Download presentation

Presentation is loading. Please wait.

1

Employee Guide to Enrolling in the Health Insurance Marketplace

3

Today’s program will show you how to apply for tax credits and insurance subsidies, compare benefits, and enroll in a PPACA Reform Health Insurance Plan

4

Comparing Benefits and your “Out of Pocket” expense. PREMIUM DEDUCTIBLE The amount that you will have to pay annually for your healthcare (such as surgical procedures, blood tests, or hospitalizations, but not routine office visits) before the health insurance pays anything OUT-OF-POCKET MAXIMUM (OOP) The most cost-sharing you will ever have to pay in a year. It is the total of your deductible, copays, and coinsurance (but does not include your premiums). Once you hit this limit, the insurance company will pick up 100 percent of your costs for the remainder of the year.

before the health insurance pays anything OUT-OF-POCKET MAXIMUM (OOP) The most cost-sharing you will ever have to pay in a year. It is the total of your deductible, copays, and coinsurance (but does not include your premiums). Once you hit this limit, the insurance company will pick up 100 percent of your costs for the remainder of the year..")

5

CO-PAY Your co-pay is the fixed amount you pay for using routine services like visiting your primary care physician or an emergency room or purchasing a prescription drug. For example, a plan may require co-pays of $20 for office visits, $100 for emergency room visits, and $15 for generic prescriptions or $30 for name-brand drugs. CO-INSURANCE Co-insurance generally applies to less routine expenses. Co-insurance is in addition to your deductible. So if your plan has a $100 deductible and 30% co-insurance and you use $1,000 in services, you’ll pay the $100 plus 30% of the remaining $900, up to your out-of-pocket maximum. COST - SHARING

6

Let’s see how this works The Plan that you are evaluating pays $500.00 deductible. 30% co- insurance, OOP $4,000. What is the benefit? You Break a Leg MEDICAL EXPENSES Hospital Charges $2,000 Doctor Fees $3,000 Without insurance you would pay out-of-pocket $5,000.00 Impact of Deductible and Co-Insurance Deductible $500.00 30% Coinsurance - after you pay the deductible ($500.00), you pay 30% of the remaining amount. $5,000.00 - $500 deductible = $4,500.00 times 30% = $1,350.00 Total that you pay out-of-pocket = $500 + $1,350 = $1,850 – You save $ 3,150.00 with this insurance plan

, you pay 30% of the remaining amount. $5, $500 deductible = $4, times 30% = $1, Total that you pay out-of-pocket = $500 + $1,350 = $1,850 – You save $ 3, with this insurance plan.")

7

Let’s see how all of this works Have an Appendectomy MEDICAL EXPENSES Hospital Charges = $12,000 Doctor Fees = $4,000 Without insurance you would pay out-of-pocket $16,000 Impact of Deductible and Co-Insurance Deductible = $500.00 OOP = $4000.00 30% Coinsurance – after you pay the deductible ($500.00), you would pay 30% of the remaining $15,500.00 = $4,650.00, but your out-of-pocket maximum is $4,000. Total that you pay out-of-pocket = $4,000 – You save $12,000.00 with this insurance plan. Note that some plans state that their out-of--pocket maximum does not include the deductible, so your total out of pocket cost would be $4,500.

8

If you enroll between October 1 and December 15, 2013, the effective date for when your insurance coverage begins will be January 1, 2014. After December 15, 2013 the effective dates will change. Enroll between:Effective Date is: December 16 – January 15, 2014 February 1, 2014 January 16 - February 15, 2014March 1, 2014 February 16 – March 15, 2014April 1, 2014 March 16 - March 31, 2014May 1, 2014 2014 and beyond – Open enrollment Dates: October 15 – December 7 REFORM INSURANCE INITIAL ENROLLMENT DATES

