Download presentation

Presentation is loading. Please wait.

1

1 John Hinners Assistant V.P. Industry Relations U.S. Meat Export Federation Global Beef Trade Outlook and Opportunities Oklahoma Cattlemen’s Association 7/29/06

2

History & Mission USMEF was formally organized in 1976 and is a non-profit trade association working to create new opportunities for beef, lamb and pork. USMEF’s mission has evolved over the years and is “to increase the value and profitability of the U.S. beef, pork and lamb industries by enhancing demand for their products in targeted export markets through a dynamic partnership of all stakeholders”.

3

U.S. Meat Export Federation Offices – 100 Employees Taipei Singapore Guangzhou Denver Mexico City Sao Paulo Moscow London Beirut Osaka Tokyo Seoul Monterrey St. Petersburg Caracas Hong Kong Shanghai

4

World Population Growth Historical Projected Double 1980 by 2050

5

Who are our international customers? Here’s what the World looks like in a village of 100 people with all existing human ratios remaining the same. What we look like, believe, own and how we live: 57 Asians, 21 Europeans, 14 from the Western Hemisphere - both North & South and 8 Africans 32 would speak a Chinese dialect 82 would be non-white, 18 would be white

6

Who are our Customers? 68 would be non-Christian, 32 would be Christian 32% of the village’s wealth would be in the hands of 5 people - all from the USA 80 would live in substandard housing 17 would be unable to read and write 50 would suffer from malnutrition 20 earn <$1 / day; 50 earn <$2 /day 33 would be without a safe water supply 1 would have a college education 7 would have access to the internet

7

Affordable Food Percentage of Disposable Income Spent on Food* U.S.- 10% U.K. - 11.2% Mexico - 24% India – 50%+ Sources: USDA/ERS, "The Public Image of America's Farmers," American Farm Bureau Federation, 2002

8

Relevance of Trade to U.S. Livestock Industries Can indirect trade issues impact U.S. beef producers?

9

Relevance of Trade to U.S. Livestock Industries On March 10, 2002 Russia banned U.S. poultry keeping 53 million pounds per week in the U.S. Did this have anything to do to the cattle market?

10

June LC Contract - 2002 On March 10, 2002 Russia banned U.S. poultry keeping 53 million pounds per week in the U.S. Source: Chicago Mercantile Exchange web site

11

Is meat consumption in the U.S. at a saturation point?

12

Exports have been a growth market for U.S. Red Meats Rest of World 234% U.S. 63%

13

Future Global Beef Demand FAO Beef Consumption Estimates Source: FAO +22% +44% % change from base year 13 million mt every 15 years

14

Globalization Globalization is increasing – livestock sector Investment and finance Retail expansion into developing markets is increasing global trade –Wal-Mart; in 2006 the world’s #1 retailer will open 230 new international stores –going from 50 to 70 outlets in China by the end of 2006 This globalization benefits our competitors as well

15

The New Era of Better Informed Consumers Consumers, both domestic and international are demanding assurances of food safety In addition to safety, consumers want to know where the product was produced, who produced it and is it fresh

16

Global Trends – New Realities Information is the cost of admission Plate to Gate, not Gate to Plate –Market is being driven by consumers, not producers Increase in branding at retail level

17

Global Trends - “New Realities” World protein complex is dealing with the dual shocks of BSE and AI Consumers are becoming increasingly concerned about food safety. Brands/traceability are becoming more important. Competition for export markets is intensifying. FTA’s are enhancing long-term market prospects.

18

Global Trends - Brands Natural Brands Store Brands Private Brands

19

The Brand Promise Randy Blach, CattleFax, Branded beef products (not even counting store brands) account for about 10% of annual fed-cattle production, and he expects it to grow significantly by the end of the decade. Source: BEEF, January 2005

20

Global Trends - “Story Meat” Voluntary Marketing Tool Shows Producer, Farm and Cattle Let’s Consumers Know Someone Stands Behind Products

21

Store Brands Becoming the Norm Branding will grow because a brand represents a promise of quality A tremendous amount of marketing and dollars will be placed behind a brand A brand can build customer loyalty & repeat buyers

