Download presentation

Presentation is loading. Please wait.

1

Setting a political budget Councillor Alan Waters, Deputy Leader, Norwich City Council Learning & Development Manager LGIU

2

National Picture The Political Context

3

Local Government Finance – The Context Local government grants from central government will reduce as a contribution to the overall deficit reduction programme. Reductions in government grants confirmed to 2015/16 and can be anticipated at least up to 2017/18 and beyond! Schools funding is the exception and is currently protected, but ring-fenced – mostly removed from Local Government control Incentives for economic growth: Community Infrastructure Levy; New Homes Bonus; Localisation of Business Rates Impact of Localism and Localism Act.

4

Cuts in central government grant: why are poorer areas most affected? Councils with a low council tax base (lower tax banded properties) need more grant (RSG) than councils who have a large number of properties in higher tax bands. Impact of Localisation of Council Tax Benefits Effect of reliance on economic growth for funding New Homes Bonus

need more grant (RSG) than councils who have a large number of properties in higher tax bands. Impact of Localisation of Council Tax Benefits Effect of reliance on economic growth for funding New Homes Bonus.")

5

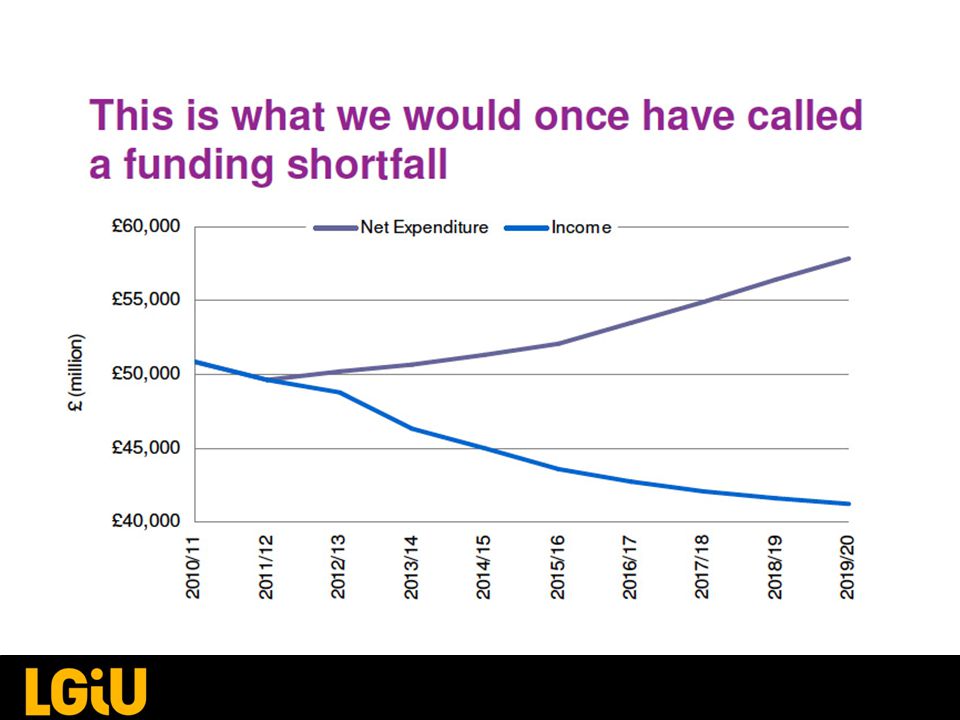

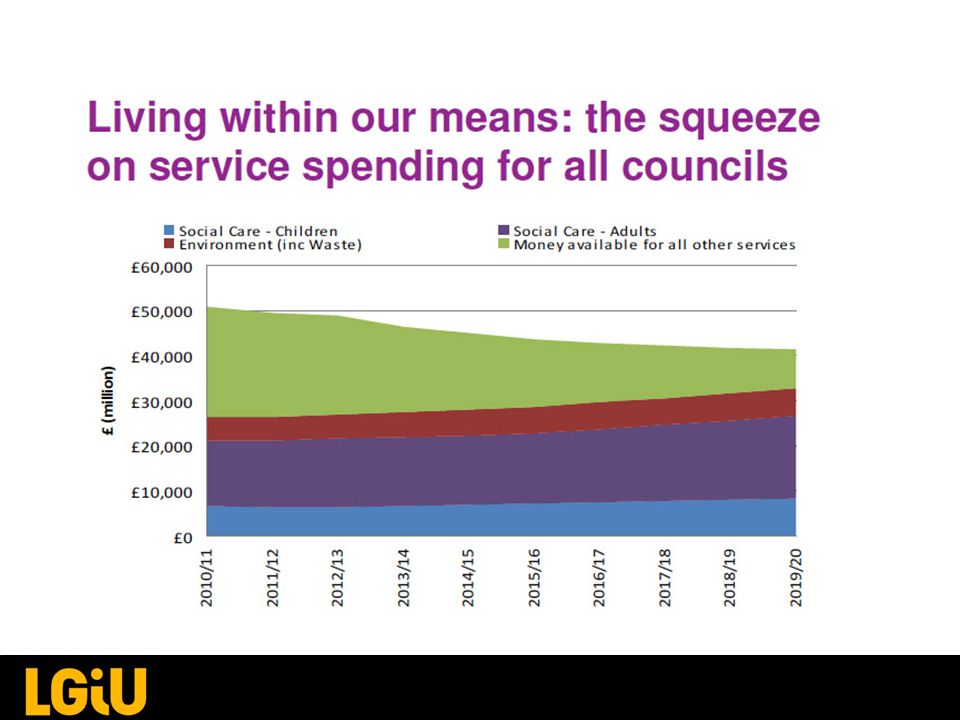

LGA Funding projections 2010 - 2020

11

Education and Public Health Education School funding largely removed from local authorities either through DSG or Academy/Free Schools models, though responsibility for some services and early years remains Public Health Now the responsibility of Local Authorities Funded from a ring-fenced government grant for 2013/14 and 2014/15

12

The wider £ implications: welfare reform Implementing Welfare Reform – e.g. Localisation of support for Council Tax Housing benefit cap & ‘bedroom tax’ Pressures on services from the impact of Welfare reform changes Impact on local economy

13

Reducing budgets – Government view. Savings can be made through - different types of partnership working to deliver “affordable services” - more “outsourcing & private sector practices” - “Community budgets”

14

‘Look after the pennies’: don’t overspend on bottled water!

15

Why is local government being treated so badly? Ring-fencing of NHS, schools, International development; growth in welfare budget Local government unprotected & hostile Secretary of State at CLG Local Government has shown that “it can take it” – so government will continue to cut.

16

Issues of financial viability Audit Commission 43% larger single tier councils 34% district councils Short or medium term risk of not being financially viable

