Download presentation

Presentation is loading. Please wait.

1

OECD Pension Fund Portfolio Allocation www.kapital-plus.net mr.sc. Tomislav Petrov

2

Introduction There is a growing need among regulatory and policy community to compare program developments and experiences to those of other countries. The availability of an comparable and up-to-date body of international statistics is a necessary tool for policy-makers, regulators and market participants, so we make OECD indicators user-friendly for the public.

3

Supervision of pension funds in Croatia One mission of HANFA is the protection of the pension fund members interests. Their assets must be adequately safeguarded from undue loss. In Croatia, as in Mexico, Poland and Slovak Republic, funded pension plans are distributed to retail investors without the intermediation of employers.

4

Types of pension plans: defined benefit and defined contribution Defined contribution plan: –Employee and/or employer contributions are based on percent of salary into individual account. The pension is a function of the contributions that have been made. –Employee bears the risk if investment returns are insufficient. The cost to the employer is fixed. Defined benefit plan: –Benefits are usually based on years of service and salary level. –Sponsor or sponsor and beneficiaries bear investment risk. The employer retains a risk that they will not be enough to pay the pensions. –Measurement of assets and liabilities determine contribution and benefit rates.

5

The on-going shift from defined benefit to defined contribution The shift from defined benefit to defined contribution pension plans is a phenomenon spread throughout most of the OECD countries. Defined benefit is complex and not attractive. The pension fund in the Czech Republic, Hungary, Italy, Poland, Portugal, the Slovak Republic and Spain are all largely or solely supporting defined contribution arrangements. When comparing the data it is therefore important that users be aware of the institutional differences between countries.

6

Structure of assets of pension funds Cash and Deposits Bills and Bonds issued by public administration Corporate Bonds Loans Shares Land and Buildings Mutual Funds (CIS) Unallocated insurance contracts Other investments

Unallocated insurance contracts Other investments")

