hungary Poland Slovenia Slovak

8

8 + IPB Track record in CEE-3, banking KBC Participation Total assets Czech Hungary Poland 19992000200120022003 ROAC 2003 90% 59% 81% 18.3 bn 5.5 bn 4.8 bn +ABN Amro - 13 m - 91m - 385 m 27 m 23 m - 10 m 1 m 15 m 50 m 159 m 191 m 169 m Note : Profit contribution to KBC Group results, before minorities. 17% 8%/20% Neg -2 m Profit contribution 365m of loan book clean-up 50 m one-off results 33 m fraud charge '03 Turnaround to come through Strong operating performance Slovak

9

9 Group revenue profile Commission income Technical and investment income, insurance Other Yield income (Interest & dividend),banking Trading income Capital gains on disposals, banking

,banking Trading income Capital gains on disposals, banking")

10

10 Balanced credit portfolio CEE. 17 bn Other 3 bn W. Eur 23 bn Note : credit portfolio as of 31 Dec 03, incl. corporate bonds and loans to banks, excl. reverse repos. US 6 bn Sector breakdown Geographical breakdown Breakdown by area of activity Belgium, retail 38 bn Belgium, corporate 15 bn

11

11 Performing asset manager Assets under management (bn EUR) Breakdown of retail funds Equity, Belgium Bonds & MM, Belgium Mixed, Belgium Capital- guaranteed, Belgium Funds of funds, Belgium Market share, retail funds Belgium :31% Czech Republic :19% Slovak Republic :6% Hungary :8% Belgium: 87% CEE: 5% Retail Corporate 89 bn 81 bn 82 bn Retail CEE Unit-linked, Belgium

Breakdown of retail funds Equity, Belgium Bonds & MM, Belgium Mixed, Belgium Capital- guaranteed, Belgium Funds of funds, Belgium Market share, retail funds Belgium :31% Czech Republic :19% Slovak Republic :6% Hungary :8% Belgium: 87% CEE: 5% Retail Corporate 89 bn 81 bn 82 bn Retail CEE Unit-linked, Belgium")

12

12 Long-term shareholdership Cera Holding & Almancora Other stable shareholders MRBB Almanij Stock Market Gevaert Private equity KBC Bank & Insurance KBL Private bank ± 17% ± 16% ± 37% ± 78% 100% ± 67% ± 29% ± 31% Almanij is an investment company (of which KBC is ± 75% of the assets) committed to supporting KBC in the long run Core holders include the Ceragroup (co-operative investment company), a farmers’ association (MRBB) and a syndicate of industrialist families. KBC/Almanij is a major asset for all of them. Free float (October 2003)

.")

13

13 Steadily growing dividend Board of Directors’ policy to maintain a steadily growing dividend Gross dividend up every year over the past 5 years (at a CAGR of 9%) Average payout : 40-45% (usually cash). Payout may be raised to keep dividend stable in case of temporary drop in profit 199819992000200120022003 EPS2.693.263.903.393.423.68 DPS1.091.231.421.481.521.64 Payout41%38%36%44% 45% Yield1.8%2.1%3.1%3.6%4.2%4.9% Note: yield = gross DPS versus average share price. Figures 2000 excl. value gain on CCF

14

14 Undemanding valuation 2000200120022003 Closing price 46.137.730.437.0 EPS3.903.393.423.68 P/E (based on closing) 11.811.18.910.1 Net Asset Value 35.233.831.633.8 P/NAV1.31.11.01.1 Key figures Analyst forecasts (27 feb 2004) EPS 2004 consensus 4.12 EPS 2005 consensus 4.58 P/E (average 2 years) 10.7 Share price at 27-Feb: 46.34 Recommendations Positive :14 Neutral :9 Negative :3 Note: N° of shares outstanding as of 31 Dec. 2003, of which 7 m not dividend-entitled for 2003 : 310.7 m Figures 2000 excl. value gain on CCF

15

15 SWOT analysis Strengths Prominent market positions in home markets, both Belgium and CEE Geographical/business diversification Unique bancassurance concept Performing asset manager and non-life insurance division Good profitability track record and very sound solvency levels Stable core shareholders (long term) Opportunities Revenue growth and barely tapped cost cutting potential in CEE Availability of excess capital Weaknesses Still high cost/income ratio, banking Cost-reduction management is rather difficult in Belgium Volatility related to level of gearing to equity markets CEE: still a somewhat higher risk zone (although steadily converging) Lack of stability and scale in Poland (work in progress) Threats Consolidation wave in Europe, if any

Opportunities Revenue growth and barely tapped cost cutting potential in CEE Availability of excess capital Weaknesses Still high cost/income ratio, banking Cost-reduction management is rather difficult in Belgium Volatility related to level of gearing to equity markets CEE: still a somewhat higher risk zone (although steadily converging) Lack of stability and scale in Poland (work in progress) Threats Consolidation wave in Europe, if any")

16

Strategy overview

17

17 Group strategy Key objectives : 1.Cross selling (bancassurance) in Belgium 2.Reducing banking costs in Belgium 3.Strengthening the second home market in CEE KBC is a bancassurer focusing on local clients (individuals and SME) in Belgium and selected countries in (Central) Europe

in Belgium 2.Reducing banking costs in Belgium 3.Strengthening the second home market in CEE KBC is a bancassurer focusing on local clients (individuals and SME) in Belgium and selected countries in (Central) Europe")

18

18 Strategy and earnings drivers Achieved to date : Premium income boosted : Life premiums more than doubled from 1.1 bn in ’98 to 2.4 in ’03 (81% sold via bank outlets) Bank distribution of non-life products growing faster (+ 33%) than distribution via traditional channels (+5%) Going forward : Tap growth potential, though not to the detriment of technical performance : For SMEs ( 20% in banking) For non-life insurance (10% via bank channel vs 81% in life) Key objective 1 : Cross selling (bancassurance) in Belgium

Bank distribution of non-life products growing faster (+ 33%) than distribution via traditional channels (+5%) Going forward : Tap growth potential, though not to the detriment of technical performance : For SMEs ( 20% in banking) For non-life insurance (10% via bank channel vs 81% in life) Key objective 1 : Cross selling (bancassurance) in Belgium")

19

19 Strategy and earnings drivers Achieved to date : Merger synergies : Integrated IT-infrastructure Branch mergers (-41%) Headcount objective reached (-12%) Going forward : Further cost reduction: Reduce product complexity in retail (action plan consisting of 364 items) Out-/co-sourcing of processing and back-office functions (within the group and with third-parties) Rationalisation of head office space and other non-FTE expenses Key objective 2 : Reducing banking costs in Belgium

