Download presentation

Presentation is loading. Please wait.

1

AIR CADET LEAGUE of Canada Financial Training Course (June 2013)

")

2

FINANCIAL TRAINING TODAY’S LESSONS Introduction - Presentation of the training course Aims and objectives Purpose of the Treasurer

3

Section 1: Basic accounting notions Section 2: Budget Section 3: Bookkeeping Section 4: Annual Financial Statement– ACC9 Section 5: GST, Provincial taxes

4

Section 6: Registered Charity Information Return (Federal T-3010B (09), Provincial TP-985.22) Section 7: Practical information and schedule Section 8: Additional Resources

, Provincial TP ) Section 7: Practical information and schedule Section 8: Additional Resources")

5

Aims and Objectives of the Training Course Respond to an actual need for volunteers Clarify the purpose of the treasurer within the organization and define expectations Provide simple working methods and tools Ensure continuity of the activities in favor of young cadets Ensure succession in the Squadron Facilitate access to the Treasurer position Standardize management of accounting information within the Squadrons

6

CHAIR 1ST VICE-CHAIR SECRETARY TREASURER EXECUTIVE COMMITTEE DIRECTOR PROCESS MAP OF THE SPONSORING COMMITTEE 2ND VICE-CHAIR

7

Function of the Treasurer 1.Record on a monthly basis, money entries and disbursements in the sub- ledger, according to the chart of account 2.Put audit controls for each financing activity in place (maximize revenues and minimize losses) 3.Submit financial statements (revenues and expenses) as well as the bank reconciliation 4.File bills 5.Ensure a rigorous follow-up on cash to be received from DND (CDT 135)

3.Submit financial statements (revenues and expenses) as well as the bank reconciliation 4.File bills 5.Ensure a rigorous follow-up on cash to be received from DND (CDT 135)")

8

Function of the Treasurer (continued) 6.Inform semi-annually to the Chair of the important budget variances and suggest alternatives 7.Prepare annually the budget in collaboration with the Chair and the Commanding Officer 8.Maintain the inventory of the goods belonging to the Squadron up-to-date 9.Prepare the (ACC-9) report and submit it within the period specified 10.Complete the different governmental reports (GST, QST, T-3010, TP-985.22) and submit them within the period specified 11.Emit receipts for charitable contributions for taxation purposes

6.Inform semi-annually to the Chair of the important budget variances and suggest alternatives 7.Prepare annually the budget in collaboration with the Chair and the Commanding Officer 8.Maintain the inventory of the goods belonging to the Squadron up-to-date 9.Prepare the (ACC-9) report and submit it within the period specified 10.Complete the different governmental reports (GST, QST, T-3010, TP ) and submit them within the period specified 11.Emit receipts for charitable contributions for taxation purposes")

9

Selection criteria for the position of treasurer: 1. Attention to detail 2. Methodical 3. Rigorous in tasks to complete 4. Discreet – confidential information 5. Trusted Pre-requisites : 1. Be confident with numbers 2. The treasurer must not have had a personal bankruptcy 3. Have a good reputation in the community

10

Section 1: Basic notions on accounting A.Accrual accounting: A purchase will be entered in an account when the merchandise is received even if the payment is only due later. The counterpart of the expense coming from this purchase will be an account to be settled. The account to be settled will only be cancelled once the payment has been done. This way of accounting is much more precise since at the end of the month or the year it takes all the revenues and charges into account even if these have not been cashed or disbursed B.Cash basis: Transactions are accounted for based on the entries and outgoings from the bank account. Revenues and expenses are only accounted for when they are cashed or disbursed. This accounting system is simple and has the advantage of being easy to follow.