9

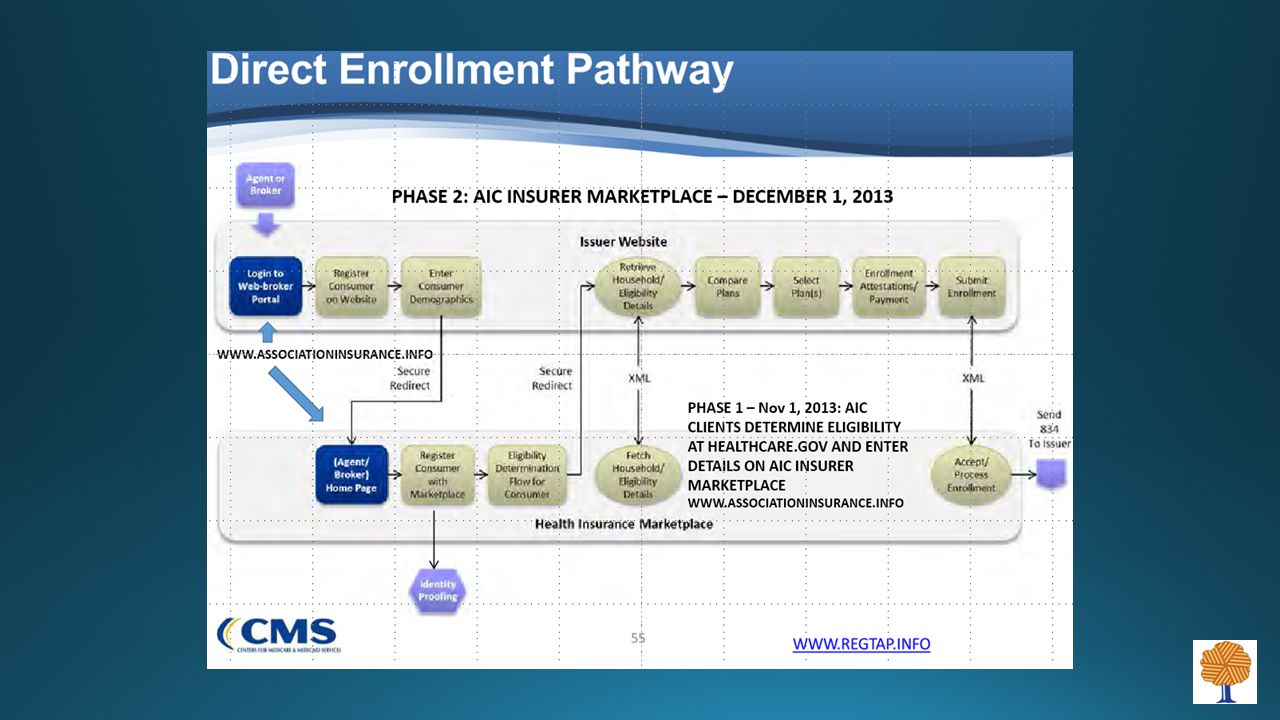

ACA Enrollment Pathways www.HealthCare.gov – Use this Federally Facilitated Marketplace site to determine your eligibility for government programs and to enroll in the Marketplace. CMS 10-4-2013: “When the consumer is logged in to the healthcare.gov page, the consumer will be shown a screen labeled, “Help applying for coverage.” On this screen, it is vital that the consumer enters the agent’s/broker’s name, NPN, and FFM User ID”. AIC Agent/Broker Name: Kennth Lee NPN: 7873397 FFM ID: lee2020 AIC Application Information on the AIC home page: www.associationinsurance.us CLICK HERE for ACA Reform Insurance for Persons Not Needing Subsidies and ACA Paper Application for Subsidies

10

AIC Insurer Pathway November: Determine Eligibility and Enroll via Insurer Website December: Eligibility and Enrollment in both On- Exchange and Off-Exchange Marketplace – “one stop”

11

Set up an account. First you'll provide some basic information. Then choose a user name, password, and three security questions for added protection. Enrollment Process Overview at HealthCare.gov