Headcount objective reached (-12%) Going forward : Further cost reduction: Reduce product complexity in retail (action plan consisting of 364 items) Out-/co-sourcing of processing and back-office functions (within the group and with third-parties) Rationalisation of head office space and other non-FTE expenses Key objective 2 : Reducing banking costs in Belgium")

20

20 Strategy and earnings drivers Achieved to date : Expansion in 5 target countries : Prominent franchises Renewed IT-infrastructure Bancassurance models set up Strengthened of internal governance model/central management structure Going forward : Performance enhancement : Sales of banking, insurance, AM products (deposits/ GDP at 45%-80% and premium/cap < 20 % of EU avg) Business reorganization in CR (HQ) and Poland 10-15% FTE downsizing Cross border cost-sharing (payments systems, IT procurement, etc.) If opportunities arise, acquisitions in Poland (banking) and Hungary (insurance) Key objective 3 : Developing a second home market in CEE

Business reorganization in CR (HQ) and Poland 10-15% FTE downsizing Cross border cost-sharing (payments systems, IT procurement, etc.) If opportunities arise, acquisitions in Poland (banking) and Hungary (insurance) Key objective 3 : Developing a second home market in CEE")

21

21 Note: combined ratio excl. re-insurance Cost/income ratio, banking 58% Combined ratio, non-life insurance 95% Tier-1, banking8% Solvency, insurance200% EPS growth (4y CAGR)10% ROE, group 16% ROAC Retail in Belgium16% Central and Eastern Europe17% Corporates12% Markets18% Demanding financial objectives Minimum targets for 2005

10% ROE, group 16% ROAC Retail in Belgium16% Central and Eastern Europe17% Corporates12% Markets18% Demanding financial objectives Minimum targets for")

22

FY ’03 financial highlights

23

23 Content Question time Performance 2003, overview Performance, banking Performance, insurance

24

24 Group result : up 8 % year-on-year Full-year results 2003 Q avg ‘01-’03 + 8% In m EUR + 1%

25

25 1 0221 034 Net profit ROE banking : 11.3 % ROE insurance : 17.4 % ROE Group: 12.7 % 1 119 Performance 2003 +8% +1% Banking : strong year-on-year performance Insurance : pressure on investment income, though high level of return in m EUR

26

26 Earnings growth peer group KBC DJ ES Banks DJ ES Insurance KBC Insurance KBC Banking Note : estimate 2003 DJ ES Banks at 20 Feb. 2004 by KBC Compared to the sector, earnings remained at a high level Earnings level 2000 = 100

27

27 Performance 2003 Overall : Change yoy pre-tax Positive impact :(m EUR) Strong income trend for all basic banking activities (spread, commission) +232 Strong premium growth, insurance+330 Strong technical result, non-life+59 Good cost control, banking+56 Less impairments on equity portfolios, banking+238 Negative impact : Higher loan-loss provisions- 211 Less gains on (‘free’) bonds, banking-148 Less favourable trading results-135 Less investment income, insurance-54 Net profit :+85

Strong income trend for all basic banking activities (spread, commission) +232 Strong premium growth, insurance+330 Strong technical result, non-life+59 Good cost control, banking+56 Less impairments on equity portfolios, banking+238 Negative impact : Higher loan-loss provisions- 211 Less gains on (‘free’) bonds, banking-148 Less favourable trading results-135 Less investment income, insurance-54 Net profit :+85")

28

28 Performance 2003 Areas of activity : Robust performance in Belgium Further improving level of costs in banking (-5%) Strong commission (+22%) and premium income (+8%) and interest spread slightly increasing (2.01% versus 1.97% in ‘02) Low level of loan loss ratio (24 bp) and non-life claims ratio (59%) Satisfactory operating performance in most CEE markets ROAC for banking in Czech (CR) / Slovak republics (SR) : 17% ROAC for banking in Hungary : 8% (20% excl. K&H Equities case) Improving performance for insurance operations (still limited scale) Higher profit of corporates (+19%) and markets (+35%) … but still disappointing performance of banking business in Poland (high loan loss provisions: 365 m) Note : ROAC = return on allocated capital

Improving performance for insurance operations (still limited scale) Higher profit of corporates (+19%) and markets (+35%) … but still disappointing performance of banking business in Poland (high loan loss provisions: 365 m) Note : ROAC = return on allocated capital.")

29

29 Growing dividend EUR Dividend per share : up 7.9% year-on-year Last 5 years : every year growing dividend (CAGR : 8.5%)

")

30

30 Business highlights 2003 Enhancing efficiency in Belgium Strengthening the position in CEE Further downscaling of less-strategic areas Finalizing the merger Product complexity reduction program Pooling of back offices and co-sourcing of transaction processing Stronger governance model and controlling Intensified cross-border initiatives in such areas as e.g. card technology Restructuring program in Poland Majority stake in WARTA (Poland) Successful start of bancassurance in Slovenia Sale of retail activities in the Netherlands, broker-related consumer lending in Belgium, non-strategic operations in CEE (Ukraine, Lithuania)

Successful start of bancassurance in Slovenia Sale of retail activities in the Netherlands, broker-related consumer lending in Belgium, non-strategic operations in CEE (Ukraine, Lithuania).")

31

31 Performance 2003, overview Performance, banking Content Performance, insurance Question time

32

32 Banking, income development Interest income : + 5% organically (margin : 1.67% 1.73%) Commission income : 12% organic growth (i.a. success of cap-guaranteed funds) Lower trading income due to i.e. lower FX income and MtM of equity derivatives Lower realized capital gains (250 m), mainly on the ‘free’ bond portfolio Lower dividends, ‘other income’ on a par with 2002 (strong leasing revenue) Total income -1% organically - 37% + 2% - 22% +15% Excluding capital gains, income + 1% 4 977 5 655 5 756

Lower trading income due to i.e. lower FX income and MtM of equity derivatives Lower realized capital gains (250 m), mainly on the ‘free’ bond portfolio Lower dividends, ‘other income’ on a par with 2002 (strong leasing revenue) Total income -1% organically - 37% + 2% - 22% +15% Excluding capital gains, income + 1%")

