Download presentation

Presentation is loading. Please wait.

1

Project Selection Models

Nadeem Kureshi

2

Project Selection Project selection is the process of evaluating individual projects or groups of projects, and then choosing to implement some set of them so that the objectives of the parent organization will be achieved. The proper choice of investment projects is crucial to the long-run survival of every firm. Daily we witness the results of both good and bad investment choices.

3

Decision Models Models abstract the relevant issues about a problem from the plethora of detail in which the problem is embedded. Reality is far too complex to deal with in its entirety. This process of carving away the unwanted reality from the bones of a problem is called modeling the problem. The idealized version of the problem that results is called a model.

4

Models may be quite simple to understand, or they may be extremely complex. In general, introducing more reality into a model tends to make the model more difficult to manipulate.

5

Criteria for Project Selection Model

1. Realism 2. Capability 3. Flexibility 4. Ease of use 5. Cost 6. Easy computerization

6

Numeric and Non-Numeric Models

Both widely used, Many organizations use both at the same time, or they use models that are combinations of the two. Nonnumeric models, as the name implies, do not use numbers as inputs. Numeric models do, but the criteria being measured may be either objective or subjective. It is important to remember that: the qualities of a project may be represented by numbers, and that subjective measures are not necessarily less useful or reliable than objective measures.

7

Nonnumeric Models Nonnumeric models are older and simpler and have only a few subtypes to consider.

8

The Sacred Cow Suggested by a senior and powerful official in the organization. Often initiated with a simple comment such as, “If you have a chance, why don’t you look into . . .,” and there follows an undeveloped idea for a new product, for the development of a new market, for the design and adoption of a global data base and information system, or for some other project requiring an investment of the firm’s resources. “Sacred” in the sense that it will be maintained until successfully concluded, or until the boss, personally, recognizes the idea as a failure and terminates it.

9

The Operating Necessity

If a flood is threatening the plant, a project to build a protective dike does not require much formal evaluation, which is an example of this scenario. If the project is required in order to keep the system operating, the primary question becomes: Is the system worth saving at the estimated cost of the project?

10

The Competitive Necessity

The decision to undertake the project based on a desire to maintain the company’s competitive position in that market. Investment in an operating necessity project takes precedence over a competitive necessity project Both types of projects may bypass the more careful numeric analysis used for projects deemed to be less urgent or less important to the survival of the firm.

11

The Product Line Extension

A project to develop and distribute new products judged on the degree to which it fits the firm’s existing product line, fills a gap, strengthens a weak link, or extends the line in a new, desirable direction. Sometimes careful calculations of profitability are not required. Decision makers can act on their beliefs about what will be the likely impact on the total system performance if the new product is added to the line.

12

Comparative Benefit Model

Organization has many projects to consider but the projects do not seem to be easily comparable. For example, some projects concern potential new products, some concern changes in production methods, others concern computerization of certain records, and still others cover a variety of subjects not easily categorized (e.g., a proposal to create a daycare center for employees with small children). No precise way to define or measure “benefit.”

. No precise way to define or measure benefit.")

13

Q-Sort Method Of the several techniques for ordering projects, the Q-Sort is one of the most straightforward. First, the projects are divided into three groups—good, fair, and poor—according to their relative merits. If any group has more than eight members, it is subdivided into two categories, such as fair-plus and fair-minus. When all categories have eight or fewer members, the projects within each category are ordered from best to worst. Again, the order is determined on the basis of relative merit. The rater may use specific criteria to rank each project, or may simply use general overall judgment.

14

The Q-Sort Method

15

Numeric Models: Profit/Profitability

A large majority of all firms using project evaluation and selection models use profitability as the sole measure of acceptability.

16

Models Present & Future Value Benefit / Cost Ratio Payback period

Internal Rate of Return Annual Value Variations of IRR

17

Present Value The Present value or present worth method of evaluating projects is a widely used technique. The Present Value represents an amount of money at time zero representing the discounted cash flows for the project. PV T = 0 +/- Cash Flows

18

Net Present Value (NPV)

The Net Present Value of an investment it is simply the difference between cash outflows and cash inflows on a present value basis. In this context, the discount rate equals the minimum rate of return for the investment Where: NPV = ∑ Present Value (Cash Benefits) - ∑ Present Value (Cash Costs)

- ∑ Present Value (Cash Costs)")

19

Present Value Example Initial Investment: $100,000

Project Life: 10 years Salvage Value: $ 20,000 Annual Receipts: $ 40,000 Annual Disbursements: $ 22,000 Annual Discount Rate: 12%, 18% What is the net present value for this project? Is the project an acceptable investment?