7

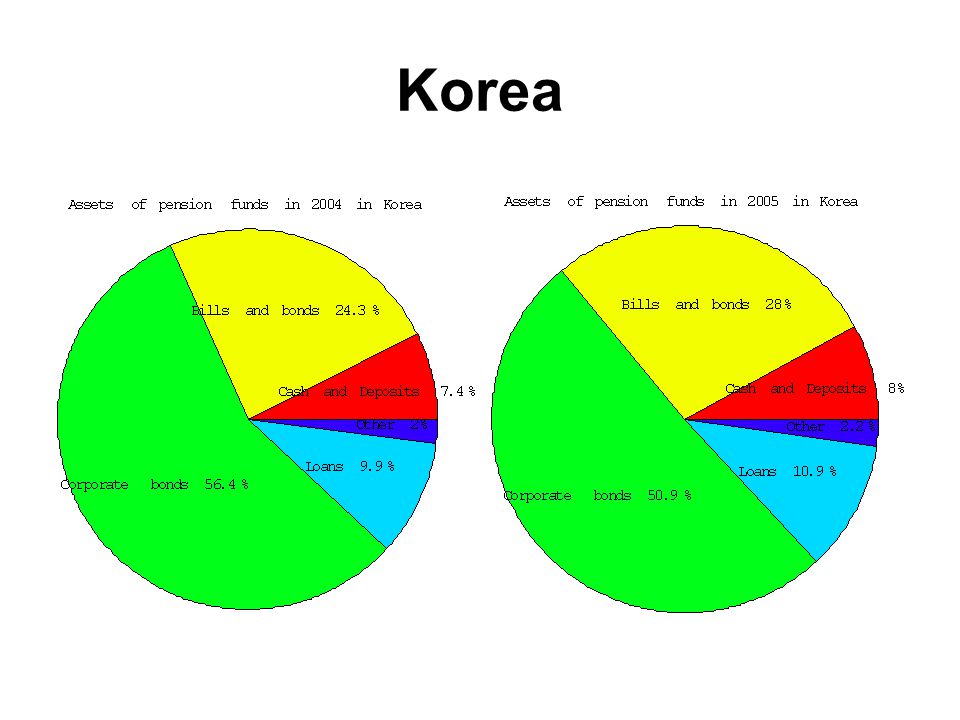

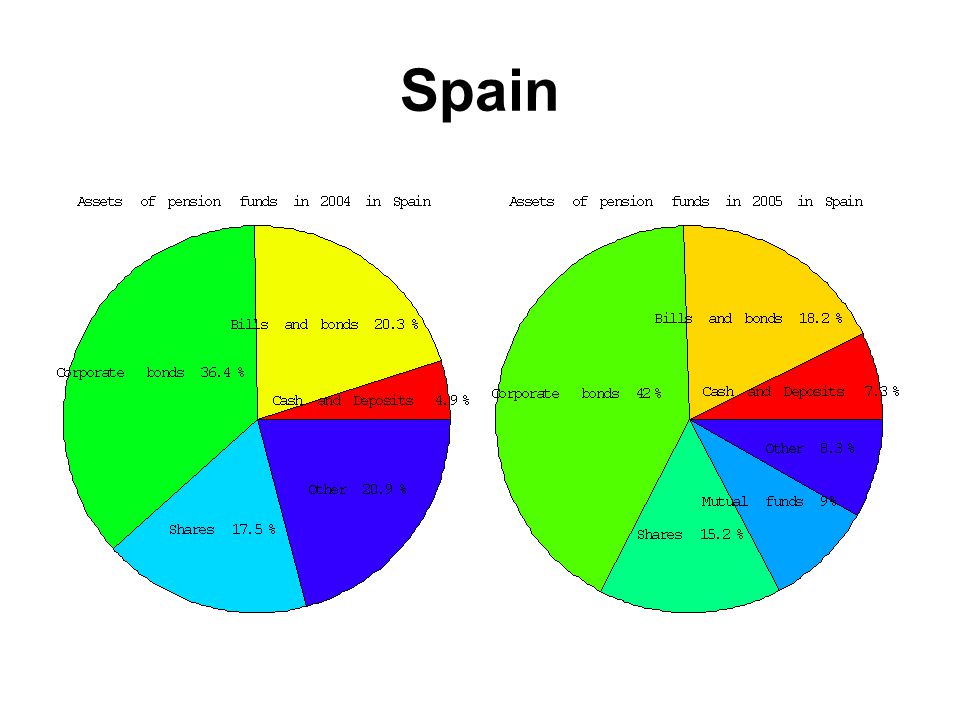

Structure of assets varies across countries Cash and Deposits account for more then 40% of the total assets in Indonesia, Brazil and Thailand, and 15.3% in Slovenia. Bills and Bonds issued by public administration account for over one half of total investments in Singapore, Mexico, Turkey, Hungary, France, Poland, Czech Republic and Bulgaria. Corporate bonds account for over 30% of the total assets in Korea, Spain, Slovenia, Netherlands, Norway and Germany.

