Download presentation

Presentation is loading. Please wait.

1

Interest rate futures

2

DAY COUNT AND QUOTATION CONVENTIONS TREASURY BOND FUTURES EURODOLLAR FUTURES Duration-Based Hedging Strategies Using Futures HEDGING PORTFOLIOS OF ASSETS AND LIABILITIES

3

The interest earned between the two dates Day Count Conventions in the U.S. Treasury Bonds:Actual/Actual (in period) Corporate and municipal Bonds: 30/360 Money Market Instruments:Actual/360

Corporate and municipal Bonds: 30/360 Money Market Instruments:Actual/360.")

4

Bond Principal 100 Coupon Payment dates 3/1, 9/1(reference period) Coupon Rate 8% Calculate the interest earned between 3/1 and 7/3 Treasury bond Actual/Actual (in period) Corporate and municipal Bonds 30/360

Coupon Rate 8% Calculate the interest earned between 3/1 and 7/3 Treasury bond Actual/Actual (in period) Corporate and municipal Bonds 30/360")

5

5 DDay counts can be deceptive(business snapshot) 2/28 2005, 3/1 2005 Which would you prefer? Treasury bond or Corporate and municipal Bonds Answer: Corporate and municipal Bonds 30/360

6

P is the quoted price(discount rate) Y is the cash price n is the remaining life of the Treasury bill measured in calendar days

Y is the cash price n is the remaining life of the Treasury bill measured in calendar days")

7

Face Value = 100 Quoted Price = 8 Interest over the 91-day life=2.0222 Interest Rate for the 91 day period=2.064%

8

Treasury Bond Price in the U.S are quoted in dollars and thirty-second of a dollar The quoted price is for a bond with a face value of $100 Cash price = Quoted price +Accrued Interest

9

2010/3/52010/1/102010/7/10 Face Value = 100 Coupon Rate = 11% Quoted Price = 95-16 or $95.50 2018/7/10 Accrued Interest= Cash price= $95.5+$1.64=$97.14 The cash price of a $100000 bond is $97140

10

Treasury bond future price are quoted in the same way as the Treasury bond prices themselves. One contract involves the delivery of $100000 face value of the bond A $1 change in the quoted futures price would lead to a $1000 change in the value of the future contract Delivery can take place at any time during the delivery month

11

Cash prices received by party with short position=(Most Recent Settlement Price × Conversion factor) + Accrued interest Example Settlement price of bond delivered = 90.00 Conversion factor = 1.3800 Accrued interest on bond =3.00 Price received for bond is (1.3800×90.00)+3.00 = $127.20 per $100 of principal

+ Accrued interest Example Settlement price of bond delivered = Conversion factor = Accrued interest on bond =3.00 Price received for bond is (1.3800×90.00)+3.00 = $ per $100 of principal")

12

The party with the short position receives = (Most recent settlement price × Conversion factor)+ Accrued interest The cost of purchasing a bond = Quoted bond price + Accrued interest The cheapest-to-deliver is Min [Quoted bond price – (Most recent settlement price × Conversion factor)]

![The party with the short position receives = (Most recent settlement price × Conversion factor)+ Accrued interest The cost of purchasing a bond = Quoted bond price + Accrued interest The cheapest-to-deliver is Min [Quoted bond price – (Most recent settlement price × Conversion factor)]](http://images.slideplayer.com/13/3856984/slides/slide_12.jpg "The party with the short position receives = (Most recent settlement price × Conversion factor)+ Accrued interest The cost of purchasing a bond = Quoted bond price + Accrued interest The cheapest-to-deliver is Min [Quoted bond price – (Most recent settlement price × Conversion factor)]")

13

The most recent settlement price =93-08, 93.25 The cost of delivering each of the bonds: Bond1:99.59 – (93.25 ×1.0382)= $2.69 Bond2:143.50 – (93.25 ×1.5188)=$1.87 Bond3:119.75 – (93.25 ×1.2615)=$2.12 Quoted bond price – (Most recent settlement price × Conversion factor)] BondQuoted bond price($) Conversion factor 199.591.0382 2143.501.5188 3119.751.2615

![The most recent settlement price =93-08, The cost of delivering each of the bonds: Bond1:99.59 – (93.25 ×1.0382)= $2.69 Bond2: – (93.25 ×1.5188)=$1.87 Bond3: – (93.25 ×1.2615)=$2.12 Quoted bond price – (Most recent settlement price × Conversion factor)] BondQuoted bond price($) Conversion factor](http://images.slideplayer.com/13/3856984/slides/slide_13.jpg "The most recent settlement price =93-08, The cost of delivering each of the bonds: Bond1:99.59 – (93.25 ×1.0382)= $2.69 Bond2: – (93.25 ×1.5188)=$1.87 Bond3: – (93.25 ×1.2615)=$2.12 Quoted bond price – (Most recent settlement price × Conversion factor)] BondQuoted bond price($) Conversion factor")

