Download presentation

Presentation is loading. Please wait.

1

Mr. Massimo M Beber Senior Tutor College Lecturer in Economics Sidney Sussex College Cambridge CB2 3HU mb65@cam.ac.uk http://people.pwf.cam.ac.uk/mb65 International Political Economy In Historical Perspective FINANCE AND DEVELOPMENT http://people.pwf.cam.ac.uk/mb65/mstir-2011 Institute of Continuing Education - Centre of International Studies

2

A Generational Perspective The evolution of economic thinking can be illustrated through the experience of successive generations: Current undergraduates - “the return of depression economics” (2007-??) Their parents - “the end of history” (1979- 2007); Their grandparents – “the managed economy” (1945-1973)

Their parents - the end of history ( ); Their grandparents – the managed economy ( )")

3

Two Hypotheses on finance Efficient Markets –Finance “oils the wheels” of the market –It speeds up income convergence at lower cost in current consumption –Rational expectations ensure stability –Competition empowers rational expectations Financial Instability –Expectations intrinsically volatile –Volatility creates real economic damage –This damage can be long-lasting (hysteresis) –Prudential regulation must be strict

–Prudential regulation must be strict")

4

“GREED IS GOOD”

5

“YOU STUPID BOY!”

8

FROM INTERMEDIATION TO SECURITIZATION

9

A BRANCH OF NORTHERN ROCK 13 TH SEPTEMBER 2007

11

NY-LEHMAN BROTHERS HQ 15 TH SEPTEMBER 2008

13

PRUDENTIAL RATIOS IN BANKING AssetsLiabilities Liquidity ReservesDeposit Liabilities Government SecuritiesNon-Deposit Liabilities Loans Equity (Shareholders’ wealth.

14

REGULATION: BETWEEN EMH AND FIH Source: Committee of European Banking Supervisors Annual Report 2004.

15

Source: Goldman Sachs (2004).

.")

16

Lt. Gen. Mikhail Kalashnikov with vodka (20 th September 2004) A TOAST TOO EARLY?

A TOAST TOO EARLY")

17

THE ECONOMIC OUTLOOK OECD recovery faster than feared –Governments running large deficits –Businesses re-building stocks –Resilience of growth in non-OECD Asia Large uncertainty factors remain –Long-term state of government finances –Long-term solvency of financial sector –Inflationary expectations

18

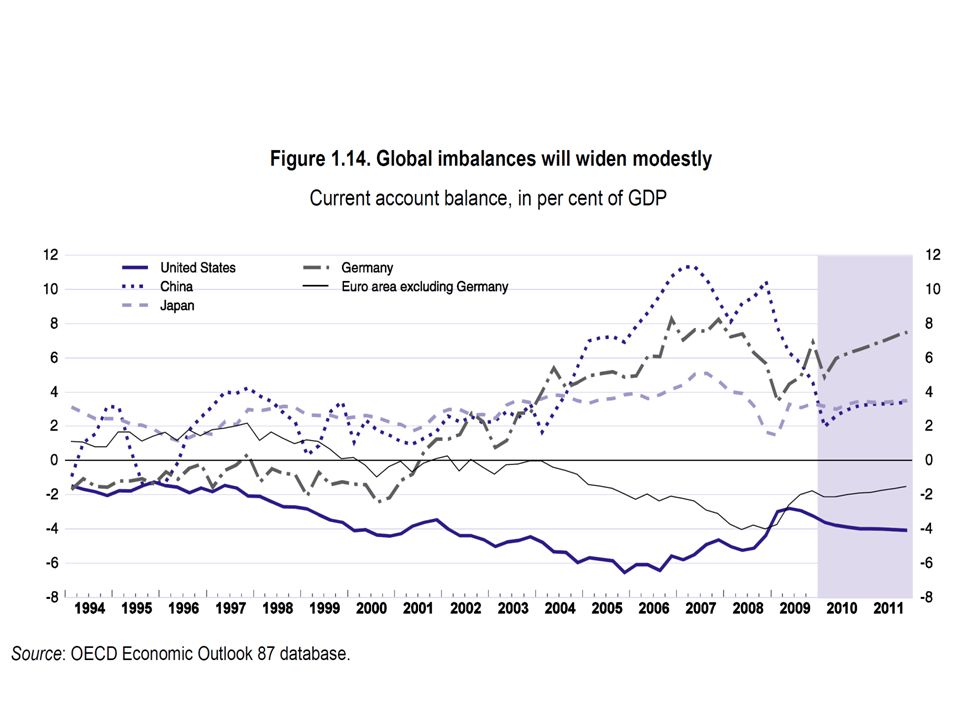

THE POLICY DEBATE (JULY 2010) Fiscal consolidation Mopping up the emergency money Re-regulation of the financial system (Without forgetting) “structural reforms” (employment legislation, competition policy, public services...) And the real question: which is the dog, and which is the tail?

Fiscal consolidation Mopping up the emergency money Re-regulation of the financial system (Without forgetting) structural reforms (employment legislation, competition policy, public services...) And the real question: which is the dog, and which is the tail")

19

CONCLUSIONS The biggest negative shock since the 1930’s Was initially met by a much bolder macroeconomic response Leading to a faster recovery than anticipated But “the markets”, missing “sound finance”, are gunning for Greece and other Eurozone members; Policy-makers may be losing their nerve: Can Keynes still be the “defunct economist... academic scribbler” to enslave them/inspire you/revive public governance?

