Download presentation

Presentation is loading. Please wait.

1

Investigating the difference between discounted cash flow and German income approach Jan Reinert Property Portfolio Analyst Phd Candidate IPD GermanyInternational Real Estate Business School jan.reinert@ipd.com jan.reinert@wiwi.uni-regensburg.de June 2012

2

o Introduction o Literature o Background o Discounted Cash Flow o German Income Approach o Hypotheses o Data Set & Methodology o Performance Measure Analysis o Regression Analysis o Conclusion & Future Research o Bibliography

3

© IPD 2012

6

o RICS IPD Valuation and Sale Price Report 2011 How much does sale price differ from previous valuation? France:8.8%Netherlands:11.8% UK:12.5%Germany:14.2% o Crosby (2007) German open ended funds: was there a valuation problem? Valuations in the UK are more objective and conceptually correct than in Germany. Over-valuations during recessions are more likely in Germany than in other markets. o Weistroffer (2010) The German open end fund crisis – A valuation problem? German valuation standards result in a smoothing effect which contributed to the open-ended fund crisis of 2005/2006. o Glaesner, Thomas and Schiereck (2010) Lack of German real estate fund volatility – is the market or the valuer to blame? In contrast to the UK, German fund managers have an interest in stable and smooth value changes. ( client influence) o Schnaidt and Sebastian (2012) German valuation: review of methods and legal framework The differences between the German and British capitalization approaches are not enough to explain any large difference in valuations and should yield comparable results. The German valuation approach is unlikely to be the reason for the observed anomalies.

German open ended funds: was there a valuation problem. Valuations in the UK are more objective and conceptually correct than in Germany. Over-valuations during recessions are more likely in Germany than in other markets. o Weistroffer (2010) The German open end fund crisis – A valuation problem. German valuation standards result in a smoothing effect which contributed to the open-ended fund crisis of 2005/2006. o Glaesner, Thomas and Schiereck (2010) Lack of German real estate fund volatility – is the market or the valuer to blame. In contrast to the UK, German fund managers have an interest in stable and smooth value changes. ( client influence) o Schnaidt and Sebastian (2012) German valuation: review of methods and legal framework The differences between the German and British capitalization approaches are not enough to explain any large difference in valuations and should yield comparable results. The German valuation approach is unlikely to be the reason for the observed anomalies..")

7

o Term: o Actual income and costs are forecasted for the near future o Costs paid by tenants are excluded o Includes special circumstances such as vacancies, rent o reviews, rent free periods and new tenant fit outs o Net cash flows are discounted at the appropriate rate o Reversion: o Expected future resale value (future net cash flow in perpetuity o at the appropriate rate) is discounted to the present

is discounted to the present")

8

o Value of the land: o Value as if vacant lot o Benchmark land values based on comparison method using o actual market transactions o Infinite value o Value of the building: o Sustainable/market income and costs o Finite value (if not upgraded) depending on economic age o Liegenschaftszinssatz = Market Net Yield (differs from regular o discount rates depending on the value of the land and the o economic age)

depending on economic age o Liegenschaftszinssatz = Market Net Yield (differs from regular o discount rates depending on the value of the land and the o economic age)")

10

German DCF valuations differ significantly from traditional German valuations (GIA) in terms of volatility and market accuracy. DCF valuations experience more volatility and are better estimates of true market values GIA valuations produce better estimates for the German real estate market German DCF valuations do not differ significantly from traditional German valuations The German market is peculiar (see Switzerland) German DCF valuations are not real DCF valuations

German DCF valuations are not real DCF valuations.")

11

German DCF valuations differ significantly from traditional German valuations (GIA) in terms of volatility and market accuracy. DCF valuations experience more volatility and are better estimates of true market values GIA valuations produce better estimates for the German real estate market German DCF valuations do not differ significantly from traditional German valuations The German market is peculiar (see Switzerland) German DCF valuations are not real DCF valuations

German DCF valuations are not real DCF valuations.")

12

o Supplied by IPD o Time Period: 2003 – 2011 o 15,036 Observations o 3,384 Properties o 80 Portfolios o Only Investors based in Germany o Including office, retail, mixed used and industrial properties o Available information: o Appraisal method o Appraised capital value o Purchase/Sale information o Passing rent (as stated in contract) o Estimated market rent o Area in sqm o Economic age o Vacancy rate at year end o Primary use o Location o Annual total return o Annual income return o Annual capital value growth

o Estimated market rent o Area in sqm o Economic age o Vacancy rate at year end o Primary use o Location o Annual total return o Annual income return o Annual capital value growth")