14

A number of factors determine the cheapest-to-deliver bond [Quoted bond price – (Most recent settlement price × Conversion factor)] Bond Yields 6% Yield Curve is The Wild Card Play

![A number of factors determine the cheapest-to-deliver bond [Quoted bond price – (Most recent settlement price × Conversion factor)] Bond Yields 6% Yield Curve is The Wild Card Play](http://images.slideplayer.com/13/3856984/slides/slide_14.jpg "A number of factors determine the cheapest-to-deliver bond [Quoted bond price – (Most recent settlement price × Conversion factor)] Bond Yields 6% Yield Curve is The Wild Card Play")

15

An exact theoretical future price for the treasury bond contract is difficult to determine Assume both the cheapest-to-delivery bond and the delivery date are known F: future price S: spot price I : present value of the coupons during the life of future contract

16

Cheapest-to-deliver coupon rate 12% Conversion factor 1.4000 Current quoted bond price $120 Interest rate 10% annum Delivery will take place in 270 days Coupon payment Current time Maturity of futures contrac t 60 days122days148days35days Cash price The present value of a coupon of$6 will be received after 122 days (0.3342years)

")

17

Coupon payment Current time Maturity of futures contrac t 60 days122days148days35days The futures contract lasts for 270 days (0.7397years) The cash price, If the contract were written on the 12%

The cash price, If the contract were written on the 12%")

18

Coupon payment Current time Maturity of futures contrac t 60 days122days148days35days There are 148 days of accrued interest. The quoted futures price, if the contract were written on the 12% bond, is calculated by subtracting the accrued interest The quoted future price =

19

A Eurodollar is a dollar deposited in a bank outside the United States Eurodollar futures are futures on the 3- month Eurodollar deposit rate (same as 3-month LIBOR rate) One contract is on the rate earned on $1 million

One contract is on the rate earned on $1 million")

20

Eurodollar futures contracts last as long as 10 years When it expires (on the third Wednesday of the delivery month) the final settlement price is 100 minus the actual three month deposit rate 100-R

the final settlement price is 100 minus the actual three month deposit rate 100-R")

21

If Q is the quoted price of a Eurodollar futures contract, the value of one contract is 10,000[100- 0.25(100-Q)] A change of one basis point or 0.01 in a Eurodollar futures quote corresponds to a contract price change of $25 The $25 per basis point rule is consistent that an interest rate per year changes by 1 basis point, the interest earned on 1 million dollar for 3 months change by 1000000×0.0001(0.01%) ×0.25(3 個月期 )=25 or $25

![If Q is the quoted price of a Eurodollar futures contract, the value of one contract is 10,000[ (100-Q)] A change of one basis point or 0.01 in a Eurodollar futures quote corresponds to a contract price change of $25 The $25 per basis point rule is consistent that an interest rate per year changes by 1 basis point, the interest earned on 1 million dollar for 3 months change by ×0.0001(0.01%) ×0.25(3 個月期 )=25 or $25](http://images.slideplayer.com/13/3856984/slides/slide_21.jpg "If Q is the quoted price of a Eurodollar futures contract, the value of one contract is 10,000[ (100-Q)] A change of one basis point or 0.01 in a Eurodollar futures quote corresponds to a contract price change of $25 The $25 per basis point rule is consistent that an interest rate per year changes by 1 basis point, the interest earned on 1 million dollar for 3 months change by ×0.0001(0.01%) ×0.25(3 個月期 )=25 or $25")