8

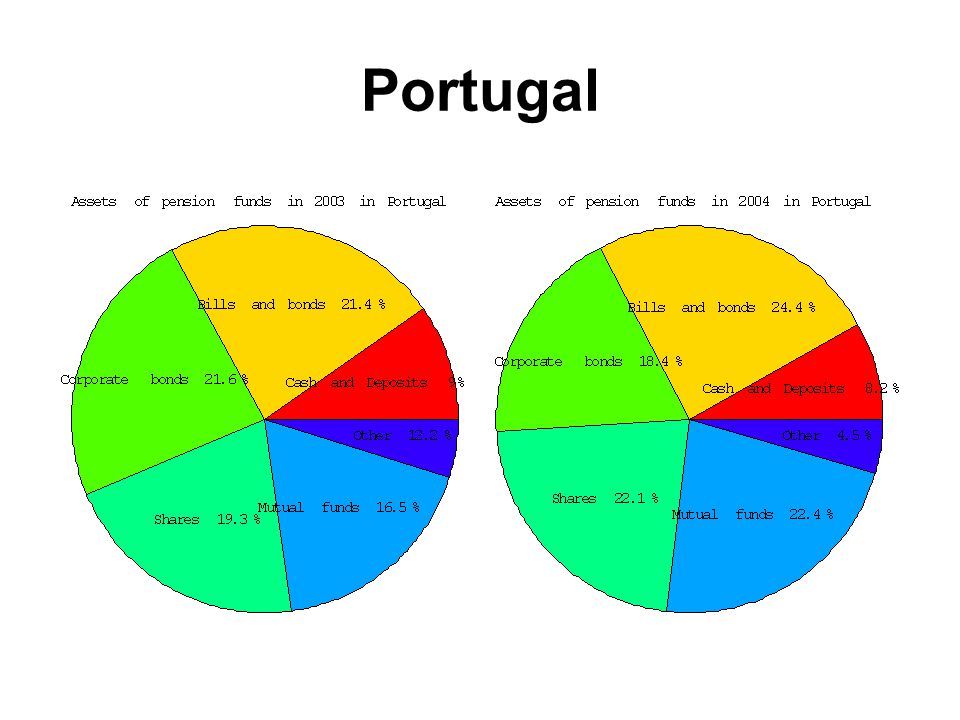

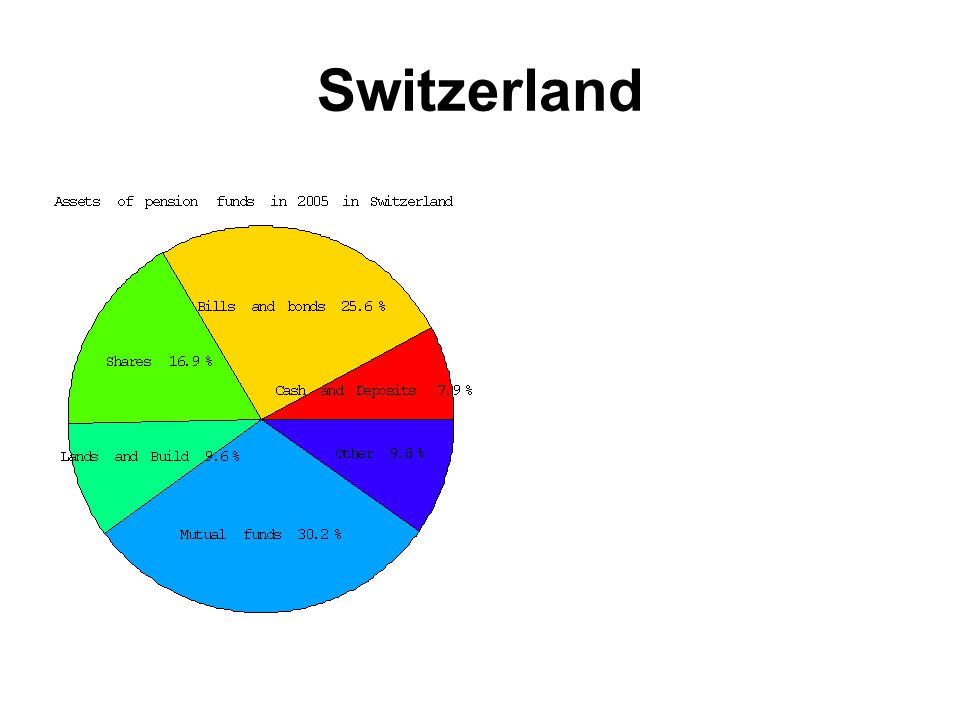

Structure of assets varies across countries Loans account for over 25% of the total assets in Germany. Shares account for over 30% of the total assets in Netherlands, United States, Finland, United Kingdom, Estonia, Austria, Germany, Iceland and Poland. Real estate account almost 10% of the total assets in Switzerland, Portugal, Italy and Finland. Mutual funds account for over 65% of the total assets in Belgium and Australia, and over 30% of the total assets in Canada, Switzerland, France and United States.

9

Asset allocation trends A move towards greater international diversification of pension fund portfolios (over 50%) and strategic shift towards a greater share of high-quality long-term bonds (demographic developments have downward pressure on long-term interest rates with maturity of ten years or longer) was observed. Growing allocations into bonds in countries with high equity investment, into shares in countries with high investments into fixed income securities and general shift towards alternative investments was observed.

