Download presentation

Presentation is loading. Please wait.

1

McGraw-Hill/Irwin1 25-1 © The McGraw-Hill Companies, Inc., 2006 Capital Budgeting and Managerial Decisions Chapter 25

2

McGraw-Hill/Irwin2 25-2 © The McGraw-Hill Companies, Inc., 2006 Capital budgeting: Analyzing alternative long- term investments and deciding which assets to acquire or sell. Outcome is uncertain. Large amounts of money are usually involved. Investment involves a long-term commitment. Decision may be difficult or impossible to reverse. Capital Budgeting

3

McGraw-Hill/Irwin3 25-3 © The McGraw-Hill Companies, Inc., 2006 Payback period = Cost of Investment Annual Net Cash Flow Payback Period The payback period of an investment is the time expected to recover the initial investment amount. Managers prefer investing in projects with shorter payback periods. Exh. 25-2

4

McGraw-Hill/Irwin4 25-4 © The McGraw-Hill Companies, Inc., 2006 FasTrac is considering buying a new machine that will be used in its manufacturing operations. The machine costs $16,000 and is expected to produce annual net cash flows of $4,100. The machine is expected to have an 8-year useful life with no salvage value. Calculate the payback period. Payback period = Cost of Investment Annual Net Cash Flow Payback period = $16,000 $4,100 = 3.9 years Payback Period with Even Cash Flows

5

McGraw-Hill/Irwin5 25-5 © The McGraw-Hill Companies, Inc., 2006 In the previous example, we assumed that the increase in cash flows would be the same each year. Now, let’s look at an example where the cash flows vary each year. $4,100 $5,000 Payback Period with Uneven Cash Flows

6

McGraw-Hill/Irwin6 25-6 © The McGraw-Hill Companies, Inc., 2006 FasTrac wants to install a machine that costs $16,000 and has an 8-year useful life with zero salvage value. Annual net cash flows are: Payback Period with Uneven Cash Flows Exh. 25-3

7

McGraw-Hill/Irwin7 25-7 © The McGraw-Hill Companies, Inc., 2006 4.2 We recover the $16,000 purchase price between years 4 and 5, about 4.2 years for the payback period. Payback Period with Uneven Cash Flows Exh. 25-3

8

McGraw-Hill/Irwin8 25-8 © The McGraw-Hill Companies, Inc., 2006 Ignores the time value of money. Ignores cash flows after the payback period. Unacceptable for projects with long lives where time value of money effects are major. Using the Payback Period

9

McGraw-Hill/Irwin9 25-9 © The McGraw-Hill Companies, Inc., 2006 Consider two projects, each with a five-year life and each costing $6,000. Would you invest in Project One just because it has a shorter payback period? Using the Payback Period

10

McGraw-Hill/Irwin10 25-10 © The McGraw-Hill Companies, Inc., 2006 The accounting rate of return focuses on annual income instead of cash flows. Accounting Rate of Return Accounting Annual after-tax net income rate of return Annual average investment = Beginning book value + Ending book value 2 Exh. 25-5,6

11

McGraw-Hill/Irwin11 25-11 © The McGraw-Hill Companies, Inc., 2006 Accounting Annual after-tax net income rate of return Annual average investment = Reconsider the $16,000 investment being considered by FasTrac. The annual after-tax net income is $2,100. Compute the accounting rate of return. Beginning book value + Ending book value 2 Accounting Rate of Return Exh. 25-5,6

12

McGraw-Hill/Irwin12 25-12 © The McGraw-Hill Companies, Inc., 2006 Accounting Annual after-tax net income rate of return Annual average investment = Reconsider the $16,000 investment being considered by FasTrac. The annual after-tax net income is $2,100. Compute the accounting rate of return. Accounting Rate of Return Beginning book value + Ending book value 2 Exh. 25-5,6

13

McGraw-Hill/Irwin13 25-13 © The McGraw-Hill Companies, Inc., 2006 Accounting $2,100 rate of return $8,000 == 26.25% $16,000 + $0 2 Accounting Rate of Return Reconsider the $16,000 investment being considered by FasTrac. The annual after-tax net income is $2,100. Compute the accounting rate of return. Exh. 25-5,6