20

Present Value Example Solution

Annual Receipts $40,000(P/A, 12%, 10) $ 226,000 Salvage Value $20,000(P/F, 12%, 10) $ 6,440 Annual Disbursements $22,000(P/A, 12%, 10) -$124,000 Initial Investment (t=0) -$100,000 Net Present Value $ 8,140 Greater than zero, therefore acceptable project

$ 226,000. Salvage Value. $20,000(P/F, 12%, 10) $ 6,440. Annual Disbursements. $22,000(P/A, 12%, 10) -$124,000. Initial Investment (t=0) -$100,000. Net Present Value $ 8,140. Greater than zero, therefore acceptable project.")

21

Future Value The future value method evaluates a project based upon the basis of how much money will be accumulated at some future point in time. This is just the reverse of the present value concept. FV T = 0 +/- Cash Flows

22

Future Value Example Initial Investment: $100,000

Project Life: 10 years Salvage Value: $ 20,000 Annual Receipts: $ 40,000 Annual Disbursements: $ 22,000 Annual Discount Rate: 12%, 18% What is the net future value for this project? Is the project an acceptable investment?

23

Future Value Example Solution

Annual Receipts $40,000(F/A, 12%, 10) $ 701,960 Salvage Value $20,000(year 10) $ 20,000 Annual Disbursements $22,000(F/A, 12%, 10) -$386,078 Initial Investment $100,000(F/P, 12%, 10) -$310,600 Net Future Value $ 25,280 Positive value, therefore acceptable project Can be used to compare with future value of other projects

$ 701,960. Salvage Value. $20,000(year 10) $ 20,000. Annual Disbursements. $22,000(F/A, 12%, 10) -$386,078. Initial Investment. $100,000(F/P, 12%, 10) -$310,600. Net Future Value $ 25,280. Positive value, therefore acceptable project. Can be used to compare with future value of other projects.")

24

PV/FV No theoretical difference if project is evaluated in present or future value PV of $ 25,282 $25,282(P/F, 12%, 10) $ 8,140 FV of $ 8,140 $8,140(F/P, 12%, 10) $ 25,280

$ 8,140. FV of $ 8,140. $8,140(F/P, 12%, 10) $ 25,280.")

25

Annual Value Sometimes it is more convenient to evaluate a project in terms of its annual value or cost. For example it may be easier to evaluate specific components of an investment or individual pieces of equipment based upon their annual costs as the data may be more readily available for analysis.

26

Annual Analysis Example

A new piece of equipment is being evaluated for purchase which will generate annual benefits in the amount of $10,000 for a 10 year period, with annual costs of $5,000. The initial cost of the machine is $40,000 and the expected salvage is $2,000 at the end of 10 years. What is the net annual worth if interest on invested capital is 10%?

27

Annual Example Solution

Benefits: $10,000 per year $10,000 Salvage $2,000(P/F, 10%, 10)(A/P, 10%,10) $ Costs: $5,000 per year -$ 5,000 Investment: $40,000(A/P, 10%, 10) -$ 6,508 Net Annual Value -$1,383 Since this is less than zero, the project is expected to earn less than the acceptable rate of 10%, therefore the project should be rejected.

(A/P, 10%,10) $ 125. Costs: $5,000 per year -$ 5,000. Investment: $40,000(A/P, 10%, 10) -$ 6,508. Net Annual Value -$1,383. Since this is less than zero, the project is expected to earn less than the acceptable rate of 10%, therefore the project should be rejected.")

28

Benefit/Cost Ratio The benefit/cost ratio is also called the profitability index and is defined as the ratio of the sum of the present value of future benefits to the sum of the present value of the future capital expenditures and costs.

