Download presentation

Presentation is loading. Please wait.

1

Solar Energy in the United States U.S. Trade and Development Agency Business Center November 5, 2009 Scott Hennessey Manager, Climate and Energy Markets Solar Energy Industries Association

2

Introduction to SEIA U.S. National Trade Association for Solar Companies Over 1000 member companies Members include all solar technologies Represent over 80,000 people employed by solar 14 state and regional chapters SEIA’s Mission Expand Markets Remove Market Barriers Strengthen R&D Improve Education and Outreach The Voice of Solar in U.S.

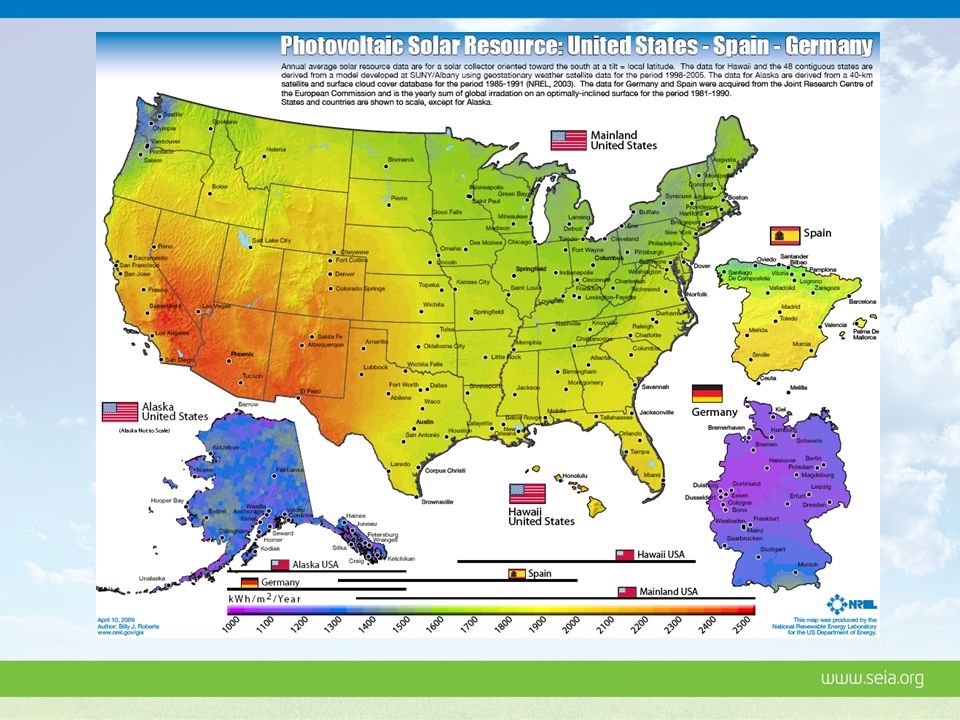

3

PV: Residential Retrofit - 6 kW

4

J&J Skillman, NJ – 505 kW Source: SunPower

5

Solar Water Heating

7

CSP Dish System

8

CSP – Trough System

10

US PV Market - 2008 PV market grew by 71% On-grid PV grew by 81% Off-grid PV grew by 21% Residential +32% Commercial +110% Utility +97% Domestic manufacturing continues to grow Thursday, October 02, 2014 © 2009 SEIA 10 Domestic PV Cell Manufacturing (MW DC ) 20072008pGrowth Production27141453% Capacity41568565% Source: Greentech Media Research/Prometheus Institute

pGrowth Production % Capacity % Source: Greentech Media Research/Prometheus Institute")

11

Grid-Tied PV Capacity Additions by Market Segment Thursday, October 02, 2014 © 2009 SEIA 11 Sources: IREC

