Download presentation

Presentation is loading. Please wait.

1

Credit Suisse Global Leveraged Finance Conference March 28-30, 2006 - Phoenix, Arizona

2

/ 2 Forward Looking Statements This presentation contains forward-looking statements, which are subject to known and unknown risks and uncertainties that could cause the Company's actual results to differ materially from those set forth in the forward-looking statements. These risks include changes in customer demand for the Company's products, changes in raw material and equipment costs and availability, seasonal fluctuations in customer orders, pricing actions by competitors, and general changes in the economic environment. Currency Unless noted otherwise, all dollars are expressed in Canadian dollars. LTM Results are for the period ended December 31, 2005

3

/ 3 Mark D’Souza Vice President, Finance Jean-François Pruneau Treasurer Management Attendee

4

Quebecor Media Overview

5

/ 5 Key Highlights Strong Brand Names with Leading Market Positions Differentiated Bundled Product Offerings Significant Barriers to Entry Stable and Diversified Cash Flow Generation Experienced Management Team

6

/ 6 Corporate Structure Notes:Segmented revenues include inter-company revenues. Segmented EBITDA excludes head office. Vidéotron Telecom was merged with Vidéotron Ltée on 1/1/06. 54.7% Inc. 45.3% 45% Economic 99% Voting 100% 2005 Revenue :$2,703 2005 EBITDA :734 2005 Revenue: $1,002 2005 EBITDA: 382 2005 Revenue: $916 2005 EBITDA: 222 2005 Revenue: $401 2005 EBITDA: 53 2005 Revenue: $487 2005 EBITDA: 75 #1 Pay television operator in Quebec; #3 cable operator in Canada; #1 video store chain in Quebec Largest newspaper publisher in Quebec; second largest in Canada 100% ($ in millions) Book Retailing New Media Business Telecom Other Largest French language broadcaster and magazine publisher in Quebec and in North America

Book Retailing New Media Business Telecom Other Largest French language broadcaster and magazine publisher in Quebec and in North America.")

7

/ 7 Quebecor Media can reach 60% of English Canadians in major Canadian markets and 95% of French Canadians in Quebec on a weekly basis. Leading Market Positions Sources: BBM Survey (Sep 1 – Nov 30, 2004); NADbank 2003; PMB 2004; comscore (Media Metrix December 2004); CARD (Infopresse Annual Media Guide); IMS (Media Mix). National Presence #2 Newspaper publisher Leading content-focused national and local Internet portals Leading Market Position in Quebec #1 Newspaper publisher #1 Cable operator #1 High speed Internet service provider #1 Television broadcaster #1 Magazine publisher #1 Video store chain #1 Music producer/distributor/retailer #1 Internet portal

; NADbank 2003; PMB 2004; comscore (Media Metrix December 2004); CARD (Infopresse Annual Media Guide); IMS (Media Mix). National Presence #2 Newspaper publisher Leading content-focused national and local Internet portals Leading Market Position in Quebec #1 Newspaper publisher #1 Cable operator #1 High speed Internet service provider #1 Television broadcaster #1 Magazine publisher #1 Video store chain #1 Music producer/distributor/retailer #1 Internet portal.")

8

/ 8 Cable 52.1% Newspapers 30.3% Leisure and Entertainment 3.7% Broadcasting 7.2% Cable 37.1% Other & Inter-Segment 0.9% Broadcasting 14.9% Leisure and Entertainment 9.4% Newspapers 33.9% Corporate & Other 2.4% Business Telecommunications 3.8% Business Telecommunications 4.3% 2005 EBITDA 2005 Revenue Revenues = $2.7 billionEBITDA = $734 million QMI Diversified Financial Profile Note: Cable excludes Vidéotron Telecom, which was merged with Vidéotron Ltée on 1/1/06.