13

DCF Valuations: 2003: 3.4% 2011: 9.6%

14

A) Performance Measure Analysis o Comparison of total return, income return & capital value growth for GIA and DCF valuations B) Regression Analysis* o Deriving hedonic indices for GIA and DCF valuations o Using mass appraisals to derive transaction prices o Comparing the difference between transaction prices and actual valuations * see Weistroffer (2010)

Performance Measure Analysis o Comparison of total return, income return & capital value growth for GIA and DCF valuations B) Regression Analysis* o Deriving hedonic indices for GIA and DCF valuations o Using mass appraisals to derive transaction prices o Comparing the difference between transaction prices and actual valuations * see Weistroffer (2010)")

15

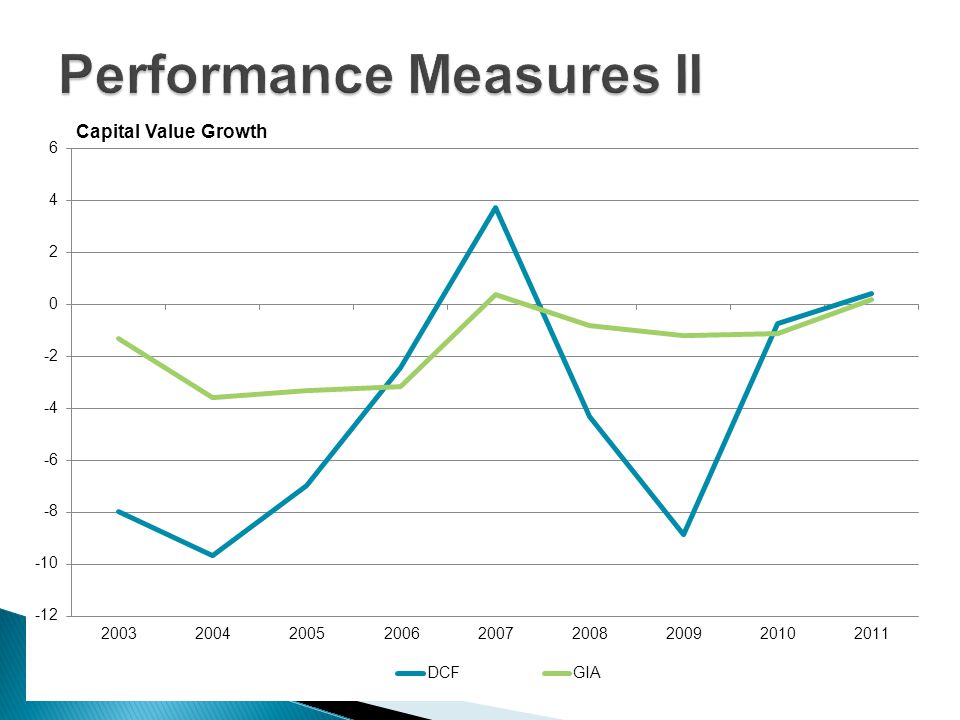

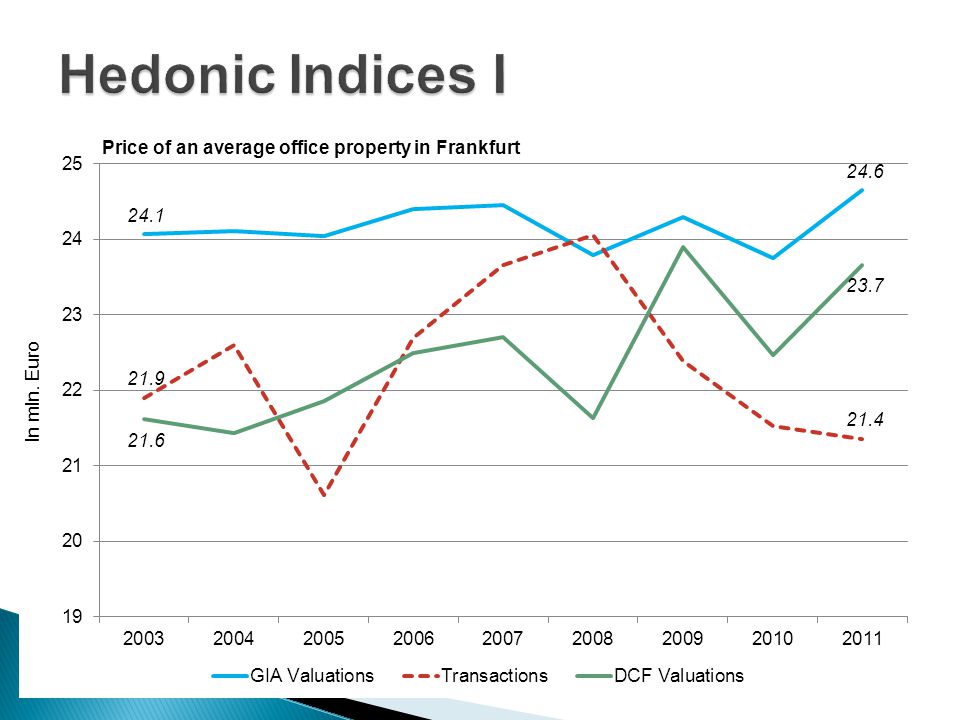

Performance Measure Analysis

19

Regression Analysis

20

lnprice lnvalue CoefficientSt. Err.P>t Coef.St. Err.P>t y04 0.0110.0130.405 -0.0100.0040.009 … ……… ……… y11 0.0030.0170.841 -0.0160.0040.000 lnquality 0.7800.1270.000 0.9960.0110.000 lnrent 0.2080.0720.004 0.0910.0090.000 lnage -0.0740.0140.000 -0.0430.0040.000 lnvacancy -0.0130.0150.383 -0.0090.0020.000 lnarea 0.7600.0880.000 0.9320.0100.000 large 0.0150.0190.428 -0.0030.0050.561 small -0.0180.0150.236 0.0230.0050.000 retail 0.0190.0090.030 -0.0100.0030.000 indus -0.1260.0400.002 -0.0760.0110.000 mixed 0.0390.0080.000 0.0140.0030.000 st -0.0540.0250.028 -0.0220.0060.000 … ……… ……… th -0.0870.043 -0.0350.0100.000 _cons 1.4020.2310.000 0.9740.0330.000 dcf_y03 -0.0470.0380.225 … ……… dcf_y11 -0.0180.0080.023 Obs. 1,914 12,665 Prob > F 0.000 R-squared 0.934 0.963 Adjusted R2 0.932 0.963