29

B/C Ratio Example Project A Project B Present value cash inflows

$500, $100,000 Present value cash outflows $300, $ 50,000 Net Present Value $200, $ 50,000 Benefit/Cost Ratio

30

Payback Period One of the most common evaluation criteria used.

Simply the number of years required for the cash income from a project to return the initial cash investment. The investment decision criteria for this technique suggests that if the calculated payback period is less than some maximum value acceptable to the company, the proposal is accepted. Example illustrates five investment proposals having identical capital investment requirements but differing expected annual cash flows and lives.

31

Payback Period

32

Example Calculation of the payback period for a given investment proposal. Prepare End of Year Cumulative Net Cash Flows Find the First Non-Negative Year Calculate How Much of that year is required to cover the previous period negative balance Add up Previous Negative Cash Flow Years a b c) = 10,500/13,500 d)

0.78 = 10,500/13,500. d)")

33

Example: Calculate the payback period for the following investment proposal

34

Example: Calculate the payback period for the following investment proposal

35

Example: Calculate the payback period for the following investment proposal

36

Example: Calculate the payback period for the following investment proposal

37

Example: Calculate the payback period for the following investment proposal

38

Example: Calculate the payback period for the following investment proposal

39

IRR & Discount Rates

40

Internal Rate of Return

Internal Rate of Return refers to the interest rate that the investor will receive on the investment principal IRR is defined as that interest rate (r) which equates the sum of the present value of cash inflows with the sum of the present value of cash outflows for a project. This is the same as defining the IRR as that rate which satisfies each of the following expressions: ∑ PV cash inflows - ∑ PV cash outflows = 0 NPV = 0 for r ∑ PV cash inflows = ∑ PV cash outflows In general, the calculation procedure involves a trial-and-error solution. The following examples illustrate the calculation procedures for determining the internal rate of return.

which equates the sum of the present value of cash inflows with the sum of the present value of cash outflows for a project. This is the same as defining the IRR as that rate which satisfies each of the following expressions: ∑ PV cash inflows - ∑ PV cash outflows = 0. NPV = 0 for r. ∑ PV cash inflows = ∑ PV cash outflows. In general, the calculation procedure involves a trial-and-error solution. The following examples illustrate the calculation procedures for determining the internal rate of return.")

41

Example Given an investment project having the following annual cash flows; find the IRR. Solution: Step 1. Pick an interest rate and solve for the NPV. Try r =15% NPV = -30(1.0) -1(P/F,1,15%) + 5(P/F,2,15) + 5.5(P/F,3,15) + 4(P/F,4,15) + 17(P/F,5,15) + 20(P/F,6,15) + 20(P/F,7,15) - 2(P/F,8,15) + 10(P/F,9,15) = + $5.62 Since the NPV>0, 15% is not the IRR. It now becomes necessary to select a higher interest rate in order to reduce the NPV value. Step 2. If r =20% is used, the NPV = - $ 1.66 and therefore this rate is too high. Step 3. By interpolation the correct value for the IRR is determined to be r =18.7%

-1(P/F,1,15%) + 5(P/F,2,15) + 5.5(P/F,3,15) + 4(P/F,4,15) + 17(P/F,5,15) + 20(P/F,6,15) + 20(P/F,7,15) - 2(P/F,8,15) + 10(P/F,9,15) = + $5.62. Since the NPV>0, 15% is not the IRR. It now becomes necessary to select a higher interest rate in order to reduce the NPV value. Step 2. If r =20% is used, the NPV = - $ 1.66 and therefore this rate is too high. Step 3. By interpolation the correct value for the IRR is determined to be r =18.7%")

42

IRR using Excel Using Excel you should insert the following function in the targeted cell C6:

43

Analysis The acceptance or rejection of a project based on the IRR criterion is made by comparing the calculated rate with the required rate of return, or cutoff rate established by the firm. If the IRR exceeds the required rate the project should be accepted; if not, it should be rejected. If the required rate of return is the return investors expect the organization to earn on new projects, then accepting a project with an IRR greater than the required rate should result in an increase of the firms value.

