Download presentation

Presentation is loading. Please wait.

2

Merrill Lynch now charges a percentage instead of commissions to a lot of people. This means they have no incentive to churn. Means less trading, not less owning. Also index ETFs don’t have to do a lot of buying nadn selling, but the old style managed mtual funds did much more. Huge rise in ETFs and also a rise in index mutual funds. A large drop in managed equity mutual funds Lower volatility means less high frequency trading

3

Macrotrend stocks

5

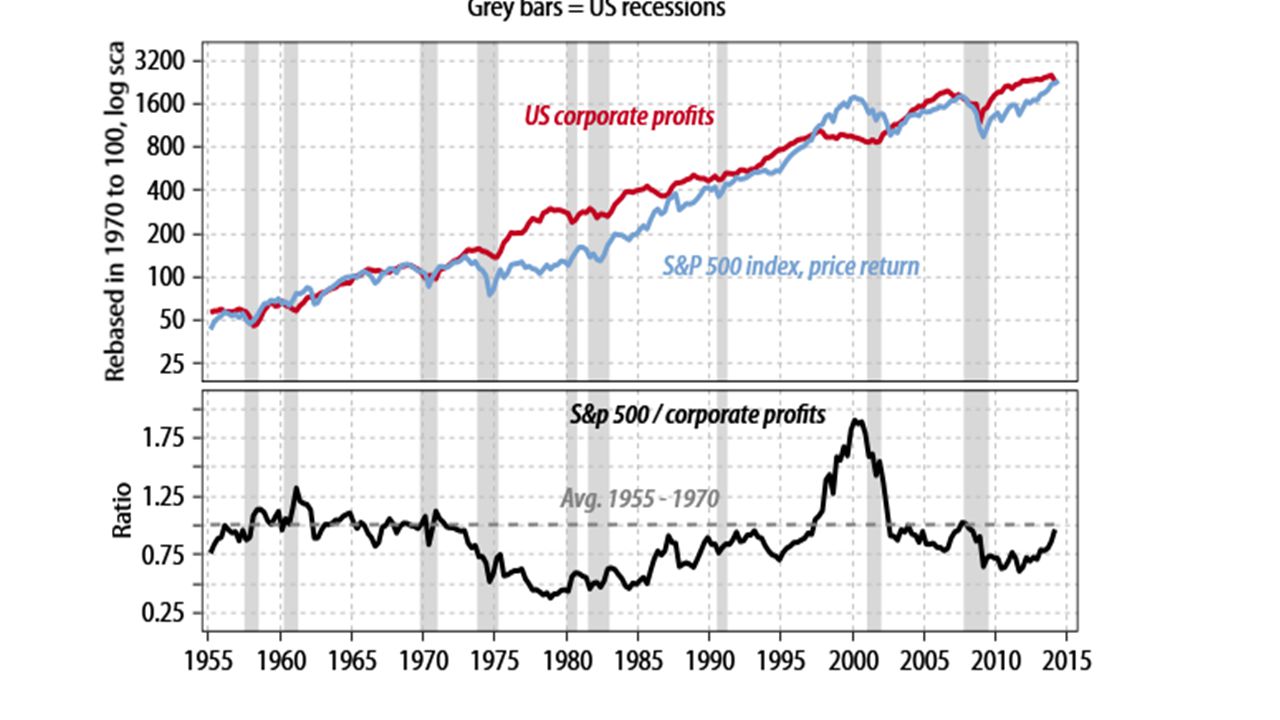

Switched to S&P 500, emphasizing size instead of effective capital deployment.