14

McGraw-Hill/Irwin14 25-14 © The McGraw-Hill Companies, Inc., 2006 Depreciation may be calculated several ways. Income may vary from year to year. Time value of money is ignored. So why would I ever want to use this method anyway? Using Accounting Rate of Return

15

McGraw-Hill/Irwin15 25-15 © The McGraw-Hill Companies, Inc., 2006 Now let’s look at a capital budgeting model that considers the time value of cash flows. Net Present Value

16

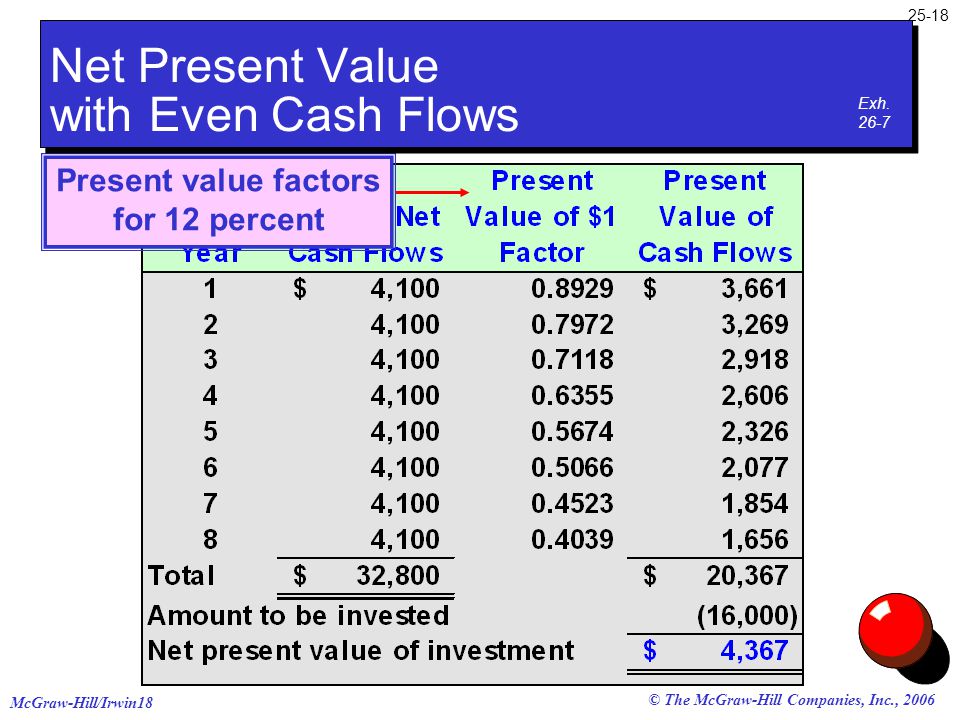

McGraw-Hill/Irwin16 25-16 © The McGraw-Hill Companies, Inc., 2006 Discount the future net cash flows from the investment at the required rate of return. Subtract the initial amount invested from sum of the discounted cash flows. FasTrac is considering the purchase of a conveyor costing $16,000 with an 8-year useful life with zero salvage value that promises annual net cash flows of $4,100. FasTrac requires a 12 percent compounded annual return on its investments. Net Present Value

17

McGraw-Hill/Irwin17 25-17 © The McGraw-Hill Companies, Inc., 2006 Net Present Value with Even Cash Flows Exh. 26-7

18

McGraw-Hill/Irwin18 25-18 © The McGraw-Hill Companies, Inc., 2006 Present value factors for 12 percent Net Present Value with Even Cash Flows Exh. 26-7

19

McGraw-Hill/Irwin19 25-19 © The McGraw-Hill Companies, Inc., 2006 A positive net present value indicates that this project earns more than 12 percent on the investment. Net Present Value with Even Cash Flows Exh. 26-7

20

McGraw-Hill/Irwin20 25-20 © The McGraw-Hill Companies, Inc., 2006 General decision rule... Using Net Present Value

21

McGraw-Hill/Irwin21 25-21 © The McGraw-Hill Companies, Inc., 2006 Although all projects require the same investment and have the same total net cash flows, project B has a higher net present value because of a larger net cash flow in year 1. Net Present Value with Uneven Cash Flows Exh. 26-8

22

McGraw-Hill/Irwin22 25-22 © The McGraw-Hill Companies, Inc., 2006 Internal Rate of Return (IRR) The interest rate that makes... Present value of cash inflows Present value of cash outflows = The net present value equal zero.