44

Analysis There are several reasons for the widespread popularity of the IRR as an evaluation criterion: Perhaps the primary advantage offered by the technique is that it provides a single figure which can be used as a measure of project value. Furthermore, IRR is expressed as a percentage value. Most managers and engineers prefer to think of economic decisions in terms of percentages as compared with absolute values provided by present, future, and annual value calculations.

45

Analysis Another advantage offered by the IRR method is related to the calculation procedure itself: As its name suggests, the IRR is determined internally for each project and is a function of the magnitude and timing of the cash flows. Some evaluators find this superior to selecting a rate prior to calculation of the criterion, such as in the profitability index and the present, future, and annual value determinations. In other words, the IRR eliminates the need to have an external interest rate supplied for calculation purposes.

46

Selecting a Discount Rate

“There is nothing so disastrous as a rational investment policy in an irrational world” John Maynard Keynes We have discussed the time value of money and illustrated several examples of its use. In all cases an interest rate or “discount rate” is used to bring the future cash flows to the present (NPV - Net Present Value) The selection of the appropriate discount rate has been the source of considerable debate and much disagreement. In most companies, the selection of the discount rate is determined by the accounting department or the board of directors and the engineer just uses the number provided to him, but short of just being provided with a rate, what is the correct or appropriate rate to use?

The selection of the appropriate discount rate has been the source of considerable debate and much disagreement. In most companies, the selection of the discount rate is determined by the accounting department or the board of directors and the engineer just uses the number provided to him, but short of just being provided with a rate, what is the correct or appropriate rate to use")

47

Example IRR What is the impact of the discount rate on the investment?

Cash Flow Yr 0 Cash Flow Yr 1 Cash Flow Yr 2 Cash Flow Yr 3 Cash Flow Yr 4 Cash Flow Yr 5 -500 +750 +600 +800 +1000 ROR NPV 2% 1,941 6% 1,581 10% 1,283 15% 981 20% 739 IRR 47.82%

48

Real Option Model Recently, a project selection model was developed based on a notion well known in financial markets. When one invests, one foregoes the value of alternative future investments. Economists refer to the value of an opportunity foregone as the “opportunity cost” of the investment made. The argument is that a project may have greater net present value if delayed to the future. If the investment can be delayed, its cost is discounted compared to a present investment of the same amount. Further, if the investment in a project is delayed, its value may increase (or decrease) with the passage of time because some of the uncertainties will be reduced. If the value of the project drops, it may fail the selection process. If the value increases, the investor gets a higher payoff. The real options approach acts to reduce both technological and commercial risk.

with the passage of time because some of the uncertainties will be reduced. If the value of the project drops, it may fail the selection process. If the value increases, the investor gets a higher payoff. The real options approach acts to reduce both technological and commercial risk.")

49

Numeric Models: Scoring

In an attempt to overcome some of the disadvantages of profitability models, particularly their focus on a single decision criterion, a number of evaluation/selection models hat use multiple criteria to evaluate a project have been developed. Such models vary widely in their complexity and information requirements. The examples discussed illustrate some of the different types of numeric scoring models.

