Download presentation

Presentation is loading. Please wait.

1

E5-26A: Cost-Method Consolidation for Majority- Owned Subsidiary Brett Bronenkamp Haoyi Du Stephen Jones Kevin McCarthy Alicia Rackers

2

Calculations

3

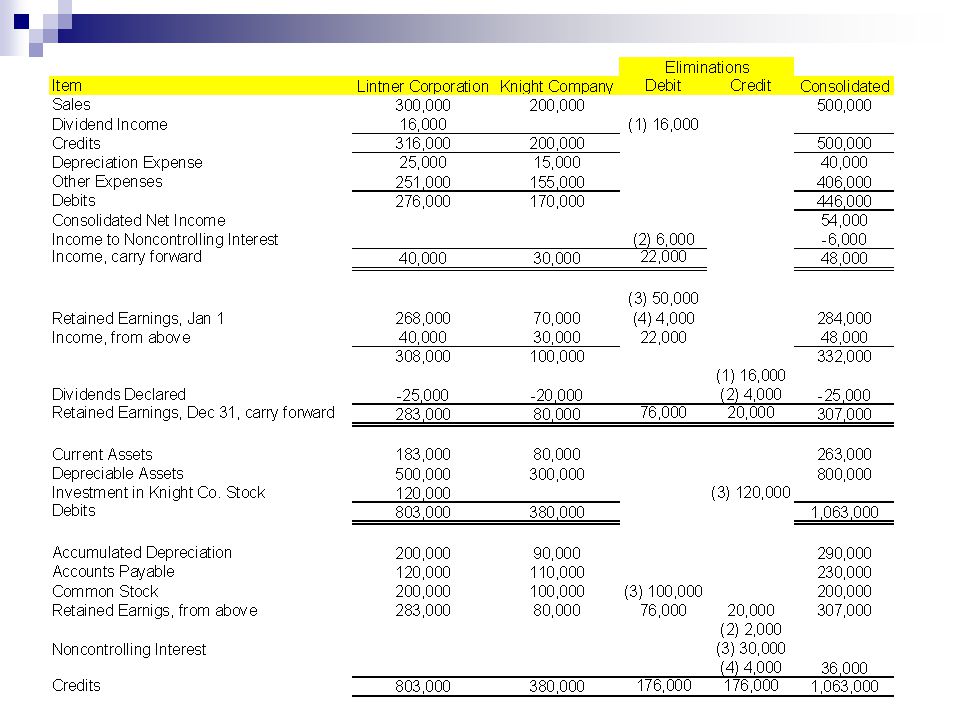

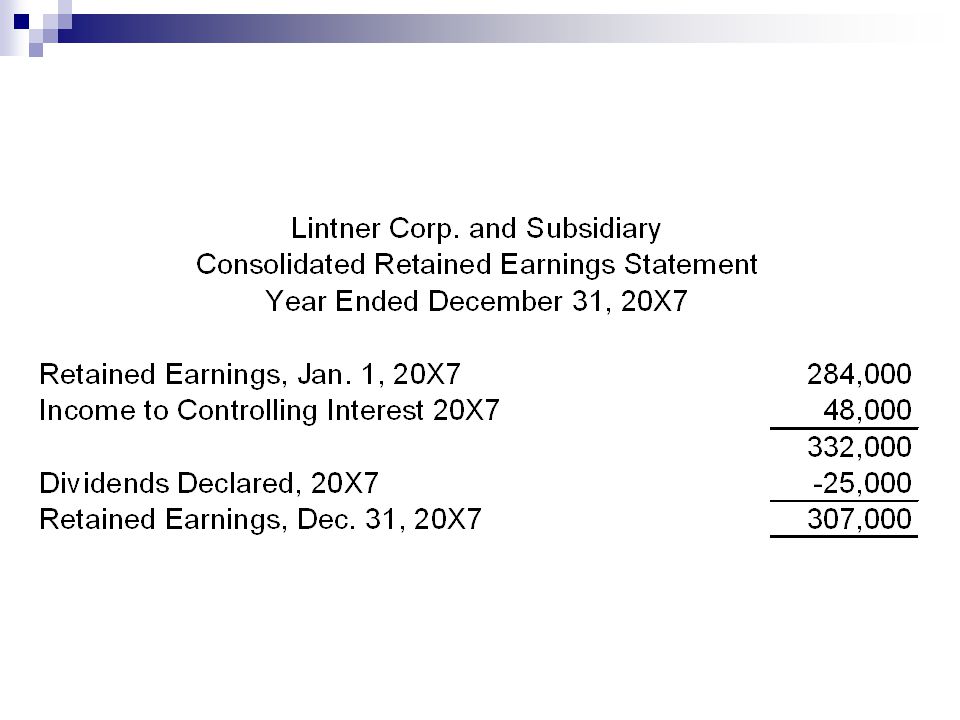

Elimination Entries, Dec 31, 20X7 E1Dividend Income16,000 Dividends Declared16,000 Eliminate Dividend Income from Subsidiary E2Income to Noncontrolling Interest6,000 Dividends Declared4,000 Noncontrolling Interest2,000 Assign income to noncontrolling interest E3Common Stock Knight Co.100,000 Retained Earnings, Jan 150,000 Investment in Knight Co. Stock120,000 Noncontrolling Interest30,000 Eliminate original investment balance E4Retained Earnings, Jan 14,000 Noncontrolling Interest4,000 Assign undistributed prior earnings of subsidiary to noncontrolling interest.

8

Differences Between the Cost and Equity Method ● The choice of the cost or equity method has no effect on the consolidated financial statements. ● Under the cost method, in the year of the combination no entries are made on the parent’s books to write off the portions of the differential that expire during that year. ● Consolidation differences become more evident in the second year of ownership. ● Under the cost method, the investment elimination entry continues to be the same in each subsequent year unless there is a change in ownership level or a change in the number of subsidiary shares outstanding.

9

Questions?

Similar presentations