33

33 Growth in banking assets Customer deposits (bn EUR) Customer loans (bn EUR) Note : mortgage growth adjusted for currency depreciations Customer deposits : up 5% (excl. repos) Shift to demand deposits Shift to life products and mutual funds Customer loans : organically flat (excl. repos) Strong organic mortgage growth : Belgium :+ 10% C/SR : + 36% Hungary : + 69% Poland : + 24% Corporate book (excl. repos) down 3 bn EUR, reflecting : currency depreciations (2.4bn) build down of ‘old book’ (IPB) in CR (1.7 bn) & in the Netherlands (0.4bn) write-downs in Poland (0.3 bn)

Shift to demand deposits Shift to life products and mutual funds Customer loans : organically flat (excl. repos) Strong organic mortgage growth : Belgium :+ 10% C/SR : + 36% Hungary : + 69% Poland : + 24% Corporate book (excl. repos) down 3 bn EUR, reflecting : currency depreciations (2.4bn) build down of ‘old book’ (IPB) in CR (1.7 bn) & in the Netherlands (0.4bn) write-downs in Poland (0.3 bn).")

34

34 Banking, expense development Belgium : Expenditures : - 5% (- 105 m) Headcount reduction : target of 1 650 FTE (-12%) achieved Central and Eastern Europe : Expenditures : - 1% (-12 m) Headcount reduction : CR (HQ) : 54% of target of 1 000 FTE (-27%) achieved Poland : 28% of target of 1000/1200 FTE (-15%) achieved Other : Expenditures : + 14% (+60 m) Cost/Income ratio: 65% (65% for FY 02) 3 510 3 751 3 695 2001: KB only 4Q01 Ytd expenses (m EUR) Continuing cost control -1%

Headcount reduction : target of FTE (-12%) achieved Central and Eastern Europe : Expenditures : - 1% (-12 m) Headcount reduction : CR (HQ) : 54% of target of FTE (-27%) achieved Poland : 28% of target of 1000/1200 FTE (-15%) achieved Other : Expenditures : + 14% (+60 m) Cost/Income ratio: 65% (65% for FY 02) : KB only 4Q01 Ytd expenses (m EUR) Continuing cost control -1%")

35

35 Cost control in Belgium Merger completed, full extent of cost savings in bottom-line as of 1H 04 Lower cost/income ratio ahead, thanks to : Income growth Co-sourcing of transaction processing and pooling of back-office activities within the group and with third-parties Monitoring of real-estate-related and other non-FTE-costs Reduction in product complexity in retail Although Belgium is a ‘mature’ market, further growth and improvement in performance can be expected

36

36 Reducing product complexity PlannedRealizedE xample : To do Example : Payment services 5924% N o of types of credit cards from 8 to 4 76% N o of transactions forms from 34 to 5 Investment products 12940% N o of types of savings accounts from 8 to 1 60% Reduction in highly complex orders Home, car and travel services 4538% No add’l floating rates for consumer loans 62% N o of types of mortgages from 50 to 15 Services to companies 13140% Reduction in interest rate formulas for cash facilities 60% Integrating 15 types of insurance policies in more comprehensive policies TOTAL364 37%63% Note : situation as of Feb-2004 Implementation running or further enquiry required

37

37 Banking, loan provisions Customer loan book Gross loans Dec. 03 Loss ratio FY 03 Loss ratio FY 02 Belgium49.9 bn0.24%0.29% Hungary3.8 bn0.32%0.34% CR / SR6.0 bn0.34%-0.62% Poland3.8 bn8.68%4.20% International29.4 bn0.48%0.70% Total92.9 bn0.71%0.55% Loan loss provisions (m EUR) Loan loss ratio : 0.71% (0.55% for FY 02) Note : Loan loss = specific provisions to average gross outstanding loans Intensive clean-up of loan portfolio in Poland Loan loss ratio excl. Poland : 0.35% 676 321 465

Loan loss ratio : 0.71% (0.55% for FY 02) Note : Loan loss = specific provisions to average gross outstanding loans Intensive clean-up of loan portfolio in Poland Loan loss ratio excl. Poland : 0.35%")

38

38 Note: Profit contribution excl. retail asset management and excl. retail insurance. Loan loss ratio on risk-weighted assets Retail banking in Belgium Return on allocated capital 14% 13% x5 16% FY profit, banking: 225 m, ROAC : up to 12% from 2% Income growth : + 10% (strong commission and rebound in interest) Cost reduction : - 7% Provisions remain low (21 bp) Marketing headlines 2004 : New customer acquisition Bancassurance Wealth management 2003 has seen a strong turnaround in Belgian retail on the back of robust commission income and cost savings Profit contribution after minorities

Cost reduction : - 7% Provisions remain low (21 bp) Marketing headlines 2004 : New customer acquisition Bancassurance Wealth management 2003 has seen a strong turnaround in Belgian retail on the back of robust commission income and cost savings Profit contribution after minorities.")

39

39 Banking performance in CEE CR & SR : ROAC target of 17 % achieved in spite of pressure on margins (and fewer one-offs), thanks to commission income and modest expense growth Hungary : income and volume growth more than set off pressure on margin, but adverse impact of K&H Equities loss (pre-tax impact: 20 m) Poland : difficult economic conditions and high loan provisions due to thorough credit review (pre-tax impact 277m) Notes : profit contribution excl. minority interests. Change (%) adjusted for currency effect. Allocated capital: 7% on RWA + non-amortized goodwill. CEE 2 nd home In m EURFY 03% ChgROAC 03 CR / SR 143+0 %17% Hungary 13-13% (+97%)8% (20%) Poland -295-- Slovenia 10-- Contribution of banking operations to KBC Group profit Satisfactory performance in Czech Republic, Slovakia and Hungary (even further improvement expected). Polish turnaround being implemented

adjusted for currency effect. Allocated capital: 7% on RWA + non-amortized goodwill. CEE 2 nd home In m EURFY 03% ChgROAC 03 CR / SR %17% Hungary 13-13% (+97%)8% (20%) Poland Slovenia 10-- Contribution of banking operations to KBC Group profit Satisfactory performance in Czech Republic, Slovakia and Hungary (even further improvement expected). Polish turnaround being implemented.")