23

McGraw-Hill/Irwin23 25-23 © The McGraw-Hill Companies, Inc., 2006 Projects with even annual cash flows Project life = 3 years Initial cost = $12,000 Annual net cash inflows = $5,000 Determine the IRR for this project. 1. Compute present value factor. 2.Using present value of annuity table... Internal Rate of Return (IRR) Exh. 26-9

Exh")

24

McGraw-Hill/Irwin24 25-24 © The McGraw-Hill Companies, Inc., 2006 1. Compute present value factor. $12,000 ÷ $5,000 per year = 2.4000 2.Using present value of annuity table... Projects with even annual cash flows Internal Rate of Return (IRR) Exh. 26-9 Project life = 3 years Initial cost = $12,000 Annual net cash inflows = $5,000 Determine the IRR for this project.

Exh Project life = 3 years Initial cost = $12,000 Annual net cash inflows = $5,000 Determine the IRR for this project..")

25

McGraw-Hill/Irwin25 25-25 © The McGraw-Hill Companies, Inc., 2006 Locate the row whose number equals the periods in the project’s life. 1.Determine the present value factor. $12,000 ÷ $5,000 per year = 2.4000 2.Using present value of annuity table... Internal Rate of Return (IRR) Exh. 26-9

Exh")

26

McGraw-Hill/Irwin26 25-26 © The McGraw-Hill Companies, Inc., 2006 In that row, locate the interest factor closest in amount to the present value factor. 1.Determine the present value factor. $12,000 ÷ $5,000 per year = 2.4000 2.Using present value of annuity table... Internal Rate of Return (IRR) Exh. 26-9

Exh")

27

McGraw-Hill/Irwin27 25-27 © The McGraw-Hill Companies, Inc., 2006 1.Determine the present value factor. $12,000 ÷ $5,000 per year = 2.4000 2.Using present value of annuity table... IRR is the interest rate of the column in which the present value factor is found. IRR is approximately 12%. Internal Rate of Return (IRR) Exh. 26-9

Exh")

28

McGraw-Hill/Irwin28 25-28 © The McGraw-Hill Companies, Inc., 2006 If cash inflows are unequal, trial and error solution will result if present value tables are used. Sophisticated business calculators and electronic spreadsheets can be used to easily solve these problems. Internal Rate of Return – Uneven Cash Flows

29

McGraw-Hill/Irwin29 25-29 © The McGraw-Hill Companies, Inc., 2006 Internal Rate of Return l Compare the internal rate of return on a project to a predetermined hurdle rate (cost of capital). l To be acceptable, a project’s rate of return cannot be less than the cost of capital. Using Internal Rate of Return

30

McGraw-Hill/Irwin30 25-30 © The McGraw-Hill Companies, Inc., 2006 Exh. 25-10 Comparing Methods

31

McGraw-Hill/Irwin31 25-31 © The McGraw-Hill Companies, Inc., 2006 Let’s change topics. Managerial Decisions

32

McGraw-Hill/Irwin32 25-32 © The McGraw-Hill Companies, Inc., 2006 Decision making involves five steps: Define the problem. Identify alternatives. Collect relevant information on alternatives. Select the preferred alternative. Analyze decisions made. Decision Making Exh. 25-11

33

McGraw-Hill/Irwin33 25-33 © The McGraw-Hill Companies, Inc., 2006 Costs that are applicable to a particular decision. Costs that should have a bearing on which alternative a manager selects. Costs that are avoidable. Future costs that differ between alternatives. 1 2 Relevant Costs

34

McGraw-Hill/Irwin34 25-34 © The McGraw-Hill Companies, Inc., 2006 All costs incurred in the past that cannot be changed by any decision made now or in the future. Sunk costs should not be considered in decisions. All costs incurred in the past that cannot be changed by any decision made now or in the future. Sunk costs should not be considered in decisions. Classification by Relevance: Sunk Costs Example: You bought an automobile that cost $10,000 two years ago. The $10,000 cost is sunk because whether you drive it, park it, trade it, or sell it, you cannot change the $10,000 cost.

