Download presentation

Presentation is loading. Please wait.

1

Health Insurance Exchanges: What Your States Need to Do

2

What You Need Exchange for the individual market and a SHOP exchange One exchange or two? Exchanges will serve as Regulatory body Subsidy administrator Enrollment portal Informational portal Federal grants for establishing exchange will begin in March 2011 HHS issuing more guidance on structure of exchanges through 2011 Including what are essential benefits

3

Exchange Timeline October, 2010 HHS awards first round of planning and establishment grants to states January, 2011 – March, 2012 States authorize exchange through legislation January, 2013 HHS determines if state is willing and able to establish exchange by January, 2014 November, 2013Exchange begins selling health insurance January, 2014State exchange must be fully operational January, 2015Exchange must be self-sustaining 2017State may open exchange to large groups (>100)

")

4

Developing the Website Portal Secretary is required to operate and maintain an internet portal and assist states in developing and maintaining theirs Directs qualified individuals and employers to… Standardized information on qualified health plans Eligibility determination Premium tax credit or cost-sharing reductions eligibility Still waiting on further guidance

5

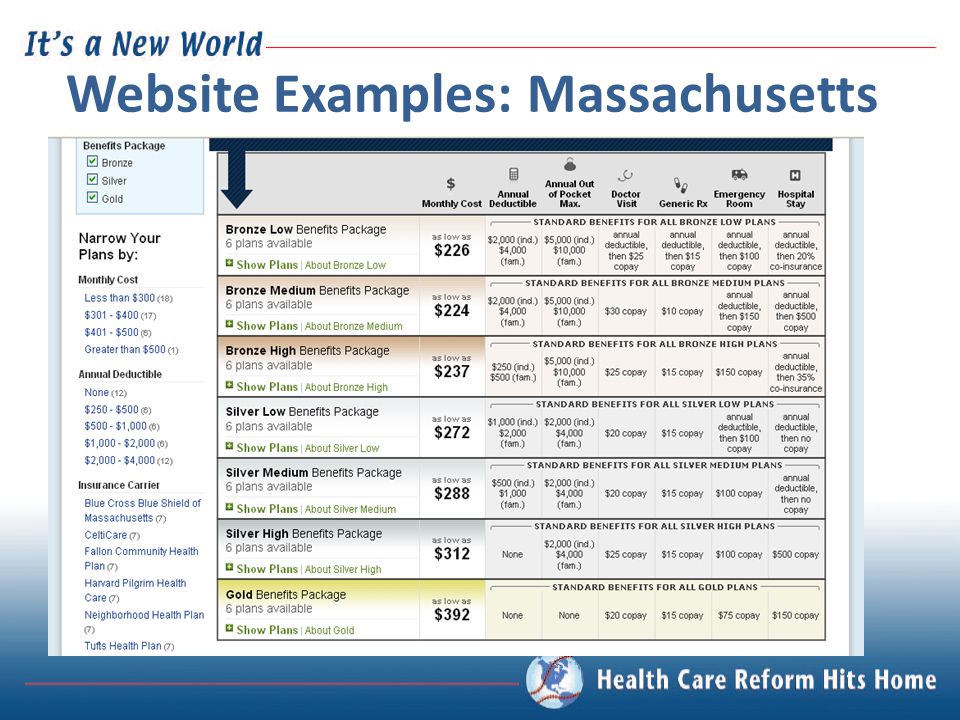

Website Examples: Massachusetts

7

Website Examples: Utah

9

Website Examples: Wisconsin, prototype

11

Governance Structure Bricks and Mortar Approach Establish new governance structure Might duplicate existing state government functions Utilize existing state regulatory authorities Department of Insurance State Medicaid/CHIP Offices Non-Profit Entity Most state exchanges will be governed by a Board representing stakeholders and policymakers.

12

Financing: Start Up Grants State Government financing In July, HHS provided $50 million in grants to help states start the planning process In January, HHS announced a second round of grants to help states to continue implementation States will have multiple opportunities to apply for funding as they progress through Exchange establishment Exchanges must be financially self-sustaining by 2015

13

Financing: Ongoing Operations State options to finance Exchanges after 2015: Massachusetts imposes a 4 percent assessment on exchange participants Utah assists only small groups offering defined contribution coverage, and does not impose a levy on enrollees Additional Fees: Exchange participants All consumers State Government Financing Increase burden on state budgets Expand the Individual Mandate penalty Additional penalty state collects to finance exchange States may explore assessments on carriers

14

Pooling PPACA requires insurers to pool all individual members in one risk pool and all small employer group members in another Currently carriers keep the two pools entirely distinct State exchange can determine if they want combined risk pools or separate Individual market benefit from larger risk pool? PPACA contains mechanisms that ensure adequate sized pools in all markets Massachusetts combination experience resulted in higher premiums 2007-2008: premiums in small group grew 5.8%