40

40 CEE banking, share of group wallet Impact of paid goodwill Improved cost structure under way Heavy credit risk charge in Poland in 2003 Value-added products and commission income to grow Note : banking business lines, excluding group center FY03 earnings Pre-tax result

41

41 Restructuring in Poland Capital base strengthened (265 m in 2 steps) Risk sensitivity greatly reduced Credit risk policies redefined and credit decision authority reduced ‘Historic’ loan book cleaned up Risk control and risk management improved Cost base to be further reduced Centralizing back offices, strengthening HR and performance measurement Reducing headcount (driven by new central IT system) by 1000/1200 FTE, real estate expenses (15-20 %) and other tangible costs (5-10%) by ‘04 Disinvesting non-strategic activities (Ukraine, Lithuania, PKB, Pension Fund,…) Market position to be improved on the retail market Thorough customer segmentation in the nationwide network Intensified transfer of product knowhow (AM, retail lending, bancassurance,…) Acceleration of bancassurance efforts with WARTA Insurance Profound restructuring plan being implemented Central Europe 2 nd home market

Risk sensitivity greatly reduced Credit risk policies redefined and credit decision authority reduced ‘Historic’ loan book cleaned up Risk control and risk management improved Cost base to be further reduced Centralizing back offices, strengthening HR and performance measurement Reducing headcount (driven by new central IT system) by 1000/1200 FTE, real estate expenses (15-20 %) and other tangible costs (5-10%) by ‘04 Disinvesting non-strategic activities (Ukraine, Lithuania, PKB, Pension Fund,…) Market position to be improved on the retail market Thorough customer segmentation in the nationwide network Intensified transfer of product knowhow (AM, retail lending, bancassurance,…) Acceleration of bancassurance efforts with WARTA Insurance Profound restructuring plan being implemented Central Europe 2 nd home market")

42

42 Central Europe 2 nd home market Loan provisioning level in Poland Adequately provisioned compared to peer group Sources: companies’ financial reports and presentations (consolidated basis)

")

43

43 Improving economic indicators Outlook : Economic growth is picking up Corporate tax reduction (to 19% in ’04) Credit demand is accelerating, notably mortgages/consumer lending Shift from deposits to funds (off-balance) is likely, compensating further margin pressure Poland GDP growth (y/y)

Credit demand is accelerating, notably mortgages/consumer lending Shift from deposits to funds (off-balance) is likely, compensating further margin pressure Poland GDP growth (y/y)")

44

44 Situation as of Dec 2002 : the network model CEE, governance model - 2002 CEE Group companies Co-ordination Unit CEE Insurance (2) Business co-ordinators (12) KBC expats (31) Co-ordination Unit CEE Banking (1) Moreover : audit and market and credit risk managment centralized (for credit risk in Poland only from end of 2002) Executive Committee Management Committee CEE (5) Initiating and followup of : Transfer of knowhow Shared business projects

Business co-ordinators (12) KBC expats (31) Co-ordination Unit CEE Banking (1) Moreover : audit and market and credit risk managment centralized (for credit risk in Poland only from end of 2002) Executive Committee Management Committee CEE (5) Initiating and followup of : Transfer of knowhow Shared business projects")

45

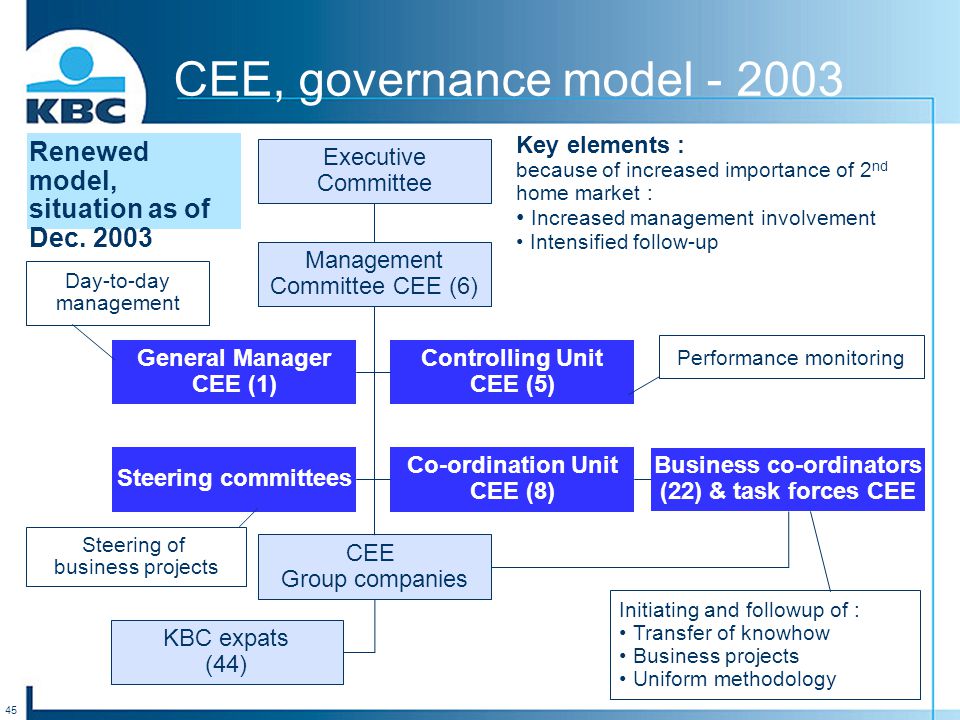

45 CEE, governance model - 2003 Executive Committee Management Committee CEE (6) General Manager CEE (1) Controlling Unit CEE (5) Steering committees Co-ordination Unit CEE (8) Business co-ordinators (22) & task forces CEE Performance monitoring CEE Group companies KBC expats (44) Day-to-day management Steering of business projects Initiating and followup of : Transfer of knowhow Business projects Uniform methodology Key elements : because of increased importance of 2 nd home market : Increased management involvement Intensified follow-up Renewed model, situation as of Dec. 2003

46

46 Asset Management division FY profit : 116 m (stable) : income pressure (market context) compensated by lower costs and taxes AUM : + 10% Retail assets : 10% including retail funds : + 11% of which : ± 5% net inflow Institutional (3rd party): + 6% Group assets : + 18% Note: As of 2004, in financial reporting, incorporated in retail / corporate area Assets under management (in bn EUR) 82 81 89 Retail Corporate Belgium : 87 % Central Europe : 5 % +10%

: income pressure (market context) compensated by lower costs and taxes AUM : + 10% Retail assets : 10% including retail funds : + 11% of which : ± 5% net inflow Institutional (3rd party): + 6% Group assets : + 18% Note: As of 2004, in financial reporting, incorporated in retail / corporate area Assets under management (in bn EUR) Retail Corporate Belgium : 87 % Central Europe : 5 % +10%")

47

47 FY profit : 220 m, + 7% Cost decrease (- 6%) due to strict cost control, especially in Belgium / Western Europe Strong income growth in leasing, Ireland, diamond sector but no repeat of 2002 one-off revenues. As a balance, income down 2% Lower provisions for problem loans, i.a. in traditional banking in the US Corporate banking division Profit contribution corporate banking (in m EUR, excl. minorities) +7% Details on corporate activities (m EUR)

+7% Details on corporate activities (m EUR).")

