Download presentation

Presentation is loading. Please wait.

1

Capital Investment Decisions Management Accounting: The Cornerstone for Business Decisions Copyright ©2006 by South-Western, a division of Thomson Learning. All rights reserved.

2

Learning Objectives 1.Explain what a capital investment decision is and distinguish between independent and mutually exclusive capital investment decisions. 2.Compute the payback period and accounting rate of return for a proposed investment and explain their roles in capital investment decisions. 3.Use net present value analysis for capital investment decisions involving independent projects.

3

Learning Objectives 4.Use the internal rate of return to assess the acceptability of independent projects. 5.Explain the role and value of post audits. 6.Explain why NPV is better than IRR for capital investments decisions involving mutually exclusive projects.

4

How to calculate payback. Payback period = original investment / annual cash flow Suppose that an new car wash facility requires an investment of $120,000 and has either: a.Even cash flows of $40,000 per year or b. The following annual cash flows $20,000, $40,000, $40,000, $50,000, and $30,000 REQUIRED: Calculate the payback period for each case. Calculation: a.Even cash flows Payback period = original investment / annual cash flow = $120,000 / $40,000 = 3 years 13-1

5

b. Uneven cash flows Unrecovered InvestmentAnnualTime Needed Year(Beginning of the Year)Cash Flowfor Payback 1$120,000$20,0001.0 year 2100,00040,0001.0 year 360,00040,0001.0 year 420,00050,0000.4 year 5030,0000.0 year Total3.4 years At the beginning of year 4, $20,000 is needed to recover the investment. Since a net cash flow of $50,000 is expected only 0.4 year ($20,000 / $50,000 is needed to recover the remaining $20,000 assuming a uniform cash flow throughout the year). How to calculate payback. 13-1

Cash Flowfor Payback 1$120,000$20, year 2100,00040, year 360,00040, year 420,00050, year 5030, year Total3.4 years At the beginning of year 4, $20,000 is needed to recover the investment. Since a net cash flow of $50,000 is expected only 0.4 year ($20,000 / $50,000 is needed to recover the remaining $20,000 assuming a uniform cash flow throughout the year). How to calculate payback")

6

List Four Ways Payback Can be Used by Managers 1.To help control the risks associated with the uncertainty of future cash flows 2.To help minimize the impact of an investment on a firm’s liquidity problems 3.To help control the risk of obsolescence 4.To help control the effect the of the investment on performance measures

7

How to calculate the accounting rate of return (ARR). ARR = Average Income / Initial Investment Assume that an investment requires an investment requires an initial outlay of $140,000. The life of the investment is 5 years with following income stream: $30,000, $40,000, $40,000 $50,000, and $40,000. REQUIRED: Calculate the accounting rate of return. Calculation: Total net income (five years) = $200,000 Average net income = $200,000 / 5 = $40,000 Accounting rate of return = $40,000 / $140,000 = 0.35 or 35% 13-2

= $200,000 Average net income = $200,000 / 5 = $40,000 Accounting rate of return = $40,000 / $140,000 = 0.35 or 35%")

8

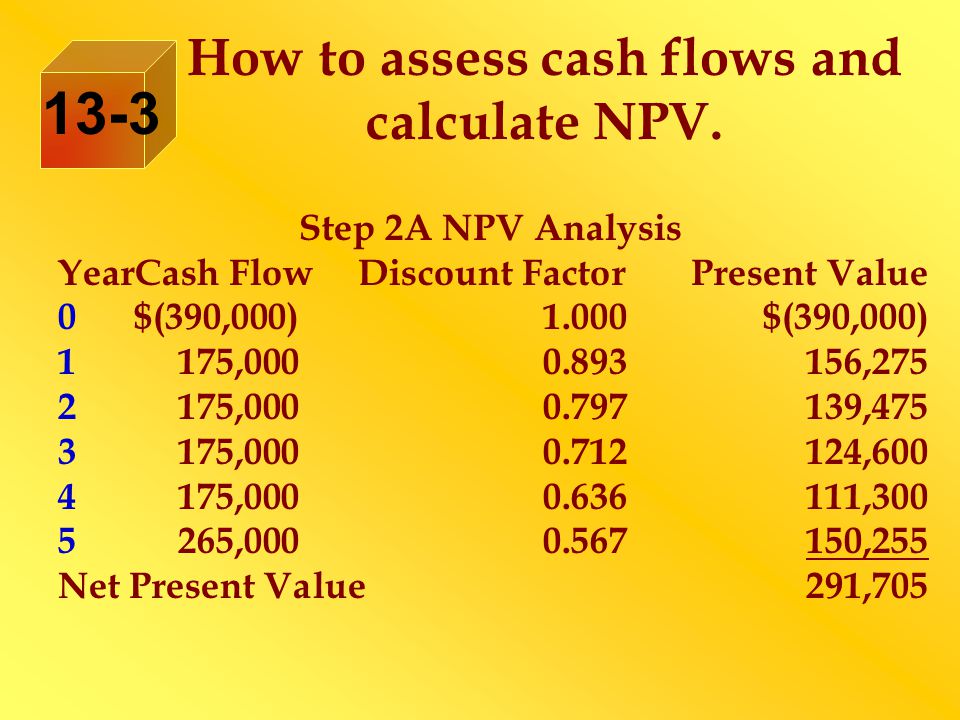

How to assess cash flows and calculate NPV. A market study revealed expected annual revenues of $320,000 for the new cordless headset. Equipment to produce the cordless headset would cost $350,000. After five years, the equipment can be sold for $50,000. In addition, to the equipment, working capital is expected to increase $40,000 because of increases in inventories and receivables. The firm expects to recover the investment in working capital at the end of the project’s life. Annual cash operating expenses are estimated at $175,000. The required rate of return is 12%. REQUIRED: Estimate the annual cash flows and calculate the NPV. 13-3