10

Australia

11

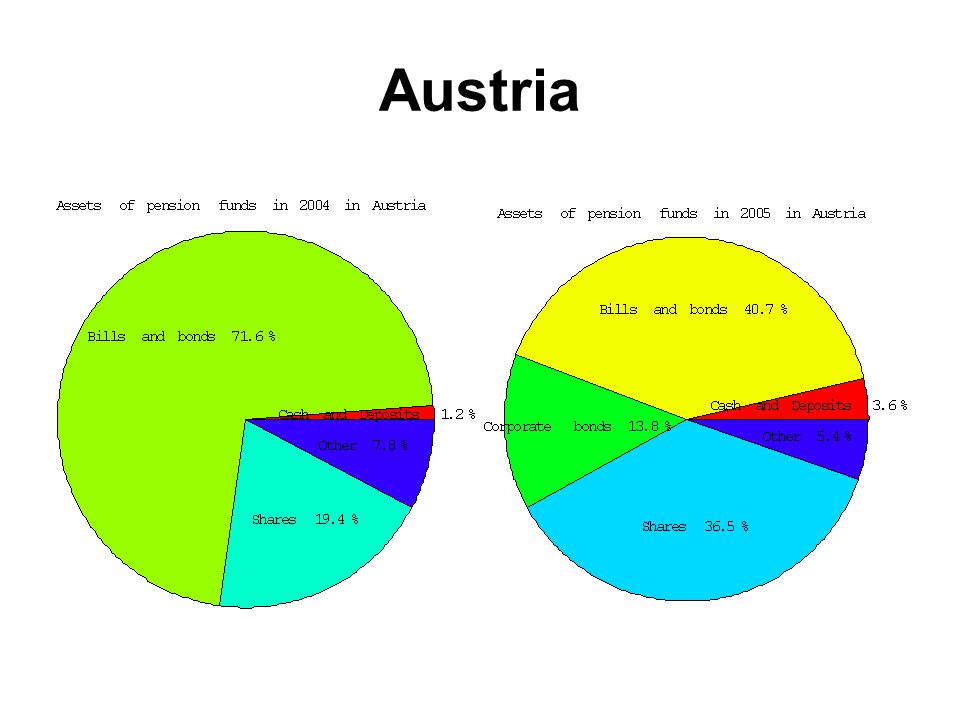

Austria

14

Belgium

16

Brazil

17

Bulgaria

20

Canada

22

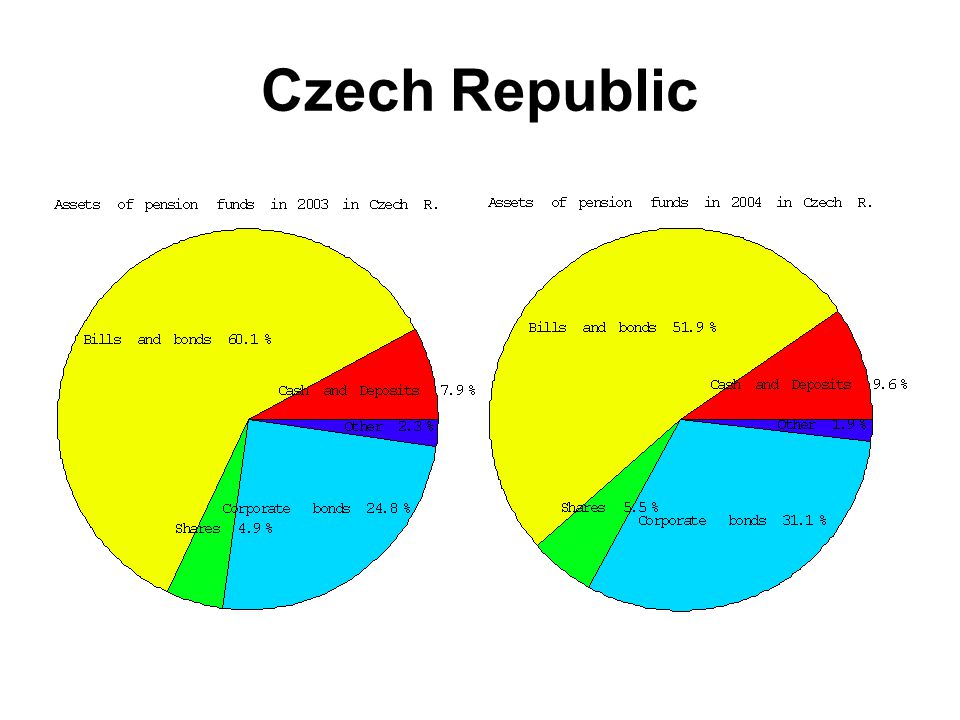

Czech Republic

25

Denmark

28

Estonia

31

Finland

33

Germany

36

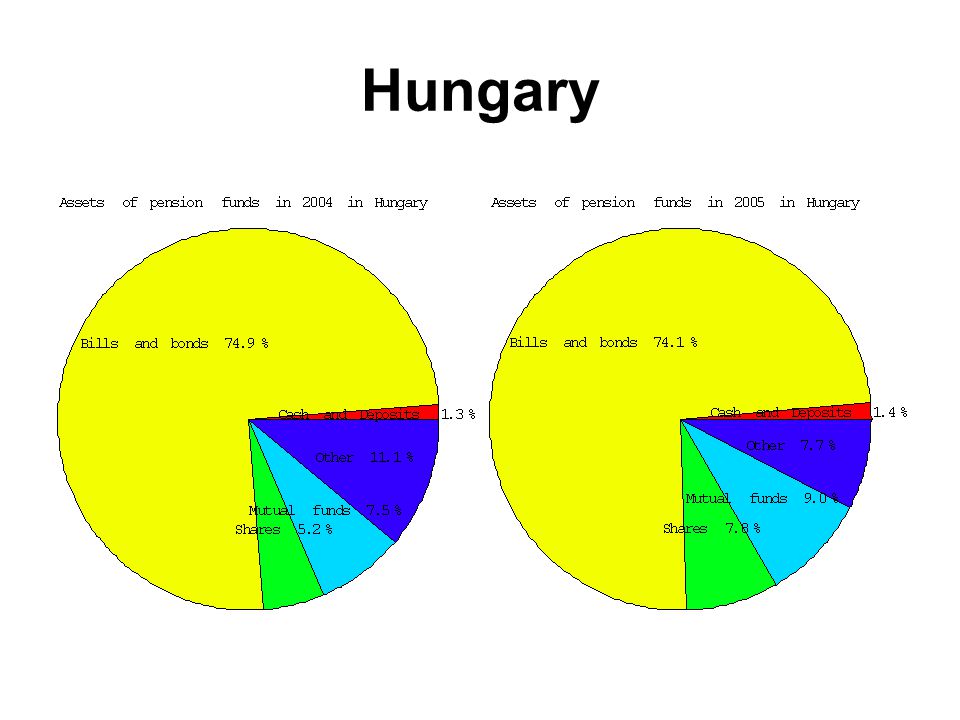

Hungary

38

Iceland

41

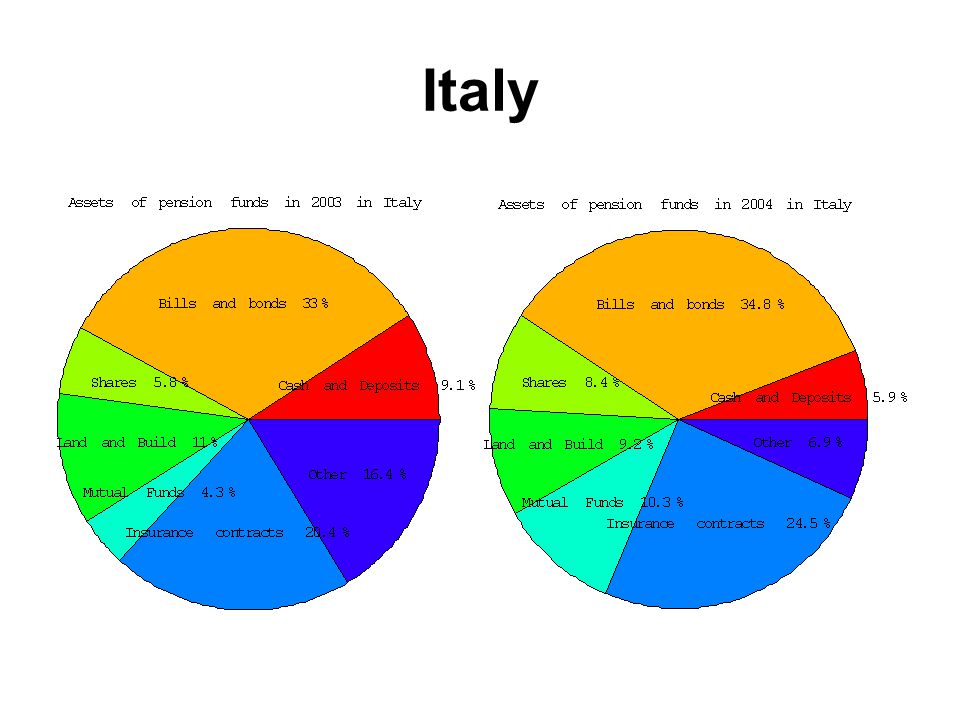

Italy

44

Korea

47

Mexico

49

Netherlands

51

Norway

53

Poland

56

Portugal

59

Slovak Republic

60

Slovenia

62

Spain

65

Switzerland

67

Turkey

68

United Kingdom

70

United States

73

Return on pension fund assets Country20032004 Australia11.9%11.3% Belgium8.6%8.9% Bulgaria11.4% Hungary3.3%16.5% Mexico10.4%6.7%

74

Guard against insolvency Pension Protection Fund is introduced to charge a risk-based levy to pension funds in United Kingdom. Pension Benefit Guarantee Corporation responsibilities are similar in United States.

75

Guard against insolvency Additional protection measures for pension benefits are insolvency guarantee schemes and priority creditor rights. Pension benefit guarantee schemes are insurance type arrangements, with premiums paid by pension funds, which takes on outstanding pension obligations