48

48 Financial markets division FY profit : 125 m (+ 35%) Money and capital markets : strong performance (+ 43%) Equity trading : substantial loss situation reversed Derivatives : satisfactory result but negative MtM for long derivatives Profit contribution market activities (excl. minorities): Details on market activities : FY 01FY 02FY 03 m EUR Note: including trading-, interest and commission income from market activities,excluding trading income in CEE and related to treasury and investment book +35%

: Details on market activities : FY 01FY 02FY 03 m EUR Note: including trading-, interest and commission income from market activities,excluding trading income in CEE and related to treasury and investment book +35%.")

49

49 Faster asset growth in line with expected 'faster' GDP growth : Full year impact of deposit rate cut in Belgium (if competition / capital market levels allow rates to be stable) and positive impact from higher interest rates/steeper yield curve Asset Management driven by ‘private pension building’ and expansion in CEE Expected higher contribution from equity subsidiaries Cost control : In Belgium : full impact of merger synergies + sustained cost discipline In CEE : efficiency programs in progress Cost sensitivity in all divisions Strong decrease in loan loss levels : Towards a 'normalized' level in Poland (versus 365 in 2003) Going forward, 2004 2004Real growth GDPInflation10y-yield Belgium CEE 0.9% 1.8% 2.5 / 4% 3.5 / 4.5% 1.3% 1% Diverse 4.1% 4.5% Diverse

and positive impact from higher interest rates/steeper yield curve Asset Management driven by ‘private pension building’ and expansion in CEE Expected higher contribution from equity subsidiaries Cost control : In Belgium : full impact of merger synergies + sustained cost discipline In CEE : efficiency programs in progress Cost sensitivity in all divisions Strong decrease in loan loss levels : Towards a normalized level in Poland (versus 365 in 2003) Going forward, Real growth GDPInflation10y-yield Belgium CEE 0.9% 1.8% 2.5 / 4% 3.5 / 4.5% 1.3% 1% Diverse 4.1% 4.5% Diverse")

50

50 Performance 2003, overview Performance, banking Content Performance, insurance Question time

51

51 Underwriting result, life FY 03 : 5% CEE Premiums ytd 8% organic growth FY 03 : 95% Belgium Very strong growth (bancassurance-driven) and shift to non-linked products Guaranteed rate (10y) in Belgium : 1H 03 : 3.25% 2H 03 : 2.75% Net premium income Total FY 01: 1 689 Total FY 02: 2 246 Total FY 03: 2 438

and shift to non-linked products Guaranteed rate (10y) in Belgium : 1H 03 : 3.25% 2H 03 : 2.75% Net premium income Total FY 01: Total FY 02: Total FY 03: 2 438")

52

52 Underwriting result, non-life Very low level Combined ratio Premiums +15% organically 104% 105% 96% 821 910 1 048 Very sound business, partly driven by upward trend in rates and by strong risk and cost discipline Net premium income

53

53 Cross selling, bancassurance Clients with both banking and insurance products sold by KBC (Belgium) Cross selling 2003, Belgium : Mortgage / fire insurance :50% Mortgage / death cover :67% Consumer loan / death cover :66% Cross selling continues

Cross selling 2003, Belgium : Mortgage / fire insurance :50% Mortgage / death cover :67% Consumer loan / death cover :66% Cross selling continues")

54

54 Insurance, investment income FY 02FY 03 Interest, dividend, rent 449455+1% Capital gains on shares 198138-30% Total647593-8% Investment return in FY 03 down to 5.9% from 7.2 % Suffering from low investment yields Note: capital gains on shares: 5.30 % on portfolio value (incl. write-back from provision for financial risk at 45 m in ‘03), excl. value adjustments for unit-linked products. Planned recurring value gains on shares in 2004 : 4.75 % on market value of portfolio.

, excl. value adjustments for unit-linked products. Planned recurring value gains on shares in 2004 : 4.75 % on market value of portfolio..")

55

55 Insurance in CEE, overview Premium 2003 Premium growth Profit contribution 2002 Profit contribution 2003 Czech Republic 165+9%-12.1-1.6 Hungary67+40%1.70.3 Slovak Republic 22---0.3 Poland440--6.2-1.9 Slovenia 10---0.8 Startup in 2003 : retail market share from zero to ± 4% Acquired at the end of 2002 Note : premium growth adjusted for changes in currency value. Profit contribution to KBC result after minorities. Bancassurance models now set up in all target countries, but looking for more significant scale Majority since end of 2003

56

56 Insurance in CEE, Poland WARTA Market position : Market share, non-life : 13 % (no 2) Nation-wide coverage Customers : ± 1.5 m Workforce : ± 4 000 FTE Premium income 2003 : 330 m EUR non-life 110 m EUR life Individual : 65% of premium income Leading product : motor insurance KBC’s footprint : 2000 : First stake (40%) 2003 : Majority stake (51%) 2004 : Clear control (75%) Strategic focus : Optimization of agency sales network Intensifiying bancassurance with KB Stronger expansion to small-sized enterprises Centralization of back-office activities and sustained cost discipline Majority in WARTA (Poland), important leverage of scale for KBC’s insurance activities in CEE Poland

Nation-wide coverage Customers : ± 1.5 m Workforce : ± FTE Premium income 2003 : 330 m EUR non-life 110 m EUR life Individual : 65% of premium income Leading product : motor insurance KBC’s footprint : 2000 : First stake (40%) 2003 : Majority stake (51%) 2004 : Clear control (75%) Strategic focus : Optimization of agency sales network Intensifiying bancassurance with KB Stronger expansion to small-sized enterprises Centralization of back-office activities and sustained cost discipline Majority in WARTA (Poland), important leverage of scale for KBC’s insurance activities in CEE Poland")