22

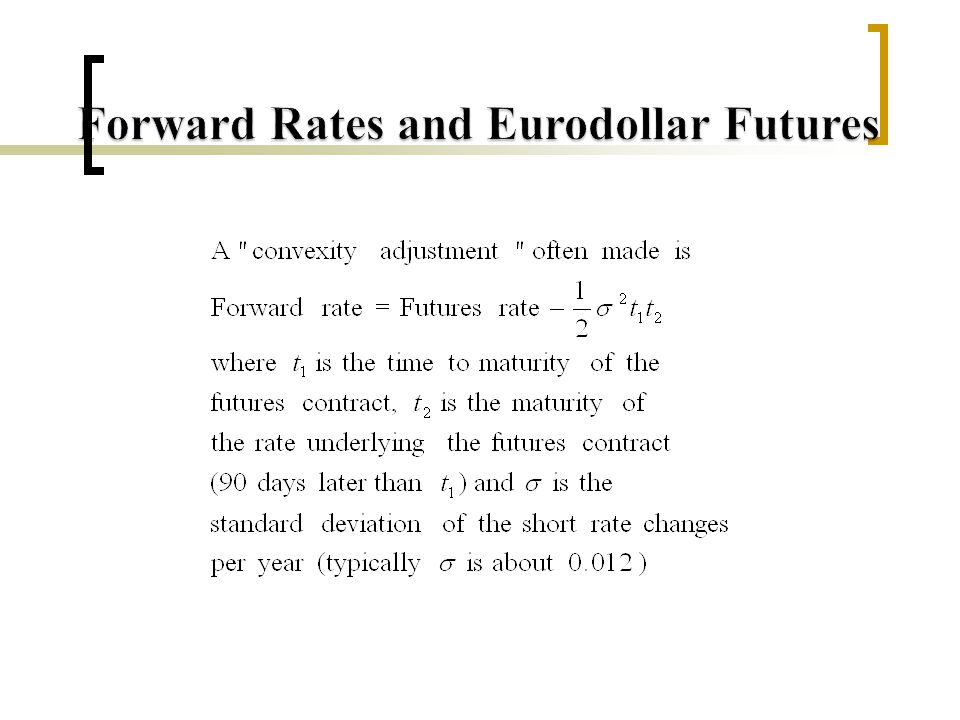

For Eurodollar futures lasting beyond two years we cannot assume that the forward rate equals the futures rate There are Two Reasons reduce the forward rate 1.Futures is settled daily where forward is settled once 2.Futures is settled at the beginning of the underlying three-month period; forward is settled at the end of the underlying three- month period

24

Consider the situation where σ=0.012 and we wish to calculate the forward rate when the 8- year Eurodollar futures price quote is 94. 1. In this case T1=8, T2=8.25, and convexity adjustment is or 0.475%(47.5 basis points)

.")

25

2.The future rate is 6% per annum on an actual/360 basis, annual rate of 6%(365/360) = 6.083% 3.The estimate of the forward rate is 6.083-0.475=5.608%

= 6.083% 3.The estimate of the forward rate is =5.608%")

26

Maturity of Futures Convexity Adjustment (bps) 23.2 412.2 627.0 847.5 1073.8

")

27

LIBOR deposit rates define the LIBOR zero curve out to one year Once the convexity adjustment just described has been made, Eurodollar futures are often used to extend the zero curve Eurodollar futures can be used to determine forward rates and the forward rates can then be used to extend the zero curve It is usually assumed that the forward interest rate calculated from the future contract applies to the

28

Suppose that Fi is the forward rate calculate from the ith Eurodollar futures contract and is the zero rate for a maturity Ti equation(4.5) So that

So that")

29

If the 400 day LIBOR rate has been calculated as 4.80% with continuous compounding and the forward rate for the period between 400 and 491 days is 5.30%, the 491 days rate is 4.893%

30

Define: FCFC Contract price for interest rate futures DFDF Duration of asset underlying futures at maturity PValue of portfolio being hedged DPDP Duration of portfolio at hedge maturity

31

Assumes that only parallel shift in yield curve take place Assumes that yield curve changes are small It is approximately true that (4.15) It is also approximately true The number of contracts required to hedge against an uncertain is

It is also approximately true The number of contracts required to hedge against an uncertain is")

32

When the hedge instrument is a Treasury bond futures contract, the hedger must base on an assumption that one particular bond will be delivered, this mind the hedger must estimate the cheapest-to-deliver bond the interest rates and future prices move in opposite direction

33

It is August 2. A fund manager has $10 million invested in a portfolio of government bonds with a duration of 6.80 years and wants to hedge against interest rate moves between August and December The manager decides to use December T-bond futures. The futures price is 93-02 or 93.0625 and the duration of the cheapest to deliver bond is 9.2 years The number of contracts that should be shorted is

34

This involves hedging against interest rate risk by matching the durations of assets and liabilities It provides protection against small parallel shifts in the zero curve Duration matching does not immunize a portfolio against nonparallel shifts in the zero curve

35

This is a more sophisticated approach used by banks to hedge interest rate. It involves Bucketing the zero curve Hedging exposure to situation where rates corresponding to one bucket change and all other rates stay the same.

Similar presentations

t FUTURE VALUE OF A SUM F v INVESTED TODAY AT A RATE r FOR A PERIOD t :>")

, maturity –Risk-free interest rates.>")