21

lnvalue CoefficientSt. Err.P>t y04 -0.0100.0040.014 … ……… y11 -0.0140.0040.000 lnquality 0.9960.0110.000 lnrent 0.0900.0090.000 lnage -0.0430.0040.000 lnvacancy -0.0090.0020.000 lnarea 0.9320.0100.000 large -0.0020.0050.617 small 0.0230.0050.000 retail -0.0100.0030.001 indus -0.0770.0110.000 mixed 0.0140.0030.000 st -0.0220.0060.000 … ……… th -0.0340.0100.001 dcf -0.0300.0070.000 _cons 0.9750.0330.000 Obs. 12,665 Prob > F 0.000 R-squared 0.963 Adjusted R2 0.963 lnvalue CoefficientSt. Err.P>t y04 -0.0100.0040.009 … ……… y11 -0.0160.0040.000 lnquality 0.9960.0110.000 lnrent 0.0910.0090.000 lnage -0.0430.0040.000 lnvacancy -0.0090.0020.000 lnarea 0.9320.0100.000 large -0.0030.0050.561 small 0.0230.0050.000 retail -0.0100.0030.000 indus -0.0760.0110.000 mixed 0.0140.0030.000 st -0.0220.0060.000 … ……… th -0.0350.0100.000 _cons 0.9740.0330.000 dcf_y03 -0.0470.0380.225 … ……… dcf_y11 -0.0180.0080.023 Obs. 12,665 Prob > F 0.000 R-squared 0.963 Adjusted R2 0.963

25

Simple Average Deviation from Valuation (Transaction - Valuation) / Valuation 200320042005200620072008200920102011 All Years St. Dev. DCF9.3%15.1%15.2%6.4%-0.3%5.2%5.8%1.1%-1.5%4.3%20.8% GIA-9.4%-7.2%-5.0%-11.1%-6.2%-3.1%-0.2%-6.6%-9.6%-6.8%12.8% Including all observations: Excluding the top and bottom 5%: Simple Average Deviation from Valuation (Transaction - Valuation) / Valuation 200320042005200620072008200920102011 All Years St. Dev. DCF34.8%18.1%16.0%11.6%36.0%23.5%8.6%6.3%1.2%16.1%117.2% GIA-8.4%-3.8%-1.4%-9.7%-1.7%0.8%7.9%0.3%-5.4%-6.8%32.8%

/ Valuation All Years St. Dev. DCF34.8%18.1%16.0%11.6%36.0%23.5%8.6%6.3%1.2%16.1%117.2% GIA-8.4%-3.8%-1.4%-9.7%-1.7%0.8%7.9%0.3%-5.4%-6.8%32.8%.")

