Download presentation

Presentation is loading. Please wait.

1

European Mortgage Markets after the Credit Crisis Plenary Session 3 ENHR Toulouse 7 July 2011 Kath Scanlon London School of Economics

2

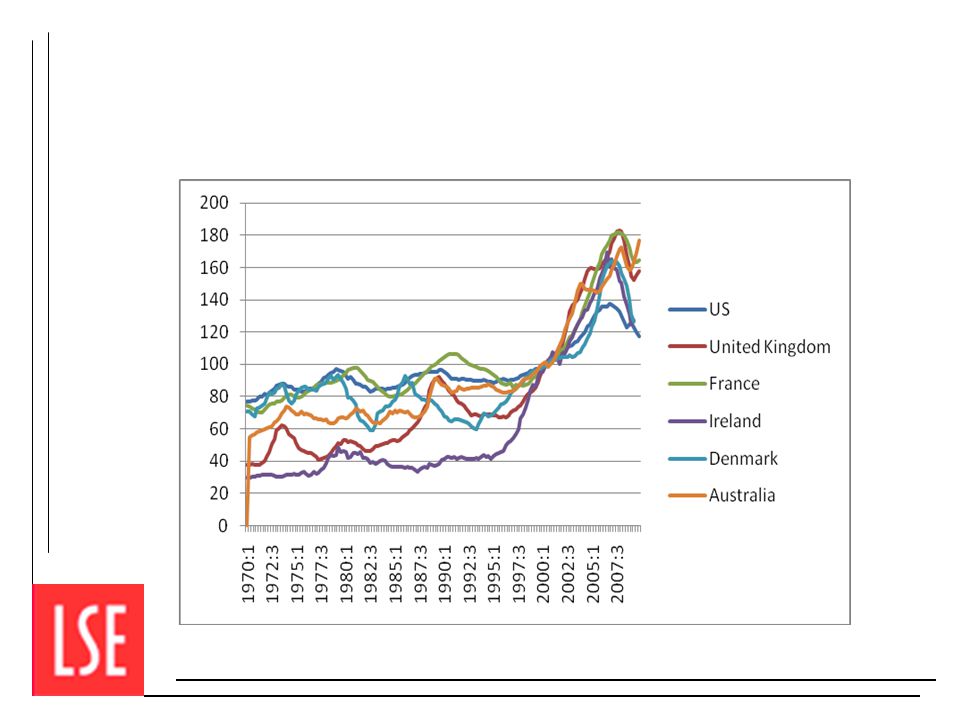

Mortgage industries in the boom Mortgage market deregulation: new entrants, more competition New funding models Rising house prices ↓ ( ↑) Proliferation of new mortgage products ↓ Higher household indebtedness

Proliferation of new mortgage products ↓ Higher household indebtedness")

3

The traditional mortgage Annuity (each payment contains both principal and interest) 20- to 25-year term Maximum 80% loan-to-value ratio (in some countries lower) Maximum loan amount determined by borrower income (2.5 to 3x annual income OR payment less than 30% of monthly income)

20- to 25-year term Maximum 80% loan-to-value ratio (in some countries lower) Maximum loan amount determined by borrower income (2.5 to 3x annual income OR payment less than 30% of monthly income)")

4

New products Interest-only Longer terms Foreign currency High loan-to-value ratios High loan-to-income ratios Self certification All achieve lower monthly payments

5

Funding of mortgage lenders Traditional Retail deposits Bonds Innovative Money markets (inter-bank loans) Securitization (the norm in USA, less so elsewhere )

Securitization (the norm in USA, less so elsewhere )")

6

Consequences of changes in products and funding Eased affordability problems for borrowers Fuelled house-price increases New products added to risk, especially in combination New funding models vulnerable to credit market conditions

7

Outlook If house prices continued to rise and general economy remained healthy: Good If house prices fell and general economy deteriorated: Poor

8

Crisis timeline 2006: Housing transactions begin to fall in some countries 2007: House prices begin to fall in most countries 2008: Lehman Brothers collapse closes inter-bank lending markets

10

Banking & development industries after 2007 Bank crisis and restructuring, including nationalisations, in many countries Not necessarily involving mortgage lenders or domestic housing markets—but reflecting new more globalised funding patterns Decline in housing starts and completions, leading to financial problems for developers.

11

Mortgages post-2007 Increases in defaults/arrears as job losses hit Borrowers could not remortgage because of declines in house values and tighter lending criteria Lenders could not get funding so tightened credit availability Rollbacks/elimination of innovative products

12

Gross new residential mortgage lending: 07 to 08

13

Government policies: Dealing with effects Developers Financial assistance to prevent bankruptcy and protect jobs Low interest rates help both Borrowers Help with mortgage payments Bans/limits on repossessions Sale/rent-back programs

14

The post-crisis period: 2009 onwards National experiences diverge Some countries (Ireland, Spain) still struggling Others show signs of recovery

still struggling Others show signs of recovery")

15

New residential mortgage lending late 2009 & late 2010

17

Changes in mortgage availability: market driven Australia: Subprime mortgages no longer offered UK: Lenders much more conservative— requiring higher down payments and documents verifying income Ireland, Spain: Lenders have tightened criteria Poland: Sharp change in domestic banks’ perception of exchange rate risk and credit risk for housing loans Portugal: Higher-risk loan types less available; LTVs down

18

What should governments do? Has the market self-corrected? (CML: yes) Is the answer better information? (Shiller: yes) Or do behavioural biases mean consumers should be protected from themselves?

Is the answer better information. (Shiller: yes) Or do behavioural biases mean consumers should be protected from themselves .")

19

National regulations in place Information Finland: Stress tests for borrowers at 6% interest rate, inform them about consequences of higher rates Poland: More information for borrowers in foreign currencies Lending practices Netherlands: Tighter rules on loan-to-income ratios Ireland: No loans to households in negative equity (subsequently loosened) Sweden: LTVs capped at 85% Poland: Increased collateral required for foreign- currency loans

Sweden: LTVs capped at 85% Poland: Increased collateral required for foreign- currency loans")

20

EU proposal: Directive on Credit Agreements Relating to Residential Property Information to be provided through examples & info sheets, but also in a ‘personalised manner’ Lenders should assess creditworthiness—member states invited to limit LTVs or LTIs Borrowers must be permitted to repay loans early, but lender may be entitled to ‘fair and objectively justified’ compensation Intermediaries & non-credit institutions to be licensed

21

Conclusions (1) Post-crisis developments depended on institutional and cultural factors in each country, as well as on global financial trends Mortgage lending is now growing again in most countries, especially eastern Europe, but continues to fall in some

Post-crisis developments depended on institutional and cultural factors in each country, as well as on global financial trends Mortgage lending is now growing again in most countries, especially eastern Europe, but continues to fall in some")

22

Conclusions (2) Lenders have become significantly more conservative in their lending practices Governments (national and EU) have become more interventionist. New regulations 1.Limit ‘risky’ product types and loan features 2.Require lenders to provide more information to consumers

23

What does it all mean for ‘sustainability’? For households More sustainable for those who do achieve home ownership--but at the cost of closing off options for others For lenders Limits downside risk; a forced return to more traditional models of housing finance.

Similar presentations