Download presentation

Presentation is loading. Please wait.

2

Copyright(© MTS-2002GG): You are free to use and modify these slides for educational purposes, but please if you improve this material send us your new version. The Land of the Unit Roots Gloria González-Rivera University of California, Riverside and Jesús Gonzalo U. Carlos III de Madrid

3

Why should we care about the existence of unit roots? Growth Forecast The effect of a shock Spurious Regression Asymptotic Results Testing for unit roots Problems of testing for unit roots Structural Breaks

4

Some plots: Inflation

5

Some Plots: Production

6

Some Plots: Dutch stock market index

7

How do we model Growth? Most of the macro-economic variables: GNP, Consumption, Investment,...etc show a growing pattern through time. This pattern is impossible to be captured with our stationary ARMA models: t t How do we describe trends as the following?

8

How do we model Growth? (cont) Two options: An ARMA model with a deterministic trend component (TS=Trend Stationary) A Unit Root process with a drift term (DS=difference stationary) t

Two options: An ARMA model with a deterministic trend component (TS=Trend Stationary) A Unit Root process with a drift term (DS=difference stationary) t.")

9

1. Deterministic time trend 2. Stochastic trend. Unit root processes Random walk with drift

10

How can we relate processes 1. and 2. ? Consider the process:

12

Differencing this type of non-stationary process makes it stationary Warning Non-invertible MA Two differences are needed to achieved stationarity * In general, d-differences are necessary for stationarity

13

Forecasts Deterministic time trend:

14

Forecasts (cont) Unit Root:

Unit Root:")

15

Forecasts: Examples Forecast error (l elements in sum )

")

16

Forecasts: Examples (cont) Example ARIMA(0,1,1)

Example ARIMA(0,1,1)")

17

The Effect of a Shock Transitory shock: Permanent shock: Examples: (1)

")

18

The effect of a shock (cont) The unit impulse response function for the AR(1) process y t = 0.8 y t-1 + t

The unit impulse response function for the AR(1) process y t = 0.8 y t-1 + t")

19

The effect of a shock (cont)

")

20

The Effect of a Shock (cont) (2) (3)

(2) (3)")

21

The Effect of a Shock (cont) Q1: Calculate the effect of a perturbation on a t in the following TS model:

Q1: Calculate the effect of a perturbation on a t in the following TS model:")

22

Spurious Regresions Consider two independent random walks: By construction, there is no relation between x and y. Consider the regression Q2: Which values do you expect the estimates of and will take? What about the R 2 ? You will find the right answer in two more lectures.

23

Some Asymptotic Results Consider the stationary case Asymptotically (CLT) from the previous lecture:

from the previous lecture:")

24

Some asymptotic results (cont) When the asymptotic result is not valid to perform inferences because What to do when ?

When the asymptotic result is not valid to perform inferences because What to do when")

26

In summary, the statistic has a non-standard distribution known as the Dickey-Fuller distribution that is dominated by the chi-squared behavior of the numerator. We can construct a pseudo-t test as

27

This pseudo-t test does not have the usual limiting Gaussian distribution -1.95 5% Dickey-Fuller distribution Normal distribution Reject the unit root too often

28

Some Asymptotic Results (cont) The asymptotic distributions can be written in a more compact way

The asymptotic distributions can be written in a more compact way")

29

Some Asymptotic Results (cont) where W(r) is a Brownian Motion (see the applets from this lecture). A Brownian Motion is defined by the following properties: W(0)=0 W(t) has stationary and independent increments and for all t and s such that for t>s we have W(t)-W(s) is N(0, (t-s)) W(t) is N(0,t) for every t W(t) is sample path continuous.

=0 W(t) has stationary and independent increments and for all t and s such that for t>s we have W(t)-W(s) is N(0, (t-s)) W(t) is N(0,t) for every t W(t) is sample path continuous..")