12

Grid-Tied PV Capacity (MW) – State by State StateInstalled in 2008Cumulative California178.6530.1 New Jersey22.570.2 Colorado21.635.7 Nevada14.934.2 Hawaii11.315.8 New York7.021.9 Arizona6.425.3 Connecticut5.38.8 Oregon4.77.5 North Carolina4.04.7 Florida0.93.0 Others14.734.6 Total292791 Thursday, October 02, 2014 © 2009 SEIA 12

– State by State StateInstalled in 2008Cumulative California New Jersey Colorado Nevada Hawaii New York Arizona Connecticut Oregon North Carolina Florida Others Total Thursday, October 02, 2014 © 2009 SEIA 12")

13

Solar Water Heating Systems Installed in 2008 Thursday, October 02, 2014 © 2009 SEIA 13 Source: SRCC

14

Solar Installation Forecasts Thursday, October 02, 2014 © 2009 SEIA 14

15

2008 Breakthrough Success Tax Credit Extension – after 17 Votes in Congress –Filibustered 9 times Bailout Bill – October 3 –Extended investment tax credits for 8 years Additional Solar Legislation Introduced –SOLAR Act

16

Investment Tax Credit- SOLAR History: –EPAct 2005: first residential tax credit in 20 years –30% capped at $2,000, only 2 years Expands commercial credit –30%, no cap, only 2 years –Fall 2006, ITC expanded an additional year –Fall 2008- extended by 8 years and expanded Thursday, October 02, 2014 © 2009 SEIA 16

17

Investment Tax Credit- SOLAR What We Got in 2008: –8-year extension of the 30% business ITC –8-year extension of the 30% residential ITC –Total elimination of the residential $ cap for solar electric property –Alternative Minimum Tax (AMT) relief for commercial and residential –Elimination of the public utility exception –Authorized $800 million for clean energy bonds for renewable energy generating facilities, including solar. Thursday, October 02, 2014 © 2009 SEIA 17

18

2008 was a Record Year Last 3 Months Extremely Difficult Good News

19

Creating a Solar President

20

Thursday, October 02, 2014 © 2009 SEIA 20

21

Changes in Washington Obama Administration –Carol Browner – WH Energy and Climate Coordinator** –Dr. Steven Chu – Secretary of Energy –Nancy Sutley – Council on Environmental Quality –Lisa Jackson – Environmental Protection Agency –Cathy Zoi – Assistant Secretary EERE Congress –Waxman replaces Dingell Chairman of House Committee on Energy & Commerce –Markey Subcommittee on Global Warming –Senate – Democrat majority increases, more difficult for Republican filibuster

22

HR 1 American Recovery and Reinvestment Act 19 Provisions to Benefit Solar Companies –Improves existing tax credits Refundability Remove subsidized energy financing penalty –Improves loan guarantee program –Increases government procurement ($25 billion) –Creates new manufacturing tax credits –State energy program funding ($3.1 billion) –Expands CREBS funding ($1.6 billion) –Funds school repair and construction ($53.6 billion) –Funds water treatment repair and construction ($6 billion) –Supports construction of new transmission –Increases access to federal lands –Increases DOE solar appropriation –Improves tax credit for solar water heating –Funds worker training –Increases profile of solar with top political leaders

–Creates new manufacturing tax credits –State energy program funding ($3.1 billion) –Expands CREBS funding ($1.6 billion) –Funds school repair and construction ($53.6 billion) –Funds water treatment repair and construction ($6 billion) –Supports construction of new transmission –Increases access to federal lands –Increases DOE solar appropriation –Improves tax credit for solar water heating –Funds worker training –Increases profile of solar with top political leaders")

23

Understanding ARRA’s implementation Executive Implementation Tax code provisions effective upon enactment Enhanced funding for infrastructure and state programs Agency-specific appropriations Thursday, October 02, 2014 © 2009 SEIA 23