11

Terminology Statement of income : Accounting report which resumes the financial situation of an entity during its financial year. The totality of the revenues and expenses are presented here. The exceeding amount of the revenues on the expenses is a profit (loss). Financial year : Period of time between July 1st and June 30th of the next year Balance sheet : State of the financial situation on a given date. The balance sheet presents the whole of the assets (what one possesses) and of the liabilities (what one owes). The total of the assets must always balance with the total of the liabilities. General ledger : Represents the whole of the accounting accounts used by the entity (see ACC-9 for more details) Sub-ledger : Revenue journal « revenue » (cash inflow) and journal of the « Expenses» (disbursements)

. Financial year : Period of time between July 1st and June 30th of the next year Balance sheet : State of the financial situation on a given date. The balance sheet presents the whole of the assets (what one possesses) and of the liabilities (what one owes). The total of the assets must always balance with the total of the liabilities. General ledger : Represents the whole of the accounting accounts used by the entity (see ACC-9 for more details) Sub-ledger : Revenue journal « revenue » (cash inflow) and journal of the « Expenses» (disbursements).")

12

Terminology (continued) Petty cash: Sum of money serving to pay certain expenses such as stationery, stamps, etc… The petty cash must be regularly reconciled and must appear in the balance sheet in the end of the financial year. Each expense must be supported by a receipt. The petty cash is optional, depending on operational needs of the Squadron. (Buying office supplies, availability of the subscribers, etc.) Inventory: Register in which one writes the whole of the Squadron’s goods. This register must contain the date of procurement of a good, a brief description, the serial number and the amount paid.

Inventory: Register in which one writes the whole of the Squadron’s goods. This register must contain the date of procurement of a good, a brief description, the serial number and the amount paid..")

13

Section 2: Budget General: The budget must be prepared in conjunction with the Chair and the Commanding Officer of the Squadron and should be presented to the personnel as well as the parents of the cadets during the parents’ meeting scheduled in the fall of each year. The budget is a tool, a guide, in which projects are presented as are the ways the funds collected will be spent. It serves as a map that indicates the trip for the year ahead. To reach our objectives …. We need a plan… The BUDGET is the solution !

14

DESCRIPTION OF THE BUDGET PROCEDURE Determination of the objectives (recruiting objective, cadet retention activities, material purchases, etc) Chair and Commanding Officer Acceptation of the common objectives June - July Preparation of the cadet activities program (sending the program to the RCSU (East) begining of September) Commanding Officer and Training Officer (Inform the President) June – July - August Preparation of the financing activities (L’Auto-Cadet lottery, packaging, car wash, etc.) Chair and Executive committee and/or Directors (Inform the Commanding Officer) June – July - August Make the budget of mandatory activities (DND) following guidelines for the activities Plan emitted by the RCSU (East) (before called ATD) Commanding Officer and Officers July - August Make the budget of optional activities and financial obligations of the Squadron (occupation fees) Chair and Treasurer July - August Mix the two budgets (civil and military) and final adjustments. Adoption of the budget during session Chair, Commanding Officer, Treasurer August - September Preparation of the presentation to the personnel, parents, and senior cadets Chair and Commanding Officer September Application of the budget and implementation of the activities All September to June Revision of the budget (identification of the anomalies and finding solutions for them) Chair and Commanding Officer January

Chair and Commanding Officer January.")

15

Sources of information for the preparation of the annual budget 1.Financial statement of the previous financial year (ACC-9) a)Identification of the source for funds (financing activities) b)Identification of the expenses of funds (cadet activities) 2.Annual Operation Directive (AOD) emitted by RCSU (EAST) (http://www.cadets.ca/regions/est/content-contenu.aspx?id=60712&terms=aod) Specifies the yardsticks that will be used by RCSU (East) (Regional support Cadet Unit – Eastern Region) for the re-imbursement of the expenses related to the cadet activities (mandatory and optional) 3.Effective strength for the year a)The effective strength is the fundamental element on which certain revenues and expenses are based (i.e.: L’Auto-Cadet, summer camp, military personnel, yardstick for re-imbursement)

a)Identification of the source for funds (financing activities) b)Identification of the expenses of funds (cadet activities) 2.Annual Operation Directive (AOD) emitted by RCSU (EAST) ( id=60712&terms=aod) Specifies the yardsticks that will be used by RCSU (East) (Regional support Cadet Unit – Eastern Region) for the re-imbursement of the expenses related to the cadet activities (mandatory and optional) 3.Effective strength for the year a)The effective strength is the fundamental element on which certain revenues and expenses are based (i.e.: L’Auto-Cadet, summer camp, military personnel, yardstick for re-imbursement)")