8

These look like a lousy deal starting with march 2014

14

undervalued overvalued

15

So where are we today? The ratio between stock prices and corporate profits is right on the average that persisted between 1955 and 1970 and hence I have a hard time believing that US equities are greatly over- valued. More broadly, the experience of the last 60 years shows periods of tremendous undervaluation (1978) and phases when the market was far too high (2000). This is not the case today. Plenty of bear markets have started from a “correct valuation” level since investors have tended to hugely underestimate the chance of a big decline in earnings (this was the case in 1962, 1970, 1973, 1981 and 2008)

and phases when the market was far too high (2000). This is not the case today. Plenty of bear markets have started from a correct valuation level since investors have tended to hugely underestimate the chance of a big decline in earnings (this was the case in 1962, 1970, 1973, 1981 and 2008).")

16

As things stand today, corporate profits have been flat for the last two years while the stock market is up more than 26%. The good news is that each time the decision rule offered such a clear signal in the post- 1982 period, investors for the most part benefited by buying long dated bonds. A simple rule of thumb is that when corporate profits are decelerating or falling, then investors should buy a fixed return rather than a variable return (see chart overleaf

17

Corporate profits fell behind stock prices by 26%. As of November 2013. Remember flat profits in Q4 2013 and Q1 2014. Regardless of excuse. They seem to be picking up right now. I’m not predicting a crash. I am observing excessive optimism and excessive confidence. See the relative performance of 30 year strips vs stocks

18

Charles Gave Gave-Kal

21

Sunday night just signaling short term bottom for russel 2000

24

After February a transition occurred in the stock market which continues today. Only the large cap, SP-500 is holding up. Small caps down by between 6 and 10%. S&P 500 holding up in the face airplanes being shot down, disorder everywhere. I moved from profit growth portfolio to Index, and growth stocks continue to underperform the large cap index. There is a good chance the S&P 500 will continue uninterrupted for many more months, Possibilities: 1.market correction continues but S&P 500 holds up fine 2.Serious correction develops which spreads to the big caps, then the market rallies after 3.Serious geopolitical concerns overtake the market. 4.Have not been moving assets for timing reason, only to preserve capital in the face of danger.

25

Issues: 1.Should we protect portfolio when geopolitical events threaten or just stay withbig Cap stocks? The odds favor the stock market holding up, but gaining extra few percent would not be as important to your life as losing a pile of money, even if unlikely. Portfolio plan 1.Can set up a million dollar fund which stays in until the bull market ends, risking geopolitics but high odds of substantial gain. Large cap – S&P 500 and NASDAQ 100 stocks. Individual profitable companies are not performing in this late stage bull market. beat s&P but no crash no guarantee. 2.Buy macrotrend stocks gradually and do not use them to compare to short-term movements of the S&P 500. The index is just momentum investing. It is allocating assets by size of company instead of by efficiency of resource utilization. It will eventually push the prices of large companies to the point where they are no longer worth buying. For now, though, they are the only thing going UP. The biggest moneymakers are bargains. They are not outperforming as stocks. They are outperforming as companies. We invest and make a fortune on the best companies… gilead, constellation brands, boeing, pioneer, emes, 3.set up fracking, portfolio – 20% of assets- to hold, not compete with index short term. This is where you can make major profits over a few years 1.upstream- engineering, drilling eog, pioneer, C&J 2.Proppant – EMES 4.5% dividend, HCLP 3.8% dividend 3.Midstream - train cars and pipelines KMP 7%, EPD if stock comes down. 4.Downstream – refinery – later after sell-off based on crack spread 4. 30% bonds and income – You have bonds bought earlier under better terms than are available now. Right now pipelines and income are a better deal. Yields are too low on higher yielding bonds. Will buy them at discount when economy turns down.

27

In other words, highly profitable to borrow Euros and buy U.S. assets. This supports U.S. stocks and bonds. Also profitable to short euros and buy U.S bonds. As 2 separate trades to synthesize carry trade.

28

Equity futures are infinitely more efficient, cost less and if you do them right they are exactly the same as owning the index.

Similar presentations

FIN 200: Personal Finance Topic 17–Stock Analysis and Valuation Lawrence Schrenk, Instructor.>")