which cannot be met by the insolvent plan sponsor. Priority creditor rights should be given to unpaid and due contributions and care should be taken that pension beneficiaries be treated at least as well as other creditors in any bankruptcy or restructuring process (e.g. ensuring their representation on creditor committees).

..")

76

Pension funds total investments as a share of GDP and as a share of market capitalization www.kapital-plus.net mr.sc. Tomislav Petrov

77

Total investments of pension funds (as a percent of GDP) OECD Countries2001200220032004 Australia57.758.156.172.7 Canada (1)53.347.852.1 Denmark27.225.627.630.0 Iceland 86.487.6101.9111.9 Ireland (4)44.335.139.442.6 Japan (5)13.914.115.314.2 Netherlands (1)107.089.4106.2 Switzerland (1) (8)104.496.7111.6 United Kingdom (1) (9)72.5 65.1 United States (10)93.982.092.095.0

OECD Countries Australia Canada (1) Denmark Iceland Ireland (4) Japan (5) Netherlands (1) Switzerland (1) (8) United Kingdom (1) (9) United States (10)")

78

Total investments of pension funds (as a percent of GDP) OECD Countries2001200220032004 Austria 3.9 4.24.5 Czech Republic2.32.83.13.6 Germany3.33.43.63.8 Hungary4.04.65.46.8 Italy 2.32.42.52.6 Mexico 4.35.25.86.3 Poland 2.54.05.57.0 Slovak Republic (1)10.716.622.7 Spain (6)5.85.76.29.0

OECD Countries Austria Czech Republic Germany Hungary Italy Mexico Poland Slovak Republic (1) Spain (6)")

79

Pension fund assets growth Countries that have started from a relatively small base are experiencing fast growth in pension fund assets.

80

Pension fund cash flow Pension fund cash flow is the difference between revenues and expenditures. Revenue is a primarily composed of contributions, profits on the sale of investments and dividends and interest. Expenditures consist of pension payments and losses on the sale of investments. Cash flow = [Total contributions + Net investments income + Other income] - [Benefits + Operational expenses + Other expenses]

81

OECD contacts jean-marc.salou@oecd.org, the Global Pension Statistics Project manager in the Financial Affairs Divisionjean-marc.salou@oecd.org www.iopsweb.org, the International Organization of Pension Supervisors (IOPS) have projects in risk-based supervision, education and training.www.iopsweb.org OECD-IOPS Global Forum on Private Pensions, Istanbul, Turkey, Dec. 2006

Similar presentations