16

4.Local activities program a)Allows to identify periods of the year when the Squadron’s activities will take place b)Identification of the needs for resources (material, financial and human) 5.Bank statement and Bank reconciliation a)Allows to know the sum of money that will serve to cover certain expenses before the first financing activities begin. 6.Identification of the flexibility (cash flow) essential to the smooth functioning of the Squadron’s activities. Fixing a cash flow budget on a monthly basis that permits to identify at which moment during the year are previewed the income and outgoings of funds (ex: financing campaigns from September to December and the majority of expenses happen between January to June)

essential to the smooth functioning of the Squadron’s activities. Fixing a cash flow budget on a monthly basis that permits to identify at which moment during the year are previewed the income and outgoings of funds (ex: financing campaigns from September to December and the majority of expenses happen between January to June).")

17

Section 3: Bookkeeping Accounting of the accounts entry according to the cash accounting 1st step : Familiarize oneself with the chart of account used for the ACC-9 and add particularities specific to the Squadron. 2 nd step: Account all revenues and expenses regularly in the corresponding accountable accounts of the auxiliary books (Revenues sub-ledger or the Expenses sub- ledger of the ACC-9)

.")

18

INTERNAL CONTROL TWO (2) MAIN OBJECTIVES: Minimize losses: Protect the Squadron’s goods (lock, inventory) List of cadet names (name, address, telephone) Maximize revenues: Plan, organize an control the different financing activities (Identification of the need in material human and financial resources)

MAIN OBJECTIVES: Minimize losses: Protect the Squadron’s goods (lock, inventory) List of cadet names (name, address, telephone) Maximize revenues: Plan, organize an control the different financing activities (Identification of the need in material human and financial resources)")

19

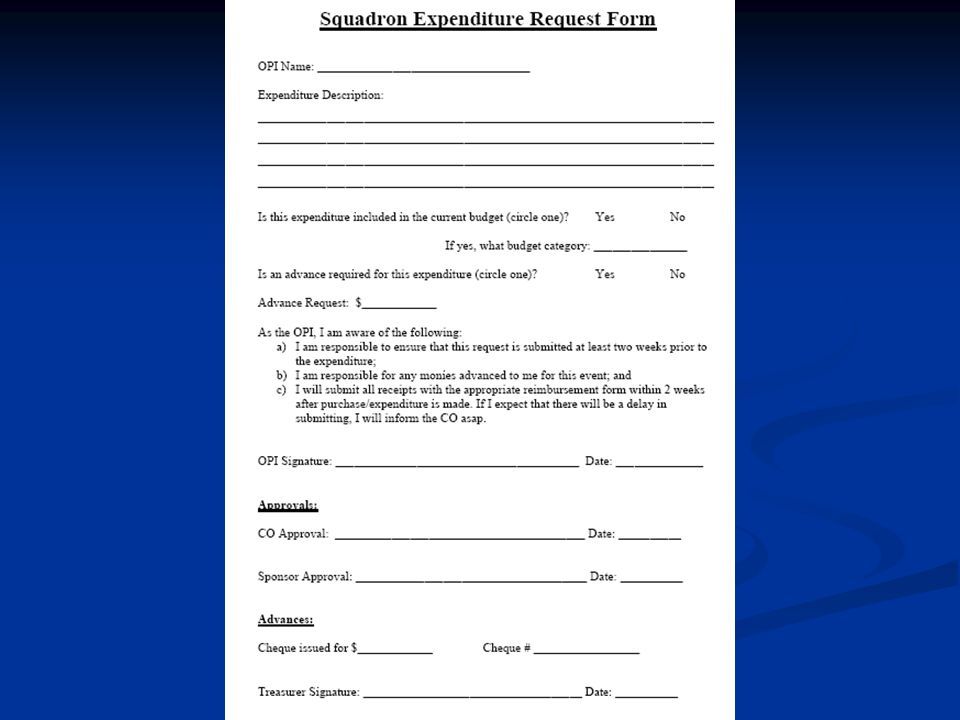

a) DISBURSMENTS All payments done by the Squadron must correspond to the following criteria: Be accompanied of a bill The good or service must have been pre-authorized by the Commanding Officer and/or the Chair The expense must be planned in the budget All payments must be done by check and must be counter-signed by two authorized signatories by the sponsoring committee (Chair and/or the Treasurer and the vice-chair). The signatories must not be related (i.e.: spouses) Have the required funds available at the moment of payment (never do a check with insufficient funds (NSF)).