24

Treasury Grant Program Overview –Treasury program that monetizes commercial tax credit –Applicants receive 30% rebate on system costs when placed in service –Projects must begin by 12/31/2010 and be complete by 1/1/2017 Intelligence –Guidance was released by Treasury on July 9 regarding terms and conditions of the program Treasury July 31 Announcement –The Treasury Department released full application instructions for the 30-percent grant –Treasury will review and respond to applications within 60 days –Applicants will receive funds within 5 days of being approved Thursday, October 02, 2014 © 2009 SEIA 24

25

Loan Guarantee Program Overview –Expands existing EPAct title XVII Program Establishes a temporary loan guarantee program at DOE for renewable energy projects, manufacturing facilities, transmission Covers: solar electric and solar thermal, associated manufacturing, transmission projects that “commence construction” by 9/30/2011 –Appropriates $4 billion for credit subsidy cost –Streamline application and approval process Operational by Fall? –Benefits Lowers the cost of financing Help compete for debt equity Provides $60 billion in loan guarantees Thursday, October 02, 2014 © 2009 SEIA 25

26

Loan Guarantee Program Intelligence –Project construction must begin by 9/30/2011 –Two application processes Pre-Qualified Lender Program (PQL) for projects that can be outsourced to private lenders, i.e. commercially proven technologies. (Solicitation at end of July) Direct DOE Process for projects that require direct DOE involvement (Process similar to 1703) –Davis-Bacon Compliance –Most existing 1703 provisions still apply –1703 may be allowed to switch to 1705 –Under 1705, applicants not responsible for credit subsidy cost Latest Updates –July 29 expanded program and issued Innovative Technologies and Commercial Transmission Project Solicitations Thursday, October 02, 2014 © 2009 SEIA 26

Direct DOE Process for projects that require direct DOE involvement (Process similar to 1703) –Davis-Bacon Compliance –Most existing 1703 provisions still apply –1703 may be allowed to switch to 1705 –Under 1705, applicants not responsible for credit subsidy cost Latest Updates –July 29 expanded program and issued Innovative Technologies and Commercial Transmission Project Solicitations Thursday, October 02, 2014 © 2009 SEIA 26.")

27

Manufacturing Tax Credit Overview –Covers new & expanded assets used to manufacture advanced energy property; projects certified by Treasury, in consultation with DOE, through competitive process –Eligibility and weighting of criteria (commercial viability, direct & indirect job creation, geographic distribution, emission reductions) not defined –Program efficacy evaluation not required until 4 years after enactment, early indicators point to OMB taking highly conservative approach Thursday, October 02, 2014 © 2009 SEIA 27

not defined –Program efficacy evaluation not required until 4 years after enactment, early indicators point to OMB taking highly conservative approach Thursday, October 02, 2014 © 2009 SEIA 27")

28

Manufacturing Tax Credit Latest Updates –August 13 The Advanced Energy Manufacturing Tax Credit (MTC) was authorized in Section 1302 of ARRA was authorized –$2.3 billion in ARRA tax credits now available for renewable energy manufacturers –Preliminary applications were due September 16, 2009 –Final applications due October 16, 2009. –January 15, 2010: will have received notification of acceptance or rejection, and approved amount awarded. Credits allocated until the program funding ($2.3 billion) is exhausted. Thursday, October 02, 2014 © 2009 SEIA 28

is exhausted. Thursday, October 02, 2014 © 2009 SEIA 28.")

29

DOE EERE Program Funding Overview –$16.8 billion provided R & D and Deployment activities account has $1.25B for unspecified technologies –Solar Technology Program should be a major beneficiary –Additional $ should leverage new R & D and work already underway State Energy Programs provided $3.1B for RE grants –This amount in addition to $3.2B for EE & Conservation Block Grants –DOE Solar Technology Program should issue guidance on favored / qualifying solar activities Context note: DOE Solar Program annual authorizations fluctuates between $150-200M Thursday, October 02, 2014 © 2009 SEIA 29

