Download presentation

1

Summary so far…….

4

SPECIAL JOURNALS Special journals classify and summarise data from source documents. The use of special journals allows for totals to be entered in ledger accounts, removing clutter from the General Ledger. What story does this diagram show?

5

THE GENERAL LEDGER A ledger is a system of keeping accounts in a double-entry system. The General Ledger is the main collection of business accounts, e.g. Bank, Debtors Control, Creditors Control, Capital, etc. THE SUBSIDIARY LEDGER The Subsidiary Ledger contains all the individual accounts for debtors and creditors (detail) POSTING Posting is the process of transferring totals from Special Journals to General Ledger accounts on the last day of each month. Double-entry rules still apply.

POSTING Posting is the process of transferring totals from Special Journals to General Ledger accounts on the last day of each month. Double-entry rules still apply..")

6

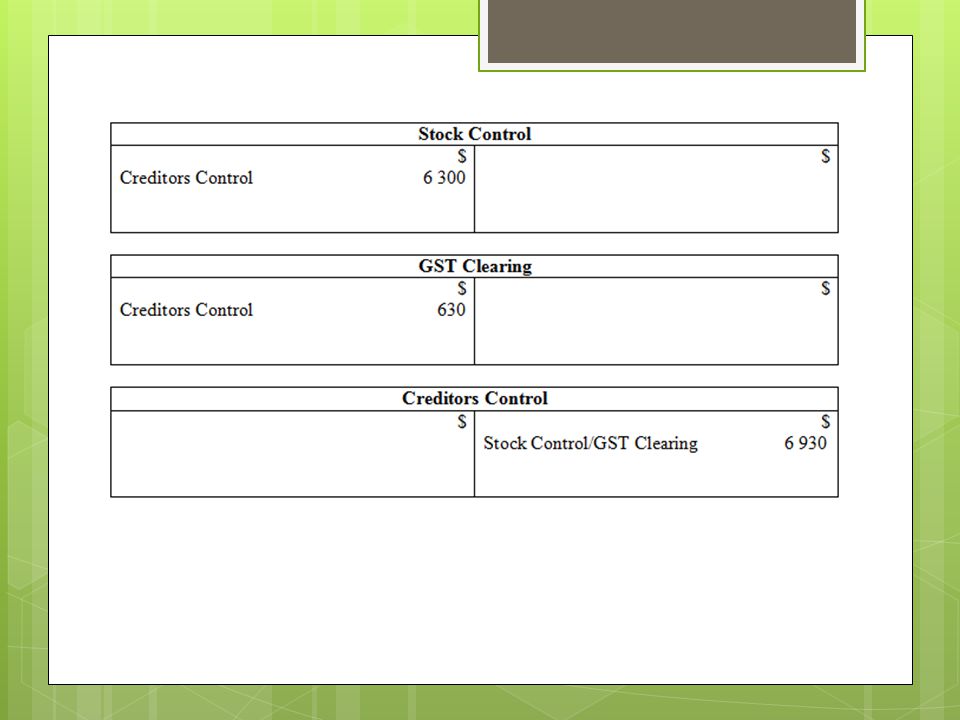

PURCHASES JOURNAL The Purchases Journal records all credit purchases of stock from creditors, evidenced by purchase invoices. = + CR DR

8

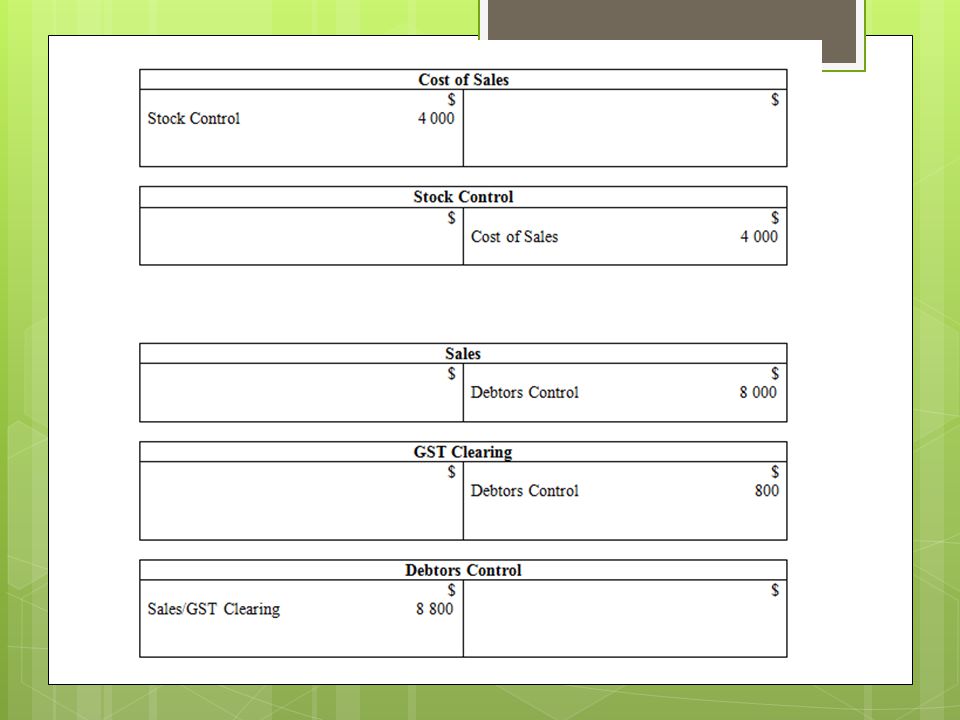

SALES JOURNAL The Sales Journal records all credit sales of stock to debtors, evidenced by sales invoices. += DR CR