30

Testing for Unit Roots (DF test) Problem: Tests for unit root are conditional on the presence of deterministic regressors; and tests for the presence of deterministic regressors are conditional on the presence of unit root. Reparametrization of the model Dickey-Fuller consider three models with deterministic regressors:

31

Pseudo-t statistics for : Pseudo-F statistic for :

32

Testing for Unit Roots: A procedure for the DF test 1. Start with a general model 2. Test for trend 3. Estimate 4. Test for drift 5. Estimate

33

Augmented Dickey-Fuller test The previous results are only valid when the error term t is iid. If this is not the case, for instance if t follows a linear process: then it can be proved that it can be proved that we can re-write the DF regression by adding lags of the increments of y t-1 until the error term becomes iid. This solves the problem. The strategy is the same and the A.D are the same as before.

34

Q3: Think on two different ways to choose the right order “p”. Q4: Discuss briefly two reasons why we deal with the null of unit root instead of the null of stationarity. Q5: I am sure you have read and heard many many many times that unit root tests do not have power. What about other tests? Any comments?

35

Structural Breaks versus unit Roots See notes and discussion in class. Unit Roots, Cointegration and Structural Change See Part IV of “Unit Roots, Cointegration and Structural Change” by Maddala and Kim. Cambridge University Press 1998.

36

Applications in Finance

37

Asset price levels (logs) US market

US market")

38

US stock market returns 1980-2000

39

Looking at information in past prices: returns and past returns

40

Histogarm US returns

41

Interest rate USA

42

Histogram of Interest rates in the USA

43

Scatter plot: unveiling information of past interest rate level

44

ACF and PAC for interest rates

45

AC and PAC of interest rate changes

46

Regression for the DF test

48

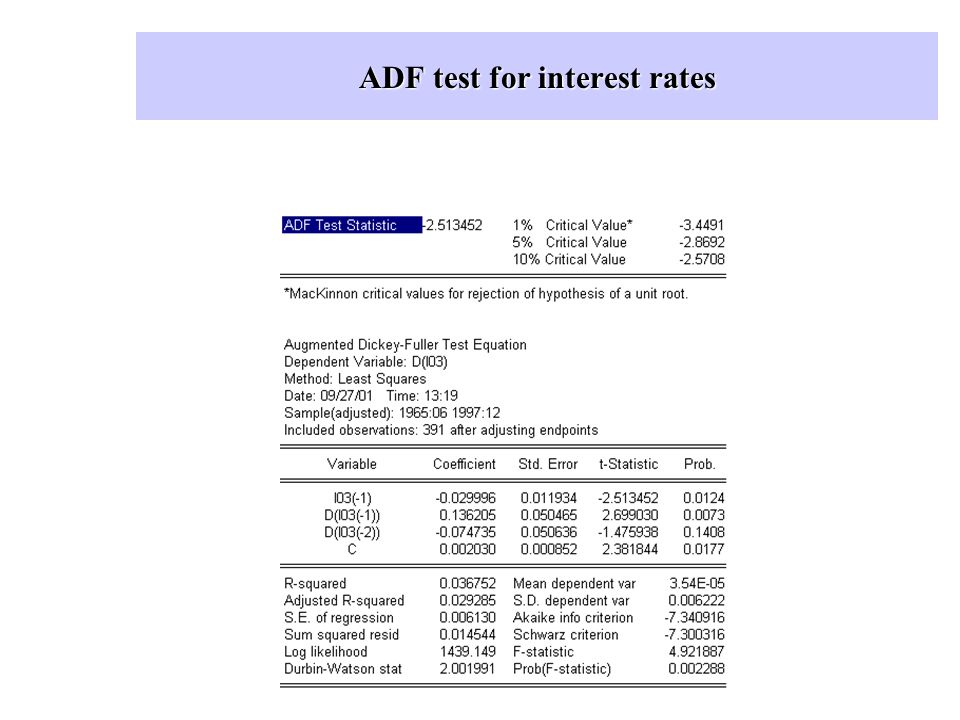

ADF test for interest rates

49

Model fit

Similar presentations

– the constant is the mean AR(p) – the mean is the constant.>")

Material.>")