9

/ 9 QMI Strategic Focus Execute Residential and Mobile Telephony Strategy Generate Free Cash Flow Implement integrated on-line strategy Improve Productivity Target Accretive Acquisitions in Core Business Segments

10

/ 10 Notes: (1) Debt / EBITDA according to the Vidéotron credit agreement. (2) Debt / EBITDA according to the Sun Media credit agreement. (3) Debt / EBITDA according to the TVA credit agreement. Free Cash Flow and conservative leverage at the subsidiary level minimize debt at the holding level Free Cash Flow + Additional Debt Leverage (Debt / EBITDA) Current2.57x Leverage (Debt / EBITDA) Current 2.94x No debt 45% économic 99% voting 100% Editions QMI (1) (2) 58% économic 58% voting Leverage (Debt / EBITDA) Current 2.23x No debt (3) QMI Financing Strategy

Debt / EBITDA according to the Sun Media credit agreement. (3) Debt / EBITDA according to the TVA credit agreement. Free Cash Flow and conservative leverage at the subsidiary level minimize debt at the holding level Free Cash Flow + Additional Debt Leverage (Debt / EBITDA) Current2.57x Leverage (Debt / EBITDA) Current 2.94x No debt 45% économic 99% voting 100% Editions QMI (1) (2) 58% économic 58% voting Leverage (Debt / EBITDA) Current 2.23x No debt (3) QMI Financing Strategy.")

11

/ 11 Overview of Refinancing Plan – January 2006 With the recent refinancing of its high yielding Notes, QMI continued to take advantage of favourable credit momentum and market conditions to meet its capital structure objectives. ObjectivesRefinancing Impact Reasonable leverage Pro forma QMI leverage of 4.7x at Dec. 31, 2005 down from over 7x at YE ’01 Reduce interest expense Consolidated interest savings estimated at $80M, including the impact of the July 2005 partial tender Enhance liquidity Increase size of revolving credit facility from $75M to $100M 364 day (renewable) Revolver replaced with 5 year Revolver Enhance flexibility Covenant package reflecting improved credit profile Increased ability to pay dividends Optimize debt portfolio Extended maturities to 2011 - 2016 Material portion of prepayable debt (without penalty) Balanced mix of floating rate and fixed rate debt

Revolver replaced with 5 year Revolver Enhance flexibility Covenant package reflecting improved credit profile Increased ability to pay dividends Optimize debt portfolio Extended maturities to Material portion of prepayable debt (without penalty) Balanced mix of floating rate and fixed rate debt.")

13

/ 13 Nationwide Presence and Strategically Clustered Nationwide presence covering key markets offers national advertising and distribution solutions Clustering provides significant cost efficiencies and opportunities for bundled advertising packages 195 Community Newspapers and Specialty Publications 8 Paid Urban Dailies 3 Free Commuter Dailies

14

/ 14 Strong and Established Newspaper Franchise Le Journal de Montréal1 272.7 1,238.9 1964 The Toronto Sun2 199.0 1,910.4 (a) 1971 Le Journal de Québec1 103.4 357.0 1967 The London Free Press1 86.8 248.0 1849 The Edmonton Sun2 73.2 380.0 1978 The Calgary Sun2 66.4 362.4 1980 The Winnipeg Sun2 41.8 250.7 1980 The Ottawa Sun2 50.3 264.8 1988 Total 893.6 5,012.2 Urban Daily Publications Avg. Daily Circulation Weekly Readership Note: Circulation data from Sun Media as of December 2005. Readership based on NADbank 7-day cumulative data. (a) Based on total readership, whereas figures for other newspapers reflect local market only. (average daily circulation and weekly readership in 000’s) Market Position Year Founded 13 Sun Media’s community newspapers are often the only general circulation newspapers published in their respective markets – the majority hold a #1 market position

Based on total readership, whereas figures for other newspapers reflect local market only. (average daily circulation and weekly readership in 000’s) Market Position Year Founded 13 Sun Media’s community newspapers are often the only general circulation newspapers published in their respective markets – the majority hold a #1 market position.")