30

DOE EERE Program Funding Results-to-date: $117.6 million in Recovery Act funding to accelerate widespread commercialization of solar (additive to normal DOE solar program appropriations) –Photovoltaic Technology Development ($51.5 Million) DOE will expand investment in advanced photovoltaic concepts and high impact technologies, with the aim of making solar energy cost- competitive and strengthen domestic manufacturers –Solar Energy Deployment ($40.5 Million) Projects will focus on non-technical barriers to solar energy deployment, including grid connection, market barriers to solar energy adoption in cities, and shortage of trained solar energy installers –Concentrating Solar Power Research and Development ($25.6 Million) Work will focus on improving the reliability of concentrating solar power technologies and enhancing the capabilities of DOE National Laboratories to provide test and evaluation support to solar industry Thursday, October 02, 2014 © 2009 SEIA 30

–Photovoltaic Technology Development ($51.5 Million) DOE will expand investment in advanced photovoltaic concepts and high impact technologies, with the aim of making solar energy cost- competitive and strengthen domestic manufacturers –Solar Energy Deployment ($40.5 Million) Projects will focus on non-technical barriers to solar energy deployment, including grid connection, market barriers to solar energy adoption in cities, and shortage of trained solar energy installers –Concentrating Solar Power Research and Development ($25.6 Million) Work will focus on improving the reliability of concentrating solar power technologies and enhancing the capabilities of DOE National Laboratories to provide test and evaluation support to solar industry Thursday, October 02, 2014 © 2009 SEIA 30")

31

DOE EERE Program Funding Results-to-date –States submitted plans for SEP grant spending May 12 th –Approval for many states is still pending –SEIA is tracking project announcements CA plan includes $20 million for green job training. Other funds will expand existing RE programs. NJ $15 million for competitive RE grants and $7 million for solar mortgages TN $62 million for 5 MW solar farm and Tennessee Solar Institute CO $7.8 million for rebates, Renewable Energy Financing Program FL $20 million for PV on schools Thursday, October 02, 2014 © 2009 SEIA 31

32

Solar on Federal Property Overview –Most projects funded by GSA were already “pre- selected” But still need to support President’s vision for a “clean energy future” Inclusion of solar in sub-contracts of currently selected GSA projects contemplated House Infrastructure Committee told by GSA that up to 70% of “high performance” facilities will include a solar –March 31, GSA issued list of projects $4.5 billion to convert federal properties to high-performing green facilities $750 million to renovate federal buildings and courthouses $300 million to renovate land ports of entry Thursday, October 02, 2014 © 2009 SEIA 32

33

Thursday, October 02, 2014 © 2009 SEIA 33 State RPS Policies www.dsireusa.orgwww.dsireusa.org / September 2009 State renewable portfolio standard State renewable portfolio goal Solar water heating eligible Extra credit for solar or customer-sited renewables Includes non-renewable alternative resources WA: 15% by 2020* ☼ NV : 25% by 2025* ☼ AZ: 15% by 2025 ☼ NM: 20% by 2020 (IOUs) 10% by 2020 (co-ops) HI: 40% by 2030 ☼ Minimum solar or customer-sited requirement TX: 5,880 MW by 2015 UT: 20% by 2025* ☼ CO: 20% by 2020 (IOUs) 10% by 2020 (co-ops & large munis)* MT: 15% by 2015 ND: 10% by 2015 SD: 10% by 2015 IA: 105 MW MN: 25% by 2025 (Xcel: 30% by 2020) ☼ MO: 15 % by 2021 WI : Varies by utility; 10% by 2015 goal MI: 10% + 1,100 MW by 2015* ☼ OH : 25% by 2025 † ME: 30% by 2000 New RE: 10% by 2017 ☼ NH: 23.8% by 2025 ☼ MA: 15% by 2020 + 1% annual increase (Class I Renewables) RI: 16% by 2020 CT: 23% by 2020 ☼ NY: 24% by 2013 ☼ NJ: 22.5% by 2021 ☼ PA: 18% by 2020 † ☼ MD: 20% by 2022 ☼ DE: 20% by 2019* ☼ DC: 20% by 2020 VA: 15% by 2025* ☼ NC : 12.5% by 2021 (IOUs) 10% by 2018 (co-ops & munis) VT: (1) RE meets any increase in retail sales by 2012; (2) 20% RE & CHP by 2017 29 states & DC have an RPS 6 states have goals KS: 20% by 2020 ☼ OR : 25% by 2025 (large utilities )* 5% - 10% by 2025 (smaller utilities) ☼ IL: 25% by 2025 WV: 25% by 2025* †