12

Fill out the online application. Enrollment Process Overview

13

Compare your options. Shortly upon entering the information, you will see all the options you qualify for, including private insurance plans and free and low-cost coverage through Medicaid and the Children’s Health Insurance Program (CHIP).MedicaidChildren’s Health Insurance Program (CHIP) The Marketplace will tell you if you qualify for lower costs on your monthly premiums and out-of-pocket costs on deductibles, copayments, and coinsurance. You’ll see details on costs and benefits.lower costs on your monthly premiumsout-of-pocket costsdeductibles copaymentscoinsurancedetails on costs and benefits Make sure that your physician is part of the network – On Exchange Policies may have a limited provider network Enrollment Process Overview

.MedicaidChildren’s Health Insurance Program (CHIP) The Marketplace will tell you if you qualify for lower costs on your monthly premiums and out-of-pocket costs on deductibles, copayments, and coinsurance. You’ll see details on costs and benefits.lower costs on your monthly premiumsout-of-pocket costsdeductibles copaymentscoinsurancedetails on costs and benefits Make sure that your physician is part of the network – On Exchange Policies may have a limited provider network Enrollment Process Overview.")

14

Health Insurance Marketplace Plans, Benefits, and Costs “Metal Tiers” Bronze Plan: You pay 40% and the plan pays 60%. Silver Plan: You pay 30% and the plan pays 70%. Gold Plan: You pay 20% and the plan pays 80%. Platinum Plan: You pay 10% and the plan pays 90%. Catastrophic plans will be available for persons who are under 30, persons with financial hardship, and certain other demographics. These plans will be qualified health plans and have lower premium cost, but the plans will have less coverage and higher co-pays and co-insurance. Persons with this coverage are not eligible for tax credits or subsidies.

15

Health Insurance Marketplace Plans, Benefits, and Costs A Qualified Health Plan is a Marketplace certified “health plan” that offers an “essential health benefits package.” To provide the essential health benefits package, a plan must include: ACA required preventative services. Essential health benefits. Include the four metal tiers.

16

Age Forty, Male, Non-Smoker Indiana - 46151Ohio - 44130

17

AIC SUMMARY AIC will assist you to determine eligibility for tax credits and insurance subsidies. Enrollments between October 1 and December 15, 2013 have an effective date of January 1, 2014. Qualified Health Plans: guarantee issue, no pre-existing condition limitations, Essential Health Benefits (EHB). Only DHHS certified agents and brokers can help you to choose and purchase QHP. An Employee Guide to Enrolling in the Indiana, Ohio, Illinois, and Michigan Health Insurance Marketplace.

. Only DHHS certified agents and brokers can help you to choose and purchase QHP. An Employee Guide to Enrolling in the Indiana, Ohio, Illinois, and Michigan Health Insurance Marketplace..")

18

ACA Application - Short Form (Individuals) ACA Application - Short Form Instructions ACA Application - Long Form (Applicants with Dependents) ACA Application - Long Form Instructions Determining Eligibility for Subsidies Using a Paper Application

ACA Application - Short Form Instructions ACA Application - Long Form (Applicants with Dependents) ACA Application - Long Form Instructions Determining Eligibility for Subsidies Using a Paper Application")

19

Important Links Federally Facilitated Marketplace https://www.healthcare.gov/index.html Estimate Your Tax Credits or Subsidy at http://kff.org/interactive/subsidy-calculator/ ACA Required Preventive Services Individual Mandate Flow Chart Employee Guide to Health Care Reform's Tax Credits Association Insurance Cooperative Website – www.associationinsurance.us AIC Insurer Marketplace – www.associationinsurance.info

20

Contact Information Kenneth S. Lee, Program Director – email: klee@mynpi.org klee@mynpi.org Bob Brodell, AIC General Agent – email: bob@imaginehealthsolutions.com bob@imaginehealthsolutions.com AIC Website: www.associationinsurance.uswww.associationinsurance.us AIC Insurer Website: www.associationinsurance.infowww.associationinsurance.info

Similar presentations

Plans CY 2010. Medicare Medicare is a Federal health insurance program for those age 65 or older or individuals at any age who have.>")

>")

OCIIO Office of Oversight Office of Insurance Programs Office of Consumer Support Office.>")

Information and Open Forum St. Norbert College Health and Wellness Services AND Student Government Association March 27, 2014.>")