Download presentation

Presentation is loading. Please wait.

1

What Should States Do about Electronic Commerce? Some Thoughts for Tax Administrators Dan R. Bucks, Executive Director Multistate Tax Commission June 7, 1999 Views expressed are those of the author and not necessarily those of the Commission.

2

Two Parts Historical Perspective –Increasing Structural Obsolescence of Existing Taxes. –Shift of Tax Burden –Identify Factors Relevant to Electronic Commerce Response to Electronic Commerce –Need for Joint Action among States –Saving the Sales Tax –Policy Choices in Business Taxation –Skip the Property Tax for Now

3

Structural Obsolescence “Structural obsolescence” of a tax base occurs when economic and/or behavioral trends cause a shift of economic activity from taxable to non-taxable categories. Alternatively, it is “non-legislated” erosion in the tax base.

4

State and Local Tax Bases Last 20 to 25 Years Sales tax bases have been steadily eroding in relative terms since the early 1970’s. Property and corporate income tax bases, again in relative terms, have been steadily eroding since 1980’s. Tax base erosion masked by sales tax rate increases and strong economic growth (plus some one-time fiscal events) in the 1990’s.

in the 1990’s..")

5

E-Commerce in Historical Context Electronic commerce will accelerate and amplify the economic and behavioral trends that have steadily undermined property, corporate income and sales tax bases in the recent past.

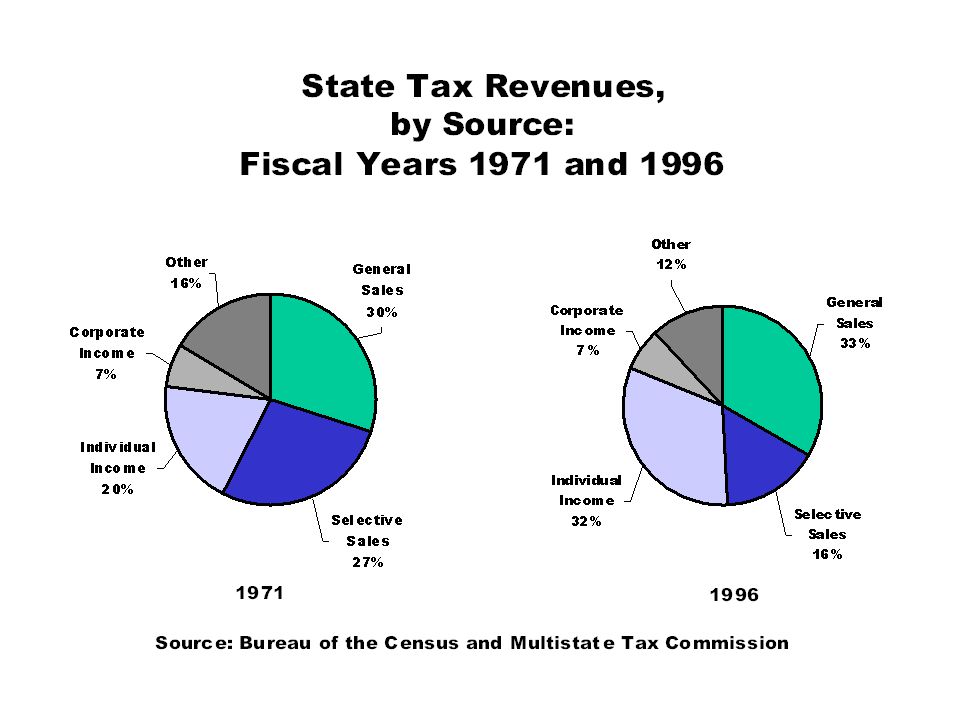

7

Local Tax Revenues, by Source: Fiscal Years 1971 and 1996 19711996 Source: Bureau of the Census and Multistate Tax Commission

9

State and Local Property Taxes as Percent of Assets: 1946 to 1998 Source: U.S. Bureau of Economic Analysis and Multistate Tax Commission Tangible Assets All Assets

10

State and Local Property Taxes as Percent of Assets: 1981 to 1998 Source: U.S. Bureau of Economic Analysis and Multistate Tax Commission Tangible Assets All Assets

11

Property Tax Story Property taxes are increasing on physical wealth as intangible wealth goes largely untaxed. Intangible wealth is of increasing importance in a knowledge economy.