10% by 2020 (co-ops) HI: 40% by 2030 ☼ Minimum solar or customer-sited requirement TX: 5,880 MW by 2015 UT: 20% by 2025* ☼ CO: 20% by 2020 (IOUs) 10% by 2020 (co-ops & large munis)* MT: 15% by 2015 ND: 10% by 2015 SD: 10% by 2015 IA: 105 MW MN: 25% by 2025 (Xcel: 30% by 2020) ☼ MO: 15 % by 2021 WI : Varies by utility; 10% by 2015 goal MI: 10% + 1,100 MW by 2015* ☼ OH : 25% by 2025 † ME: 30% by 2000 New RE: 10% by 2017 ☼ NH: 23.8% by 2025 ☼ MA: 15% by % annual increase (Class I Renewables) RI: 16% by 2020 CT: 23% by 2020 ☼ NY: 24% by 2013 ☼ NJ: 22.5% by 2021 ☼ PA: 18% by 2020 † ☼ MD: 20% by 2022 ☼ DE: 20% by 2019* ☼ DC: 20% by 2020 VA: 15% by 2025* ☼ NC : 12.5% by 2021 (IOUs) 10% by 2018 (co-ops & munis) VT: (1) RE meets any increase in retail sales by 2012; (2) 20% RE & CHP by states & DC have an RPS 6 states have goals KS: 20% by 2020 ☼ OR : 25% by 2025 (large utilities )* 5% - 10% by 2025 (smaller utilities) ☼ IL: 25% by 2025 WV: 25% by 2025* †")

34

State RPS Policies with Solar/DG Provisions Thursday, October 02, 2014 © 2009 SEIA 34 State renewable portfolio standard with solar / distributed generation (DG) provision State renewable portfolio goal with solar / distributed generation provision Solar water heating counts toward solar provision WA: double credit for DG NV: 1.5% solar by 2025; 2.4 to 2.45 multiplier for PV UT: 2.4 multiplier for solar AZ: 4.5% DG by 2025 NM: 4% solar-electric by 2020 0.6% DG by 2020 TX: double credit for non-wind (Non-wind goal: 500 MW) CO: 0.8% solar-electric by 2020 MO: 0.3% solar-electric by 2021 MI: triple credit for solar OH: 0. 5% solar by 2025 NC: 0. 2% solar by 2018 MD: 2% solar-electric in 2022 DC: 0.4% solar by 2020; 1.1 multiplier for solar NY: 0.1312% customer-sited by 2013 DE: 2.005% solar PV by 2019; triple credit for PV NH: 0.3% solar-electric by 2014 NJ: 2.12% solar-electric by 2021 PA: 0.5% solar PV by 2020 MA: TBD 16 states & DC have an RPS with solar/DG provisions OR: 20 MW solar PV by 2020; double credit for PV IL: 1. 5% solar PV by 2025 WV: various multipliers www.dsireusa.orgwww.dsireusa.org / September 2009

35

US Market Strong in 2009 California continues to be the dominant market but… More states adding incentives –Virginia adding incentive –Pennsylvania adding incentive –District of Columbia adding incentive –New York adding more incentives –Maryland providing more funding for incentives –Missouri new solar carve-out for RPS –Vermont feed-in tariff Federal incentives stronger than ever