10

CASH RECEIPTS JOURNAL The cash receipts journal records all cash received by the business, evidenced by receipts and cash register rolls. ++ + + =

12

CASH PAYMENTS JOURNAL The cash payments journal records all cash paid by the business, evidenced cheque butts. + + + + + =

14

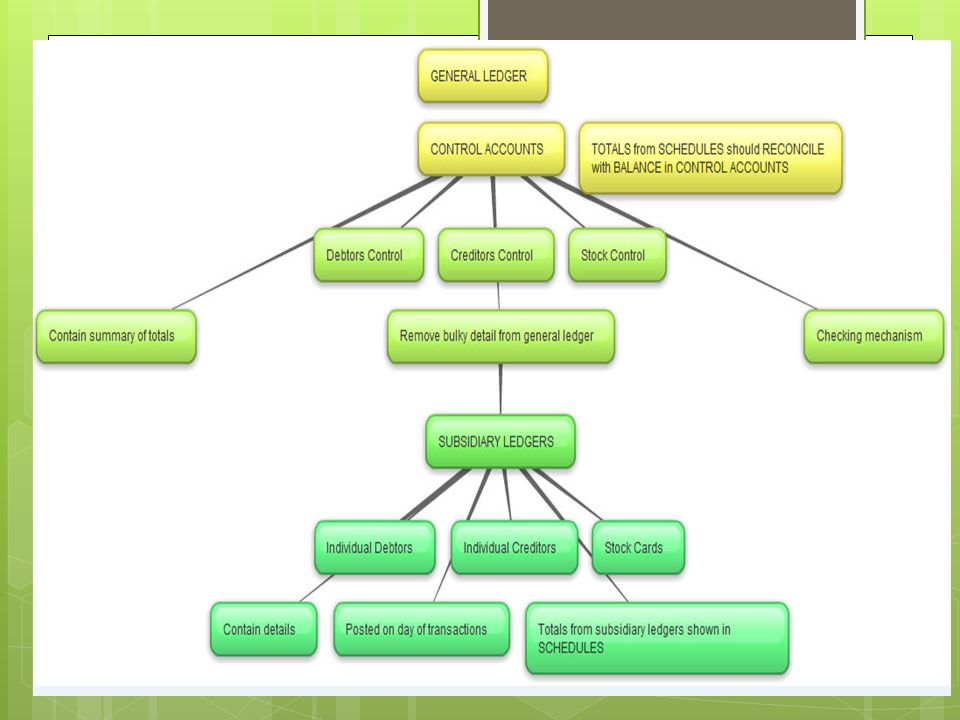

Need for CONTROL ACCOUNTS So many transactions General ledger would get cluttered with the many individual debtors/creditors accounts Control accounts allow for totals to be posted reduce the bulky detail in the general ledger Summary of all debtors/creditors The bulky detail of individual debtors or creditors goes into what is called the subsidiary ledger

15

POSTING TO THE SUBSIDIARY LEDGER Individual transactions for debtors and creditors are not posted to the General Ledger, they are posted to the Subsidiary Ledger. THE CREDITORS SCHEDULE The Creditors Schedule is a report that shows the closing balance of each individual creditor account from the Creditors Subsidiary Ledger. The total of these balances must equal the closing balance of the Creditors Control account in the General Ledger. THE DEBTORS SCHEDULE This schedule lists the closing balances from the Debtors Subsidiary Ledger and checks them against the closing balance of the Creditors Control account. This process of checking is called ‘reconciliation’.

16

THE RELATIONSHIP BETWEEN CONTROL ACCOUNTS AND SUBSIDIARY LEDGER ACCOUNTS Control accounts summarise the information from the Subsidiary Ledger accounts. Control accounts include Debtors Control, Creditors Control and Stock Control. All control accounts are part of the General Ledger. All account balances in the General Ledger will appear in the Trial Balance. All individual accounts for debtors and creditors are in the Subsidiary Ledger. The Subsidiary Ledger accounts are not shown in the Trial Balance. Account balances for debtors and creditors in the Subsidiary Ledger are summarised in schedules. The total of the Debtors Schedule must equal the balance of the Debtors Control account. The total of the Creditors Schedule must equal the balance of the Creditors Control account.

and __________________ (A/P) increases as the business expands.>")