57

57 Insurance, non-recurring items In m EURFY 02FY 03 Non-recurring result : Value adjustments, shares- 299- 96 Non-recurring gains on securities+113+122 Other (write-back from egalization reserve in ’03 and other) +38+ 79 Transfer from (to) provision for fin. risks+157-140 Total non-recurring result9-35 Note: provision for financial risks, balance at 31 Dec. 2003 : 93 m EUR Non-recurring income offset by value adjustments and allocation to the provision for financial risks

58

58 Going forward, 2004 Full consolidation of WARTA Insurance (premium line impact : 435 m) Organic premium growth : sustained high single-digit growth, driven by Successful bancassurance model Consumer trend for ‘private pension building’ (life) Sustained good technical results (though '03 was ‘very’ good) Mitigated pressure on investment income Impairments on equity portfolio 2004 : In m EUR Market level Dec 2003 + 5%+ 10%+ 15% Expected impairments190170150130 Available provision for fin. risks93 Potential impact on P/L97775737 Available non-realized value gains 115175240300 Note : Available non-realized value gains in excess of 'normal' level of value gains of ±125 m (at 4.75% of market value of portfolio)

.")

59

Additional information

60

60 Year-to-date results, detailed overview m EUR FY 02FY 03 %% Organic % Gross operating income6 5936 498-1 % - banking5 7565 655-2%-1% - insurance852847-1% Administrative expenses- 4 212-4 2020% - banking- 3 751-3 695-1% - insurance-457-4999%7% Operating result2 3812 297-4%-2% - banking2 0051 961-2%-1% - insurance396348-12% Loan loss provisions Value adjust., non-recurring, extraordinary and other results - 465 - 205 - 676 20 Pre-tax profit1 7111 641- 4%- 4%- 4% Taxes- 511- 442 Minority interests- 166- 80 Net profit1 0341 1198%

61

61 Impact on gross operating income NLB Bank Equity method Q3Q4 2003 Ergo Insurance Krefima Bank Full consolidation Deconsolidation (previously full consolidation) Full consolidation as of 1Q04 ( previously equity method) 2004 Warta Insurance Q1Q2Q1Q2 +0.1% -0.4% Limited net impact of changes in consolidation in 2003 Main changes in scope of consolidation

Full consolidation as of 1Q04 ( previously equity method) 2004 Warta Insurance Q1Q2Q1Q2 +0.1% -0.4% Limited net impact of changes in consolidation in 2003 Main changes in scope of consolidation")

62

62 Group, key performance ratios Dec 01Dec 02Dec 03 Cost / income, banking70.5%65.2%65.3% Combined ratio, insurance99.9%101.4%94.8% Solvency (Tier 1), banking8.8% 9.5% Solvency, insurance504%320%316% Return on equity13.2%12.7% Growth in EPS (y-o-y)-13%+1%+8% Notes: combined ratio: excluding reinsurance. Solvency insurance: including unrealized gains.

63

63 Areas of activity, profit contribution Note : Profit contribution excluding minority interests. Profit growth in CEE after adjustments for currency effects. ActivityProfit % ROACHeadlines Retail, Belgium 453 m 25%16% - Strong commission and premium income - Cost reduction in banking (- 7% y-o-y) - Low loan losses (21 bp/RWA) and low combined ratio non-life (93%) Central Europe : - banking, CR/SR - banking, Hungary - banking, Poland -148 m 143 m 13 m -295 m = 0% 13% - 17% 8/20% - - Strong commissions in CR (but margin pressure and fewer one-offs) - Strong income growth in Hungary (but fraud provision charge of 33m) - High loan losses in Poland (365m) - Improvement in insurance (though limited scale) Asset management 116 m=- - AUM up 10% vs Dec 02 Corporate services 230 m 19%11% - Successful cost control and significant lower loan losses - Less one-off income (CLOs) - Reinsurance out of the red Market activities 125 m 35%11% - Fixed income: very strong - Equities: modest but cost-cutting successful - Derivatives: satfisfactory (suffered from MtM) Strong rebound in Belgium. Substantial adverse impact of Poland

- Low loan losses (21 bp/RWA) and low combined ratio non-life (93%) Central Europe : - banking, CR/SR - banking, Hungary - banking, Poland -148 m 143 m 13 m -295 m = 0% 13% - 17% 8/20% - - Strong commissions in CR (but margin pressure and fewer one-offs) - Strong income growth in Hungary (but fraud provision charge of 33m) - High loan losses in Poland (365m) - Improvement in insurance (though limited scale) Asset management 116 m=- - AUM up 10% vs Dec 02 Corporate services 230 m 19%11% - Successful cost control and significant lower loan losses - Less one-off income (CLOs) - Reinsurance out of the red Market activities 125 m 35%11% - Fixed income: very strong - Equities: modest but cost-cutting successful - Derivatives: satfisfactory (suffered from MtM) Strong rebound in Belgium. Substantial adverse impact of Poland.")

64

64 Interest spreads in Belgium Interest margin, banking Spread on new loans Going forward, increasing market rates could fuel top-line growth

65

65 Merger completed in Belgium Realization of merger synergies (% of objective)

")

66

66 Credit portfolio : cyclical sectors % of total portfolioDec '01Dec '02Dec '03EUR bnChg 03-02 Real estate5% 7.2-6% Electricity & water6%4% 4.6-24% Aviation1% 1.5-7% Shipping1% 1.4-7% Telecom2% 1%1.4-37% Hotel & restaurant1% 1.2-16% IT0.4% 0.68% Media0.5%0.4%0.3%0.5-16%

67

67 Low Interest rate risk covered by provisions (4% ref. rate) Premium growth 2002 Life portfolio Life reserves, Belgium (non-linked) Rate4.75%3.75%3.25%2.75%OtherTotal Traditional14%-8%--22% Universal28%23%22%2%3%78% Note : Universal life: flexible premium payments with 10-year interest rate guarantee on current premiums and without guarantee for future premiums Premium growth 1H2003 Premium growth 2H2003 Asset-backing allowing hedging of Interest rate risk

Premium growth 2002 Life portfolio Life reserves, Belgium (non-linked) Rate4.75%3.75%3.25%2.75%OtherTotal Traditional14%-8%--22% Universal28%23%22%2%3%78% Note : Universal life: flexible premium payments with 10-year interest rate guarantee on current premiums and without guarantee for future premiums Premium growth 1H2003 Premium growth 2H2003 Asset-backing allowing hedging of Interest rate risk.")