15

/ 15 Reported revenue and EBITDA have grown at a CAGR of 2.2% and 3.3% (4.3% excluding the impact of the recent start-up of free dailies), respectively, since 1999. Demonstrated Financial Performance CAGR = 3.3% Reported EBITDA Note: Excludes discontinued operations. CAGR = 2.2% Reported Revenue

16

/ 16 Sun Media has continued to deliver industry leading margins despite increased costs from new free dailies and higher raw material costs Maintained Strong Margins * As of January 31, 2006. ** As of November 31, 2005. Notes: Torstar & CanWest - Newspaper segment. GTC - Media segment. Sun Media EBITDA MarginPeer Comparison (LTM) 24,3%

24,3%.")

17

/ 17 Strong and Growing Market Share Market Share* Sun Media is the second largest newspaper publisher in Canada, with a 21.0% national market share (1) All urban daily newspapers rank first or second in their markets (1) Urban Dailies ROP Linage Notes: CNA December reports. * Market share vs. competing broadsheets (including The Globe and Mail). (1) In terms of weekly paid circulation.

. (1) In terms of weekly paid circulation..")

18

/ 18 Strong Market Reception for Free Dailies Source: NADbank 2004 Study; Montreal CMA, Toronto CMA. Leger Marketing Study, Vancouver, October 2005, Sample: 1,000. (1) Internal statistics as of December 31, 2005 24 Hours Toronto has a pick-up rate of 98% 24 heures has a circulation that is 10% higher than Metro’s Confirms Sun Media’s strategy and will translate into robust long-term return on its current investment 24 Hours Toronto 24 heures Montreal 24 Hours Vancouver Circulation249,900136,700128,600 Readership (Daily)308K153K28% vs. 18% by Metro Exclusive Readership46%35%N/A Readership (Adult 18-49)80% 64% Readership (Female)56%49%61% (1)

Internal statistics as of December 31, 2005 24 Hours Toronto has a pick-up rate of 98% 24 heures has a circulation that is 10% higher than Metro’s Confirms Sun Media’s strategy and will translate into robust long-term return on its current investment 24 Hours Toronto 24 heures Montreal 24 Hours Vancouver Circulation249,900136,700128,600 Readership (Daily)308K153K28% vs. 18% by Metro Exclusive Readership46%35%N/A Readership (Adult 18-49)80% 64% Readership (Female)56%49%61% (1).")

19

/ 19 Circulation Strategies Sun Media is implementing various initiatives in order to stimulate circulation and increase revenues Install additional boxes and dealer racks Increase telemarketing to attract new customers and lengthen subscription terms Invest in content and format ("star" columnists) Reduce cover price in specific markets (25¢ in Ottawa and 50¢ in Toronto) Introduce 7-day home delivery for Toronto Sun

Reduce cover price in specific markets (25¢ in Ottawa and 50¢ in Toronto) Introduce 7-day home delivery for Toronto Sun")

20

/ 20 Online Strategy Consumers are increasingly relying on Internet as a primary source of information, contributing to the negative trend in circulation Sun Media is implementing a more formal online strategy to compensate for lower circulation Six Urban Daily websites redesigned in 2005 to reflect vibrant tabloid personality of Urban Dailies In Q4-2005, unique visitors and page views grew 30% $2M of online retail advertising revenues in H2-2005, a new revenue stream at Sun Media Priorities for 2006 Improve sites functionality to increase traffic (videos, blogs, e-mail alerts, etc.) Protect and grow the classified franchise by integrating three verticals (Jobs, Cars, and Real Estate)

Protect and grow the classified franchise by integrating three verticals (Jobs, Cars, and Real Estate)")

22

/ 22 Leading Canadian Cable Operator -1,506K basic subs (475K digital subs) as of Dec. 31 -Fastest growing digital TV provider in Canada (cable or satellite) during LTM -Superior offering including VOD and SVOD Cable TV -638K HSD subs as of Dec. 31 -Fastest growing cable Internet provider in Canada during LTM -Highest speed in its market Internet -Launched in H1-2005 -Hybrid VoIP telephony service -163K subs as of Dec. 31 -Integration of Vidéotron Telecom on January 1 st, 2006 -Strong lift effect for other services Telephony -Will operate under a MVNO strategy (“white label”) utilizing Rogers Wireless’ network -Expected to be launched in H1-2006 -Will complete Vidéotron bundling offer Wireless Quadruple Play Vidéotron continues to lead the industry in new service deployment.