35

McGraw-Hill/Irwin35 25-35 © The McGraw-Hill Companies, Inc., 2006 Future outlays of cash associated with a particular decision. Example: Considering the decision to take a vacation or stay at home, you will have travel costs (out-of- pocket costs) only if you choose a vacation. Classification by Relevance: Out-of-Pocket Costs

only if you choose a vacation. Classification by Relevance: Out-of-Pocket Costs.")

36

McGraw-Hill/Irwin36 25-36 © The McGraw-Hill Companies, Inc., 2006 The potential benefit that is given up when one alternative is selected over another. Example: If you were not attending college, you could be earning $20,000 per year. Your opportunity cost of attending college for one year is $20,000. Classification by Relevance: Opportunity Costs

37

McGraw-Hill/Irwin37 25-37 © The McGraw-Hill Companies, Inc., 2006 We will now examine several different types of managerial decisions. Managerial Decision Tasks

38

McGraw-Hill/Irwin38 25-38 © The McGraw-Hill Companies, Inc., 2006 The decision to accept additional business should be based on incremental costs and incremental revenues. Incremental amounts are those that occur if the company decides to accept the new business. Accepting Additional Business

39

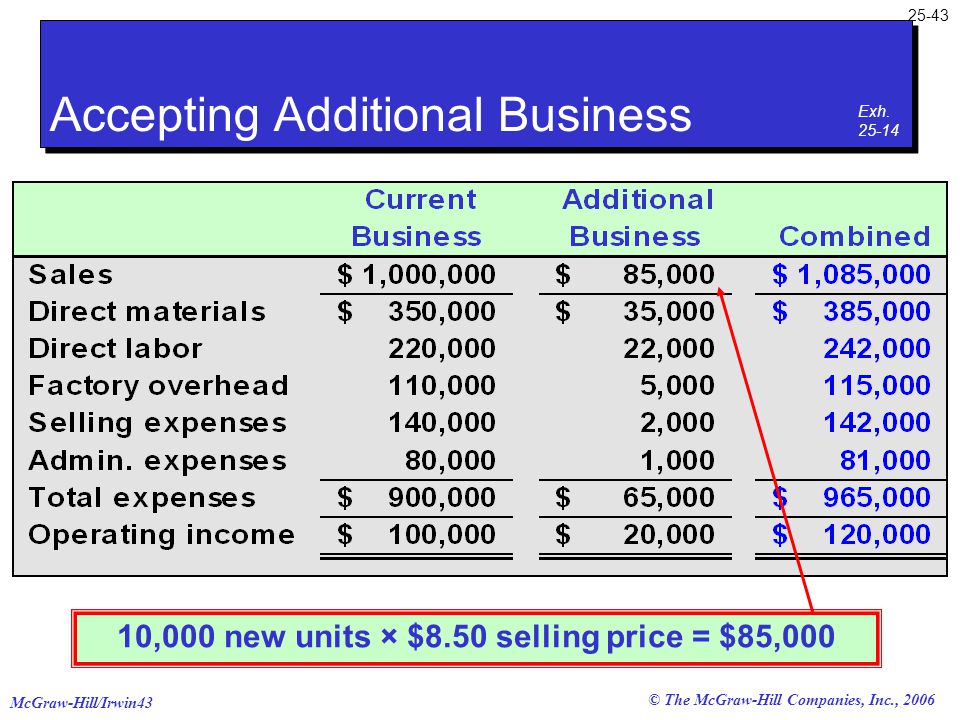

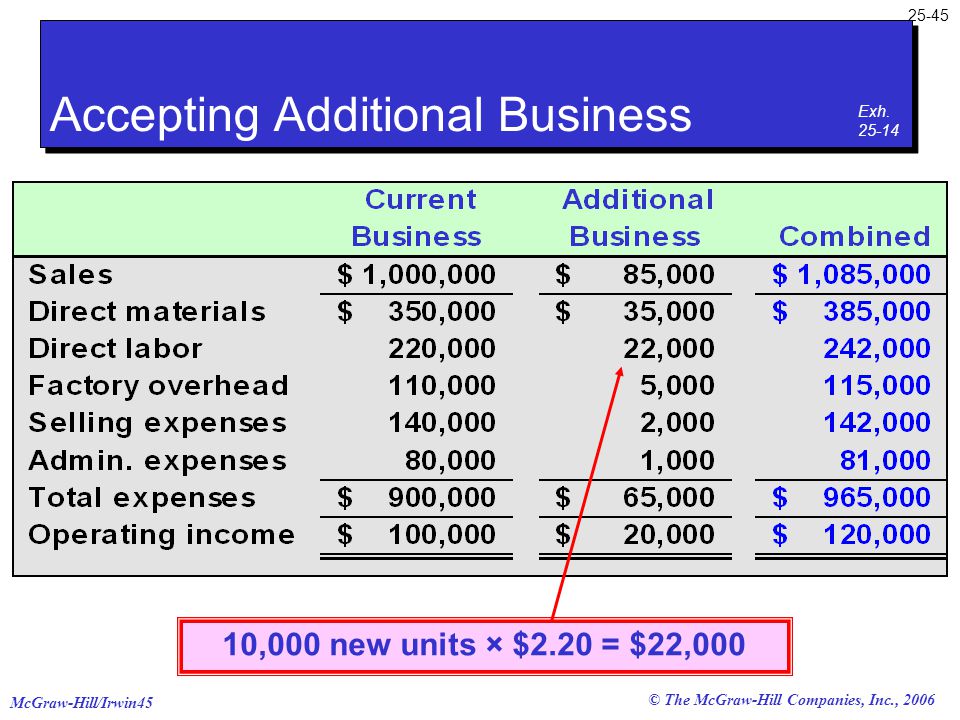

McGraw-Hill/Irwin39 25-39 © The McGraw-Hill Companies, Inc., 2006 FasTrac currently sells 100,000 units of its product. The company has revenue and costs as shown below: Accepting Additional Business Exh. 25-12

40

McGraw-Hill/Irwin40 25-40 © The McGraw-Hill Companies, Inc., 2006 FasTrac is approached by an overseas company that offers to purchase 10,000 units at $8.50 per unit. If FasTrac accepts the offer, total factory overhead will increase by $5,000; total selling expenses will increase by $2,000; and total administrative expenses will increase by $1,000. Should FasTrac accept the offer? Accepting Additional Business