68

68 Sound business, even in low-interest-rate environment Profitability dynamics, life (non-linked) Reserve (1st yr) 100 Return on investment 4.83 % Allocated capital 9.25 Investment income, reserves 4.83 Investment income, capital 0.45 Investment income 5.27 Guaranteed rate 2.75 Profit BT 2.52 X X + - Simplified example : ROAC 20% Tax 0.68 Investment mix :75%Treasury bonds Return :4.20% (Example)20% Shares6.70% 5% Real estate6.70% 4.83% Return on allocated capital Note : reserve for year n = 100 x 1.048 ^n ROACYear1Year 2Year3Year n Rate at 2.75 %20%21 %23% Rate at 3.25 %16 %17 %19% -

Reserve (1st yr) 100 Return on investment 4.83 % Allocated capital 9.25 Investment income, reserves 4.83 Investment income, capital 0.45 Investment income 5.27 Guaranteed rate 2.75 Profit BT 2.52 X X + - Simplified example : ROAC 20% Tax 0.68 Investment mix :75%Treasury bonds Return :4.20% (Example)20% Shares6.70% 5% Real estate6.70% 4.83% Return on allocated capital Note : reserve for year n = 100 x ^n ROACYear1Year 2Year3Year n Rate at 2.75 %20%21 %23% Rate at 3.25 %16 %17 %19% -")

69

69 Low combined ratio, significant leverage on return Profitability dynamics, non-life Reserve ratio 200 Return on investment 5.45% Allocated capital 40 Investment income, reserves 10.9 Investment income, capital 2.2 Premium 100 Combined ratio -95.0 Investment income +13.1 Profit BT 18.1 Tax - 3.7 ROAC 36% X X + + - Investment mix :50%Treasury bonds Return :4.20% (Example)45% Shares6.70% 5% Real estate6.70% 5.45% Combined ratio105 %100%95% ROAC16 %26 %36 % - Simplified example : Return on allocated capital

45% Shares6.70% 5% Real estate6.70% 5.45% Combined ratio105 %100%95% ROAC16 %26 %36 % - Simplified example : Return on allocated capital")

70

70 Czech & Slovak republics - CSOB Market position : Inhabitants : 15 m Market share : 18% / 6 % Customers : ± 3.2 m Branches : 281 (+3400 POS) Workforce : ± 10 400 FTE KBC’s footprint : 1999 : Majority (privatization) 2000 : Take-over of IPB Bank Current stake : 90% Investment : ± 1.4bn (± 2.3 xBV) Financial track record : m EUR, IAS‘99‘00‘01‘02‘ 03 Net profit78134175214196 RWA : 6.8 bn (7% of KBC’s banking operations) Allocated equity : 1.0 bn (13% of KBC banking) Gross margin Cost/ income Loan loss Pretax margin Ratio10.0%71%34bp2.5% Share in KBC banking total 12%13%6%13% Margins on RWA Profit contribution 2003 : Sustained satisfactory results (though positive impact of exceptionals mainly in ‘01-’02) Note: participation including increase from 85% to 90% in 2004

Workforce : ± FTE KBC’s footprint : 1999 : Majority (privatization) 2000 : Take-over of IPB Bank Current stake : 90% Investment : ± 1.4bn (± 2.3 xBV) Financial track record : m EUR, IAS‘99‘00‘01‘02‘ 03 Net profit RWA : 6.8 bn (7% of KBC’s banking operations) Allocated equity : 1.0 bn (13% of KBC banking) Gross margin Cost/ income Loan loss Pretax margin Ratio10.0%71%34bp2.5% Share in KBC banking total 12%13%6%13% Margins on RWA Profit contribution 2003 : Sustained satisfactory results (though positive impact of exceptionals mainly in ‘01-’02) Note: participation including increase from 85% to 90% in 2004")

71

71 Hungary - K&H Bank Market position : Inhabitants : 10 m Market share : 11% Customers : ± 0.7 m Branches : 155 Workforce : ± 3 800 FTE KBC’s footprint : 1997 : Reference stake (32%) 2000 : Full ownership (100%) 2001 : Merger ABN Amro Magyar Current stake : 59% Investment : 0.3 bn (1.3 x BV) Financial track record : m EUR, IAS‘99‘00‘01‘02‘ 03 Net profit- 3210154636 RWA : 3.8 bn (4% of KBC’s banking operations) Allocated equity : 0.3 bn (4% of KBC banking) Gross margin Cost/ income Loan loss Pretax margin Ratio8.2%78%32bp 1.6% / 0.8% Share in KBC banking total 6%7%2%2% / 5% Margins on RWA Profit contribution 2003 : Turnaround proven to be successful. K&H Equities loss in '03. Stand-alone incl. minorities

72

72 Poland - Kredyt Bank Market position : Inhabitants : 38 m Market share : 6% Customers : ± 0.8 m Branches : 359 Workforce : ± 9 600 FTE KBC’s footprint : 1997 : First stake (5%) 1999 : Reference shareholder (49%) 2001 : Full ownership (56%) 2002 : Full control (76%) Current stake : 85% * Investment : 0.8 bn (c.2x est BV) Financial track record : m EUR, IAS‘99‘00‘01‘02‘ 03 Net profit2839-9-108-353 RWA : 4.4 bn (5% of KBC’s banking operations) Allocated equity : 0.4 bn (5% of KBC banking) Gross margin Cost/ income Loan loss Pretax margin Ratio7.8%87%9%Neg Share in KBC total 6%8%54%Neg Margins on RWA Profit contribution 2003 : Stand-alone, incl. minorities Thorough clean-up of loan book since '02 (late in the cycle) In-depth restructing plan being implemented. Turnaround to come Note: investments including capital increase of 4Q03 and 1Q04

In-depth restructing plan being implemented. Turnaround to come Note: investments including capital increase of 4Q03 and 1Q04.")

73

73 CEE, credit ratings upgrade in 2003 UpdateCountry rating Company rating Outlook CSOB (CR) Jan. 2001BBB + Stable Sept. 2003A-A- A-A- Stable K & H (Hungary) Oct. 2000BBB + Stable July 2003A-A- A-A- Stable KB (Poland) Oct. 1999BBB + Stable Sept. 2003BBB + Stable NLB (Slovenia) Feb. 1997BBB + Stable Sept. 2003A+A+ A-A- stable Fitch credit ratings

Oct. 2000BBB + Stable July 2003A-A- A-A- Stable KB (Poland) Oct. 1999BBB + Stable Sept. 2003BBB + Stable NLB (Slovenia) Feb. 1997BBB + Stable Sept. 2003A+A+ A-A- stable Fitch credit ratings.")