during LTM -Superior offering including VOD and SVOD Cable TV -638K HSD subs as of Dec. 31 -Fastest growing cable Internet provider in Canada during LTM -Highest speed in its market Internet -Launched in H Hybrid VoIP telephony service -163K subs as of Dec. 31 -Integration of Vidéotron Telecom on January 1 st, Strong lift effect for other services Telephony -Will operate under a MVNO strategy ( white label ) utilizing Rogers Wireless’ network -Expected to be launched in H Will complete Vidéotron bundling offer Wireless Quadruple Play Vidéotron continues to lead the industry in new service deployment..")

23

/ 23 Robust new service deployment has led to strong financial performance. Strong Financial Performance CAGR = 17.5% Reported EBITDA Note:Excludes Vidéotron Telecom, which was merged with Vidéotron Ltée on 1/1/06. CAGR = 8.7% Reported Revenue

24

/ 24 Continued Momentum in Q4 2005 Subscriber Results Basic cable: 34,500 net additions – largest quarterly net growth in five years Digital cable: 50,000 net additions – largest quarterly increase since service was launched in 1999 High speed Internet: 50,300 net additions – largest quarterly increase since service was launched in 1998 VoIP telephony: 67,000 net additions Q4 2005 subscriber results continue Vidéotron’s positive momentum and highlight success of bundling strategy.

25

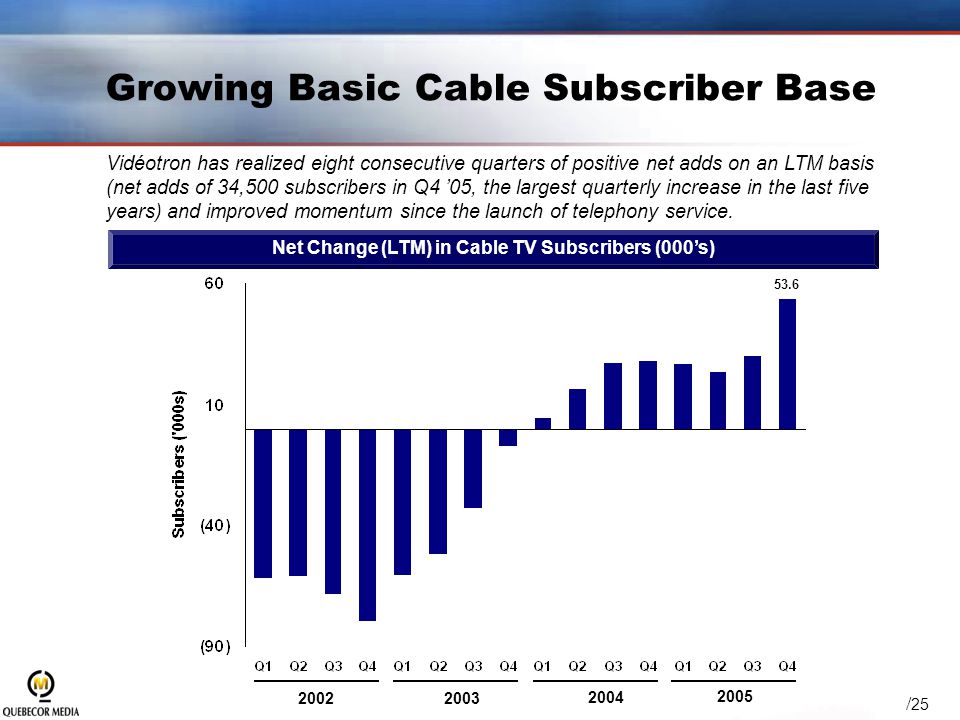

/ 25 2005 Growing Basic Cable Subscriber Base 2002 2003 2004 Net Change (LTM) in Cable TV Subscribers (000’s) Vidéotron has realized eight consecutive quarters of positive net adds on an LTM basis (net adds of 34,500 subscribers in Q4 ’05, the largest quarterly increase in the last five years) and improved momentum since the launch of telephony service. 53.6