41

McGraw-Hill/Irwin41 25-41 © The McGraw-Hill Companies, Inc., 2006 First let’s look at incorrect reasoning that leads to an incorrect decision. Our cost is $9.00 per unit. I can’t sell for $8.50 per unit. Accepting Additional Business

42

McGraw-Hill/Irwin42 25-42 © The McGraw-Hill Companies, Inc., 2006 This analysis leads to the correct decision. Accepting Additional Business Exh. 25-14

43

McGraw-Hill/Irwin43 25-43 © The McGraw-Hill Companies, Inc., 2006 10,000 new units × $8.50 selling price = $85,000 Accepting Additional Business Exh. 25-14

44

McGraw-Hill/Irwin44 25-44 © The McGraw-Hill Companies, Inc., 2006 10,000 new units × $3.50 = $35,000 Accepting Additional Business Exh. 25-14

45

McGraw-Hill/Irwin45 25-45 © The McGraw-Hill Companies, Inc., 2006 10,000 new units × $2.20 = $22,000 Accepting Additional Business Exh. 25-14

46

McGraw-Hill/Irwin46 25-46 © The McGraw-Hill Companies, Inc., 2006 Even though the $8.50 selling price is less than the normal $10 selling price, FasTrac should accept the offer because net income will increase by $20,000. Accepting Additional Business Exh. 25-14

47

McGraw-Hill/Irwin47 25-47 © The McGraw-Hill Companies, Inc., 2006 Incremental costs also are important in the decision to make a product or purchase it from a supplier. The cost to produce an item must include (1) direct materials, (2) direct labor and (3) incremental overhead. We should not use the predetermined overhead rate to determine product cost. Make or Buy Decisions

direct materials, (2) direct labor and (3) incremental overhead. We should not use the predetermined overhead rate to determine product cost. Make or Buy Decisions.")