22

22 U.S. Beef Exports What has been lost and when do we resume exports?

23

12/24/03 Bans on U.S. Beef Begin

24

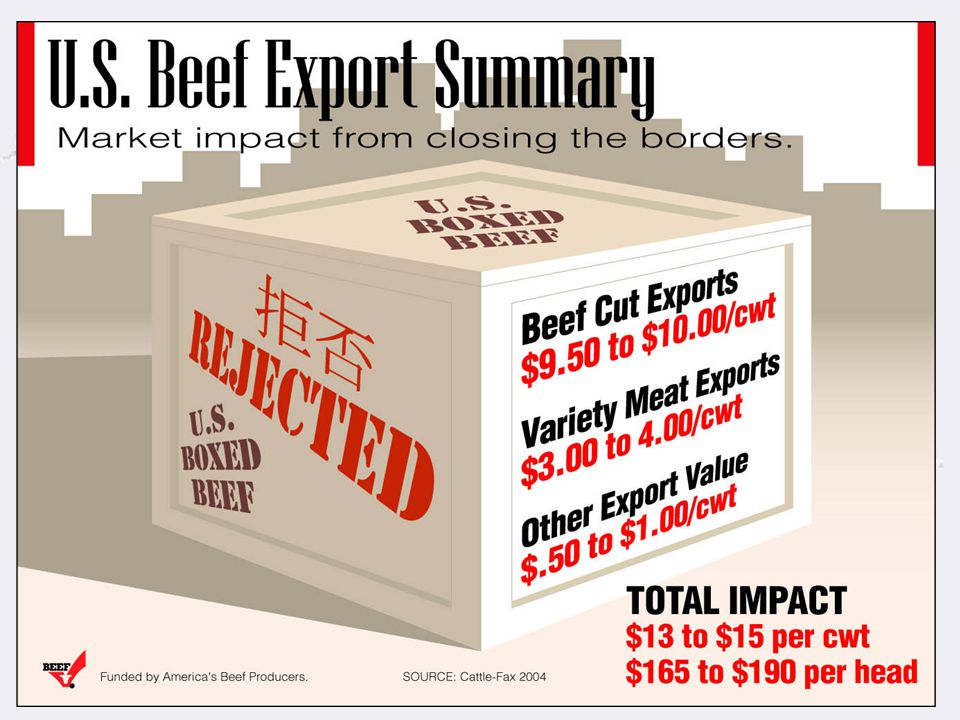

Beef Exports Beef and beef variety meats exports in 2003 represented –1.2 million MT with value of $3.5 billion –9% of all muscle cuts –47% of all variety meats 90,000 MT of livers 27,000 MT of tongues The equivalent of 3.5 million head of cattle (roughly 60,000 head per week)

")

26

Beef Export Premiums Export premiums on these 5 cuts alone represent $78 per head Source: USMEF

28

What’s the Current Status 133 countries imported U.S. beef between 1999-2003. 72 instituted bans in December 2003. –26 markets currently closed to U.S. beef. –Of those that have reopened, access has often limited. –6 markets accounted for 90% of ’03 exports and 2 remain closed. U.S. Beef & BVM Exports (1,000 MT’s)

.")

29

7/27/07 Japan lifts ban on U.S. beef imports! Japan U.S. beef/bvm exports of 384K mt worth $1.4 billion in 2003 64% of beef consumed is imported – half was U.S. Beef is 4 th protein source behind Fish, Pork, Poultry

31

Winning back consumers around the world More And More Consumers Give U.S. Beef Thumbs Up Online tracking surveys were conducted May 5-7 to update consumer reaction toward U.S. beef import resumption, safety and purchase intention. The survey showed 34 percent (up 3.2 percent from the last survey) of respondents support trade resumption. Approximately 18.5 percent would purchase U.S. beef. The results are higher than those from April.

of respondents support trade resumption. Approximately 18.5 percent would purchase U.S. beef. The results are higher than those from April..")

32

Putting U.S. Beef Back On the World’s Market

33

Where Do We Go From Here? To compete globally: Focus on U.S. advantages: –Diversity, flexibility of programs, grain-fed Aggressively pursue trade and competition Embrace trade enhancing policies “Export-minded” mentality

34

How Well We Cooperate Will Determine How Well We Compete !

35

Questions?

Similar presentations

13 th Annual Farmer Cooperatives Convention December 6-7, 2010 Economic.>")