15

Plan Selection Negotiator vs. Facilitator Models Negotiate with plans to lower rates Exclude plans with bids that are “too high” or benefits that are inadequate Greater standardization and easier to compare plans Facilitate a marketplace- more or less “file and use” Exchange does not manage plan selection Greater plan design flexibility and better able to compete with the non-exchange market

16

Questions & Comments

17

Adam Brackemyre abrackemyre@nahu.org 703.276.3808 Brooke Bell bbell@nahu.org 703.276.3818 Russ Childers childr@bellsouth.net 229.924.7617 Contact Us Danielle Jaffee djaffee@nahu.org 703.276.3839 Michael Keegan mkeegan@nahu.org 703.276.3809 Ken Statz saquotecenter@msn.com 440.546.8330

18

Health Insurance Exchanges: What States Are Doing

19

Existing Exchanges: Massachusetts Massachusetts Health Insurance Connector established in 2006 Separate legal entity from the state Massachusetts Connector Authority 10 member board, with a spot specifically reserved for a member of the Massachusetts AHU Financed through premium surcharges on Commonwealth Care and Commonwealth choice products Individual Mandate Penalty assessed based on income and cost of the lowest- priced Commonwealth Care plan Employer Mandate Offer coverage or a “fair share” contribution

20

Existing Exchanges: Massachusetts Connector open to: Individual Market, “nongroup” Small Group (2-50) Limited large group: all employers establish section 125 plans for employees not eligible/offered group coverage Four Product Tiers: Bronze- low premium, higher cost-sharing Silver- moderate premiums, moderate cost-sharing Gold- high premiums, low cost sharing Young Adult Plans (YAP)- special low-cost and low benefit coverage for those up to age 26 Merged small group and individual market pools Same risk pool inside and outside of connector for each carrier

Limited large group: all employers establish section 125 plans for employees not eligible/offered group coverage Four Product Tiers: Bronze- low premium, higher cost-sharing Silver- moderate premiums, moderate cost-sharing Gold- high premiums, low cost sharing Young Adult Plans (YAP)- special low-cost and low benefit coverage for those up to age 26 Merged small group and individual market pools Same risk pool inside and outside of connector for each carrier")

21

Existing Exchanges: Utah Controlled by Office of Consumer Health Services, part of the Governor’s Office of Economic Development State retains budgetary control and authority Connector serves as an informational portal “Travelocity” model Exchange open to: Small group (2-50) No individual market- links individuals to carriers, producers and an insurance plan comparison chart Launching a large group pilot program this year Does not administer additional programs

No individual market- links individuals to carriers, producers and an insurance plan comparison chart Launching a large group pilot program this year Does not administer additional programs")

22

Existing Exchanges: Utah Exchange functions to allow small employers to offer defined contribution plans Employer contributes specific amount and employee free to choose plan for themselves Allow employees to pull money from multiple sources Individuals can carry plan with them if they change jobs No employer or individual mandate No set product levels or plan choices Small group risk pool combined for inside and outside of the exchange

23

Developing Legislation States will likely pass legislation to create the exchange during the 2011 legislative session States need to provide a business model to HHS in 2013 Legislation Currently introduced in: AK, AZ, DC, HI, MD, NJ*, NH, MS TX NAIC and NAHU models currently circulating NAIC model very straightforward to what PPACA outlines Leaves several areas vague for states to determine States can adapt for their existing markets and insurance laws No two exchanges will look the same

24

Key Differences in the NAHU Model Definition of “Health Insurance Producer” Establish a producer as an individual licensed to sell health insurance in a state Navigators and their qualifications Enrolling individuals in a qualified health plan requires you be licensed and regulated by the State and the Commissioner Includes all individuals affiliated or employed by an entity facilitating enrollment Still allows Navigators to serves as informational resource

25

Key Differences in the NAHU Model Governance Structure Public-private partnership Establish Exchange Board of Directors Representation: 3 persons affiliated with state authorized health insurers 2 licensed health insurance producers 3 representatives of the general public 1 state Medicaid representative Insurance commissioner or his/her designee Duties Board accountable to the Insurance Commissioner

26

What States Are Currently Doing Nebraska Working on developing a business model before legislation Develop structure, financing, authority Texas Rep. John Zerwas introduced HB 636 Bill tracks the NAIC model, but requires 3 of the 5 voting board members to have insurance background Establishes “Navigator” program consistent with PPACA Ohio Received grant from the Robert Woods Johnson Foundation in 2008 State Coverage Initiative tasked to look at way to cover more Ohio consumers Recommendations included many PPACA-related reforms

27

Questions & Comments

28

Adam Brackemyre abrackemyre@nahu.org 703.276.3808 Brooke Bell bbell@nahu.org 703.276.3818 Russ Childers childr@bellsouth.net 229.924.7617 Contact Us Danielle Jaffee djaffee@nahu.org 703.276.3839 Michael Keegan mkeegan@nahu.org 703.276.3809 Ken Statz saquotecenter@msn.com 440.546.8330

Similar presentations