48

McGraw-Hill/Irwin48 25-48 © The McGraw-Hill Companies, Inc., 2006 FasTrac currently makes part #417, assigning overhead at 100 percent of direct labor cost, with the following unit cost: Make or Buy Decisions

49

McGraw-Hill/Irwin49 25-49 © The McGraw-Hill Companies, Inc., 2006 FasTrac can buy part #417 from a supplier for $1.20. How much overhead do we have to eliminate before we can continue to make this part? Make or Buy Decisions Exh. 25-15

50

McGraw-Hill/Irwin50 25-50 © The McGraw-Hill Companies, Inc., 2006 FasTrac can buy part #417 from a supplier for $1.20. How much overhead do we have to eliminate before we can continue to make this part? We must eliminate $.25 per unit of overhead, leaving a maximum of $0.25 per unit. Make or Buy Decisions Exh. 25-15

51

McGraw-Hill/Irwin51 25-51 © The McGraw-Hill Companies, Inc., 2006 Costs incurred in manufacturing units of product that do not meet quality standards are sunk costs and cannot be recovered. As long as rework costs are recovered through sale of the product, and rework does not interfere with normal production, we should rework rather than scrap. Scrap or Rework

52

McGraw-Hill/Irwin52 25-52 © The McGraw-Hill Companies, Inc., 2006 FasTrac has 10,000 defective units that cost $1.00 each to make. The units can be scrapped now for $.40 each or reworked at an additional cost of $.80 per unit. If reworked, the units can be sold for the normal selling price of $1.50 each. Reworking the defective units will prevent the production of 10,000 new units that would also sell for $1.50. Should FasTrac scrap or rework? Scrap or Rework

53

McGraw-Hill/Irwin53 25-53 © The McGraw-Hill Companies, Inc., 2006 10,000 units × $1.50 per unit 10,000 units × $0.40 per unit Scrap or Rework Exh. 25-16

54

McGraw-Hill/Irwin54 25-54 © The McGraw-Hill Companies, Inc., 2006 10,000 units × $0.80 per unit 10,000 units × ($1.50 - $1.00) per unit Scrap or Rework Exh. 25-16

55

McGraw-Hill/Irwin55 25-55 © The McGraw-Hill Companies, Inc., 2006 FasTrac should scrap the units now. If FasTrac fails to include the opportunity cost, the rework option would show a return of $7,000, mistakenly making rework appear more favorable. Scrap or Rework Defects Exh. 25-16

56

McGraw-Hill/Irwin56 25-56 © The McGraw-Hill Companies, Inc., 2006 Businesses are often faced with the decision to sell partially completed products or to process them to completion., As a general rule, we process further only if incremental revenues exceed incremental costs. Sell or Process

57

McGraw-Hill/Irwin57 25-57 © The McGraw-Hill Companies, Inc., 2006 FasTrac has 40,000 units of partially finished product Q. Processing costs to date are $30,000. The 40,000 unfinished units can be sold as is for $50,000 or they can be processed further to produce finished products X, Y, and Z. The additional processing will cost $80,000 and result in the following revenues: Continue Sell or Process

58

McGraw-Hill/Irwin58 25-58 © The McGraw-Hill Companies, Inc., 2006 Should FasTrac sell product Q or continue processing into products X, Y, and Z? Sell or Process Exh. 25-17

59

McGraw-Hill/Irwin59 25-59 © The McGraw-Hill Companies, Inc., 2006 FasTrac should continue processing. Note that the earlier $30,000 cost for product Q is sunk and therefore irrelevant to the decision. Sell or Process Should FasTrac sell product Q or continue processing into products X, Y, and Z? Exh. 25-17,18

60

McGraw-Hill/Irwin60 25-60 © The McGraw-Hill Companies, Inc., 2006 When a company sells a variety of products, some are likely to be more profitable than others. To make an informed decision, management must consider... The contribution margin of each product, The facilities required to produce each product and any constraints on the facilities, and The demand for each product. Sales Mix Selection

61

McGraw-Hill/Irwin61 25-61 © The McGraw-Hill Companies, Inc., 2006 Consider the following data for two products made and sold by FasTrac. If each product requires the same time to make, and the demand is unlimited, FasTrac should produce only Product B. Sales Mix Selection Exh. 25-19

62

McGraw-Hill/Irwin62 25-62 © The McGraw-Hill Companies, Inc., 2006 Consider this additional information. Consider the following data for two products made and sold by FasTrac. Sales Mix Selection Exh. 25-19

63

McGraw-Hill/Irwin63 25-63 © The McGraw-Hill Companies, Inc., 2006 Consider the following data for two products made and sold by FasTrac. Product B has a greater contribution margin than Product A, but it requires more machine hours per unit to produce. With unlimited demand for A and B, produce as many units of A as possible since A provides more dollars per hour worked. Sales Mix Selection Exh. 25-19

