Download presentation

Presentation is loading. Please wait.

1

presented by Carrie A. Gilchrist, Ph.D. Oakland University Choosing the Right Investments: Smart Saving for College

2

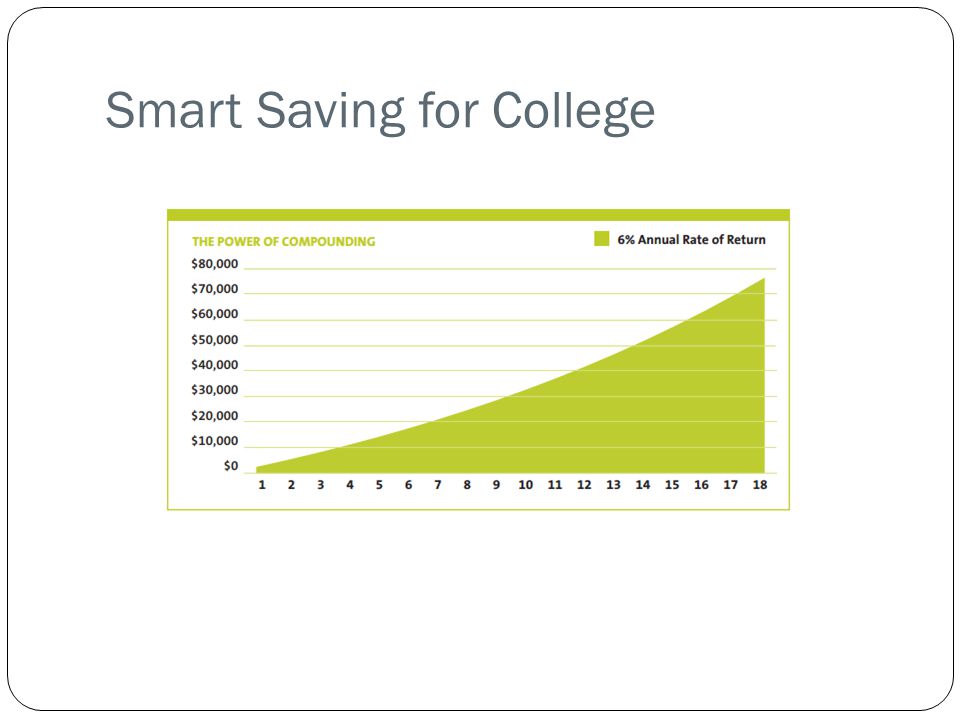

Smart Saving for College Do you know how much college costs? Do you know how much money you need to save? Do you know the many different tax advantaged ways to save for college?

3

Smart Saving for College Costs to consider: Tuition Housing – on or off campus Books Transportation Miscellaneous living expenses

4

Smart Saving for College

6

How will saving and investing affect my eligibility for aid? The impact on financial aid varies depending on whether the savings belong to the parent or the child. Savings in a parent’s name can reduce federal financial aid eligibility by at most 5.64% Assets saved in a child’s name can reduce aid eligibility by as much as 20% 529 accounts owned by a child or set up as a custodial 529 account are treated at the lower 5.64%

7

Smart Saving for College Education Benefits for Service members – Post 9/11 GI Bill Pays for education and housing costs for service members and veterans who served at least 90 days of aggregate service on or after September 11, 2001 Eligible veterans can claim benefits for up to 15 years after leaving the military Funds: undergraduate, graduate, on-the-job-training, apprenticeship programs, flight schools, and other non-degree seeking programs

8

Smart Saving for College Education Benefits for Service Members – Post 9/11 GI Bill Tuition and fee reimbursement All in-state tuition and fee charges are reimbursed at public institutions For private and foreign institutions have a benefit cap A stipend for books and supplies A monthly housing allowance Ability to transfer unused educational benefits to spouse and children

9

Smart Saving for College Tax-Advantaged Alternatives 529 plans Prepaid tuition plans College savings plans Coverdell Education Savings Accounts Custodial accounts UGMA/UTMA Savings bonds

10

Smart Saving for College 529 plans Contributions can vary and are only limited by the maximum and minimum contribution limits set by most plans. In most states, the maximum amount that you can contribute for one beneficiary exceeds $250,000. Number of investment options Common fees: Enrollment fee Annual maintenance fee Sales charge (Front-End Sales Load) Deferred Sales Charge Administration/Management Fee Underlying Fund Expenses

Deferred Sales Charge Administration/Management Fee Underlying Fund Expenses.")

11

Smart Saving for College Coverdell Education Savings Accounts Except for investing in life insurance contracts, you can buy and sell what you want whenever you want. Also, you can set them up at almost any brokerage firm, mutual-fund company or other financial institution. contributions are not deductible, but earnings in ESAs are tax-deferred, and withdrawals that are used for qualified education expenses are tax-free. tax-free withdrawals to pay for private elementary and high school expenses, as well as post-secondary school expenses Limited to $2000 in contributions per year

12

Smart Saving for College Custodial accounts Your investing options are virtually limitless and there are no contribution or income limitations. Withdrawals can be used for any purpose, not just qualified education expenses, without penalty. In tax year 2013, for children younger than 19 or younger than 24 if a full-time student, the first $950 of unearned income is tax-free. The next $950 is taxed at the child's federal tax rate. Any earnings over $1,900 are taxed at the custodian's federal tax rate. UGMA/UTMA

13

Smart Saving for College Savings bonds Backed by the full faith and credit of the United States government, the interest from these bonds is tax-free if used for qualified higher education expenses. Income limits apply

14

Smart Saving for College

15

College Tax Credits American Opportunity Credit This credit reduces the amount of income tax you may have to pay. available for four years of college and can be used for course materials, in addition to tuition and fees This credit has a maximum credit of $2,500 per student Student must be pursuing a degree, going to school at least half time and not have a felony drug conviction Income limits apply

16

Smart Saving for College College Tax Credits Lifetime Learning Credit Allows you to claim up to 20% of the first $10,000 paid for college tuition and fees, for a maximum credit of $2,000 per tax return There is no limit on the number of years you can claim the Lifetime Learning Credit Can be used for under-graduate and graduate courses and even for tuition and fees when the student attends half time. Income limits apply

17

Smart Saving for College Resources www.finra.org/college_calc www.studentaid.ed.gov www.fafsa.gov www.irs.gov www.collegesavings.org

18

Choosing the Right Investments

Similar presentations

>")