Have the required funds available at the moment of payment (never do a check with insufficient funds (NSF))..")

22

INTERNAL CONTROL b)CASH INFLOW Since most of the cash inflows are done with cash, it is important to put in place a system of internal control that, while being simple to put into practice, insures a minimum of internal control and discourages tentative for embezzlement. Practical examples for Squadrons: Cadet Lotteryduration: ~6 months (September to ?) Packagingduration: 4 days (Thursday to Sunday) Tagging duration: twice a year ? Canteen duration: during the whole year

Packagingduration: 4 days (Thursday to Sunday) Tagging duration: twice a year . Canteen duration: during the whole year.")

23

Fundraising campaign L’Auto-Cadet Lottery This financial resource being common to all, it is important to reduce the losses that can happen during the few months in which the campaign lasts. i.Have the cadets sign when the tickets are handed to them Recommendation: For recruits, only allow 10 tickets at once in the objective of reducing losses to a minimum ii.Transmit a letter to parents giving them information concerning the financing campaign and to sensitize them to the cause iii.When cadets hand in the money for their tickets, they must endorse this by putting their initials on the control document

24

Tagging : This activity normally lasts a week-end and has the advantage of being of short duration at the same time as revenues are maximized. i.Ensure yourself to have a sufficient amount of cadets and of supporting personnel (military or civil) to ensure service at each working period ii.Cumulate donations after each shift and keep an accounting up to date for the activity (for statistic purposes) iii.Possibility of selling back the money (coin rolls) to the commerce at the end of the activity iv.Always have multiple people handling the money. Transparency! v.Make a deposit in the shortest delays possible. If possible, make a deposit each day to avoid robbery or losses

to ensure service at each working period ii.Cumulate donations after each shift and keep an accounting up to date for the activity (for statistic purposes) iii.Possibility of selling back the money (coin rolls) to the commerce at the end of the activity iv.Always have multiple people handling the money. Transparency. v.Make a deposit in the shortest delays possible. If possible, make a deposit each day to avoid robbery or losses.")

25

DEMANDS FROM THE MILITARY PARTNER Follow-up on requests for refunds (CDT 135): The military partner demands that requests for refunds be submitted on a specific form called CDT 135. The treasurer completes this form and sends it to the Commanding Officer. The government requires that this form be accompanied by original documents (*) and must mention that they are paid (balance is at zero, copy of both sides of the check). You must keep a copy on file of all the documents that will be submitted to the RCSU (East). The delay for refunding is about 45 days. The Squadron must pay this charge before being refunded. The management for the cash flow of the treasury takes here all its importance. (*) including the numbers for GST, QST

and must mention that they are paid (balance is at zero, copy of both sides of the check). You must keep a copy on file of all the documents that will be submitted to the RCSU (East). The delay for refunding is about 45 days. The Squadron must pay this charge before being refunded. The management for the cash flow of the treasury takes here all its importance. (*) including the numbers for GST, QST.")

26

Section 3: Bookkeeping (continued) Other elements to be considered: The sponsoring committee cannot engage the Squadron towards financial obligations that exceed a (1) year. (ie: lease, contract of equipment rental – photocopier rental, etc) The mandate if the sponsoring committee is renewable each year during elections (June)

The mandate if the sponsoring committee is renewable each year during elections (June).")