64

McGraw-Hill/Irwin64 25-64 © The McGraw-Hill Companies, Inc., 2006 If demand for A is limited, produce to meet that demand, then use the remaining facilities to produce B. Consider the following data for two products made and sold by FasTrac. Sales Mix Selection Exh. 25-19

65

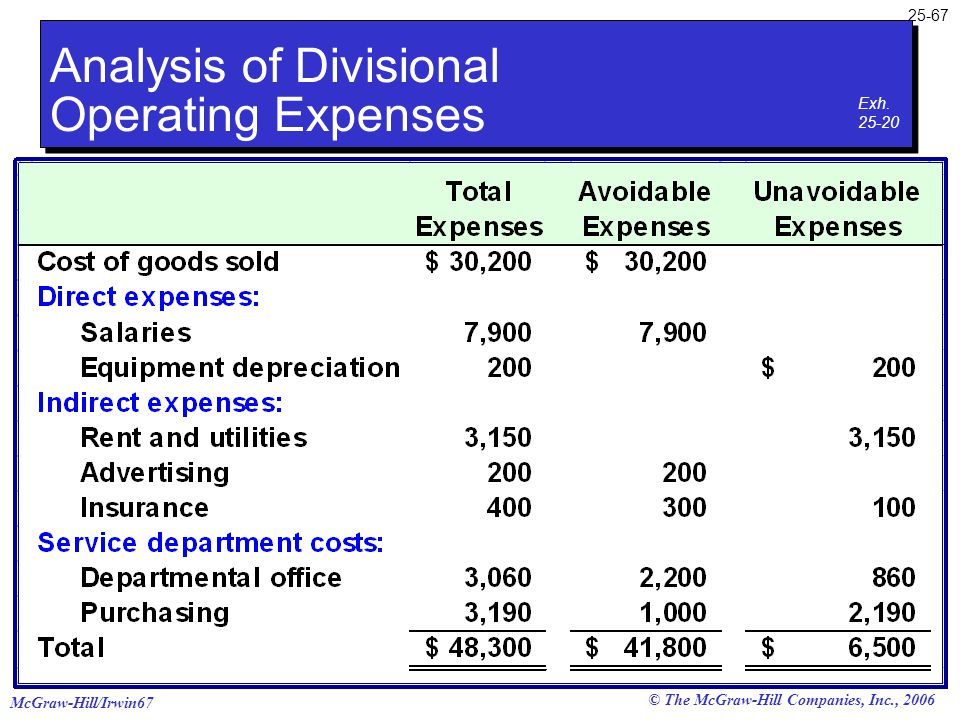

McGraw-Hill/Irwin65 25-65 © The McGraw-Hill Companies, Inc., 2006 FasTrac is considering eliminating its Treadmill Division because total expenses of $48,300 are greater than its sales of $47,800. A segment is a candidate for elimination if its revenues are less than its avoidable expenses. Continue Segment Elimination

66

McGraw-Hill/Irwin66 25-66 © The McGraw-Hill Companies, Inc., 2006 Let’s identify avoidable expenses. Analysis of Divisional Operating Expenses Exh. 25-20

67

McGraw-Hill/Irwin67 25-67 © The McGraw-Hill Companies, Inc., 2006 Analysis of Divisional Operating Expenses Exh. 25-20

68

McGraw-Hill/Irwin68 25-68 © The McGraw-Hill Companies, Inc., 2006 Do not eliminate the Treadmill Division! Segment Elimination

69

McGraw-Hill/Irwin69 25-69 © The McGraw-Hill Companies, Inc., 2006 Qualitative factors are involved in most all managerial decisions. For example: Quality. Delivery schedule. Supplier reputation. Employee morale. Customer opinions. Qualitative Factors in Decisions

70

McGraw-Hill/Irwin70 25-70 © The McGraw-Hill Companies, Inc., 2006 Homework for Chapter 25 Ex 25-2, 5, 7, 8, 9, 10, 11, Problem 1A, 5A,

71

McGraw-Hill/Irwin71 25-71 © The McGraw-Hill Companies, Inc., 2006 End of Chapter 25

Similar presentations