26

Simple Average Deviation from Valuation (Transaction - Valuation) / Valuation 200320042005200620072008200920102011 All Years St. Dev. DCF9.3%15.1%15.2%6.4%-0.3%5.2%5.8%1.1%-1.5%4.3%20.8% GIA-9.4%-7.2%-5.0%-11.1%-6.2%-3.1%-0.2%-6.6%-9.6%-6.8%12.8%

27

Absolute Average Deviation from Valuation (Transaction - Valuation) / Valuation 200320042005200620072008200920102011 All Years St. Dev. DCF19.0%20.3%21.1%19.6%17.8%17.0%12.0%10.3%9.2%14.6%15.5% GIA13.3%12.5%11.7%14.6%11.4%10.4%9.5%10.8%12.7%12.1%7.9%

28

German DCF valuations differ significantly from traditional German valuations (GIA) in terms of volatility and market accuracy. DCF valuations experience more volatility and are better estimates of true market values GIA valuations produce better estimates for the German real estate market German DCF valuations do not differ significantly from traditional German valuations The German market is peculiar (see Switzerland) German DCF valuations are not real DCF valuations

German DCF valuations are not real DCF valuations.")

29

1)There seems to be a significant difference between traditional German valuations (GIA) and German DCF valuations. 2)The analysis suggests that the GIA produces more stable valuations than DCF appraisals. 3)GIA valuations tend to be on average above transaction prices while DCF valuations are on average below market prices. 4)When using simple averages DCF valuations appear to be better estimates of transaction prices. 5)When using absolute deviation from valuation GIA valuations seem to be on average closer to transaction prices.

The analysis suggests that the GIA produces more stable valuations than DCF appraisals. 3)GIA valuations tend to be on average above transaction prices while DCF valuations are on average below market prices. 4)When using simple averages DCF valuations appear to be better estimates of transaction prices. 5)When using absolute deviation from valuation GIA valuations seem to be on average closer to transaction prices..")

30

o Model is likely to suffer from sample selection bias (Only certain properties (offer > reserve) result in a sale. This might explain the rising transaction prices of 2008 in the model) Heckman (1979) o Are German DCF valuations „real“ DCF valuations? (50% of DCF valuations report „economic age“ which is only relevant for the GIA method) o Does the valuation method influence transaction prices? o As more German investors are using DCF valuations a larger o data set will be available in the future (Possibility to carry out more in depth analyses over longer periods of time) o Is the gap between DCF valuations and transaction prices o going to decrease further?

Heckman (1979) o Are German DCF valuations „real DCF valuations. (50% of DCF valuations report „economic age which is only relevant for the GIA method) o Does the valuation method influence transaction prices. o As more German investors are using DCF valuations a larger o data set will be available in the future (Possibility to carry out more in depth analyses over longer periods of time) o Is the gap between DCF valuations and transaction prices o going to decrease further .")

31

o Crosby, N. (2007) German open ended funds: was there a valuation problem?, Working Papers in Real estate and Planning 05/07, University of Reading o Glaesner, S., Thomas, M., Schiereck, D. (2010) Lack of German real estate fund volatility – is the market or the valuer to blame?, in Return Patterns of German Open-End Real Estate Funds – An empirical Explanation of Smooth Fund Returns by Glaesner, S., Peter Lang, Frankfurt, pp. 35-56 o RICS IPD Valuation and Sale Price Report 2011 (2012), rics.org/research o Schnaidt, T., Sebastian, S. (2012) German valuation: review of methods and legal framework; Journal of Property Investment & Finance, Vol. 30, No.2, pp. 145-158 o Weistroffer, C. (2010) The German Open-End Fund Crisis – A Valuation Problem?, Working Paper, Goethe-University, Frankfurt

German open ended funds: was there a valuation problem , Working Papers in Real estate and Planning 05/07, University of Reading o Glaesner, S., Thomas, M., Schiereck, D. (2010) Lack of German real estate fund volatility – is the market or the valuer to blame , in Return Patterns of German Open-End Real Estate Funds – An empirical Explanation of Smooth Fund Returns by Glaesner, S., Peter Lang, Frankfurt, pp o RICS IPD Valuation and Sale Price Report 2011 (2012), rics.org/research o Schnaidt, T., Sebastian, S. (2012) German valuation: review of methods and legal framework; Journal of Property Investment & Finance, Vol. 30, No.2, pp o Weistroffer, C. (2010) The German Open-End Fund Crisis – A Valuation Problem , Working Paper, Goethe-University, Frankfurt.")

32

Jan Reinert Property Portfolio Analyst Phd Candidate IPD GermanyInternational Real Estate Business School jan.reinert@ipd.com jan.reinert@wiwi.uni-regensburg.de June 2012

Similar presentations