50

Some factors to consider

51

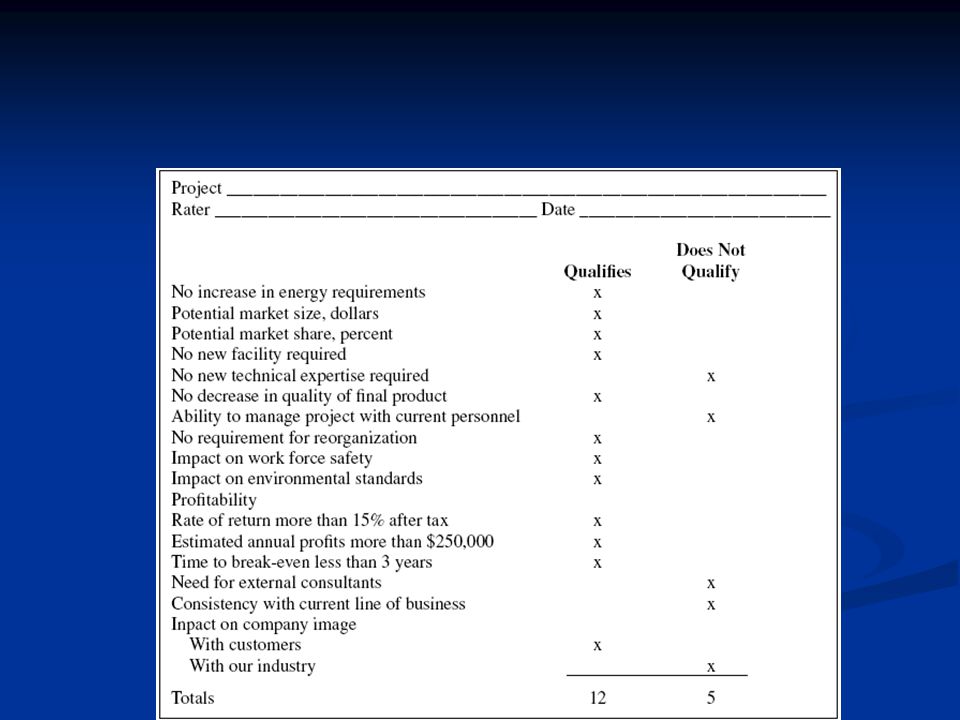

Unweighted 0–1 Factor Model

A set of relevant factors is selected by management and then usually listed in a preprinted form. One or more raters score the project on each factor, depending on whether or not it qualifies for an individual criterion. The raters are chosen by senior managers, for the most part from the rolls of senior management. The criteria for choice are: (1) a clear understanding of organizational goals (2) a good knowledge of the firm’s potential project portfolio. Next slide: The columns are summed, projects with a sufficient number of qualifying factors may be selected. Advantage: It uses several criteria in the decision process. Disadvantage: It assumes all criteria are of equal importance and it allows for no gradation of the degree to which a specific project meets the various criteria.

a clear understanding of organizational goals. (2) a good knowledge of the firm’s potential project portfolio. Next slide: The columns are summed, projects with a sufficient number of qualifying factors may be selected. Advantage: It uses several criteria in the decision process. Disadvantage: It assumes all criteria are of equal importance and it allows for no gradation of the degree to which a specific project meets the various criteria.")

53

Unweighted Factor Scoring Model

X marks in 0-1 scoring model are replaced by numbers, from a 5 point scale.

54

Weighted Factor Scoring Model

When numeric weights reflecting the relative importance of each individual factor are added, we have a weighted factor scoring model. In general, it takes the form where Si the total score of the ith project, Sij the score of the ith project on the jth criterion, and Wj the weight of the jth criterion.

55

Constrained Weighted Factor Scoring Model

Additional criteria enter the model as constraints rather than weighted factors. These constraints represent project characteristics that must be present or absent in order for the project to be acceptable. We might have specified that we would not undertake any project that would significantly lower the quality of the final product (visible to the buyer or not). We would amend the weighted scoring model to take the form: where Cik 1 if the i th project satisfies the Kth constraint, and 0 if it does not.

. We would amend the weighted scoring model to take the form: where Cik 1 if the i th project satisfies the Kth constraint, and 0 if it does not.")

56

Example: P & G practice Would not consider a project to add a new consumer product or product line: that cannot be marketed nationally; that cannot be distributed through mass outlets (grocery stores, drugstores); that will not generate gross revenues in excess of $—million; for which Procter & Gamble’s potential market share is not at least 50 percent; and that does not utilize Procter & Gamble’s scientific expertise, manufacturing expertise, advertising expertise, or packaging and distribution expertise.

; that will not generate gross revenues in excess of $—million; for which Procter & Gamble’s potential market share is not at least 50 percent; and that does not utilize Procter & Gamble’s scientific expertise, manufacturing expertise, advertising expertise, or packaging and distribution expertise.")

57

Final Thought Selecting the type of model to aid the evaluation/selection process depends on the philosophy and wishes of management. Weighted scoring models preferred for three fundamental reasons. they allow the multiple objectives of all organizations to be reflected in the important decision about which projects will be supported and which will be rejected. scoring models are easily adapted to changes in managerial philosophy or changes in the environment. they do not suffer from the bias toward the short run that is inherent in profitability models that discount future cash flows.

58

ACTIVITY Exercise – Project Selection Approximate Time: 30 minutes

Similar presentations