26

/ 26 High-Speed Internet CustomersDigital Customers Digital Services Subscriber Growth Vidéotron is the fastest growing Canadian cable digital TV and HSD service provider Cable telephony launch and Bell’s recent anti-piracy measures (new smart cards) have been followed by increased momentum for Vidéotron’s digital services Source: Vidéotron and Company Reports. Vidéotron CAGR = 44% 2004 20022003 2005 Vidéotron CAGR = 28% 2004 20022003 2005

27

/ 27 Strong Residential Telephony Momentum Strong consumer reception 47%+ lift experienced (more than one new product) in Q4 ’05 25% new customers in Q4 ’05 98% taking more than 1 product 68% taking all three (1) Includes some areas of North Shore. Telephony SubscribersRoll-out Progress TerritoryLaunch Date Number of Homes (‘000s) South ShoreJanuary 24300 LavalMarch 29145 West IslandMay 3090 Quebec CityJuly 11268 Rest of MontrealAugust 17825 North Shore (1) November 2457 TotalDec. 31, 20051,685

South ShoreJanuary LavalMarch West IslandMay 3090 Quebec CityJuly Rest of MontrealAugust North Shore (1) November 2457 TotalDec. 31, 20051,685.")

28

/ 28 Vidéotron has realized a strong 8.6% CAGR in its ARPU since 2001. Net Total ARPU Source: Vidéotron (ARPU excludes accounting changes relating to installation revenues starting Q2-04). Growing ARPU CAGR = 8.6% 2002 2003 2004 2001 2005

. Growing ARPU CAGR = 8.6%")

29

/ 29 Bundling Results in Lower Churn (a) Figures presented are monthly averages. 20042005 Monthly Churn (a)

.")

30

Other Businesses Overview

31

/ 31 TVA - Leading Margins and Market Share Industry leading margins As at November 31, 2005 Note: TVA is excluding Sun TV Peer Comparison (LTM) French-language TV Market Share Consistently delivering strong market share despite increased fragmentation – 19 of top 20 shows in Fall 2005 season Source:Audimétrie BBM; Monday - Sunday, 6am to 2am. 2 years + August 29th to December 4th 2005.

32

/ 32 Quebec’s leading Internet portals: General and special interests (Jobboom, Réseaucontact, Autonet, Canoe) In September 2005, launched Micasa.ca, a portal devoted to real estate In the first month of operations, Micasa.ca was the #1 real-estate site in Québec with over 536K unique visitors and 5.4M page views (Source: ComScore MediaMetrix) Canoe is well positioned to take full advantage of the Internet QMI’s value should benefit from Canoe’s impressive growth Canoe: Blossoming in a Growing Market Note: Excluding Progisia

In September 2005, launched Micasa.ca, a portal devoted to real estate In the first month of operations, Micasa.ca was the #1 real-estate site in Québec with over 536K unique visitors and 5.4M page views (Source: ComScore MediaMetrix) Canoe is well positioned to take full advantage of the Internet QMI’s value should benefit from Canoe’s impressive growth Canoe: Blossoming in a Growing Market Note: Excluding Progisia")

33

Financial Highlights

34

/ 34 QMI – Financial Performance

35

/ 35 QMI’s intense focus on profitable growth and cost containment has resulted in significant improvements in EBITDA and Free Cash Flow Current capex programs at QMI and Vidéotron are expected to impact Free Cash Flow in the short-run; significant growth is expected in the future Free Cash Flow Growth Note: Free Cash Flow is defined as EBITDA, less interest expense, less cash taxes, less Capex. Vidéotron Free Cash FlowSun Media Free Cash Flow QMI Consolidated Free Cash Flow

Similar presentations

Indicators Gaborone, Botswana 26-29 October 2004>")