13

Sales Tax Story Sales taxes rates are rising faster than the base is eroding—with sales taxes increasing in overall importance in state and local finance. How long can rising rates bail out a failing base?

14

Sales Tax Base Erosion Remote Sales Shift to Services Legislative Changes

15

State and Local Corporate Profit Tax Accruals as Percent of Corporate Profits Source: Bureau of Economic Analysis, Multistate Tax Commission.

17

Corporate Tax Story Effective rates of corporate tax fell by half from mid-1980’s, with revenues holding steady due to corporate profit trends.

18

Corporate Tax Story Tax Incentives for Mobile Businesses Rising Importance of Intangible Assets Weakened Apportionment Policies Growth of Pass-Through Entities Aggressive Tax Planning

19

State and Local Individual Income Taxes as Percent of Adjusted Personal Income Source: U.S. Bureau of Economic Analysis and Multistate Tax Commission.

20

Income Tax Story Individual income tax is the only state and local tax resting on a solid base. State governments are relying more on income tax—increasing rates on an increasing base. How long will individual income taxpayers be willing and able to pick up the tab?

21

Summing Up the History “Horse and Buggy” Sales Tax “Swiss Cheese” Corporate Income Tax System. The Property Tax is the “Elephant in the Living Room.” Individual Income Tax is the “Engine.”

22

Winners & Losers Winners Interstate Commerce Service and Knowledge Sectors Losers Local Commerce and Residents Goods Sectors

23

What Does the Past Say about the Future? In recent past, tax bases eroded because of: Growth of Intangibles Shift to Services Geographic Mobility of Production

24

E-Commerce and Future of State & Local Taxes As electronic commerce grows: Intangibles will become more important. Goods will be converted to services. Mobility of production will accelerate.

25

Thinking about Future Action No one state can resolve the issues of electronic commerce alone... unless your state wants to be a tax haven.

26

What Should States Do? Fix the Sales Tax... Together. Clarify Goals for Corporate Income or Business Activity Taxation... Then Work Together to Achieve Goals. Pray for the Property Tax.

27

Fixing the Sales Tax Aim for Zero Burden for Remote Sellers Quill: –Burden of Collection + Retroactivity = Barrier to Nexus. –Zero Burden of Collection + Prospectivity = Zero Barrier for Nexus

28

Fixing the Sales Tax Simplify, Simplify, Simplify Pay for Complexity Enforce Current Nexus Rules Fairly and Properly Then, States Need to Ask Congress or Courts to Change Nexus Rules

29

Some Key Simplifications Rate Simplification: One Rate per State for Remote Sales, or Geographic Information System with Safe Harbor Tax Included Option

30

Some Key Simplifications Joint, Multistate Registration System Filing and Payment Simplification: Uniform Electronic Funds Payment Systems State Level Returns Only Electronic “Pitcher and Catcher” Systems

31

Pay for Complexity Based on competition, certify and pay for software for calculation, filing and payment of tax on electronic commerce sales. E-commerce runs on software... so pay to embed tax collection software in electronic commerce systems. Software is the future tax instruction booklet.

32

Additional Simplifications Improved Exemption Administration: –All states should accept uniform exemption certificate... and it should be electronic. –State electronic database of exempt entities. Streamline Audit Process Develop Uniform Definitions for Tax Base

33

Corporate Income Taxes State Governors and Legislatures Need to Decide if They Want a Real Tax or a Pretend Tax. Role of Tax Administrators: Help Policy-Makers Understand What is Happening to Tax and Why.

34

Corporate Income Taxes: Policy Options Options for a Real Tax: Revive the Corporate Income Tax or Switch to a Broad-Based Business Activity Tax with Uniform Multistate Apportionment.

35

Corporate Income Taxes If the policy choice is to revive the tax, then the goal should be to achieve equal treatment with other income taxpayers... and that means full apportionment of income in reasonable relationship to where the income is earned.

36

Corporate Income or Business Activity Taxes Regardless of the policy choice of the form of the tax, uniform multistate rules and systems are needed to make these taxes work properly.

37

Key to the Future If states wish to make their tax systems work, they need to work together.

Similar presentations

Streamlined Sales Tax Project (SSTP) Overview Society for Information Management (SIM)>")

Aid.>")

Grants state and local jurisdictions the right to require the collection.>")