Download presentation

Presentation is loading. Please wait.

1

Supply and Demand: Price and Quantity Determination in Competitive Markets The Economics Department, UMR Presents:

2

u Demand u Supply u Equilibrium and Disequilibrium Starring

3

Featuring u The Law of Demand u D = D(PENTE) u The Tendency of Supply u S = S(PENT) u Equilibrium/Disequilibrium

u The Tendency of Supply u S = S(PENT) u Equilibrium/Disequilibrium")

4

In Three Parts DemandSupplyEquilibrium/Disequilibrium

5

What is Demand? u It is the relationship between quantity demanded and price, c.p., within a specific period u Or, it is the relationship between the maximum willingness to pay in return for something of value Part 1

6

Individual vs. Market Demand u Market demand is the horizontal sum of individual demands u It is market demand that commands our interest

7

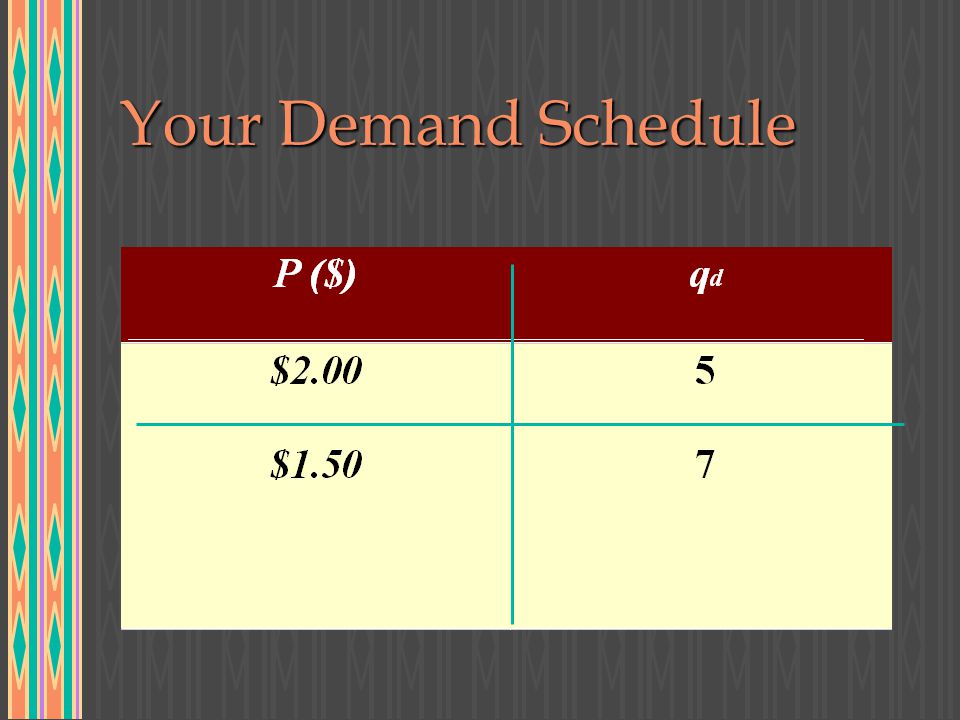

But Start with Individual Demand u Consider your demand for peanuts per semester (This is called “Quantity Demanded, q d ”) u We will first look at this information in a table called a “Demand Schedule”

u We will first look at this information in a table called a Demand Schedule")

8

Your Demand Schedule Demand Schedule - a table showing the relationship between the price of a good and the quantity demanded per period of time, ceteris paribus. Peanuts are measured in pounds.

9

Your Demand Schedule

11

10

12

Law of Demand u The price (willingness to pay) of a product, service, or activity is inversely related to the quantity demanded, ceteris paribus. u Applies to Market Demand (but notice your demand for peanuts obeyed the law)

.")

13

Demand Schedules and Curves u Demand Curve - a graph of the demand schedule showing the relationship between the price of a good and the quantity demanded per period of time, ceteris paribus.

14

Individual Demand Curve P($) q d per semester Note: ALWAYS label your axes!

q d per semester Note: ALWAYS label your axes!")