20

REFERENCES Eatwell, John (2004) “International regulation, risk management, and the creation of instability” (Lecture at the IMF, 1 st October 2004) Eichengreen, Barry and Kevin O’Rourke (2010) “What do the new data tell us?” (vox.eu posting, accessed July 2010)Eichengreen, Barry and Kevin O’Rourke (2010) International Monetary Fund (2010) Global Financial Stability Report (April).International Monetary Fund (2010) OECD (2010) Economic Outlook no. 87 (May): “General Assessment of the Economic Situation”.OECD (2010) Rodrik, Dani and Arvind Subramanian (2008) “Why did financial globalisation disappoint?”Rodrik, Dani and Arvind Subramanian (2008) Obstfeld, Maurice and Kenneth Rogoff (2009) “Global Imbalances and the Financial Crisis: Products of Common Causes”Obstfeld, Maurice and Kenneth Rogoff (2009) VOX.EU “The Global Crisis Debate” (various postings by academic economists and professional policy-makers)VOX.EU

: General Assessment of the Economic Situation .OECD (2010) Rodrik, Dani and Arvind Subramanian (2008) Why did financial globalisation disappoint Rodrik, Dani and Arvind Subramanian (2008) Obstfeld, Maurice and Kenneth Rogoff (2009) Global Imbalances and the Financial Crisis: Products of Common Causes Obstfeld, Maurice and Kenneth Rogoff (2009) VOX.EU The Global Crisis Debate (various postings by academic economists and professional policy-makers)VOX.EU.")

21

OUTPUT VOLATILITY The business cycle in the industrial world simmered down since the early 1980s (USA), or 1990s (Europe) Source: Martin and Rowthorn (2004) “Will Stability Last?”, UBS Global Asset Management. EXCEPTIONALLY “NICE”? The “Non-Inflationary, Consistently Expansionary” 1990’s were explained in terms of smaller shocks, more flexible markets, and better policies.

22

LEVERAGE

23

Source: Obstfeld and Rogoff (2004).

.")

24

GLOBAL INDUSTRIAL PRODUCTION

25

EQUITY PRICES

26

WORLD EXPORTS

27

MONETARY POLICY I: INTEREST RATE and Ben Bernanke. The central bank response has differed globally. Figure 4. Central Bank Discount Rates, Now vs Then (7 country average)

.")

28

MONETARY POLICY II: QE

29

Source: OECD (2010a), p. 8.

, p. 8.")

33

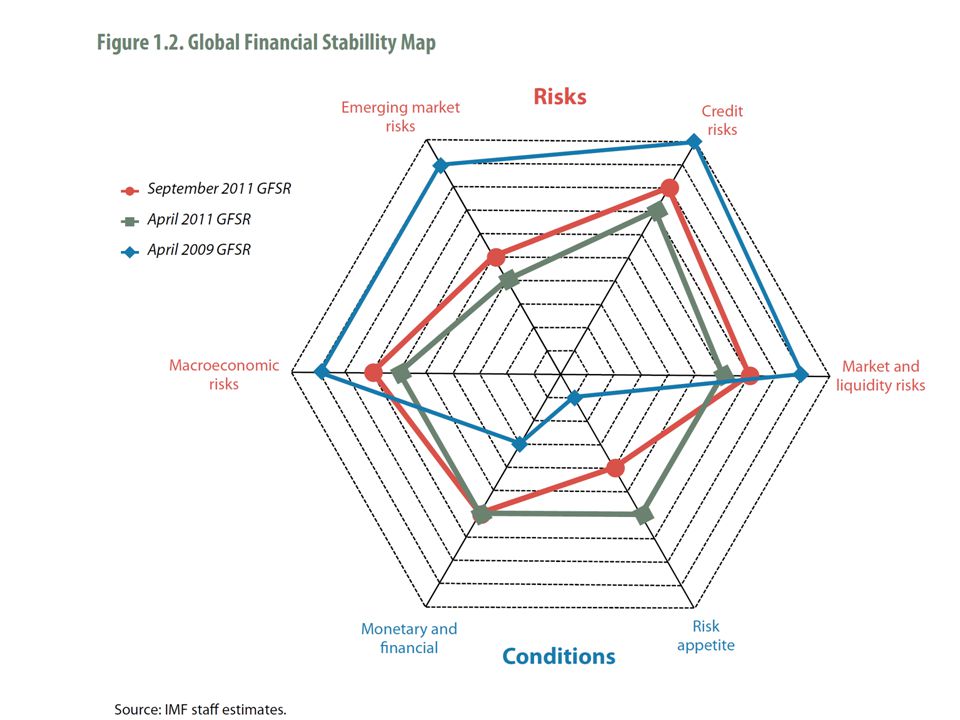

MARKET CONDITIONS AND PERCEIVED RISKS

34

FISCAL POLICY

35

ASSESSING EU SOVEREIGN RISK

36

Caption: Editor to Charles Dickens: "I wish you would make up your mind Mr. Dickens. Was it the best of times or was it the worst of times? It couldn't possibly have been both." © 2002 The New Yorker Collection from cartoonbank.com. All Rights Reserved.

Similar presentations

>")