27

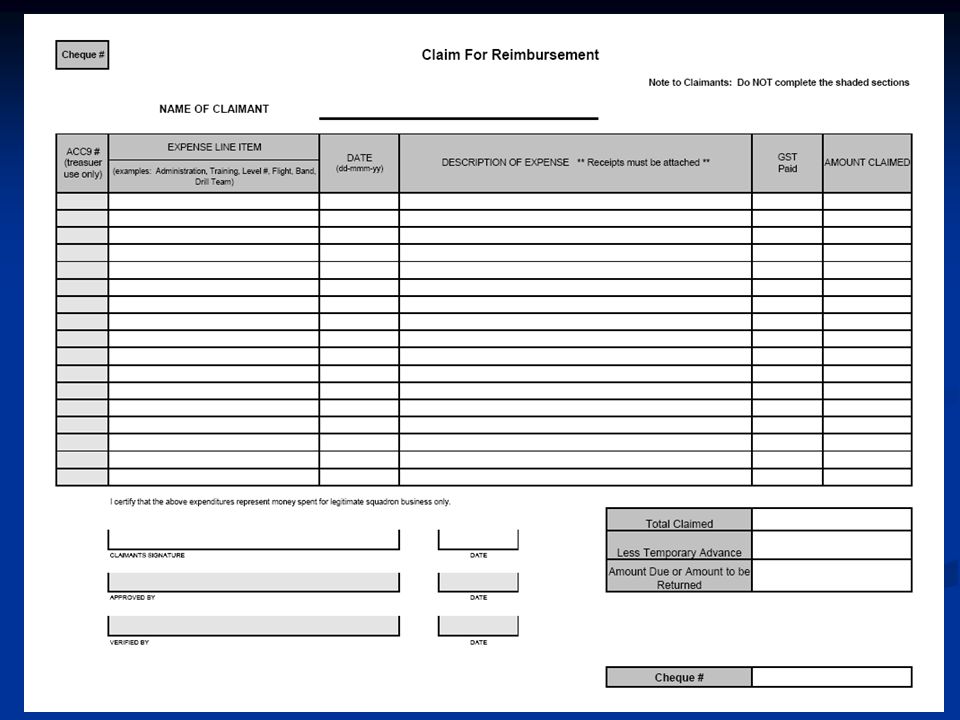

The Annual Financial Report– ACC-9 The ACC-9 is a financial report system designed using Excel that can meet ALL of your Squadron’s financial reporting needs through out the year. It includes: Journals for both expenses and revenues Monthly financial report capability Budget tracking and budget estimations Yearly financial report Produces the financial numbers for the Revenue Canada Registered Charity Report (T3010-1) Calculates both the GST rebate and Provincial Tax rebate (if applicable – registered charities only) Sample

Calculates both the GST rebate and Provincial Tax rebate (if applicable – registered charities only) Sample.")

28

There are now 3 versions of the ACC-9 to use. Which one is right for you? Multi Bank Account version (acc9mv14.0.xls) Multi Bank Account version (acc9mv14.0.xls) for SSCs that operate with two or more bank accounts. for SSCs that operate with two or more bank accounts. Single Bank Account version (acc9sv14.0.xls) Single Bank Account version (acc9sv14.0.xls) for SSCs that operate with only one bank account for SSCs that operate with only one bank account Paper Version (acc9p_e.pdf) Paper Version (acc9p_e.pdf) for SSCs that prefer to use another accounting program and just fill in the yearly report. for SSCs that prefer to use another accounting program and just fill in the yearly report.

Multi Bank Account version (acc9mv14.0.xls) for SSCs that operate with two or more bank accounts. for SSCs that operate with two or more bank accounts. Single Bank Account version (acc9sv14.0.xls) Single Bank Account version (acc9sv14.0.xls) for SSCs that operate with only one bank account for SSCs that operate with only one bank account Paper Version (acc9p_e.pdf) Paper Version (acc9p_e.pdf) for SSCs that prefer to use another accounting program and just fill in the yearly report. for SSCs that prefer to use another accounting program and just fill in the yearly report..")