17

The Pickles Plan Reason for the frontloaded cuts It is important that local government restructure its administration and its services, and the only real way to do that is to start the process early on’ Eric Pickles – CLG Select Committee 2010

18

The Government’s ‘Vision’. “Even if there was 10% growth next year we would still want to shrink the State” Brandon Lewis, Under Secretary of State for Local Government

19

Key political point in managing the cuts The Poll Tax question…….. WHO GETS THE BLAME?

20

BACK TO BASICS How the system works

21

Back to Basics The law Capital and Revenue The General Fund and the Housing Revenue Account

22

The Law Local Government Act section 151 –The council must make provision for effective financial management –The “Section 151 Officer” The Local Government Act 2003 –Medium Term Financial Strategy –“Balanced” and “robust” budget with “adequate” reserves –Councils must follow “proper accounting practice” Important residents know that you are running a tight ship.

23

The Law Localism Act 2011 –Local referendum on “excessive” rises in Council Tax Local Government Finance Act 2012 –Business Rates Retention –Local support of Council Tax –Changes on Council Tax for empty and second homes

24

Four Budgets General Fund budget ( under most pressure) Non-Housing Capital Programme Housing Revenue Account Housing Capital Programme

Non-Housing Capital Programme Housing Revenue Account Housing Capital Programme")

25

Capital and Revenue Revenue Running costs expenditure – under 1 year useful life Employee costs, maintenance and repairs, utility bills, supplies and services Income sources CAN be spent on capital expenditure Capital Expenditure on funding and improving assets – over a 1 year life New build, renovation, new vehicles and infrastructure Most councils have a “de minimis” level before expenditure becomes capital Income sources CANNOT be spent on revenue expenditure

26

General Fund and HRA Housing Revenue Account Only required if council is a “landlord” to housing tenants (including ALMOs) Therefore not required if council has sold its housing stock to an RSL Income and expenditure is “ring-fenced” General Fund All other services Will include non-landlord based housing services e.g. some housing benefits, support to RSLs

27

HRA Funding New system from April 2012 for councils with their own housing stock. In exchange for taking a “one off” distribution of housing debt able to invest housing rents in upgrading and building new homes. Councils developing long term investment plans for their housing stock & some modest new build.