9

Step 1. Cash- Flow Identification YearItemCash Flow 0Equipment$(350,000) Working capital(40,000) Total$(390,000) 1-4Revenues$350,000 Operating expenses(175,000) Total$175,000 5Revenues$350,000 Operating expenses(175,000) Salvage value50,000 Recovery of working capital40,000 Total$265,000 How to assess cash flows and calculate NPV. 13-3

Working capital(40,000) Total$(390,000) 1-4Revenues$350,000 Operating expenses(175,000) Total$175,000 5Revenues$350,000 Operating expenses(175,000) Salvage value50,000 Recovery of working capital40,000 Total$265,000 How to assess cash flows and calculate NPV")

10

Step 2A NPV Analysis YearCash FlowDiscount FactorPresent Value 0$(390,000)1.000$(390,000) 1175,0000.893156,275 2175,0000.797139,475 3175,0000.712124,600 4175,0000.636111,300 5265,0000.567150,255 Net Present Value291,705 How to assess cash flows and calculate NPV. 13-3

11

Step 2B NPV Analysis YearCash FlowDiscount FactorPresent Value 0$(390,000)1.000$(390,000) 1-4175,0003.037531,475 5265,0000.567150,255 Net Present Value$291,255 How to assess cash flows and calculate NPV. 13-3

12

How to calculate IRR with Uniform Cash flows. Assume that a hospital has the opportunity to invest $160,000 in a blood analyzer that will produce a net cash flow of $57,184 in each of the next four years. REQUIRED: Calculate the IRR for the blood analyzer. Calculation: df = Investment / Cash Flow =$160,000 / $57,184 = 2.798 Since the life of the investment is four years, find the four row of Exhibit 13B-2 and then move across this row until df = 2.798 is found. The interest rate corresponding to 2.798 is 16%, which is the IRR. 13-4

13

Multiple Period Settings With Uneven Cash Flows The simple truth is performing IRR is one of the easiest tasks there is in Excel. It is a matter of listing outflows in a column as negative amounts and then in the same column inflows as positive amounts. Simply follow the directions in the Excel drop down box and it will take less than a couple of seconds to get a precise answer.

14

Define and Describe a Post Audit ◙ It is the follow up when the capital project is implemented. ◙ It compares the actual benefits with the budgeted benefits. ◙ It compares actual operating costs with the budgeted operating costs. ◙ It evaluates the overall outcome of the investment and proposes corrective action if needed.

15

What are the benefits of a post audit? 1.It ensures that resources are used wisely. 2.It has an impact on managers behavior. Because a post audit will be conducted, managers are more likely to make decisions in the best interest of the firm. 3.More objective results are obtained if the post audit is done by an independent party. 4.Post audits are costly to conduct.

16

Compare NPV to IRR

17

How to calculate NPV & IRR for mutually exclusive projects. Consider two pollution prevention projects. Design Papa and Oscar. Both have a project life of 7 years. Design Papa requires an outlay of $140,000 and has a net after-tax inflow of $40,000 (revenues of $180,000 minus costs of $140,000). Design Oscar, with an initial outlay of $300,000 has a net annual cash inflow of $50,000 ($240,000 - $190,000). The after-tax cash flows are summarized as follows: 13-5

. Design Oscar, with an initial outlay of $300,000 has a net annual cash inflow of $50,000 ($240,000 - $190,000). The after-tax cash flows are summarized as follows:")

18

Cash Flow Pattern YearDesign PapaDesign Oscar 0$(240,000)$(300,000) 140,00050,000 240,00050,000 340,00050,000 440,00050,000 540,00050,000 640,00050,000 740,00050,000 The cost of capital for the company is 12%. REQUIRED: Calculate the NPV & the IRR for each. How to calculate NPV & IRR for mutually exclusive projects. 13-5

19

Calculation:Design Papa: NPV Analysis YearCash FlowDiscount FactorPresent Value 0$(240,000)1.000$(240,000) 1-740,0004,564182,560 Net Present Value$(57,440) Design Papa: IRR Analysis Discount factor = Initial Investment / Annual cash flow = $240,000 / $40,000 = 6.000 From Exhibit 13B-2, df = 6.000 for 7 years implies that IRR = 4.000%. How to calculate NPV & IRR for mutually exclusive projects. 13-5

20

Design Oscar: NPV Analysis YearCash FlowDiscount FactorPresent Value 0$(300,000)1.000$(300,000) 1-750,0004,564228,200 Net Present Value$(71,800) Design Oscar: IRR Analysis Discount factor = Initial Investment / Annual cash flow = $300,000 / $50,000 = 6.000 From Exhibit 13B-2, df = 6.000 for 7 years implies that IRR = 4.000%. How to calculate NPV & IRR for mutually exclusive projects. 13-5

Similar presentations