15

Individual Demand Curve P($) q d per semester 0.50 1.00 1.50 2.00 0 51015

q d per semester")

16

Individual Demand Curve P($) q d per semester 0.50 1.00 1.50 2.00 0 51015 A

q d per semester A")

17

Individual Demand Curve P($) q d per semester 0.50 1.00 1.50 2.00 0 51015 A B 7

q d per semester A B 7")

18

Individual Demand Curve P($) q d per semester 0.50 1.00 1.50 2.00 0 51015 A B C 7

q d per semester A B C 7")

19

Individual Demand Curve P($) q d per semester 0.50 1.00 1.50 2.00 0 5101515 A B C d 7

q d per semester A B C d 7")

20

Market Demand Curve u The demand curve we just drew was the Demand for Peanuts by one person. u We want an aggregate measure of the price, quantity demanded relationship--a market demand

21

Two Views of Demand u WTP - Maximum willingness to pay for a given unit of a good (marginal WTP) or for a number of units of a good u The Law of Demand - P, Q d relationship

or for a number of units of a good u The Law of Demand - P, Q d relationship")

22

WTP and the Law of Demand P Q d /t D $2.00 15 $1.50 23 The max. WTP for the 23rd unit is $1.50. The quantity demanded at $2.00 is 15 units per period

23

Market Demand Schedule u Market Demand Schedule - a table showing the relationship between the price of a good and the total quantity demanded by all consumers in the market per period of time, ceteris paribus.

24

Market Demand Schedule u Market Demand is obtained by summing horizontally the quantity demanded by each person at each price

25

Market Demand Schedule

29

Demand Curve P Q d /t D $15 8 $10 15 $5 22 Note: the linear demand is used for convenience

30

Change in D vs. Change in Q d u Change in Demand - a change in a factor that effects demand other than the price of the good, thus there is a change in quantity demanded at EVERY price. u Change in Quantity Demanded - a movement along a given demand curve- due only to a change in the price of the good itself

31

Change in Demand u Increase in demand - demand curve shifts to the right (or up - an increase in WTP) u Decrease in demand - demand curve shifts to the left (or down - a decrease in WTP )

u Decrease in demand - demand curve shifts to the left (or down - a decrease in WTP )")

32

Increase in Demand P Q d /t D D’

33

Increase in Q d P($) D A B Q d /t

D A B Q d /t")

34

Behind the Demand Curve u A demand curve is drawn under the assumption of ceteris paribus - all other important factors remaining unchanged u Factors to be considered may be remembered by D = D(PINTE)

")

35

Factors affecting market demand, PINTE u P = Prices u I = income u N = number of buyers u T = tastes or preferences u E = expectations about future prices and market conditions

36

P rice of Other Goods u The price of substitutes u The price of complements

37

P rice of Substitutes u What would happen to the demand for Peanuts if the price of pretzels fell? v The demand for Peanuts would probably fall since people would buy pretzels instead. u There is a positive relationship between the demand for a good and the price of its substitutes

38

P rice of Substitutes u Thus an increase in the price of a substitute will increase the demand for the good u And a decrease in the price of a substitute will decrease the demand for the good

39

P rice of Complements u Complementary goods are goods used together u What if the price of beer goes up? What ought to happen to the demand for Peanuts? v It ought to go down, since people want beer to drink with Peanuts. If the price of beer rises, the demand for Peanuts will fall.

40

P rice of Complements u Thus an increase in the price of a complement will decrease the demand for the good u And a decrease in the price of a complement will increase the demand for the good

41

P rice of Other Goods - Summary u Thus, either of the following will increase Demand Price of a substitute good increases Price of a substitute good increases Price of a complement good decreases Price of a complement good decreases u And either of the following will decrease Demand Price of a substitute good decreases Price of a substitute good decreases Price of a complement good increases Price of a complement good increases

42

I ncome I ncome u For most goods there is a positive relationship between income and demand. These are defined as normal goods. u For inferior goods, there is an inverse relationship between income and demand.

43

Normal and Inferior Goods u Are Peanuts a normal good? Are they for you? If they are, upon graduation and a higher salary you would buy more peanuts. u The question is empirical - how do people react?

44

Normal and Inferior Goods u What about Spam? Is the relationship between income and demand positive or negative, c.p.? u Cheaper food products are examples of inferior goods

45

N umber of Buyers u A positive relationship - the greater the number of buyers, the larger the total quantity demanded of the good at a given price. Demand increases, or the demand curve shifts to the right. u Likewise, if there are fewer buyers in the market there is less quantity demanded at every price, so demand has decreased.

46

T astes and Preferences u If we find out Peanuts improves our attractiveness to others, our willingness to pay for Peanuts would increase (an upward shift of the demand curve) u If we find out Peanuts are unhealthy the demand for the good decreases (a leftward shift of the curve)

u If we find out Peanuts are unhealthy the demand for the good decreases (a leftward shift of the curve)")

47

E xpectations u If we were to hear a new story about how Peanut prices were going to go up would you stock up? u If you expect your employer to begin downsizing would you reduce your demand for goods now?

48

Demand Reminders u Demand curves downward and to the right. u Changes in only the price of a good cause changes in the quantity demanded. u The only demand factor that cannot cause a change in the demand of a good is a change in its own price. u PINTE factors may alone or jointly change the demand for a good.

49

The End Continue to: Supply

Similar presentations