Download presentation

Presentation is loading. Please wait.

1

Session 3

2

Learning objectives After completing this you will have an understanding of 1. Financial derivatives 2. Foreign currency futures 3. Foreign currency options 4. Foreign currency options pricing and valuation

3

1. Foreign Currency Derivatives used for two very distinct management objectives: Speculation – use of derivative instruments to take a position in the expectation of a profit Hedging – use of derivative instruments to reduce the risks associated with the everyday management of corporate cash flow

4

Foreign Currency Derivatives individual benefits: Permit firms to achieve payoffs Hedge risks Make underlying markets more efficient Reduce volatility of stock returns Minimise earnings volatility Reduce tax liabilities Motivate management (agency theory effect)

")

5

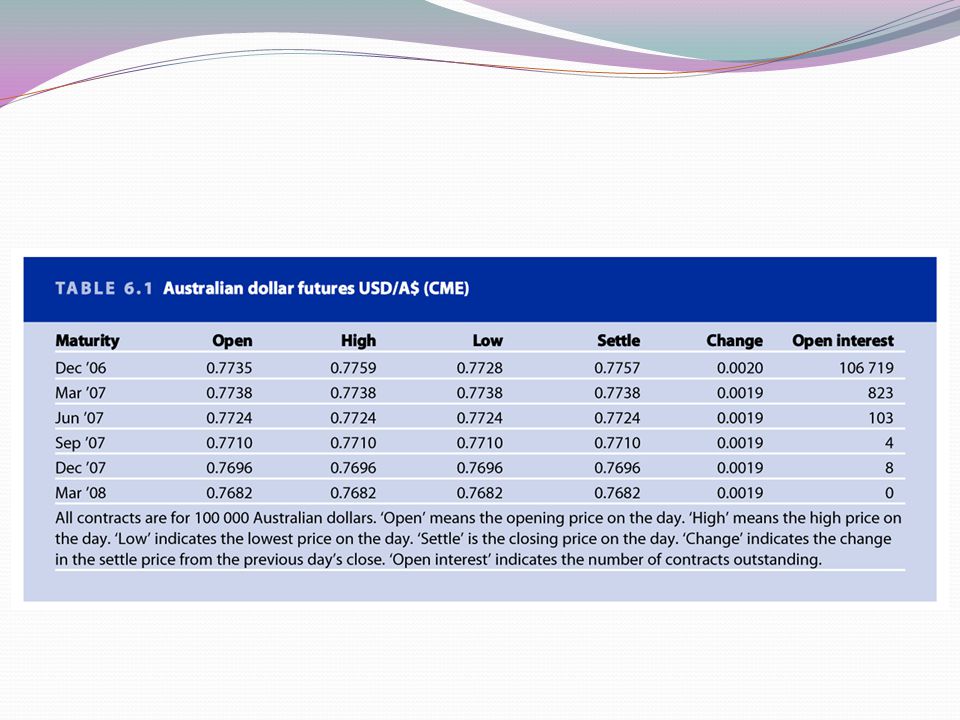

2. Foreign Currency Futures future delivery of a standard amount of foreign exchange at a fixed time, place and price. similar to futures contracts that exist for commodities such as cattle, lumber, interest-bearing deposits, gold, etc. the International Monetary Market (IMM), a division of the Chicago Mercantile Exchange (CME).

, a division of the Chicago Mercantile Exchange (CME)..")

7

Foreign Currency Futures features Contract size Method of stating exchange rates Maturity date Last trading day Collateral and maintenance margins Settlement Commissions Use of a clearinghouse as a counterparty

8

Foreign Currency Futures Foreign currency futures contracts differ from forward contracts terms of size Maturity Place of trading initial margin delivery

9

Table 6.2

10

3. Foreign Cur Options contract giving the option purchaser (the buyer) the right, but not the obligationor, to buy sell a given amount of foreign exchange at a fixed price per unit for a specified time period (until the maturity date). There are two basic types of options, puts and calls. A call is an option to buy foreign currency A put is an option to sell foreign currency

the right, but not the obligationor, to buy sell a given amount of foreign exchange at a fixed price per unit for a specified time period (until the maturity date). There are two basic types of options, puts and calls. A call is an option to buy foreign currency A put is an option to sell foreign currency.")