36

2009 Energy Bills Comprehensive Energy Legislation –House passed legislation: American Clean Energy and Security Act (ACES) Renewable Electricity Standard Carbon cap and trade program Transmission legislation And much more –Senate refining legislation now (ACELA) Senate Energy: RES and Transmission Senate EPW: Cap and Trade program

Renewable Electricity Standard Carbon cap and trade program Transmission legislation And much more –Senate refining legislation now (ACELA) Senate Energy: RES and Transmission Senate EPW: Cap and Trade program")

37

2009 Energy Bills “Clean Energy Jobs and American Power Act” S. 1733 Kerry Boxer Investments in Renewable Energy and Energy Efficiency: For investing in energy efficiency and renewable energy, States will receive approx 10% of distributed allowances in 2012 the declining Investments in Advanced Energy Research and Development: 4% of distributed allowances in 2012 (then declining) will be allocated for research on advanced energy technologies, including funding for applied research at “Clean Energy Innovation Centers” at research universities and institutions. Agriculture, Forestry and Renewable Energy: 1% of allowances in 2012 (then declining) will be allocated for investments in agriculture and renewable energy. Building Codes: 0.50% of distributed allowances will be allocated to support implementation of codes to reduce emissions of greenhouse gases from buildings. Worker Assistance and Job Training: 1.5% of distributed allowances in 2012 (then declinging) will be allocated for worker assistance, and to train workers for jobs in the areas of energy efficiency and renewable energy.

will be allocated for research on advanced energy technologies, including funding for applied research at Clean Energy Innovation Centers at research universities and institutions. Agriculture, Forestry and Renewable Energy: 1% of allowances in 2012 (then declining) will be allocated for investments in agriculture and renewable energy. Building Codes: 0.50% of distributed allowances will be allocated to support implementation of codes to reduce emissions of greenhouse gases from buildings. Worker Assistance and Job Training: 1.5% of distributed allowances in 2012 (then declinging) will be allocated for worker assistance, and to train workers for jobs in the areas of energy efficiency and renewable energy..")

38

Thursday, October 02, 2014 © 2009 SEIA 38 2009 Energy Bills ProvisionHouse (ACES)Senate (ACELA) RES6% in 2012, increasing to 20% by 2020 and through 2039 3% in 2011, increasing to 15% by 2021 and through 2039 Carbon Cap and Trade10% of carbon allowances to renewables and EE Approx 10% of allowances to renewables and EE. Additional allowances to deployment fund & agriculture Transmission Not later than 1 year after enactment, FERC shall adopt rules for national electricity grid planning principles Not later than 180 days after enactment, FERC shall publish a rule establishing planning principles for the development of transmission projects. 30 year PPA Authority for the federal gov 20 year PPA30 year PPA Clean Energy BankEstablishes a Clean Energy Deployment Administration

39

Thursday, October 02, 2014 © 2009 SEIA 39 2009 Energy Bills ProvisionHouse (ACES)Senate (ACELA) Green Worker TrainingEstablishes an Energy Efficiency and Renewable Energy Worker Training Fund. Establishes a grant program to award State educational agencies to create or expand energy career academies. Green BuildingsEstablishes a goal to improve the overall energy productivity of the U.S. by at least 2.5% annually by 2012 and to maintain that annual rate of improvement. Establishes a goal to improve the overall energy productivity by at least 2.5% annually by 2012 (measured in GDP per unit of energy input), and to maintain that annual rate of improvement till 2030.

, and to maintain that annual rate of improvement till")

40

Crystal Ball for the Fall and Next Year Energy bill: climate title, Senate floor National Renewable Electricity Standard Cap and Trade bill –Copenhagen Thursday, October 02, 2014 © 2009 SEIA 40

41

Thank You WWW.SEIA.ORG SHENNESSEY@SEIA.ORG

Similar presentations

April 20, 2009.>")