28

But.. Changes to the RTB scheme may reduce councils housing stock and the variety of homes it owns ‘Help to buy’ – which may already be pumping up house prices - could have built 175,000 new affordable homes. A cap on Housing Revenue Account borrowing – loss of estimated new build of 66,000 council houses.

29

General Fund Revenue – Key Issues Council Tax Business Rates and Government Grants The New Homes Bonus Fees and charges Reserves and Balances

30

Council Tax Local referendums for “excessive” increases – 2% for 2014/15 Council Tax Freeze Grants available from 2011/12 through to 2014/15 Freeze grant now part of the council’s base funding, but below inflation increases still erode the Council Tax base Any support for Council Tax is a discount and so also affects the Council Tax base

31

Council Tax – always newsworthy! Last year some councils not taking the council tax freeze grant got attacked for hitting “the hard pressed local taxpayer”. Important to get public endorsement for CT decision

32

Business Rate Retention All councils benefit from any above inflation increases in business rates income However, the percentage retained locally varies between councils The level of (and collection rate for) business rates is now very important for councillors to understand

business rates is now very important for councillors to understand")

33

Government Grants – the SUFA Start-Up Funding Assessment The new way Government funding works…. SUFA = Formula Grant + Specific Grants that have been “rolled in”

34

An example - LB Ealing’s SUFA 2013/14 £000 Revenue Support Grant101,248 Business Rates – Individual Authority Baseline (30% of Business Rate) 39,190 Business Rates – Top-Up28,168 Start-Up Funding Assessment168,606

39,190 Business Rates – Top-Up28,168 Start-Up Funding Assessment168,606")

35

The New Homes Bonus Commenced in 2011/12 “Match funding” for every new home and existing homes brought back into use Funding available and builds over 6 financial years Individually calculated, but included within your SUFA “Top-sliced” in London, but not elsewhere

36

Fees and Charges Check the legal position – some services must be free at the point of delivery The Local Government Act 2003 enables a council to charge for all “discretionary” services Under the LGA 2003 the charge can cover the full cost including overheads and depreciation Do you know how what services you subsidise and are you clear why?

37

Investment Interest Councils invest all surplus revenue and capital money to earn interest All interest can be used to support revenue spending Each authority has a Treasury Management Policy and investment strategy to determine where money is invested The balance between “risk” and “return” is key

38

Reserves and Balances All councils retain a variety of different reserves LGA 2003 requires council to agree a minimum level of balances as part of its budget setting process All reserves (including capital reserves) attract interest that can be used to fund revenue and capital expenditure Note: the level of reserves is set by assessing risk or uncertainty facing a council Also allows the council to ‘buy time’.

attract interest that can be used to fund revenue and capital expenditure Note: the level of reserves is set by assessing risk or uncertainty facing a council Also allows the council to ‘buy time’.")

39

Capital Funding Capital receipts Borrowing – “affordable” and “prudent” Capital Grants “Section 106” agreements The Community Infrastructure Levy Revenue contribution

40

Contributions from Developers Town and Country Planning and Land Act 1990 section 106 –A contractual agreement between council and developer to fund public realm etc. in a development –Individually negotiated Community Infrastructure Levy –A tariff based charging scheme –A proportion must be spent locally

41

What is the role of elected members in the budget process?

42

Member Involvement in the budget process Why should elected members involve themselves in the budget process?

44

Elected members legal obligations Local Government Act 2000 – responsibility of the full council to approve the budget and council tax demand Executive must act within the budget Local Government Act 2003 – council required to prepare a medium term financial plan and Chief Finance Officer required to make formal report to members when considering the budget Section 151 officer Section 114 1988 Act re unlawful expenditure or unbalanced budget

45

Member Involvement ‘Budget planning, setting, scrutinising and monitoring can be a time-consuming exercise but it is important that all councillors are involved in or take an interest in the budget process’. (Councillor’s Guide LGA)

.")