11

Foreign Currency Options The buyer –holder The seller - writer or grantor. Three different price elements: The exercise or strike price The premium The underlying or actual spot exchange rate in the market

12

Foreign Currency Options An American option gives the buyer the right to exercise the option at any time between the date of writing and the expiration or maturity date. A European option can be exercised only on its expiration date, not before. The premium, or option price, is the cost of the option.

13

Foreign Currency Options – concepts at-the-money (ATM). in-the-money (ITM). out-of-the money (OTM)

. in-the-money (ITM). out-of-the money (OTM)")

14

Foreign Currency Options Traded over-the-counter (OTC) organised exchanges are standardised

organised exchanges are standardised")

16

Foreign Currency Speculation profit by trading on expectations about prices in the future. Speculators can attempt to profit in the: Spot market Forward market Options markets

17

Option Market Speculation Buyer of a call: Assume purchase of November call option on Australian dollar with strike price of 76 (US$0.7600/A$), and a premium of US$0.0101/A$ At all spot rates below the strike price of 0.7600, the purchaser of the option would choose not to exercise because it would be cheaper to purchase A$ on the open market At all spot rates above the strike price, the option purchaser would exercise the option, purchase A$ at the strike price and sell them into the market netting a profit (less the option premium)

, and a premium of US$0.0101/A$ At all spot rates below the strike price of , the purchaser of the option would choose not to exercise because it would be cheaper to purchase A$ on the open market At all spot rates above the strike price, the option purchaser would exercise the option, purchase A$ at the strike price and sell them into the market netting a profit (less the option premium)")

19

Option Market Speculation Writer of a call: What the holder, or buyer of an option loses, the writer gains The maximum profit that the writer of the call option can make is limited to the premium If the writer wrote the option naked, that is without owning the currency, the writer would now have to buy the currency at the spot and take the loss delivering at the strike price The amount of such a loss is unlimited and increases as the underlying currency rises Even if the writer already owns the currency, the writer will experience an opportunity loss

20

Figure 6.2

21

Option Market Speculation Buyer of a Put: The basic terms of this example are similar to those just illustrated with the call The buyer of a put option, however, wants to be able to sell the underlying currency at the exercise price when the market price of that currency drops (not rises as in the case of the call option) If the spot price drops to US$0.7400/A$, the buyer of the put will deliver A$ to the writer and receive US$0.7600/A$ At any exchange rate above the strike price of 0.7600, the buyer of the put would not exercise the option, and would lose only the US$0.0020/A$ premium The buyer of a put (like the buyer of the call) can never lose more than the premium paid up front

If the spot price drops to US$0.7400/A$, the buyer of the put will deliver A$ to the writer and receive US$0.7600/A$ At any exchange rate above the strike price of , the buyer of the put would not exercise the option, and would lose only the US$0.0020/A$ premium The buyer of a put (like the buyer of the call) can never lose more than the premium paid up front")

22

Figure 6.3

23

Option Market Speculation Seller (writer) of a put: In this case, if the spot price of A$ drops below US$0.7600 per A$, the option will be exercised Below a price of US$0.7580 per A$, the writer will lose more than the premium received for writing the option (falling below break-even) If the spot price is above US$0.7600/A$, the option will not be exercised and the option writer will pocket the entire premium

of a put: In this case, if the spot price of A$ drops below US$ per A$, the option will be exercised Below a price of US$ per A$, the writer will lose more than the premium received for writing the option (falling below break-even) If the spot price is above US$0.7600/A$, the option will not be exercised and the option writer will pocket the entire premium")

24

Figure 6.4

25

Option Pricing and Valuation six elements: Present spot rate Time to maturity Forward rate for matching maturity Domestic interest rate Foreign currency interest rate Volatility (standard deviation of daily spot price movements)

")

Similar presentations

. 2 Agenda How forex futures quoted & used for speculation? Futures vs. forwards? How forex options are quoted?>")

>")

>")