29

Annual Financial Report– ACC-9 Website of the Air Cadet League of Canada (National) http://www.aircadetleague.com/ Website of the Air Cadet League of Canada (Quebec and Ottawa Valley) http://qc.liguedescadetsdelair.ca/ http://qc.liguedescadetsdelair.ca/ Website of the Ottawa Valley ACL http://ottawavalleyacl.com

Website of the Air Cadet League of Canada (Quebec and Ottawa Valley) Website of the Ottawa Valley ACL")

30

Section 5: GST and Provincial Taxes General Rules Most of the sales are exonerated (non-taxable), You can demand a partial refund (50%) of the GST that you have paid for purchases and admissible expenses Provincial Office must submit a GST-10 form that gives permission for a Squadron to claim a GST rebate For Provinces with HST, you may be able to claim back part of the provincial tax portion of the HST (RC7066-SCH) For example, in Ontario, Squadrons can claim 82% of the Provincial portion of taxes paid. Example: Squadron total HST paid for the year: $2000 GST Rebate: #384.62Provincial Rebate: $1009.23

32

Admissible Expenses: General fees of exploitation (rent, public services, administration fees) Certain allocations and refunds paid to employees or voluntaries Goods or services bought that are used, consummated or furnished for your exonerated activities Non- Admissible Expenses : Alcoholic beverages and tobacco products

Certain allocations and refunds paid to employees or voluntaries Goods or services bought that are used, consummated or furnished for your exonerated activities Non- Admissible Expenses : Alcoholic beverages and tobacco products")

33

GST Refund: Can go back up to 4 years to claim rebate Frequency: Should be done Annual at year-end Forms: GST ; FPZ - 66 (first time), GST-284 sent by CRA after that. QST ; VDZ – 387 Provincial Rebate: Can go back to when HST came into effect

34

Section 6: Registered Charity Information Return (Federal T-3010, Provincial TP-985.22 (Quebec Only)) As a Registered Charity, you have an obligation of producing an annual declaration (federal and provincial) at the latest 6 months following the end of the fiscal year. If you do not produce this declaration in a timely manner, CRA can revoke your charity status. The consequences can be: you can’t give out charitable donation receipts a fine of 500$ to get your status reinstated loss of all of your funds if a revocation audit is done The ACC-9 automatically calculates all of the financial section numbers for the T3010.

35

Official Charitable Donations Receipts Must carry the mention "Official Receipt for Income Tax Purposes" Receipt must be numbered (sequential order) Name and address of the Squadron (As it is written in the record) Registry number (ex: 123613523RRxxxx ) Date of reception of the donation (day or year of reception of donation) Total amount received by the charitable organization The name and address of the donor Place and date where the receipt was delivered Authorized signature (Chair, Treasurer) Link to access the Site of the Canada Revenue Agency (http://www.cra-arc.gc.ca/tx/chrts/menu-eng.html)

Name and address of the Squadron (As it is written in the record) Registry number (ex: RRxxxx ) Date of reception of the donation (day or year of reception of donation) Total amount received by the charitable organization The name and address of the donor Place and date where the receipt was delivered Authorized signature (Chair, Treasurer) Link to access the Site of the Canada Revenue Agency (")

36

www.cra.gc.ca/charities www.cra.gc.ca/charities www.cra-arc.gc.ca/chrts-gvng/chrts/pbs/rcpts-eng.html#sample1 www.cra-arc.gc.ca/chrts-gvng/chrts/pbs/rcpts-eng.html#sample1 http://fr.nebs.ca/onlinestore/20071116001/handwritten-forms/receipt- books/non-profit-receipts/p-13496-c-10907222.htm http://fr.nebs.ca/onlinestore/20071116001/handwritten-forms/receipt- books/non-profit-receipts/p-13496-c-10907222.htm

37

Record and Conservation Keeping - Fiscal Damaged receipts must be kept with their duplicate and bear the mention "CANCELLED" If a receipt must be replaced, the new receipt must bear the mention "REPLACED", followed by the serial number of the replacing receipt A copy (duplicate) of the receipts for tax purposes must be kept with the governmental reports (federal and provincial) The registries from the Squadron and the conviction pieces of the information that they contain must be kept in the eventuality of a verification.

of the receipts for tax purposes must be kept with the governmental reports (federal and provincial) The registries from the Squadron and the conviction pieces of the information that they contain must be kept in the eventuality of a verification.")