74

74 KBC in CEE Strengths Prominent market positions with nationwide branch networks Geographical diversification Satisfying results to date in most markets, except banking in Poland Common shared optimism on rebound of economic cycle in ’04 and long-term market growth in general As of May 2004 : all CEE affiliates (5 countries) operating in the EU Successful bancassurance and asset management concept at group level (knowhow is being transfered) Excess capital at group level with stable core shareholders (long term) Weaknesses Still high cost/income ratios (work in progress) Converging business margins CEE still a higher risk zone (allthough tempered by EU entry) Still unsatisfactory stability and scale in Poland (work in progress) Central Europe 2 nd home market Reconfirmed confidence in our strategy fundamentals

operating in the EU Successful bancassurance and asset management concept at group level (knowhow is being transfered) Excess capital at group level with stable core shareholders (long term) Weaknesses Still high cost/income ratios (work in progress) Converging business margins CEE still a higher risk zone (allthough tempered by EU entry) Still unsatisfactory stability and scale in Poland (work in progress) Central Europe 2 nd home market Reconfirmed confidence in our strategy fundamentals")

75

75 Economic outlook Real GDP growthInflation (CPI) 10-y interest rate 03e04e05e03e04e05eFeb 04Feb 05e EURO zone 0.5%1.8%2.4%2.1%1.7%1.6%4.1%4.8% Czech Republic 3.2%3.9%4.0%0.1%3.2%2.6%4.8%5.6% Slovak Republic 3.9%4.3%4.8%8.6%7.8%4.5%5.2%5.5% Hungary2.7%3.1%3.8%4.7%7.2%4.4%8.6%8.2% Poland3.9%4.4%4.2%0.8%2.5%2.0%6.8%6.7% Source: KBC Asset Management, March 2004

10-y interest rate 03e04e05e03e04e05eFeb 04Feb 05e EURO zone 0.5%1.8%2.4%2.1%1.7%1.6%4.1%4.8% Czech Republic 3.2%3.9%4.0%0.1%3.2%2.6%4.8%5.6% Slovak Republic 3.9%4.3%4.8%8.6%7.8%4.5%5.2%5.5% Hungary2.7%3.1%3.8%4.7%7.2%4.4%8.6%8.2% Poland3.9%4.4%4.2%0.8%2.5%2.0%6.8%6.7% Source: KBC Asset Management, March 2004")

76

76 Value adjustments, equity portfolio Significant value adjustments in ‘02 and in 1Q 03 (offset by non-recurring result) Investment portfolio banking Investment portfolio insurance 2 791 (26%) 638 (6%) 7 461 (69%) (book value in m EUR, at 31 Dec. 2003) 1 202 (3%) 42 093 (97%) Value adjustments, equity portfolio FY 01FY 02 FY 03 Note: portfolio insurance excl. unit-linked investment.

(3%) (97%) Value adjustments, equity portfolio FY 01FY 02 FY 03 Note: portfolio insurance excl. unit-linked investment..")

77

77 Unrealized gains In m EURDec 02Dec 03 % Banking book 1 7421 437- 18% Bonds1 6301 236 Shares113201 Insurance book 82324+ 294% Bonds497328 Shares- 516- 92 Real estate10186 Reduced losses on equity portfolio, driven by upward trend of stock markets Note: balance of gains and losses. Shares including participating interests.

78

78 Solvency 8.8% 9.5% 504% 320% 316% Banking business (Tier 1) Insurance business (Solvency margin) 581 m 676 m 1 458 m 3 793 m In m EUR Solid solvency in both banking and insurance allowing further investments if needed (no double gearing and no DAC)

Insurance business (Solvency margin) 581 m 676 m m m In m EUR Solid solvency in both banking and insurance allowing further investments if needed (no double gearing and no DAC)")

79

79 Basle II regulation Quantitative impact study (QIS 3) – 1st half 2003 : required capital compared with current required capital level : ApproachCredit riskTotal risk Standardized95%105% IRB Foundation76% 87% IRB Advanced74% 85% Positive impact from the lower weight of retail/SME portfolio But : for the time being, uncertainty prevails regarding risk classification in the CEE portfolio and on the changes emanating from the Jan-04 Basle Committee meeting Basle II may free up some capital

– 1st half 2003 : required capital compared with current required capital level : ApproachCredit riskTotal risk Standardized95%105% IRB Foundation76% 87% IRB Advanced74% 85% Positive impact from the lower weight of retail/SME portfolio But : for the time being, uncertainty prevails regarding risk classification in the CEE portfolio and on the changes emanating from the Jan-04 Basle Committee meeting Basle II may free up some capital")

80

80 EU directive : 1Q03 Regulation: 3Q04 Application : 1Q05 RequirementsImpact for KBC Group solvency No double gearing Appropriate leverage Minimum group solvency level OK Group governance 'fit and proper‘ organization Appropriate financial and risk procedures Reporting and supervision on risk concentrations and intragroup transactions Already anticipated : Integrated Executive level New Group CFRO function Centralized group risk department No material financial impact to be expected Financial conglomerate regulation

81

81 Outstanding convertible bonds In 2003, a mandatory convertible bond reached maturity : (coupon 12.2% in ’03) creating ± 6.8 m new KBCN shares (not dividend-entitled for 2003) Outstanding convertible bonds : Convertible bond 2005 : 417 m EUR (coupon 2.50%), maturing Dec. 2005, optionally convertible in 5.2 m shares (± 80 EUR/ share) of which ± 2 m held by KBC Mandatory convertible bond 2008 : 186 m EUR (coupon 3.50%), maturing 2008, to be converted in 2.7 m shares (± 69 EUR/share) No relevant dilutive instruments in the coming 4 years

of which ± 2 m held by KBC Mandatory convertible bond 2008 : 186 m EUR (coupon 3.50%), maturing 2008, to be converted in 2.7 m shares (± 69 EUR/share) No relevant dilutive instruments in the coming 4 years.")

82

82 Contact information Investor Relations Office : Luc Cool Nele Kindt Tel. : +32 2 429 49 16 E-mail : investor.relations@kbc.cominvestor.relations@kbc.com Visit www.kbc.com for the latest update on our company :www.kbc.com Press releases and E-mail alert service Financial information, annual and quarterly reports Company background, strategy and governance related items

Similar presentations

KBKBT BR (Reuters) B:KB (Datastream)>")