46

Member involvement ‘ The budget process concerns choices that may be : -Politically led -Policy led -Aimed at redirecting the way existing services spend -An aid to cross-party working’ The key thing for a councillor is to ensure that the strategy and policies agreed by the council influence and inform the budget setting process ( LGA: Councillor’s Guide 2011/12)

")

47

Activity: Member Involvement What part do each of the following play in the Budget process: The ruling group on the council Cabinet members The opposition groups on the council Scrutiny members Ward Councillors Newly elected councillors

50

Planning corporate strategy direction makes clear the priorities and aims of the organisation. Have strong headlines. service planning translates them into measurable actions capital planning integrated into medium and long term financial planning Important to have good information to help decide on budget priorities. A service planningA

51

QUESTION What does ‘growth’ mean in an overall cuts budget?

52

Audit Commission research Is there something I should know? encourages decision makers to be more demanding about the information they seek and use when making decisions

53

Value for Money Value for money is a balance of cost, output and outcome Do you have the information you need to evaluate whether a service provides value for money? How do you compare with other providers (council, private sector, third sector?) Best Value & Social Value Act

Best Value & Social Value Act.")

54

Constructing the annual budget ‘Front line and back office’ : “Front-Line” Services Running costs + Support Service charges = Total expenditure - Income from fees and charges = Net Expenditure “Central” Service Running costs + Support Service charges = Total expenditure - “Recharges” = 0 Financed by Council Tax and SUFA

55

Statutory Services: Services which a local authority are obliged by statute to provide Non – Statutory (‘discretionary’) Services which an authority has the power but not the duty to provide A word about Statutory and Discretionary services

Services which an authority has the power but not the duty to provide A word about Statutory and Discretionary services")

56

Not a straight forward choice Cut all the discretionary services to protect statutory responsibilities? - but many ‘discretionary’ services very popular – leisure; grants; parks and generate income (car parks) - and what level should Statutory services be funded at?

- and what level should Statutory services be funded at .")

57

Plan B? The case for the proper funding of local government in Greenwich

58

LGIU/MJ annual survey on local government finance Survey of 130 councils - 80% want the freedom to set council tax locally rather than another ‘deal’ - 45% wanted to see additional taxes localised - 90% not intending to employ TIF - 80% Community Infrastructure levy would not offer benefits.

59

Funding transfers rather than cuts By 2013/14 the Spending Review will have cut grants to councils by £4.3bn; while corporation tax to companies has been cut by £3.75bn. Not forgetting lost tax revenues….

61

Macro Economics Fiscal Multipliers & the IMF Then £10bn of spending cuts will reduce GDP by around £5bn and now…. £10bn of spending cuts will reduce GDP by between £9bn and £17bn).

..")

62

Importance of making the case for Local Government Investment in public services and proper funding for local government is key to economic growth and stability.

63

Local multipliers Government acknowledges the importance of local government – stimulating private sector activity (reluctantly!) Benefits of public expenditure: Every £1 of public money invested public services a further 64 pence is generated in the local economy. Real Wages stagnated to 2003 levels Welfare benefit changes millions lost to local economies Multiplier 2*: For every public sector job.4 of a job created in the private sector

64

Spending Review bids: the LGA approach Removal of council tax restrictions End ring-fencing for health and schools budgets Increase in the local share of business rates Set fees and charges locally. More control and expansion of growth funds & more of the benefits retained

65

Spending Review bids Remove housing revenue account borrowing ceiling Investment fund for housing building More local control and support over the operation of welfare reforms and funding for ‘burdens’. Community budgets – preferred model of delivery method for government departments – devolve more central government funding to local government.

66

Reading Future funding outlook for Councils from 2010/11 to 2019/20 (LGA) Rewiring public services (LGA) The cuts: UK’s damaged future. A report for UNISON by CLES Consulting Municipal entrepreneurship (APSE)

.")

67

Final Comments

Similar presentations

April 2013. MTFP The MTFP is a high-level forecasting model that enables the Council to assess the financial direction.>")