38

Section 7: Useful Information and Calendar Calendar of the Treasurer June– July – August: Payment of the received bills during the summer season and ensuring that no account is overdue to the furnishers. Finalize account entries for the end of the fiscal year Reconcile the petty cash of the Commanding Officer Registering the accounts entry (bank statement) Preparation of the budget (see schedule – Section 2) Plan the research of sponsors and plan subventions Handing in the ACC-9 to the League Head-Quarters (August 31st) September: Approbation of the annual budget and preparation of the budget presentation Send the demands for refunds for the GST and QST

Preparation of the budget (see schedule – Section 2) Plan the research of sponsors and plan subventions Handing in the ACC-9 to the League Head-Quarters (August 31st) September: Approbation of the annual budget and preparation of the budget presentation Send the demands for refunds for the GST and QST.")

39

October: Registering account entries (bank statement) for the monthly meeting (Chair – Commanding Officer) Putting the Squadron’s inventory of the goods up-to-date November: Registering account entries (bank statement) for the monthly meeting (President – Commanding Officer) 15th of November First hand-out of the l’Auto-Cadet Lottery December: Registering account entries (bank statement) for the monthly meeting (President – Commanding Officer) Deadline for cash inflows relative to charity donations (December 31st) Conciliation of the petty cash Inventory of the cadet’s cafeteria December 31st Deadline for mailing in of T-3010 form and sending of the Charitable Donations Receipts to donors (for fiscal purposes)

for the monthly meeting (Chair – Commanding Officer) Putting the Squadron’s inventory of the goods up-to-date November: Registering account entries (bank statement) for the monthly meeting (President – Commanding Officer) 15th of November First hand-out of the l’Auto-Cadet Lottery December: Registering account entries (bank statement) for the monthly meeting (President – Commanding Officer) Deadline for cash inflows relative to charity donations (December 31st) Conciliation of the petty cash Inventory of the cadet’s cafeteria December 31st Deadline for mailing in of T-3010 form and sending of the Charitable Donations Receipts to donors (for fiscal purposes)")

40

January: Registering account entries (bank statement) for the monthly meeting (President – Commanding Officer) *** Revision of the annual budget *** 2 nd hand-out of the L’Auto-Cadet Lottery Do a post-mortem of the financing campaigns and do a report to the committee on proposed improvements February: Registering account entries (bank statement) for the monthly meeting (President – Commanding Officer) Beginning February Finalization of the campaign of L’Auto-Cadet Lottery

for the monthly meeting (President – Commanding Officer) *** Revision of the annual budget *** 2 nd hand-out of the L’Auto-Cadet Lottery Do a post-mortem of the financing campaigns and do a report to the committee on proposed improvements February: Registering account entries (bank statement) for the monthly meeting (President – Commanding Officer) Beginning February Finalization of the campaign of L’Auto-Cadet Lottery")

41

March: Registering account entries (bank statement) for the monthly meeting (President – Commanding Officer) Ensure all the refunding bills have been handed in to the Commanding Officer going to the RCSU (East) (Cdt 135) (keep a copy on file for your records) Put your financial forecast until the end of the calendar up-to-date. Review expenses relative to the Annual Review as well as the year end trip (if applicable) April: Registering account entries (bank statement) for the monthly meeting (President – Commanding Officer) Review stocks rotation of the cafeteria. Maintain purchases to a minimum (stay away from merchandise loss)

April: Registering account entries (bank statement) for the monthly meeting (President – Commanding Officer) Review stocks rotation of the cafeteria. Maintain purchases to a minimum (stay away from merchandise loss).")

42

May: Registering account entries (bank statement) for the monthly meeting (President – Commanding Officer) Maintain a control over expenses. The volume of transactions tends to increase during this very busy part of the year. Update regularly financial forecast

43

Section 8: Additional Resources Website: http://ottawavalleyacl.com http://ottawavalleyacl.com Training Videos: http://ottawavalleyacl.com/ovacl/acc-9.php Training Videos: http://ottawavalleyacl.com/ovacl/acc-9.php Select English Training Videos Email: ov.coord@rogers.com ov.coord@rogers.com

44

CONCLUSION A JOB WORTH DOING ….. IS WORTH DOING WELL!

Similar presentations

>")

, You can demand a partial refund (50%) of the GST that.>")